Building the future of finance at the intersection of Crypto & Web3. 🏛️ I simplify complex markets into high-signal threads. Focus: DeFi Strategy • Web3 Alpha

Joined March 2025

- Tweets 470

- Following 341

- Followers 88

- Likes 479

87 Photos and videos

Pinned Tweet

Most beginners lose opportunities in Web3 because of simple mistakes 👀

Here are 5 mistakes every beginner should avoid 🧵👇

1

1

43

A minor setback for a major comeback. Properties can burn, but the mindset and hustle remain untouched. Glad you’re safe and sound, bro @ahmedxm01. Time to lock in for the next asset! 🚀📈

#MindsetIsEverything #ComebackStronger #Web3Community #KeepGrinding #RiseAbove

1

1

8

Giving up too early Web3 rewards consistency. Keep learning and building.

Web3 is a marathon, not a sprint.

Learn. Build. Stay safe. 🚀

Follow for more beginner-friendly Web3 content from Solana Naija Academy 🇳🇬

1

6

Abdullahi Babangida retweeted

May 28

Last Tuesday, at the Bermuda National Gallery, we celebrated many firsts with @BermudaPremier, our friends at the @bermudamonetary, @investBermuda, and leaders across insurance, tech, and finance.

1st Bitcoin denominated Life insurer, 1st Bermuda IILT (since 2023), 1st BTC audit financials (2024, 2025.)

Stayed tuned…many more firsts to come.

1

3

21

819

As we celebrate Eid al-Adha, I wish Muslims in Katsina state and across Nigeria a blessed Eid filled with love, peace, and happiness.

#EidBlessings Mubarak to you and your family!

#Eid Mubarak#Happy sallah # Islam

1

13

The future belongs to builders, learners & communities ⚡️

Follow for simple Web3 education 🇳🇬

#Solana #Web3 #CryptoNigeria #LearnWeb3 #Superteam

1

2

46

At Solana Naija Academy 🇳🇬

our goal is simple:

Make Web3 education easier for Nigerians.

1

2

16

The future belongs to builders, learners & communities ⚡️

Follow for simple Web3 education 🇳🇬

#Solana #Web3 #CryptoNigeria #LearnWeb3 #Superteam

2

15

Still learning. Still building. Still growing. ⚡️

From Nigeria to the world 🌍

Discipline today. Freedom tomorrow. 🚀

#Web3 #Solana #BuildInPublic #Nigeria #ContentCreator

1

2

29

Abdullahi Babangida retweeted

May 13

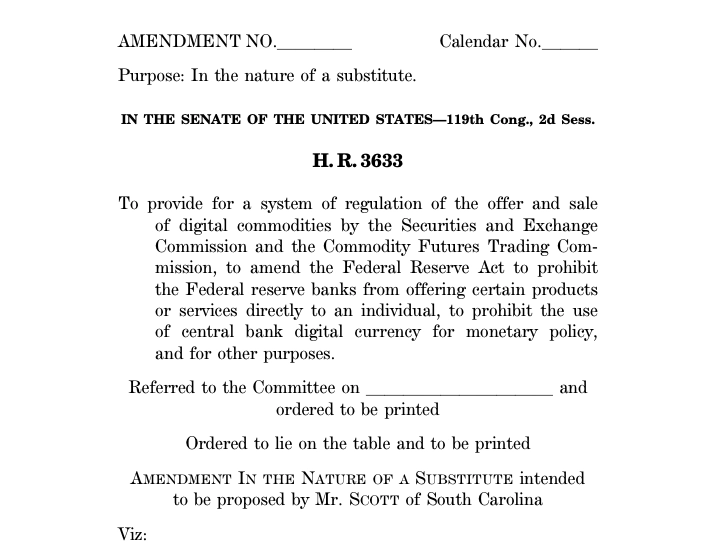

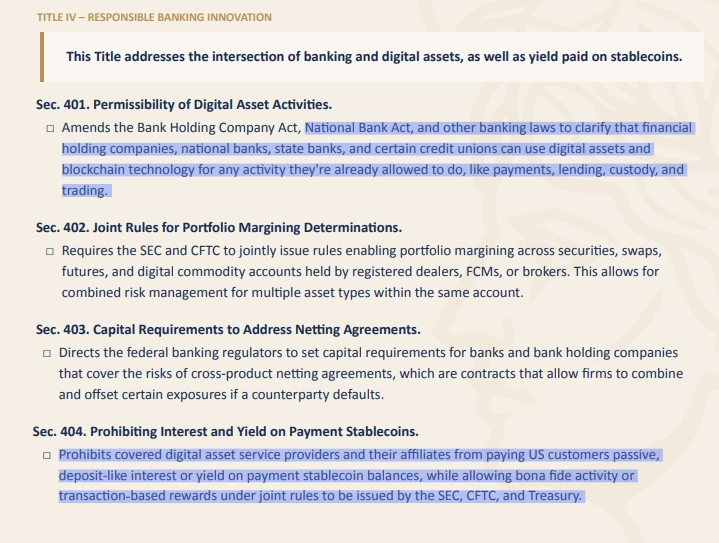

Six banking groups are lobbying hard against the CLARITY Act.

They call it a financial stability risk, while the real reason is business and profits.

Customer deposits fund around 80% of US bank lending.

This is the cheap and easy access to capital banks have.

@ABABankers' own filing against CLARITY act agrees that this could cut consumer, small-business, and agricultural lending by a fifth or more.

In response, Senate Banking Committee added 31 pages through the Tillis-Alsobrooks compromise, which restricts deposit-equivalent yield while permitting activity-based rewards.

But banks are still against it and face a trade-off.

Will they defend their deposit base at the cost of letting Americans earn better yield?

Or will they choose progress over protectionism?

Lobbying like this has slowed new financial infrastructure before, but it has been built anyway.

Whatever is the case, if passed, this regulation will define crypto market structure for decades to come.

I picked the regulated and compliant path for my company four years ago, anticipating this moment.

1

4

21

3,767

Abdullahi Babangida retweeted

Apr 21

“Nigeria’s most active Web3 ecosystem” 😎

The Nigeria Web3 Landscape Report 2025 by @HashedEm is out.

Solana and SuperteamNG show up across almost every section on developers, community, and products, and the numbers are hard to ignore.

Let's get into it 🧵

1/

18

36

138

30,567