1,615 Photos and videos

TickerTapX retweeted

🚨Lucid Trading eval giveaway! 🚨

50K Lucid Flex 🎁

How to enter:

-LIKE

-FOLLOW

-Tag 3 friends!

Make sure you are following me and

@TradingLucid , I will be checking!

50% off ALL lucid accounts with code “maple” 2pp

Ends SATURDAY 6/20

152

115

180

4,150

Jun 15

$KEEL Russell 3000 inclusion confirmed. June 29.

Every passive fund, ETF, and index tracker tied to the Russell 3000 must own KEEL when markets open June 29.

Here's the timeline:

✅ May 22 - Preliminary lists posted

✅ June 8 - Lock-down period began

📅 June 26 - Reconstitution final after market close

🟢 June 29 - Forced buying begins

6

39

187

33,009

TickerTapX retweeted

Jun 15

YES!!!! Elon verklagt jetzt das ZDF!

161

586

7,009

124,192

Jun 15

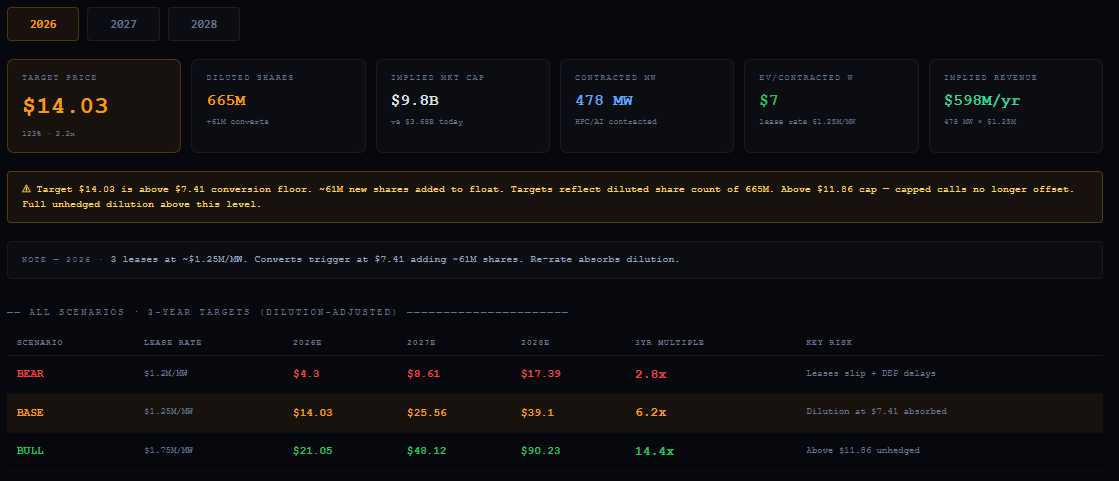

$KEEL Pricing Model V3 rebuilt after community feedback.

V2 had some real problems. @inversormodest1 called them out properly. Fixed with room to improve as we go.

What was wrong in V2:

❌ EV/watt used different denominators $CIFR on contracted MW, KEEL on pipeline GW. Apples to oranges.

❌ Used DGXX $2.75M/MW as the headline comp — that's a 40 MW outlier, not a benchmark.

❌ Price targets didn't reflect diluted share count above $7.41 conversion.

What V3 fixes:

✅ Same denominator for every peer - pipeline MW across the board

✅ CIFR $1.2M/MW used as base lease rate - the honest comp

✅ Dilution-adjusted targets - ~61M new shares reflected above $7.41

✅ Automatic warning when target crosses $7.41 and $11.86

✅ KEEL contracted EV/watt shown as UNDEFINED -because it is, until an 8-K prints

The honest peer picture on pipeline MW:

KEEL: $1.67/watt CIFR: $2.58/watt WULF: $10.00/watt APLD: $21.32/watt

Gap still exists. But it's smaller than V2 suggested — and it only becomes measurable the day contracted MW > 0.

Updated targets (dilution-adjusted) from $6.28:

🔴 Bear: $4.30 → $8.61 → $17.39 (2.8x)

🟡 Base: $14.03 → $25.56 → $39.10 (6.2x)

🟢 Bull: $21.05 → $48.12 → $90.23 (14.4x)

The contract is the event.

Everything else is framework until the 8-K prints.

Link for the updated Model V3 in replies. 👇

$KEEL 🏗️⚡

DYOR. NFA.

5

10

63

19,639

Jun 15

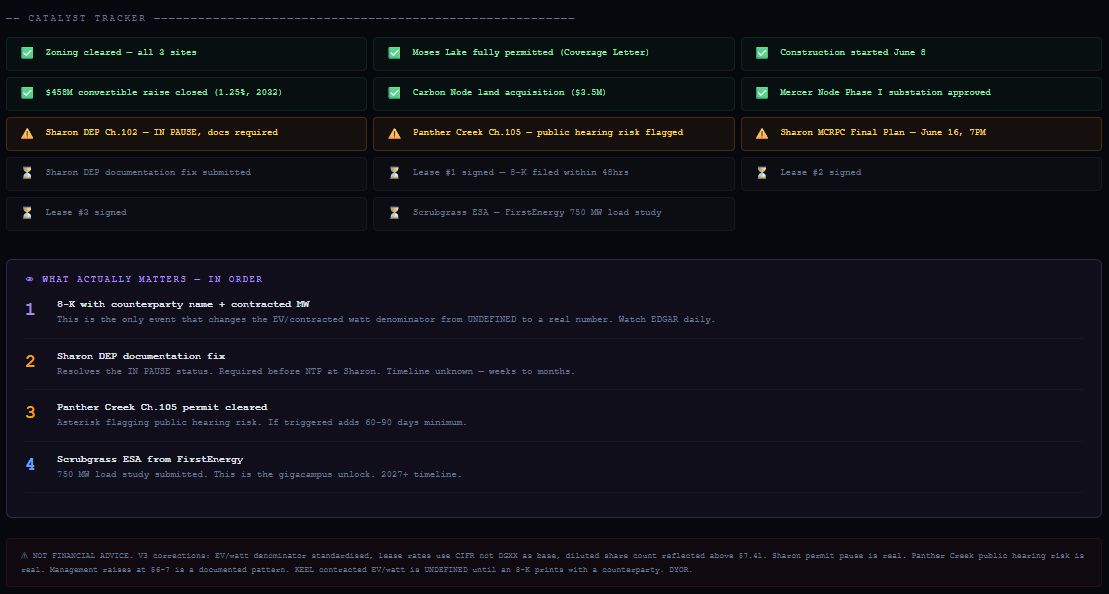

Core corrections:

Denominator fixed - all peers now shown on pipeline MW AND contracted MW separately. KEEL shows UNDEFINED on contracted EV/watt until lease signs. On pipeline EV/watt: KEEL $1.67/w vs CIFR $2.58/w vs WULF $10/w - gap exists but is smaller than V2 suggested.

Lease rate honest range - CIFR $1.2M/MW as base case, not DGXX $2.75M/MW. Toggle to see revenue sensitivity across all rates.

Dilution-adjusted targets - above $7.41 adds ~61M shares to float. Above $11.86 fully unhedged. All targets reflect diluted share count.

Live dilution warning - model flags automatically when target price crosses $7.41 or $11.86.

Updated targets from $6.28 (dilution-adjusted):

1

2

532

Jun 15

3

359

Jun 13

$KEEL - Sharon update. Two tracks. Be honest about both.

The good news - June 16:

Mercer County Planning Commission has scheduled the Final Plan review for Mercer Node Phases II & III this Monday at 7PM.

Not preliminary. Final.

April 26 - Phase I substation approved ✅

April 26 - Phase II/III preliminary approved ✅

June 16 - Final Plan review 🎯

That’s the zoning and land development track. Moving on schedule.

The part worth watching:

The PA DEP Chapter 102 stormwater permit for Sharon is currently flagged:

“IN PAUSE - ACTION REQUIRED. The applicant must complete/rectify documentation.”

This is a separate track from the planning commission. DEP found incomplete documentation and has paused the review until Keel submits corrections. Typically engineering reports, updated stormwater calculations, or a missing study.

Fixable - but not instant.

Why both matter:

Planning commission approval on June 16 doesn’t clear the DEP permit. Both need to be resolved before construction can start at Sharon.

The planning commission track is on schedule. ✅

The DEP permit track needs a documentation fix. ⚠️

Not a dealbreaker. But not something to wave away either.

Panther Creek and Moses Lake remain the cleaner near-term paths to NTP.

Watching June 16 closely. 👀

(Link to the meeting in comments)

$KEEL 🏗️⚡

DYOR. NFA.

2

6

50

3,811

TickerTapX retweeted

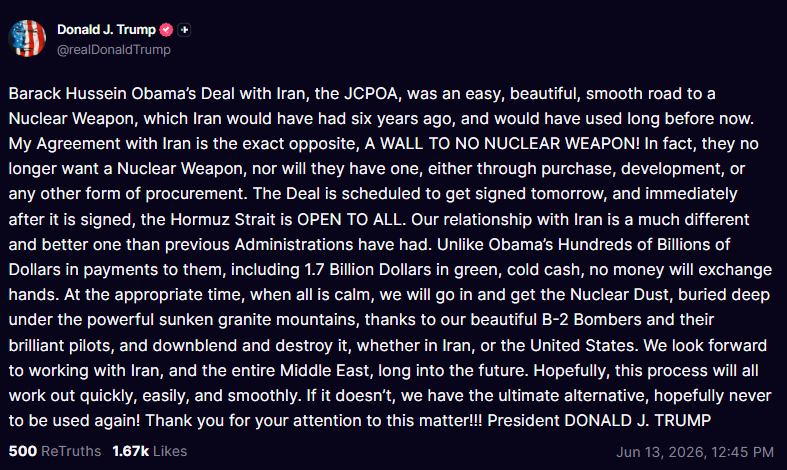

BREAKING: President Trump says a deal with Iran is scheduled to be signed tomorrow, immediately reopening the Strait of Hormuz.

577

799

8,300

1,827,558

Jun 13

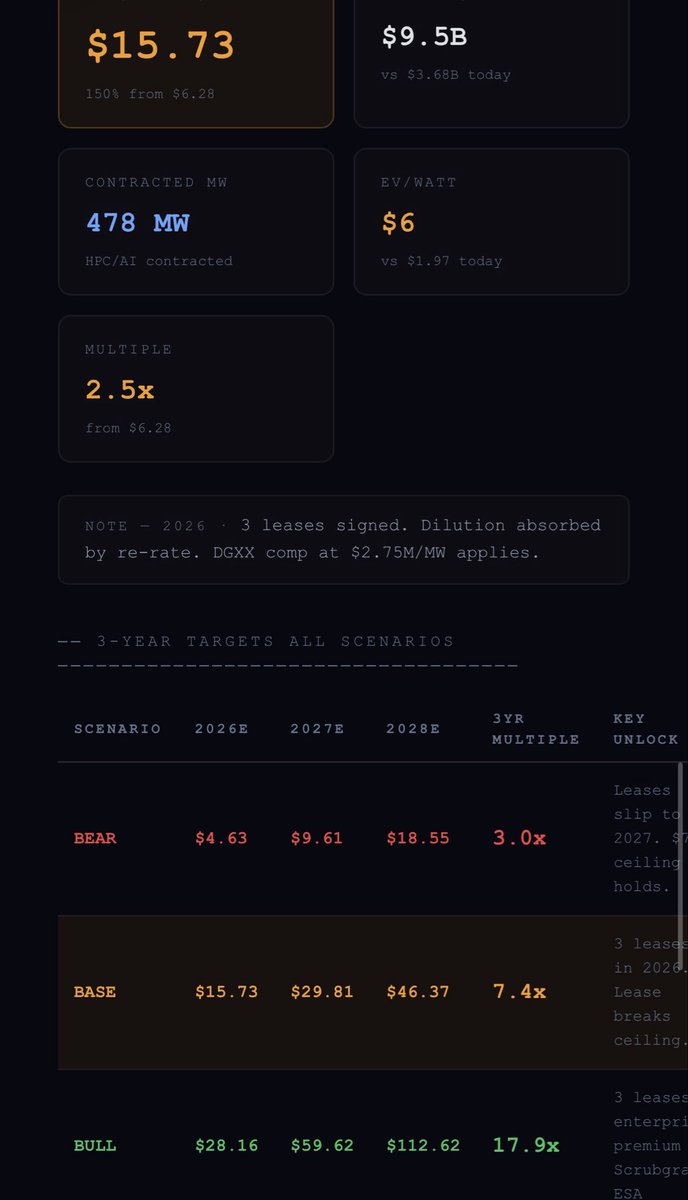

$KEEL - new 3 year price targets:

We just rebuilt the pricing model from scratch.

V2. Updated for everything that’s changed in the last month.

Here’s what’s new:

📊 Baseline updated to $6.28 · $3.68B mkt cap · $983M liquidity

🔵 Full dilution structure - convertible terms, $7.41 conversion, $11.86 cap

⚠️ Live catalyst tracker - Sharon permit pause flagged, Panther Creek Ch.105 risk noted

💰 DGXX revenue comp - $2.75M/MW applied to all 3 Keel sites = $1.31B/yr implied revenue

📉 Risk severity ratings - honest, not cheerleading

The $DGXX comp is the most important update.

DigiPower just proved $2.75M/MW is achievable - the highest rate closed in the sector. Apply that to Keel’s 3 near-term sites:

Panther Creek 350 MW → $962M/yr

Sharon 110 MW → $302M/yr

Moses Lake 18 MW → $49M/yr

Total: $1.31B/yr from 3 sites.

At 8x P/Revenue → $10.5B market cap

At 10x → $13.1B market cap

Today: $3.68B

Updated 3-year targets from $6.28:

🔴 Bear: $4.63 → $9.61 → $18.55 (3.0x)

🟡 Base: $15.73 → $29.81 → $46.37 (7.4x)

🟢 Bull: $28.16 → $59.62 → $112.62 (17.9x)

The risks are real. Dilution starts at $7.41. Sharon permit is paused. Management has raised capital at $6–7 twice now. All of that is in the model.

But so is everything else.

Link in replies. 👇

$KEEL 🏗️⚡

DYOR. NFA.

7

18

175

14,881

Jun 13

6

1,026

TickerTapX retweeted

Jun 12

$ASTS Today there was a liquidity issue. Many stocks have been dislocated and will revert back.

For example, $SATS owns 262m shares of Space X due to the spectrum sale.

The value of those shares at $163 is roughly 42.7b.

The entire market cap of $SATS closed today at 33b so the market is valuing the rest of Echostar at roughly negative 10 billion.

This obviously makes no sense and so I’m going to say that the decline in AST Spacemobile today will revert because something that dislocated the sector occurred and it’s obvious when looking at Echostar today.

8

18

315

31,870

TickerTapX retweeted

Jun 12

45

49

914

103,688

TickerTapX retweeted

Jun 12

Another banger clip from our recent visit with CEO @hashoveride on @keelinfra_ deal timing!!! ✅✅✅ $KEEL

Jun 10

🚨 Hot Off the Press 🚨

CEO @hashoveride joins us for a special podcast covering recent Convertible Note News @keelinfra_ 👀👀👀 $KEEL

youtu.be/nHdEu4CJqDk

1

10

78

7,998

Jun 12

The allocations have been completed for the Space Exploration Technologies Corp. IPO.

The offering price has been set at 135.00 USD.

You have been allocated 1 shares in the offering. LFG @elonmusk ! 🚀

258

TickerTapX retweeted

Jun 11

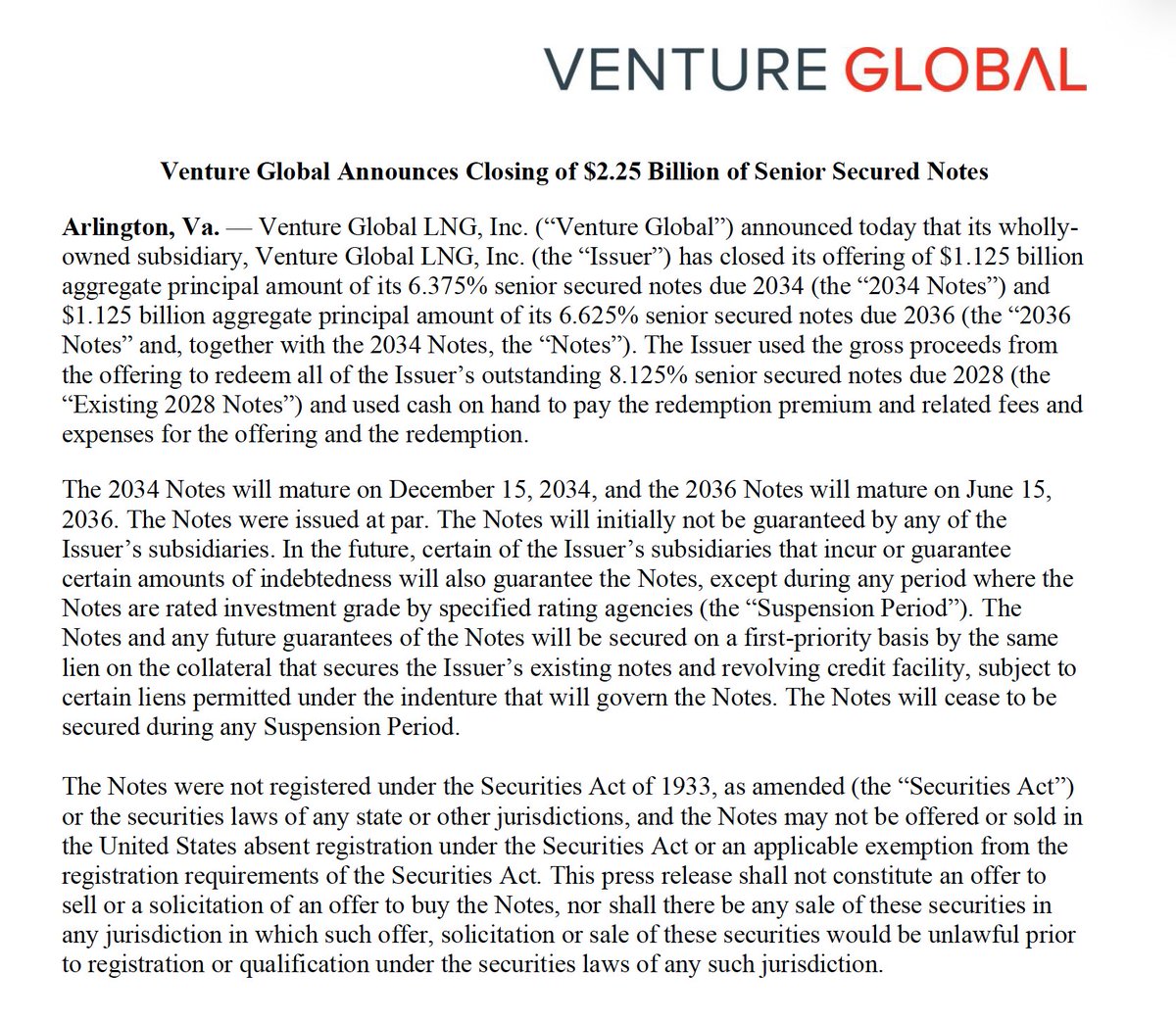

Venture Global Announces Closing of $2.25 Billion of Senior Secured Notes

businesswire.com/news/home/2…

3

13

64

16,573

TickerTapX retweeted

Jun 11

I swung 7 positions overnight 👀

If all 7 are green tomorrow, I will do the biggest giveaway & discount of the year!

Like & Repost ❤️ will select 7 winners!

23

99

214

10,982

TickerTapX retweeted

Jun 11

Building the future of AI takes more than technology.

It takes great people. $APLD

Ready to be part of it?

Apply now: applieddigital.com/careers

3

6

32

2,737

Jun 11

Jun 11

$KEEL - Ben just explained @McnallieM exactly what the $458M raise is for. (Link in the comments)

And it’s not what most people think.

The three near-term sites - Panther Creek, Sharon, Moses Lake - were already fully funded before this raise. That hasn’t changed.

This capital is for Scrubgrass.

Specifically:

•Natural gas lateral engineering and advancement

•Detailed load studies across sites

•Securing expansion capacity beyond 350 MW at Panther Creek

Ben’s words: “For Scrubgrass to advance the nat gas laterals it’s going to cost money. Same with the detailed load studies being conducted across our sites.”

They raised $458M at 1.25% interest - cheaper than a savings account pays - specifically to accelerate the gigacampus that the market isn’t even pricing in yet.

The other things Ben said that matter:

💰 Approaching $1 billion in total liquidity.

Ben called it a “game changer” for how potential customers perceive Keel. A billion dollar balance sheet changes the conversation in lease negotiations.

📉 No ATM equity issued in over 12 months.

“We’ve been really judicious when it comes to issuing equity.” The convertible note concern is valid - but they haven’t been diluting via ATM. That matters.

Ben explicitly stated: “I don’t think we’ve issued a share under the ATM in well over 12 months.”

🏭 Pennsylvania labor - zero concern.

Texas is stretched thin with man camps and imported labor. Pennsylvania has generational skilled tradespeople in ample supply. Welders, pipefitters, carpenters - all local. No premium. No shortage.

🏦 Enterprise customers will pay MORE than hyperscalers.

Ben made the clearest case yet for Sharon’s enterprise demand. Financial firms deploying AI for their own use have a completely different value function - there’s no ceiling on what AI generates for them. No token price compression. Direct relationship with the developer means better lease economics. Ben said enterprises will likely pay “significantly better terms” than hyperscalers.

The closing statement:

“We have the best balance sheet we’ve ever had. The highest confidence we’ve ever had in our assets. The furthest progressed they’ve ever been. This is the most confident we’ve ever been as a team.”

Six months left in 2026.

Three leases in the chamber.

~$1B war chest.

Scrubgrass being funded ahead of schedule.

The market still hasn’t priced any of this in.

$KEEL 🏗️⚡

DYOR. NFA.

1

3

24

1,748