Looking at LOTS of companies and sharing ideas | Research at toffcap.substack.com

Joined August 2020

- Tweets 3,855

- Following 663

- Followers 19,601

- Likes 7,568

1,396 Photos and videos

In an interview a few days ago $TIG 's CEO mentioned:

- that they received multiple competiting bids for the DIS business

- which would allow them to retire ALL debt return cash to shareholders, implying >$180m on $220m EV

- that over the next few weeks we'll get info on the refinancing

- that the rest of the business inflected and is growing again

At $180m for DIS, ~70% of the market cap would be net cash...

...with the rest of the (now growing) operations valued at ~2x...

... o/w Search is booked as held for sale with TIG mentioning formal discussions with potential acquirers back in November.

Meanwhile the share price:

Either something is very off, or 🤷♂️🤷♂️

1

7

13

3,966

A 10x in roughly a year on 2CRSi $AL2SI 🔥

I would not be surprised if this one continues to perform strongly. They could see EUR 2bn revenues in a few years - still a double at 8-10x EV/EBITDA. And given the current crazyness in the markets, who knows what multiple it can get.

But that's it for us. Thanks all.

That's 200% ytd on 2CRSi $AL2SI

Now imagine:

- still 7-8x forward ev/ebitda

- ebitda growing >100% pa

- one of the few Euro AI infra plays

Think about what them poor euro fund managers will do

2

23

7,240

Do yourself a favour and follow my friend @GrumpierBTDay here.

Grossly underfollowed.

He gets grumpier by the day, but tons of interesting flags, massive outperformance and if you think your position sizing is aggressive…

May 20

Been digging into $UMAC, trying to understand why the analyst numbers seem so off compared to CEO Allan's statements and my own guesstimates.

The consensus FY27 revenue is about $50M.

A recent Litchfield Hills report targets $50M top line for FY '27.

Needham has a FY26 estimate of $40M (raised from $25M after Q1) and a "clear path to a $100M run-rate by FY27", which implies Q4 27 at $25 M. Scale that back through the year for a FY target of about $55M to $65M

Roth Capital and Jones Trading give a $25 and $20 PT respectively, but I can't find explicit top line projections. Working backwards I figure they're modeling about $50M in FY27.

CEO Allan Evans, on the other hand, has been pretty consistent across multiple channels (AlphaWolf, the Q1 call, and the White Diamond piece). The targets he keeps repeating:

- 1,000 employees

- 100-120K motors a month

- 140K sqft of factory footprint

- $250M top line FY27 from the Drone Dominance Program alone

This is a $200M discrepancy on the top line between Allan's commentary and analyst targets. Sooooo.... what gives? Either Allan, or the analysts, are off by an order of magnitude. This is the kind of gap worth digging into.

I want to zoom in on the headcount, both because it's something Allan has articulated as an indicator, and because it stood out to me in the CC Shareholder letter.

To give a quick timeline, as reported in the last 10K:

- Mar 31, 2025: 18 employees

- Dec 31, 2025: 81 employees, $4.9M revenue

- Mar 6, 2026: 141 employees, $8.1M revenue

Then on the Q1 shareholder letter and CC we were informed they're at 200 employees, and still hiring.

So, 60 employees in roughly six weeks between the 10k and Q1. 10 employees per week. With about 85 weeks between May 14th the end of '27, 10/week would put us right at the 1000 employees Allan has targeted.

Interesting.

In Q1 they did $230k/employee annualized ($8.1M / 141 * 4), fueled by a jump in B2B revenue from basically 0 to $7.3 million. Don't forget this number includes new hires, trainees, those not yet truly productive. Compare this to Q4 where they did $240k/employee, annualized, at 81 employees.

Headcount increased 75% while rev/employee basically stayed flat. This suggests to me that UMAC is effectively hiring into demand.

What's more, the ratio between 'productive' and 'trainee' only improves from here. I expect we'll see a bit of improvement and then leveling out.

Side note: they're investing in more factory automation equipment, which should eventually boost rev/employee. I don't think $300k/ is out of the question down the road. Not using that number though.

Putting that all together, if we get to 1000 employees by end of '27 and pencil in $250k/employee, we get $250M top line. Right in line with what Allan has targeted.

Interesting.

So the pace of hiring is on track, and Allan's top line is a reasonable target if both hiring keeps pace and Allan can put 1000 people to work at a $250k annualized rate.

Are there structural barriers to hiring? No, not at all. A recent Bizumentary highlighted how the job requirements can all be taught on site. The factory has a notable contingent of former food service workers. Labor pool is effectively infinite.

The bigger question is do they have the facilities to support 1000 people?

They currently have 62k sqft of space across 5 facilities in Orlando. Let's look at the timeline:

- Jun 4 '25: 17K sqft motor center

- Oct 30 '25: 25K sqft fulfillment center

- Dec 10 '25: 9.1K sqft HQ

- Dec 15 '25: 4.5K sqft headset production

As of the Q1 CC, Allan intends to expand to 100k sqft by the end of Q2. More expansion is expected by Q4, which puts that 140k sqft '27 target clearly in view.

So hiring isn't a constraint, nor are facilities.

Equipment doesn't look like it's going to be a constraint, either. Note 6 on the most recent 10Q indicates there's 1.3M of equipment related to motor production to be delivered in Q2. This is against 2.5M of currently deployed equipment. I think we can expect that to continue to scale through the Qs.

So we've got what's essentially a doubling of manufacturing related facilities, a 50% bump in equipment related capacity, and a steady pace of hiring to put it all to use. All in the next 3 months... let alone the next 12.

What about raw materials? Considering this is a factory environment, we can use materials margins to cross-check our headcount based projections, and measure both against Allan's statements.

As of Q1, UMAC had $12M of raw materials and $13.5M of prepaid deposits. This is an expansion from the $4.2M of raw materials and $9.7M of prepaid deposits held in Q4. That's $12M of net inflow in Q1. Subsequent to Q1, UMAC placed an order for $75M of raw materials, to be delivered in Q3.

Let's carry that forward.

As of Q1, GM was 32.8%, but long term run rate is expected to be 40%. Of this, most, but not all, will be materials.

The 10Q states COGS includes "inventory costs, which includes an allocation for labor and rent for our manufactured products, direct packaging costs, and production related depreciation, if any." in addition to "certain shipping and other direct product costs including tariffs".

For Q1, COGS came out to $5.4M. Recall this was on a raw inventory of $4.2M as of Dec.

Let's hand-wave and say that labor, packaging, shipping, and tariffs eat up 30% of COGS, and that materials are the remaining 70%. This will produce a conservative revenue number vs if we give raw materials a heavier weight.

At 70% attribution, raw material contributed $3.8M, which means there's a materials-to-revenue ratio of 54%.

That would project our already-placed materials PO of $75M into $139M of top line alone.

This material should arrive

That's *far* closer to Allan's $250M target than to the consensus $50M.

Here's where it gets interesting: Allan has indicated that the $75M raw materials order is just the first of two waves. Per the April 6th AlphaWolf interview:

"And you know, in a in a week or two, we're going to have to order another 60 to 80 million dollars worth of raw material. Okay, right? And then 6 months after that, we're going to have to order 100 to 150 million dollars of raw material."

Then, on May 5th, 4 weeks later (a little delayed), the $75M order came through. The timeline places the next big order some time around December.

So for FY '26, we've got $25M of current inventory and prepaids, and $75M of new orders. That's $100M of raw inventory bought and paid for. A cold hard fact. With our assumed margins that gives us $185M top line.

Even if you totally ignore Allan's statements about another big order, that blows the consensus '26 and '27 numbers out of the water.

What would the next $100M to $150M of raw materials add? Well, at 54% revenue contribution that'd be another $185M to $277M, putting combined '26 and '27 revenue at $370M to $460M.

👏 Against 👏 $50M 👏 full 👏 year 👏 '27 👏 top 👏 line 👏 estimates👏 (did I emoji right?)

Reminder that Needham targeted $40M for FY '26, and a 'run rate $100M' end of '27. Litchfield projects $35.5M top line '26 and $50M '27.

Neither of these are even in the ballpark of what we can project based on already placed materials orders.

What's UMAC trading at today?

$685M MCAP, with $220M of cash and $60M of short term investments gives us an EV of $400M.

On our already-committed materials, and assumed $180M top line that creates, that's just beyond 2xNTM EV/Sales.

That's cheap, especially considering the defense tailwinds and supply chain mandates, let alone the DJI ban and thus domestic commercial market vacuum.

I call that optionality.

So I'm left scratching my head, wondering what these analysts are thinking, but content to keep buying.

2

2

22

11,181

$EVC might perhaps be your bias test of the year peeps.

May 19

Entravision $EVC math is pretty simple:

Media assets don't earn much, but thanks to the spectrum & FCC dereg, there's a realistic path to $500m of value

Meanwhile, Smadex, against the full $800m EV, is priced at a fraction of peers and growing faster.

Value guys afraid to buy because "they missed it" and widow of the former CEO has been selling

But there's zero street coverage and the growth guys barely know this exists (yet)

2

31

11,056

The one & only @MikeFritzell talks Korea(n) this week in KEDM!

The new KEDM is live!

This week, in collaboration with @MikeFritzell, we dig into the Korean stock market and he also shared a few value names he is watching.

Plus, as usual, plenty of actionable event-driven setups. Enjoy

1

1

6

5,539

If you're reading this in a Q1 fund letter:

"We have been actively repositioning the portfolio in 2025 in anticipation of AI-driven disruption to legacy enterprise and SaaS [...]. Taiwan remains our largest country exposure"

but the fund's Q1 return was 1.0% (!!)...

wtf did these people do??

3

1

27

7,818

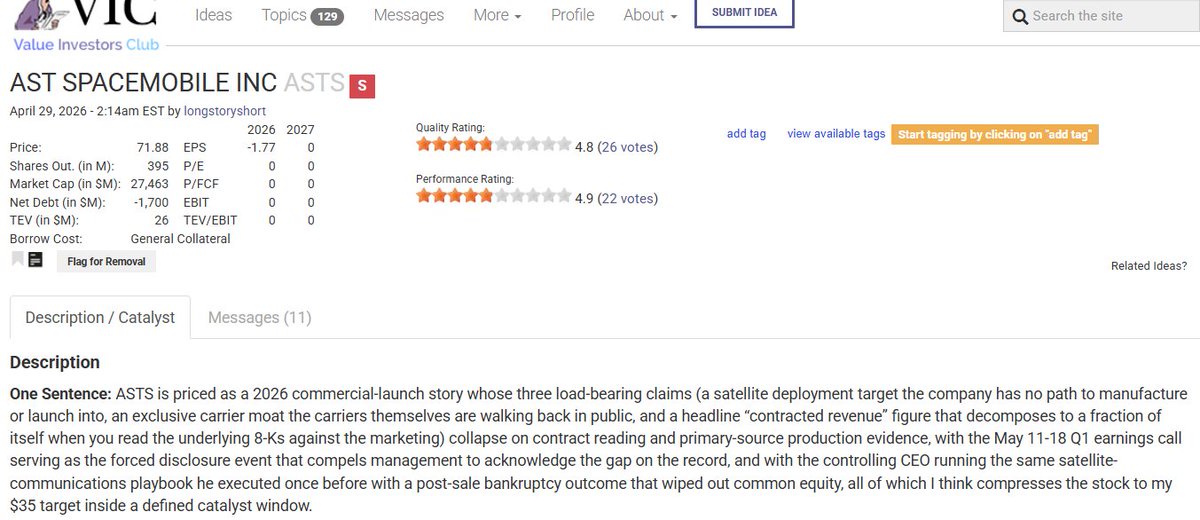

Every now and then I read write-ups where I agree on the thesis but think it would be insane to act on it.

Like $ASTS 's recent short pitch on VIC.

Sure execution is important, but 90% of the 'valuation' here is storytelling.

So what if they'll miss a quarter or two. Look at the projections. The base for valuation here is not fundamentals, it's faith.

Missing a few quarters is not going to break the thesis at all. That won't be enough to break believers' faith.

Because that's what is needed to break such stories. Faith needs to be crushed.

And that can take a long ass time. And what if in the meantime they'll beat a quarter?

5

16

4,510