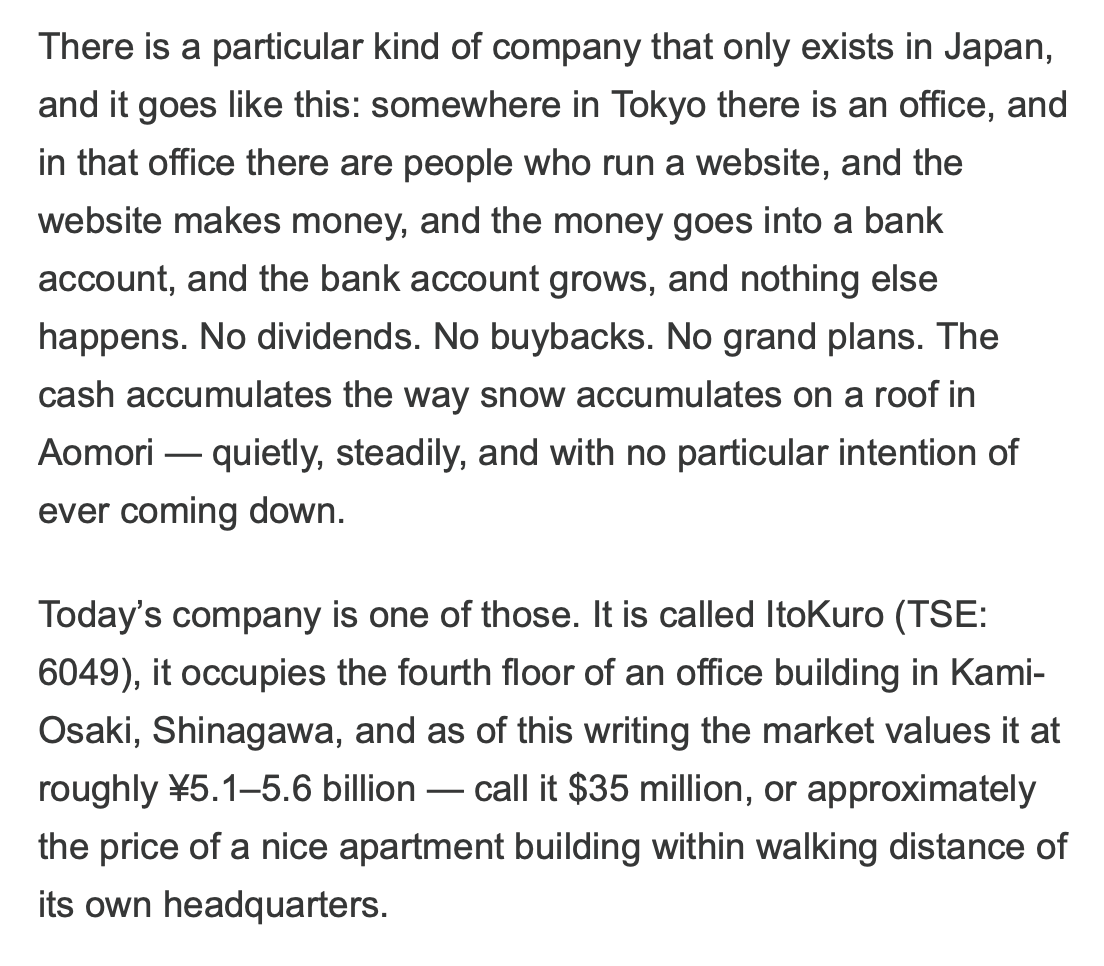

Japanese stocks are the last great deep value trade on earth. Rock solid balance sheets. Monster cash flows. Dirt cheap prices. I find them and buy them

Joined March 2026

- Tweets 306

- Following 9

- Followers 33,935

- Likes 276

27 Photos and videos

Pinned Tweet

Japanese stocks are the last great deep value trade on earth. Rock solid balance sheets. Monster cash flows. Dirt cheap prices. I find them, trade them, and do it all over again. Follow for the best deep value plays in Japan nobody else is talking about.

76

242

6,771

1,877,656

I am drinking a Sapporo at a yakitori place in the East Village and the man next to me has been quietly eating chicken hearts for 40 minutes and we have not spoken once and this is the closest I have felt to my portfolio in months. There is a kind of investing that requires you to be loud and there is a kind of investing that requires you to be the man eating chicken hearts. I do the second kind.

I own 23 Japanese small-caps and I have spoken about them out loud to maybe four people in my life. The beer is cold. The yakitori is on its fifth course. The chef has not smiled but he has not frowned either. He is performing the same six motions he has performed every night for what looks like 30 years. Behind him on the wall is a small framed photograph of a man I assume is his father doing the same six motions in 1978.

This is the entire Japanese small-cap thesis. A company has been making the same gearbox, the same valve, the same precision screw for 60 years. Three generations of the same family have run it. They have $200 million in cash and a $180 million market cap. They will not buy back stock because their grandfather did not buy back stock.

But the TSE wrote them a letter and the chairman’s son went to business school in Boston and the son has opinions about ROE that the father does not share and the son will inherit in four years. That is the trade. It is the slowest, most patient, most boring trade in the world and it is also, when it works, one of the best risk-adjusted trades you will ever make in your life.

The beer is finished. I order another. The man next to me has moved on to skin. I have learned more about Japan from sitting in rooms where nobody talks to me than I learned from any book. There is a quality of attention you can only develop in silence. The yen is 158. My positions are up modestly. My patience is intact. The chef refills the man’s beer without being asked.

They have a relationship that does not require language. That is also Japan. That is also the trade. You hold the thing long enough that you and the thing develop a relationship that does not require language. You stop checking. You stop hoping. You just own it, the way the chef owns his motions, the way the man owns his stool, the way the family owns the gearbox factory in Nagoya that has not had a down year since 1974. I pay the bill in cash. I walk home. I do not check my portfolio.

There is nothing to check. There is only the slow accumulation of evidence that the country is changing and the people who were paying attention will be the ones who benefit. I was paying attention. I am paying attention. The beer was incredible.

3

28

3,301

Jun 13

SpaceX at $200 billion is the Nifty Fifty trade of 2026. Same setup. Same vibe. Same outcome. In 1972 every fund manager in America owned the same 50 “one-decision stocks” — Polaroid, Xerox, Avon, Kodak. Quality businesses at impossible multiples that everyone agreed you simply had to own. The next decade those names returned roughly nothing while a basket of obscure cheap stocks compounded at 20% a year and built generational wealth for the few weirdos who bought them. Walter Schloss ran net-nets in the dust of those years and beat the S&P by an absurd margin. Buffett shut the partnership in 1969 because there was nothing left to buy at the top — then quietly accumulated boring small-caps through the bear market.

The pattern is the entire history of markets compressed into one rule: when the consensus trade is generational, the actual generational trade is in the corner nobody is looking at. SpaceX is generational. So was Polaroid. The IPO will price. Retail will pile in. The lockup will unwind. The story will fracture. And while that movie plays out, there is a list of 60-something American companies right now trading below their net current asset value. Cash and inventory minus all liabilities, on sale. Some of them have buildings worth more than the entire market cap and they show them on the books at 1968 cost. Nobody is talking about them because there is nothing to say. They’re just cheap. Ben Graham wrote about this trade in 1934. It still works. It works because every cycle creates a new SpaceX and a new generation of investors who’d rather own the story than own the math. You don’t have to short the bubble. You just have to not be in it. Put the IPO money in five net-nets and check back in 2030. The Nifty Fifty crowd is still apologizing for 1972. The Schloss crowd retired.

3

2

47

5,277

Jun 13

they’re buying SpaceX. I’m buying a Japanese auto-parts maker with more cash than its market cap, run by a 78-year-old who hasn’t smiled since 1991. we are not the same.

3

3

102

7,593

Jun 11

Tigers Polymer (TYO: 4231) — a textbook Japanese net-net hiding in plain sight.

Osaka-based maker of industrial hoses and rubber parts, in business since 1938. Profitable every year since 1985 except one tiny loss in 2009.

Mkt cap: ¥20B

Enterprise value: ~¥3B — cash and securities cover ~85% of the market cap

P/E: 8x

Dividend yield: 3.8%

Debt/equity: 4%

Most profits come from its US plant in Ohio, not Japan. Up ~50% in a year and still trading near liquidation value. Graham math still works in Tokyo.

2

3

32

2,958

Jun 11

Japan teaches you what time actually is. I bought a small industrial in Nagoya in 2021 at 0.4x book. It went to 0.35x. It stayed there for 14 months. I bought more. It went to 0.42x. I bought more. It is now at 0.71x and pays a 4% dividend in yen and the company has been making the same gearbox for 73 years. There are 3,800 listed companies in Japan and roughly half of them trade below book. Half. In the third largest economy on earth. Companies sitting on more cash than their entire market cap, run by 71-year-old presidents who view shareholder returns as a Western affectation they will get to eventually. The TSE wrote a letter in 2023 asking these companies to please consider the concept of capital efficiency and the letter is slowly working. Slowly. The way the tide comes in. You can watch it if you have the patience but you cannot rush it. I have 23 positions. The average holding period is now four years. I have sold three companies in that span. I have not panicked once because panicking requires believing the price means something, and the price in Japanese small-caps means nothing for years at a time until suddenly it means everything for six months. Activists are showing up. Buybacks are getting announced. The yen is 158 and my cost basis keeps getting cheaper in real terms, which I have decided is a feature. There is no urgency. There is no catalyst tomorrow. There is only the slow accumulation of evidence that the country is changing and the market hasn’t fully figured it out yet. By the time it does I will own the things you cannot buy at the prices I paid. That is the entire game. Japan is not a trade. Japan is a way of holding.

3

1

67

5,141

Jun 10

Wrote up a new Japanese cheap stock. Check it out. Link in bio.

3

21

3,582

Jun 10

Met a Japanese man at a vending machine buying the same canned coffee he’s bought every day since 1987

Wore a suit older than me

Asked what he does

“Family business,” he mumbled

Asked how big

“We make a tiny spring. It’s in every toilet seat that warms your butt. Globally.”

I laughed

He did not

Forty years profitable. Never raised a price. Never fired a soul. CEO bikes to work and the company owns three buildings it forgot about.

So much cash in the bank they literally can’t spend it fast enough

Trades at 0.3x book because investor relations is one guy named Tanaka who refuses to answer the phone

The whole company is run like a guy who still uses a flip phone and a fax machine

Because he does

Bought it before the can dropped

11

12

481

31,122

These are the books on my desk right now. Murakami Fund’s old letters, printed out and stapled. A 2003 Marc Faber report on Japan that I bought used on eBay for $40. Ben Graham’s Security Analysis open to the chapter on net-nets that everyone says no longer applies. It still applies. It applies in Osaka. There’s a printed copy of TSE’s 2023 governance letter — the one demanding companies trading below book either fix it or explain themselves — and I’ve underlined the same paragraph in three different colors over 18 months. There’s a Japanese-English financial dictionary with the cover falling off. There’s a binder labeled “Net-Nets, Sapporo to Fukuoka” with 47 tabs and only one of them has ever been wrong. Every name in there trades at less than the cash and securities on its balance sheet minus all liabilities. Some of them have been doing it for 30 years. Some of them have buildings in Ginza that are worth more than the entire market cap and they show them on the books at 1962 acquisition cost. There is no analyst coverage of any of these companies in English. There is barely any in Japanese. I have a Google Sheet with 311 names on it that I update by hand from filings I read with three browser tabs of translation software running. The yen is 158. My cost basis in real terms keeps falling. I have not sold a Japanese stock in four years. This is not a thesis. This is a vocation.

4

1

23

4,713

I have, in the back of my closet, 14 identical dark suits. They are charcoal gray, single-breasted, two-button, with notch lapels and a slight Japanese cut through the shoulders that an American tailor pointed out to me, once, in 2019, with an expression I have come to recognize as the specific facial composition of a man who is about to ask a question he does not want the answer to. I bought the first one in Tokyo, in 2013, at a small shop in Aoyama that a Japanese friend recommended to me on the condition that I never reveal the name of the shop to anyone, a condition I have honored for 13 years and will honor here. I bought the next 13 over the course of 11 trips, one or two per visit, from the same shop, from the same tailor, who is now in his late seventies and who, on my last visit, mentioned, in passing, that I am one of three foreign customers he has ever served, and that he is no longer accepting new ones, and that when he closes the shop, which he intends to do in 2027, the suits will not be replaceable by any tailor anywhere in the world, a fact I have not yet emotionally absorbed and may not, in any meaningful sense, ever.

I wear the suits only to Japanese shareholder meetings, and only in Japan. I do not wear them on the flights over. I pack them in a garment bag, fold them according to a method the tailor taught me on my second visit, and unpack them in my hotel room the night before the meeting, where I hang them on a wooden hanger I also brought from Tokyo, because the plastic hangers in Western hotels are, I have determined, an insult to the cut. I wear the suit. I attend the meeting. I bow at the angles I have practiced. I return to the hotel. I remove the suit. I hang it in the garment bag. I do not wear it again until the next meeting, which may be six months later, which may be two years later, which may, in some cases, be a meeting that has not yet been scheduled and that I am, in some part of my mind, simply waiting for.

I have tried, on three separate occasions, to wear one of the suits in the United States. The first time was in 2017, to a wedding. I noticed, halfway through the ceremony, that something was wrong, and I could not identify what. The suit fit. The suit was correct. The suit was, in every objective measure, more elegantly tailored than any other suit in the room. And yet I felt, with a certainty I cannot explain, that I was wearing a costume. I did not understand it at the time. I attributed it to the wedding. I tried again, in 2019, to a funeral, and the same feeling returned, and again I did not understand it. I tried a third time, in 2022, to a board dinner at a public company I had a small position in, and halfway through the entree, I excused myself, returned to the hotel, changed into a different suit, and returned to dinner, and I have not, since that night, attempted it again.

The suits feel wrong in American light. I have, over the years, come to believe this is a real phenomenon and not a psychological one. The light in Japan, in the small regional cities where the shareholder meetings happen, is filtered through air that has a different quality than American air, an observation I cannot defend scientifically but which I will go to my grave insisting on, and the suits were made for that light, and they were made by a man who has lived his entire life under that light, and they cannot be worn under any other. They look identical in a photograph. They feel completely different on a body.

4

2

219

40,243

This is my quant

Jun 1

It most definitely was not. I would never have forgotten my drugs.

1

9

4,177

I’ve been doing quiet “field research” in Soapland since 2022.

Call it Japanese small-cap intelligence gathering with happy endings.

Last quarter I hit a discreet spot in Kabukicho for the usual ¥52,000 course.

My therapist that night had the tired eyes of someone who’d just spent three hours power-washing the stress off a 58-year-old plant manager from a niche auto-parts maker in Aichi.

Between the mat wash and the “special massage,” she casually dropped that the old man was losing sleep over mounting China exposure, a new Chinese competitor eating 18% share, and a factory expansion in Thailand that was already 40% over budget with zero orders yet.

She even knew the exact model line bleeding cash.

I left, ran every 10-K equivalent I could find at 2 a.m., discovered the company was trading at 0.6x book with net cash > market cap and literally zero English sell-side coverage.

Took a 1.4% position in the obscure piston-ring supplier nobody’s heard of.

Eleven weeks later it popped 47% on a surprise buyback guidance cut that confirmed every bubble-sud detail.

Public Japan is still kabuki.

Real color only comes out when the suit comes off and the soap goes on.

Salarymen don’t lie naked.

That’s the edge. Still the best research method in 2026.

2

2

27

6,362

The conventional way to research a Japanese net-net is to pull the financial filings, translate them, screen for net current asset value, check the land carried on the balance sheet at acquisition cost, and look at the shareholder register for activist accumulations. This is what every American investor who has discovered the Japanese trade in the last three years now does. It works. It also misses, by some margin, the things that actually predict which names in the basket will be the ones that re-rate.

The unconventional research is what nobody runs. The unconventional research is reading the company's recruiting page, in Japanese, because the language a 70-year-old president uses to describe what he is looking for in a new hire reveals more about his actual succession thinking than anything that will ever appear in a proxy statement. A president still hiring "loyal lifetime employees" is a president who will die at his desk. A president quietly hiring "young people with international experience" is a president who has begun, in some part of his mind, to think about who will own the company after him, and that thought, statistically, precedes a sale by roughly 28 months.

The unconventional research is looking at the company's annual employee photograph, which Japanese small caps still publish in their annual reports, and counting the women, because a Japanese industrial company in a regional prefecture that has, in the last five years, gone from zero women in management positions to two, is a company whose leadership has begun, quietly, to absorb the governance pressure that the Tokyo Stock Exchange has been applying, and that absorption is itself a signal.

The unconventional research is checking the company's electricity consumption, which is reported in many municipal energy disclosures in Japan and which is, surprisingly, publicly available if you know where to look. A factory that is reducing its electricity consumption while reporting flat revenue is a factory that is, quietly, becoming more efficient, which means the operating margin trajectory in the next 18 months is going to surprise to the upside. A factory whose electricity consumption is rising faster than reported revenue is a factory that is, in some hidden way, ramping production in advance of a contract that has not yet been disclosed. The data is free. Nobody looks at it.

The unconventional research is calling the company's main bank, which is disclosed in every Japanese filing, and asking, politely, whether they have noticed any changes in the company's borrowing patterns over the last 18 months. They will not tell you anything material. They will, sometimes, mention that the company has been "more active recently," which is, in the careful coded language of Japanese regional banking, an acknowledgment that something is happening, the nature of which they will not disclose, but which you can now incorporate into your understanding of the position.

The unconventional research is reading the local newspapers of the city where the company is headquartered, in Japanese, with a translation tool, because the regional press will, in a way the national press will not, report the small ceremonial events that almost always precede major corporate transitions: a retirement banquet, a new chairman of the local chamber of commerce, the opening of a new wing at the company's longtime philanthropic project. These are not material events. They are, in aggregate, the texture of what is actually happening inside a 60-year-old industrial company in a prefecture that the rest of the world will never visit, and the texture is the thesis.

I have, over six years, built positions in 41 Japanese net-nets, and the unconventional research has, in my private accounting, accounted for somewhere north of 70% of the returns. The 30% that came from the conventional research, the screens and the filings and the activist filings, would have been available to anyone. The 70% from the unconventional research was available only to someone willing to spend their Saturday mornings reading a small-town Japanese newspaper through a translation tool, counting women in employee photographs, and calling regional banks to ask questions that would not, technically, be answered. Almost nobody is willing to do this. That unwillingness is, as it has always been in every great deep value trade in history, the entire reason the math still works.

2

17

3,728

Sources of edge on Japanese small caps:

- Hiding in the sushi restaurant bathroom near HQ

- Eavesdropping on salarymen at the izakaya at 11pm

- The smoking area outside the Tokyo Stock Exchange

- A pachinko parlor in Nagoya where the CFO allegedly goes Thursdays

- The 6am bullet train, where they read the real newspaper

- Nobody else is willing to live like this

3

27

4,503

May 31

A Japanese wood distributor doing ¥399B in sales — worth ¥35B.

Net cash covers 45% of the market cap. Land carried at pre-war cost. Management's buying back ~9% of the stock a year at a 4.5% yield.

0.55x book. ~2x EV/EBITDA.

The market's pricing a liquidation. It's a company buying itself in.

2

4

57

7,605

May 31

Just got the best stock tip of my life from a sushi chef in Tokyo. Sat at an 8-seat counter in some alley in Ginza. No English menu. Old guy slicing tuna for 40 years. Three drinks in he tells me his nephew runs ops at a company I’ve never heard of. Trades on the second section. P/E of 4. Net cash is 60% of the market cap. Sells a product that every car in Japan needs. Zero analyst coverage because the filings are only in Japanese. Family owns 38%. I am buying this on Monday with both hands. The best DD on earth is being the only foreigner in a room where nobody is trying to sell you anything.

13

3

281

56,371

May 30

My Japan deep value process:

- Buy a company trading below net cash

- Realize they own the building, the parking lot, and a golf course in Shizuoka

- All carried on the books at 1989 prices

- None of it will ever be sold

5

1

191

22,817

May 29

You can buy Japanese electric utilities under liquidation value. New writeup.

4

3

115

7,742

May 28

I have, over the last nine years, made eleven separate trips to rural Japan for the sole purpose of visiting the headquarters and factories of small-cap companies whose stocks I own, in towns that do not appear in any guidebook, that are not on any tourist itinerary, that require two trains and a bus and, on three occasions, a taxi driver who had to call the company for directions because the address did not resolve on his navigation system.

I do not speak Japanese beyond the 200 or so words I have accumulated for this specific purpose, which are heavily weighted toward terms like "factory," "thank you," "shareholder," "excuse me," and "I have come a long way." I bow at angles I have practiced in hotel rooms the night before. I bring gifts, wrapped correctly, selected on the advice of a translator I retain by the hour. I show up, unannounced or barely announced, at the headquarters of a forklift-spring manufacturer in Gifu Prefecture, or a precision-bearing company in a town outside Nagoya, or a chemical company in an industrial ward of a city most Americans could not place on a map, and I am, almost without exception, received.

The reception itself is the research. I am looking at things that do not appear in any filing. I am looking at whether the parking lot is full, which tells me whether the factory is running at capacity. I am looking at the age of the cars in the parking lot, which tells me whether the employees are paid well and have been there a long time. I am looking at the condition of the founder's photograph on the lobby wall, the freshness of the flowers at the entrance, the alignment of the slippers outside the executive office, all of which tell me, in aggregate, whether this is a company that still believes in itself or a company that has begun, quietly, to give up. I am looking at whether the president, who is almost always somewhere between 71 and 84 years old, walks me through the factory himself, which means he still loves it, or hands me off to a subordinate, which means he is preparing, in some part of his mind, to let it go.

I am served tea. The tea is almost always lukewarm. I have come to understand that the lukewarm tea is not an insult but a ritual, a small offering of hospitality to a stranger who has traveled an absurd distance to look at a factory that produces a component for a machine that most of the world does not know exists. I drink the tea. I ask my three questions, through the translator, slowly. The president answers, often at far greater length than the question required, telling me about his father, who founded the company, and his grandfather, who operated the original machine, and the 41 employees, several of whom are the children of employees who worked there before them. None of this is in the 10-K equivalent. None of this can be scraped, modeled, or found on a screen. It exists only in the room, and the only way into the room is to physically travel to it, which almost no foreign investor will ever do.

I have, on these eleven trips, visited the headquarters of 34 companies. I own 27 of them. I have, on three occasions, decided not to invest in a company I had traveled thousands of miles to visit, on the basis of something I saw in the lobby, or felt in the room, or understood from the way the president did or did not look at the founder's photograph on the wall. The trips cost me, in aggregate, somewhere north of $90,000 over nine years. The information they have produced has been worth multiples of that, not because any single visit produced a single actionable insight, but because the cumulative effect of having stood in 34 lobbies, drunk 34 cups of lukewarm tea, and bowed to 34 elderly presidents, is a felt understanding of an entire market that no amount of screen-reading could ever produce. Almost nobody is willing to do this. Almost nobody is willing to fly to a town they cannot pronounce to look at a factory they will never operate, owned by a man they cannot speak to, producing a component they do not understand. That unwillingness is, as it has always been in every great deep value trade in history, the entire reason the math still works.

4

4

36

3,310

May 27

My Japan deep value process:

- Buy a profitable company at 0.5x book

- Notice ¥4 billion in cash just sitting there

- Email investor relations

- Receive no reply, ever

7

4

739

73,499