Being Different Defines Your Uniqueness Here to escape from reality and for pleasure purpose ONLY ... Miner⛏️👷♂️

Joined December 2022

- Tweets 577

- Following 282

- Followers 294

- Likes 644

10 Photos and videos

Gustavo retweeted

May 25

There's nothing like figuring out life at a young age. People have present, senseful and well informed parents who parent well together and guide them well early. That's the bitter pill to swallow.

23

60

4,161

Gustavo retweeted

Minister Nekundi just like Desperate is very pretentious. He claims to be pro-people but goes on to make transport expensive, and over-regulate Yango to make it hard for young Namibians to access opportunities. His gifts from fugitive Malima will haunt him. Bookmark this!

17

17

173

16,234

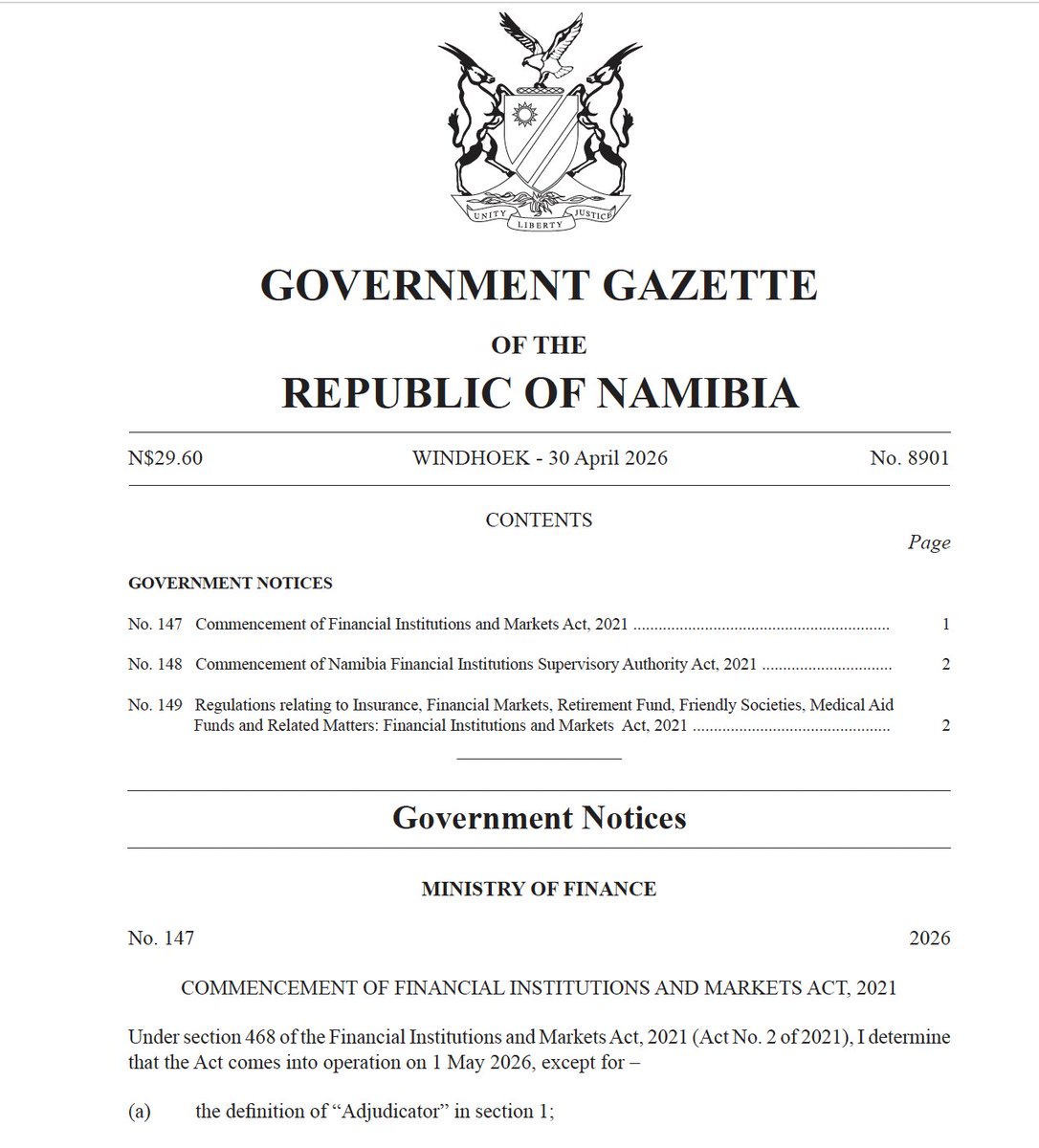

Things you need to know about Namibia’s new financial regulations

Namibia’s new financial regulations officially came into operation on 1 May 2026, and this is something or

Things you need to know about Namibia’s new financial regulations

The Government Gazette brings three major notices into effect. Government Notice 147 brings the Financial Institutions and Markets Act, 2021 into operation from 1 May 2026. Government Notice 148 brings the Namibia Financial Institutions Supervisory Authority Act, 2021 into operation from the same date. Government Notice 149 then gives the detailed regulations covering insurance, financial markets, retirement funds, friendly societies, medical aid funds and related topics.

The first thing people must understand is that the laws are not coming into force in full. The Gazette specifically excludes some provisions from commencement. Under Government Notice 147, the excluded parts of FIMA include the definition of “Adjudicator”, part of the definition of “financial services law”, section 112(2)(v), part of the definition of “defined contribution fund” in section 249, and section 427(1)(b). Under Government Notice 148, the excluded parts of the NAMFISA Act include the definitions of “Adjudicator,” “Financial Services Adjudicator Act,” and “Office of the Adjudicator,” as well as references to the Office of the Adjudicator and the Financial Services Adjudicator Act in sections 4, 31 and 55.

That is not a small issue. A financial system does not only need regulators watching institutions from above. Ordinary people also need a clear, accessible place to take complaints when pension funds, insurers, advisors or other financial institutions treat them unfairly. If the adjudicator-related provisions are not yet operational, then consumer protection is still incomplete.

The Gazette does include important retirement fund rules. It deals with actuarial surplus distribution, retirement benefit transfers, interest on delayed transfers, unpaid contributions, and housing-related loans or guarantees by retirement funds. For example, if a retirement benefit transfer is delayed beyond the allowed period, the fund must credit the transfer value with interest at the Bank of Namibia repo rate plus 4%. It also provides that unpaid required contributions bear interest, and responsible parties may remain liable.

That is important for workers because pension contributions are not just deductions on a payslip. They are part of a person’s future financial security. If an employer fails to pay contributions or a fund delays a transfer, workers should know that the law provides consequences.

But the controversial pension preservation issue remains sensitive. FIMA has commenced, but that does not mean compulsory pension preservation has automatically been implemented in full. The Gazette includes retirement fund regulations, but some of the most contested preservation-related provisions appear to have been excluded, delayed, or left for further alignment and consultation. That distinction must be made clearly so workers are not misled or unnecessarily alarmed.

The Gazette also deals with micro-insurance. Many micro-insurance categories, including funeral, disability, health, life, vehicle, fire and gap insurance, are capped at N$25,000. Personal insurance is capped at N$2,000, while miscellaneous micro-insurance may go up to N$2.5 million.

This is both useful and concerning. It creates structure for lower-cost insurance products, but ordinary people must not assume that a micro-insurance policy gives full protection. A N$25,000 payout may help with a basic emergency, but it may be far too low for serious illness, disability, funeral costs, vehicle loss or property damage.

The Gazette also tries to separate health insurance from medical aid. Health policies must not be marketed as if they are medical aid, and disclosures must make it clear that the product is an insurance policy, not a medical aid fund.

That is important, but it is also a red flag. Many people may still buy health-related policies without fully understanding the difference. A health insurance policy may give a limited benefit, while medical aid works differently. Consumers must ask directly, Is this medical aid, or is it only a limited insurance benefit?

The regulations also define money market instruments as short-term financial instruments with a maturity or redemption date of 12 months or less, designed to preserve capital, provide daily liquidity and offer returns in line with money market rates.

That is useful for people using money market funds for short-term savings, but it does not mean no risk. It means lower risk, short-term liquidity and credit quality requirements. People must still understand where their money is placed.

Another major issue is how friendly societies and medical aid funds may invest money. These institutions must keep at least 45% of their assets in domestic assets. They may also invest up to 95% in government bonds, 75% in shares, 50% in corporate bonds, 50% in foreign bonds and 10% in property, subject to additional limits.

On paper, this supports local investment. But it also creates concentration risk. Namibia’s capital market is small. If institutions are required to keep a large portion of assets locally, ordinary members may be exposed to a limited pool of local banks, bonds, companies and government-linked instruments. Local investment is important, but concentration risk should not be ignored.

The Gazette also introduces enforcement measures. A self-regulatory organisation can face a penalty of up to N$5 million for non-compliance, and late renewal of registration can attract interest of 20% per year.

That sounds strong, but enforcement is the real test. Rules are only useful if @namfisa has the capacity, independence and consistency to enforce them. Ordinary people do not benefit from strong laws that sit on paper while institutions continue business as usual.

I am looking at the new Namibia’s Financial Institutions and Markets Regulations, which came into effect on 1 May 2026. It is very interesting; I will break it down later. This regulatory framework sets the rules for how financial institutions must operate, how they may invest money, how they must treat clients, and how @namfisa can supervise the sector. This is very important because these are the rules behind pension funds, insurance policies, medical aid-related products, money market instruments, retirement transfers, and financial market conduct.

3

18

39

6,230

Gustavo retweeted

Sacky Shanghala’s delay tactics are intended to meet with Sisa’s appointment to the central committee which will inevitably give Sisa the ability to destroy the case and free his client, this is supposed to take shape at next year’s congress when Sisa takes Charge.

1

49

266

15,365

Gustavo retweeted

I am giving Sisa Namandje a grace period of 7 days to either kill me or peacefully resign from the central committee otherwise I will release privileged documents from his firm in my possession that will change his life forever. He has a choice.

27

92

481

86,826

Gustavo retweeted

A staff member of the Namandje firm who is facing harassment at work has shared with me all files of the firm’s involvement in fishrot. I intend to share those documents with the public within 7 days. After proper consultation to avoid violating attorney client privilege.

14

59

310

25,882

Gustavo retweeted

My fellow Namibians, I am disgusted and ashamed that today we are busy courting with the Devil 👿 called the USA 🇺🇸 simply because they have a huge interest in our Natural Resources.

6

17

48

3,325

Gustavo retweeted

My fellow Namibians, Tom Alweendo, Maggy Shino, Immanuel Mulunga, Victoria Sibeya and George Kamati’s Corrupt And Untruthful Cartel Uncovered.

*THE REAL OIL ROT CARTEL BUSTED*

5

14

113

14,596

Apr 16

You can’t be a stepdad from age 19-32 if you don’t a child already, niccqa create your own fam!

1

95

Apr 7

Girls be marrying our grandfathers for money but they don’t want us to marry their mothers for money.

17

Gustavo retweeted

Mar 9

No woman is getting a BBL just to stay faithful to 1 man. The whole point of that procedure is to be a h0e.

999

6,268

32,638

1,005,271

Gustavo retweeted

Feb 26

419 informal settlements. 150 in Windhoek alone. Meanwhile, government spent N$152 million building mansions for four former presidents.

3

9

22

1,235

Feb 25

I hire you as my lawyer and you send someone to come stand in for you I will need my refund.

19