Emerging euro-denominated Bitcoin treasury backed by @tyler and @cameron. Acquired Europe's largest Bitcoin event, @BitcoinConfEUR.

Joined May 2025

- Tweets 291

- Following 79

- Followers 3,393

- Likes 197

102 Photos and videos

Pinned Tweet

3 Sep 2025

Big news: Treasury launches with the ambition to become Europe’s largest Bitcoin treasury company.

Backed by @winklevosscap & @nakamoto

Treasury has:

⚡ Raised €126M ($147M)

⚡ Accumulated 1,000 BTC

⚡ Plans reverse listing on Euronext Amsterdam (ticker: $TRSR)

We’re building Europe’s Digital Golden Age. 🌍💛

More: treasury-btc.com/news/press-…

103

199

1,145

413,274

The @mattkratter - @saylor dilution debate looks crypto-native. However, it's the oldest debate in finance.

P/E is incomparable because everyone adjusts earnings. Covenant EBITDA in high yield has been stretched until leverage ratios across issuers aren't the same unit. Every metric ever invented was defined by issuers and it's for investors to criticize and discipline them.

Bitcoin treasury metrics are living that cycle in 18 months, publicly and very transparently - and Saylor deserves full credit for promoting unprecedented transparency, for any public company.

Two separate issues are being mixed. First: different metrics serve different objectives and stakeholders. Bitcoin-per-Share for $MSTR shareholders - quarterly, nobody underwrites on weekly. mNAV vs. the 1.22x breakeven for issuance discipline (1.20x today, which is why BTC Yield fired). Coverage (asset and dividend servicing) for the credit.

@Strategy's raise last week was a credit action - and scoring a credit action with an accumulation metric produces exactly this dispute.

Second: by Saylor's own admission, BTC Yield predates digital credit, i.e., the business model outran the metric. Definitions now diverge by issuer - @jackmallers' out-of-the-money convert point - and that's covenant EBITDA all over again.

The treasury sector is still so young and continues to evolve as the market develops. What matters in the end is continued transparency, and that investors truly understand the metrics, can assess differences between companies and how it impacts each part of the capital stack. We'll get there.

12

7

57

4,475

Thanks for the great conversation!

Jun 10

Ik sprak met @khingoei over Bitcoin... want wat is er aan de hand met crypto? Lees het in ons beursblog

telegraaf.nl/financieel/live…

1

1

5

334

Jun 10

Catch @khingoei's latest market commentary in @telegraaf

Jun 10

Ik sprak met @khingoei over Bitcoin... want wat is er aan de hand met crypto? Lees het in ons beursblog

telegraaf.nl/financieel/live…

1

1

171

Back at Global ABS yesterday, almost 20 years after I started in credit. This time on Bitcoin.

The highlight was @elerianm with Katie Martin of the @FT. His sharpest point: as the old pools of capital narrow, the answer is not to compete for the same capital but to expand the pool. That is what digital credit does.

Great to share what we are building at @Treasury_BTC. More to come.

1

2

4

300

Treasury retweeted

Jun 9

Why did Bitcoin really fall to the $60Ks?

@Treasury_BTC CEO Khing Oei's take: it wasn't just Strategy's Bitcoin sale — the record-breaking SpaceX IPO pulled speculative capital out of crypto. Pristine capital, yes — but still a speculative asset. 🚀

▶️ Full interview: youtu.be/CjG_rwHpXPg

#Bitcoin #SpaceX #BTC #crypto

1

1

135

1,550 BTC funded entirely off the common ATM this week, prefs untouched.

When the equity premium is there, you use it. The capital-stack flexibility is the point of the structure. Onwards.

Jun 8

Strategy has acquired 1,550 BTC for $101 million to increase our $BTC Reserve to ₿845,256. We have also increased our USD Reserve by $100 million to $1.0 billion. $MSTR $STRC strategy.com/press/strategy-…

6

1

15

1,692

Drawdowns are a great time to take a step back and look at first principles.

On the destination I'm a Maximalist: Bitcoin is the best asset and dominant digital monetary network.

On the route I'm a Capitalist: digital capital integrated through balance sheets, credit and listed equity.

However, financialization done badly recreates the fragility Bitcoin was built to escape. The Capitalist needs to build with the benefit of learning from the mistakes made in TradFi.

2

2

11

692

Jun 5

Strategy sold Bitcoin for the first time and the timelines called it the end of the treasury experiment.

@khingoei broke it down live at @money2020 Amsterdam @Cryptofocus_NL: 32 BTC out of 843,000 is balance sheet optimization, not a loss of faith.

Still a net buyer.bThe only KPI that matters is Bitcoin-per-Share.

Full interview: cryptofocus.nl/nieuws/crypto…

1

182

Treasury retweeted

Jun 4

MicroStrategy sold Bitcoin for the first time ever this week — and the market panicked.

A Bitcoin treasury CEO's take: they're still a net buyer.

"Buy 1,000, sell 32 — you're still net 968. So what's the difference?"

Khing Oei, founder of @Treasury_BTC, live at @Money2020 👇

▶️ Full interview: youtu.be/CjG_rwHpXPg

#Bitcoin #Money2020EU

3

5

469

Treasury retweeted

Jun 4

Crypto is the fastest-growing talent pool in the world — and it keeps overlooking half of it.

@laurapeijs walked onto a trading floor and saw almost no women. So she co-founded the @CryptoWomenCo.

"We need new blood, fresh perspectives."

Live at @Money2020 👇

▶️ Full interview: youtu.be/sNvCTgIn3Hk

#WomenInCrypto #Money2020EU

2

8

282

Day one at @proofoftalk in Paris.

The whole room is talking institutional adoption and tradfi meeting crypto. That convergence is the entire reason Bitcoin treasury companies exist.

But a new model owes the market something: education and accountability. The tough questions deserve real answers, not spin.

That is why we are running The Trial. luma.com/so11k1kg

2

1

10

368

May 29

We're heading to Proof of Talk in Paris. June 2 and 3.

@khingoei and @laurapeijs will be there to connect with institutions exploring Bitcoin as a long-term treasury asset. If you're attending and want to talk, find us or DM us ahead of time.

We're hosting two sessions at the conference:

A DAT roundtable in partnership with @ProofofTalk, and The Trial, a live debate on the most polarizing questions on the Bitcoin treasury model.

See you in Paris.

1

127

May 29

Strategy said they'd never sell Bitcoin.

Now? If it's accretive for the common stock shareholder, everything is on the table.

That's a big shift. @JohanMBergman breaks it down on 21-ON.

1

1

159

May 28

We are tackling the polarizing questions in Paris!

May 28

4/

June 2, 12:00. On Trial: The Bitcoin Treasury Company Model, by @Treasury_BTC.

The model goes on the stand. 10 of the stickiest questions facing Bitcoin treasury companies today. No soft pitches. No cheerleading. An honest look at where the model goes from here.

luma.com/so11k1kg

177

May 28

21 mins until we go live!

May 25

AI stocks are getting all the hype. But are Bitcoin treasury companies the better investment case?

We're going live to find out.

21-ON EP 5 · 21 min · No fluff - @TychoOnnasch x @FarmerJoe0x

17:21 CEST, May 28 on X

#Bitcoin #BTC #BitcoinTreasury

126

Treasury retweeted

May 28

4/

June 2, 12:00. On Trial: The Bitcoin Treasury Company Model, by @Treasury_BTC.

The model goes on the stand. 10 of the stickiest questions facing Bitcoin treasury companies today. No soft pitches. No cheerleading. An honest look at where the model goes from here.

luma.com/so11k1kg

1

1

2

287

Treasury retweeted

May 27

WATCH: Treasury's Khing Oei explains why European investors need a bitcoin treasury company, and how he plans to grow bitcoin:native per share through yield and consolidation.

In a conversation with Jackson Hinkle

@khingoei | @Treasury_BTC | @jacksonaltonh

1

3

10

600

May 27

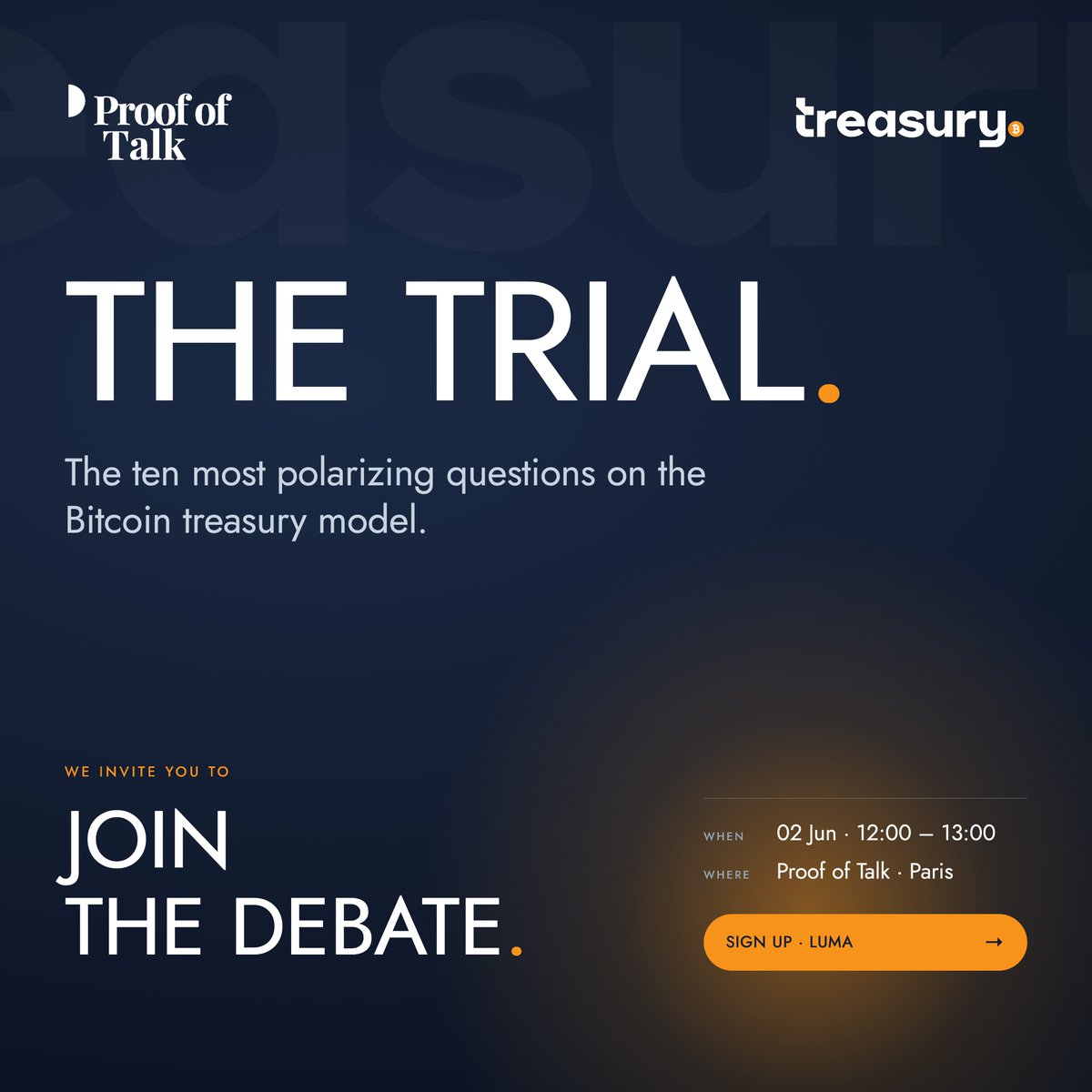

The ten most polarizing questions on the Bitcoin treasury model. No softballs.

We're hosting The Trial at @ProofofTalk in Paris on June 2, 12:00 to 13:00.

Come ready to debate. Sign up on Luma. luma.com/so11k1kg

1

6

278

May 26

"The Norwegian sovereign wealth fund is buying MSTR to hedge Bitcoin exposure in size."

That's how big this game is now.

And if Strategy sells some Bitcoin? @TychoOnnasch from @treasury_btc says the market won't care. Bitcoiners won't care. Everyone will still be here.

At some point they just have to prove it.

#Bitcoin #BTC #BitcoinTreasury

1

1

7

300