Joined November 2016

- Tweets 852

- Following 492

- Followers 2,609

- Likes 10,008

Photos and videos

Mar 11

$COFFEE.B

Rogue Core släpper trailer/release date imorgon kväll. Det största som hänt Deep Rock Galactic de senaste åren, ett av gruppens core IP, CSG äger både studio och är publisher.

Inte sett så något buzz om det från aktiehåll? Fansen däremot..

Ointressant? Under radarn?

1

10

3,098

Mar 7

Bra update heja Modus

Mar 6

Vi har intervjuat John Öhd, VD för Modus Therapeutic. I intervjun berättar John bland annat om var bolaget står idag, strategin framåt samt varför bolaget är en intressant investering.

youtube.com/watch?v=IlfhgF2d…

3

1,477

Mar 7

Kul med en ny preferensaktie!

Jag är också med på ett hörn 🤝

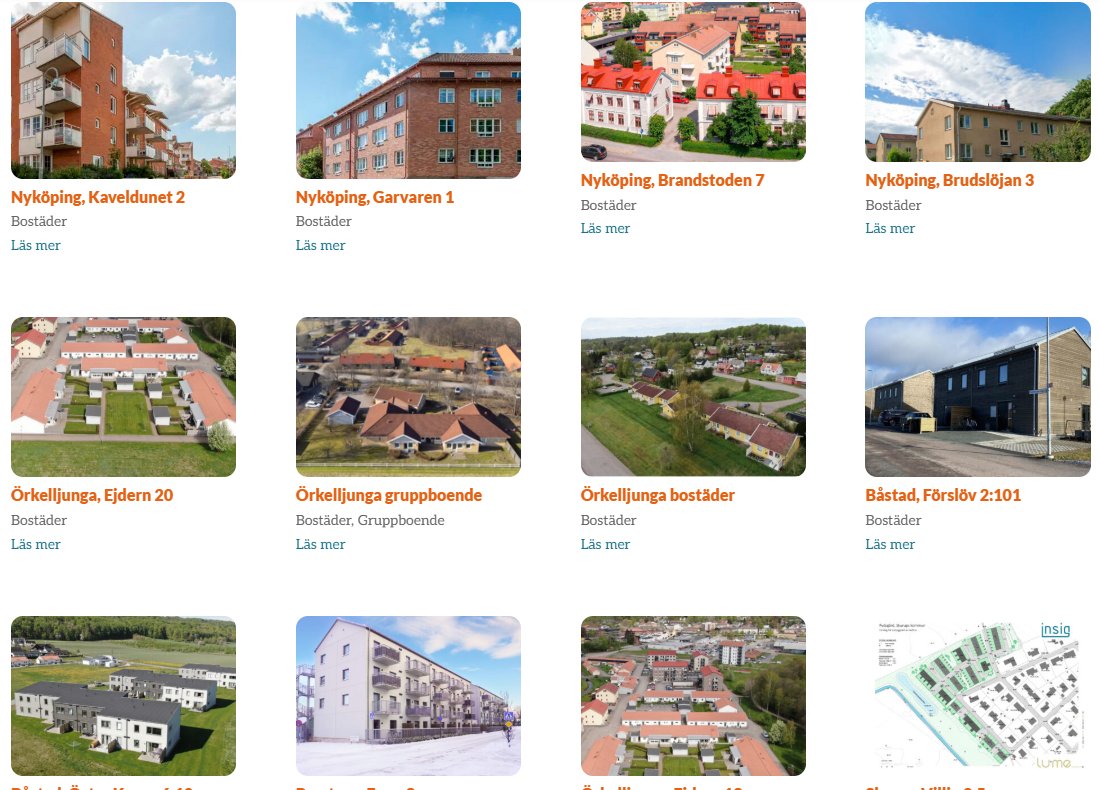

Insig, ett fastighetsbolag med fokus på södra Sverige, noterar den 27 mars preferensaktier på NGM Nordic SME. Bland investerarna återfinns Måns Flodberg och John Skogman. nyemissioner.se/borsnotering…

2

1

14

11,050

Mar 6

Största noterade teckningsoptionen inom biotech, i alla fall i modern tid. Inlösen i april efter interim.

Diamyd Medical genomför en fas 3-studie inom typ 1-diabetes och i slutet av mars kommer resultaten från en viktig interimsanalys. En stor händelse för ett relativt litet svenskt bioteknikbolag. [sponsrad] nyemissioner.se/sponsrad/vik…

2

1

8

7,053

Mar 3

Svenska Aerogel fortsätter att visa upp sig.

Dels showcase från verkligheten med semla och kaffekopp:

linkedin.com/posts/svenska-a…

Dels en intervju med Tor Einar:

nyemissioner.se/nyheter/inte…

Teckningen för TO7 drar igång nästa vecka. Vore kul med succé, vi får väl se. (Äger aktier)

2

851

Feb 27

Kul med ett livstecken! 🩹

Feb 27

Insynshandel #odinwell (källa FI).

Datum: 2026-02-27

Odinwell AB (Odinwell)

Marcus Andersson (Verkställande direktör (VD))

Volym: 200000.00

Pris: 0.19SEK

Totalt: 38600.00SEK

Förvärv

SPOTLIGHT STOCK MARKET

#odinwell #SE0015809967

1,246

Feb 27

Riktigt kul intervju med Christer om Zenicor! $ZENI

Feb 27

Intervju med Zenicors näst största aktieägare. Förvisso sponsrad artikel men ändå spot on och saklig där casets mest intressanta delar lättbegripligt lyfts fram.

Zenicor rekommenderas av myndigheter, är en vinst för samhället och lär växa på fint.

nyemissioner.se/nyheter/inte…

1

4

4,408

Feb 27

Biostock lyfter upp nyheter från FDA. Positiva för en gångs skull! Det kan bli enklare att ta läkemedel till marknaden.

Bull biotech...? Önsketänkande? 🐂🙏🌠

biostock.se/2026/02/fdas-nya…

3

794

Feb 26

Heja Aerogel. Kul med utökat distributionsavtal och så kul med en ständigt entusiastisk Per Stolt 😎🥳

Feb 26

Svenska Aerogel: Stort avtal med tyska Krahn Chemie GmbH

-Distributionsavtal

Krahn Chemie GmbH får rätt att sälja och marknadsföra Svenska Aerogels produkter i Tyskland!

KRAHN Chemie GmbH är inget litet företag. KRAHN är ett tyskt etablerat tyskt distributörsföretag av specialkemikalier och värmeöverföringsvätskor med historik tillbaka över 100 år.

Företaget säljer och distribuerar produkter till över 5000 kunder inom flera industrisegment och har cirka 280–300 anställda i Europa.

Under 2024 rapporterade KRAHN Chemie-gruppen en omsättning på över 3,5 miljarder kr.

Moderbolaget KRAHN är en del av den familjeägda Otto Krahn Group, som totalt omsätter omkring 14 miljarder och har 1700 anställda.

*Detta är ett inlägg i ett betalt samarbete. Analyser är oberoende.

1

4

1,662

Feb 23

🚁

We interviewed Erik Herlyn, CEO of Xer Tech, about the company and its long-range, heavy-lift UAV platform.

We discuss, among other things, what differentiates the technology, the key markets and demand drivers, and how the business is positioned to scale, including the commercial outlook, main risks, and the roadmap ahead.

$XER

2

1,283

Feb 19

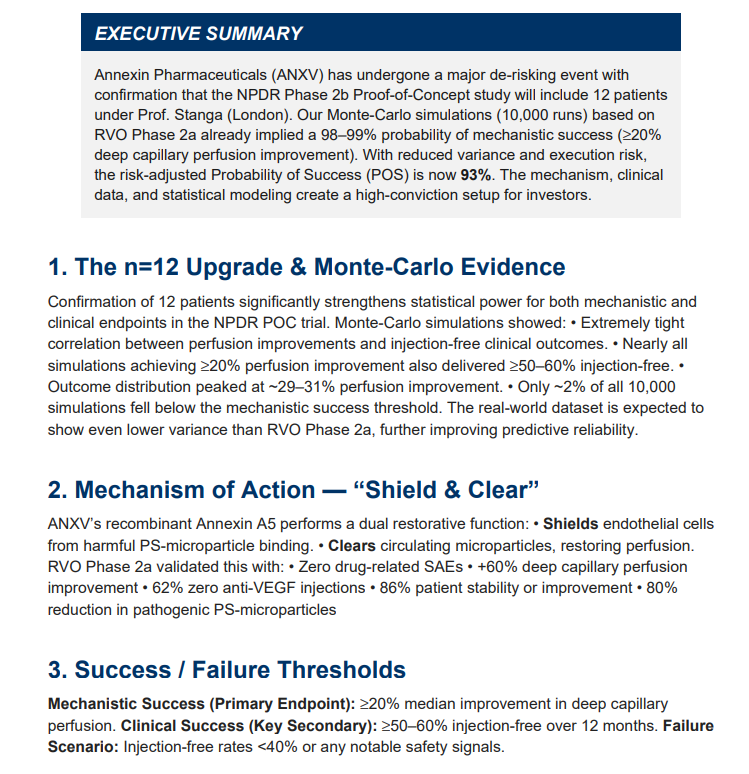

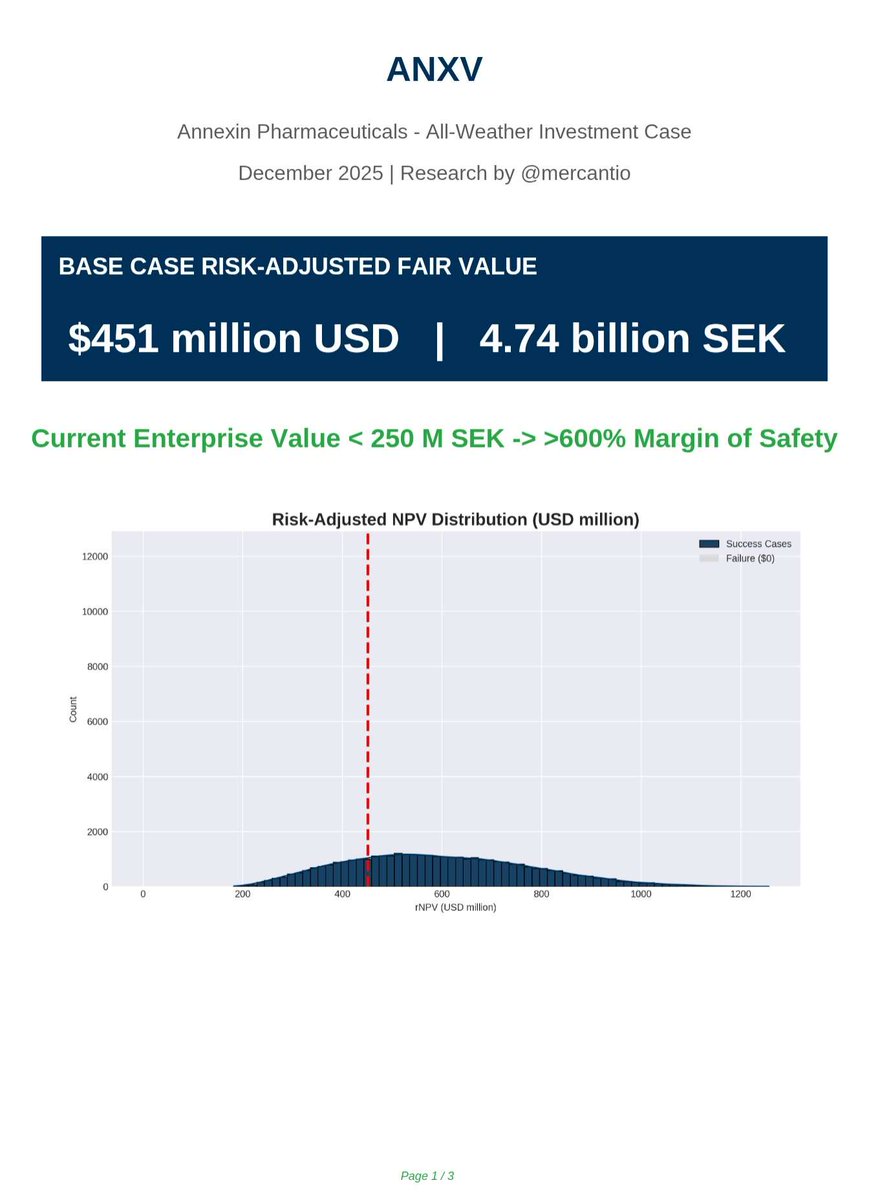

Bra sammanfattning av Annexin!

Feb 16

Intro to a new case pitch to biotech interested speculants:

Intro:

Annexin Pharmaceuticals $ANNX, currently valued at 100 MSEK, is a Swedish first-in-class biotech that has developed a novel recombinant therapy with the potential to redefine retinal disease treatment. I’ve been tracking the diabetic retinopathy research whose response to ANXV has been nothing short of extraordinary, functional improvements that standard anti-VEGF or corticosteroid therapy simply cannot deliver. This is the kind of early signal that serious investors and analysts, including Adam Feuerstein and Matthew Herper, recognize as rare and disruptive.

Data so far in terms of speculating:

My observations in terms of speculating on DR effects based on quotas, presentations, patent data. This is not company communicated, but based on patents, screen shares by the company and etc.

Clinical observations are striking. Retinal perfusion jumps 45-65 percent, capillary density on OCTA rises 40-65 percent, and macular edema and intraretinal fluid drop 50-85 percent. Microaneurysms and hemorrhages decrease 45-75 percent. Retinal function, measured by ERG and microperimetry, improves 35-65 percent, while BCVA remains stable or improves by up to eight ETDRS letters. The safety profile is pristine, no ANXV-related adverse events reported. In short, this is functional and anatomical improvement in DR and RVO that is not just incremental; it’s transformational in my opinion.

Mechanistically, ANXV targets phosphatidylserine, a pathogenic signal, directly modifying disease progression rather than merely masking symptoms. Combine that with anti-VEGF, which rapidly reduces edema, and you have a dual-action therapy that addresses both cause and effect. Patent WO2024236190A1, published in 2024, secures this combination and effectively locks in a unique IP moat.

My thoughts:

Let’s be blunt: the data should be and is world-class. Rapid perfusion gains, capillary density restoration, functional recovery, and edema reduction at these magnitudes are unheard of in diabetic retinopathy, to quote Professor Stanga:

["We can see increased retinal capillary density and increased retinal vascular perfusion in both of these vision threatening conditions. A novel drug such as ANXV with a differentiated mechanism of action has a potential to change the way we treat these patients"]

If these results replicate in NEXUS for other DR patients and in the Phase IIb, the upside is enormous: I’m talking $100- 300 million USD fair valuation, easily. And with the current uncertainty of financing, the company doesn’t need a massive rights issue, they could raise 15–30 percent of current valuation (c. ~30 MSEK) in a private placement and keep dilution minimal.

Risks:

This is high-risk, yes, but the reward profile is insane. The patient observed in the NEXUS study so far didn’t just stabilize; they showed novel anatomical improvements and enhanced light adaptation, a functional recovery that standard care never delivers. If Professor Stanga and leading ophthalmologists recognize this data as world-leading, Annexin Pharmaceuticals will become one of the most sought-after first-in-class ophthalmology assets in the market.

Outro:

Let me be clear: this is not incremental biotech. This is mechanical disease modification, a therapy that actually intervenes in ischemia and apoptosis, not just in VEGF pathways. Anyone who ignores this is leaving serious upside on the table. The data are compelling, the IP is strong, the safety is clean, and the market potential is undeniable. This is exactly the kind of asymmetric, high-conviction opportunity that investors dream of.

About me:

I have been following the research & development related to this company for three years passionately with the predictive thought of knowing that they'll enter diabetes, and diabetic retinopathy 2 years before their trial start. 2 years later, they have found signals of effect on a DR patient, in which Stanga (the PI) believes that the effects are significant and highly unlikely to be anything other than an ANXV effect.

So what do I believe about in NEXUS as a study?

I believe in a significant outcome where DR patients are showing signals of effect which will additionally de-risk the upcoming Phase IIb.

If you've come so far into the reading, this is going to be my first and only article on X related to stocks.

1

1,095

Ubbe retweeted

Feb 18

Dahlgren Capital har köpt upp eller investerat stort i fem noterade microcap-bolag, imorgon torsdag gör man sin sjätte investering. Långt poddsamtal med grundaren Peter Dahlgren som har en förmåga att provocera sin omgivning. nyemissioner.se/nyheter/pete…

3

2

20

9,798

Feb 18

Intressant med såna upplägg tycker jag, blir nog vanligare nu när garanter är försiktiga med att signa nåt.

Villkorad emission = pengarna tillbaka om de inte når en viss nivå av teckningsgrad.

Bra för nya pengar, risky för ägarna.

(Jag är neutralt inställd till caset i sig)

Feb 18

NanoEcho utvecklar en ny diagnostisk metod med målet att upptäcka spridning av tidig rektalcancer till närliggande lymfkörtlar - en idag saknad pusselbit i vårdkedjan. Företrädesemission finansierar nästa steg. [sponsrad] nyemissioner.se/sponsrad/nan…

2

1,752

Feb 17

Year of the horse, då firar vi såklart med att återbesöka detta mästerverk! 🐴

youtube.com/watch?v=NkRkuI0Z…

1

3

1,323

Feb 17

Härlig ironi i att pressmeddela att man signerat ett NDA. Man kan ju undra vad N:et står för.

"ECOMB tecknar exklusivt NDA med globalt gasbolag"

mfn.se/cis/a/ecomb/ecomb-tec…

7

2,116