Joined February 2012

- Tweets 1,523

- Following 240

- Followers 980

- Likes 1,273

87 Photos and videos

Pinned Tweet

Jan 14

After a couple months of building content, I'm officially launching Underlying Value.

The mission: find the most undervalued publicly traded investments around the world.

Get to understand my process and a preview of the exciting investment opportunities to come: open.substack.com/pub/underl…

2

2

19

15,235

Jun 13

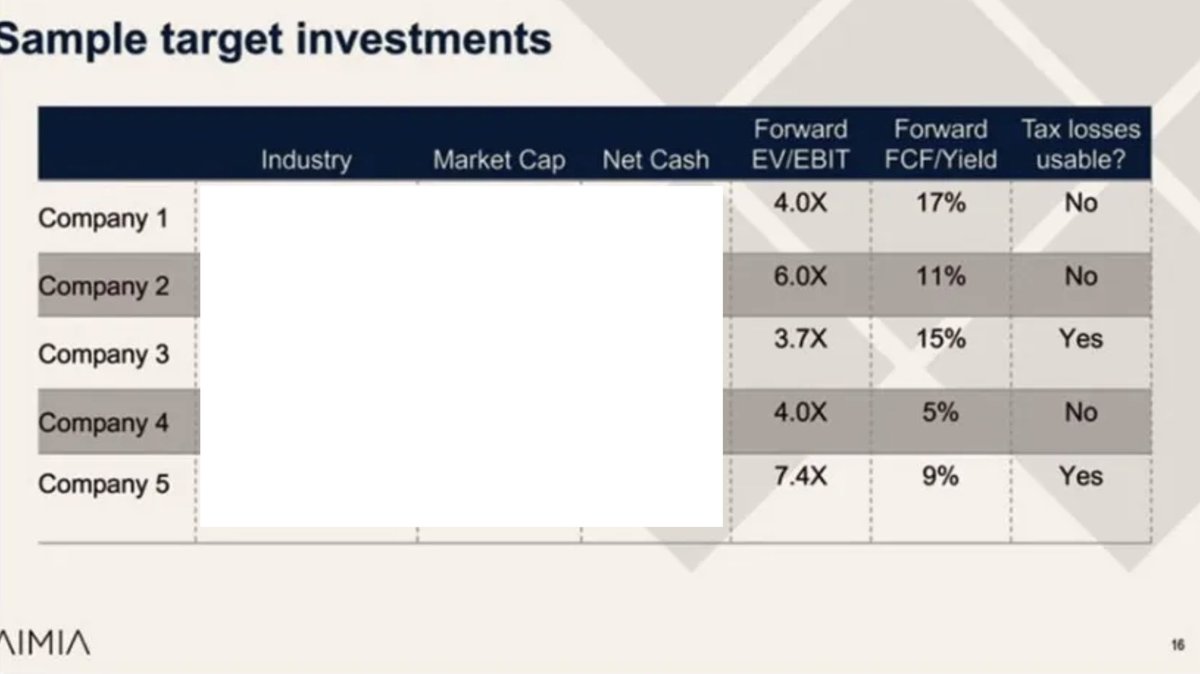

Aimia: The foundation is set for long-term compounding.

May 13th: Reviewed a slide (attached) entitled 'Sample Target Investments' at the AGM.

May 29th: Sold its largest operating asset to move to C$150M in net cash and position to acquirer mode.

Who are these target investments? I've done the work to try and put the pieces together.

1

7

652

Jun 12

The most important aspect of any good business (which comes down to FCF generation in my book) is capital allocation. Done well, it obviously creates incredible shareholder returns.

Being the allocator in a wonderful company also tends to breed hubris. Hubris that leads to decisions that place growth before all else.

I like to find the exceptions that return that capital by finding high ROIC organic opportunities (ideally) or lining our pockets as owners via dividends and buybacks.

4

206

Jun 12

Know how management is incentivized and what their personal aspirations are. While speaking with management:

- Ask what excites them about the business. If an executive is not passionate, they are getting their ass kicked daily by someone who is.

- Salary: Is their salary growing with inflation, the business or is this a personal enrichment scheme.

- Shares: Always prefer PSUs > RSUs. Why? Because they actually have goal based thresholds that need to be hit in order to vest. Know what metrics they need to hit and over what time period. I love FCF per share targets, not so much those that aren't tied to share count and can be manipulated through dilution / acquisitions - like revenue or EBITDA growth. Open market buys >>> share comp vesting.

Most American SaSS names remain untouchable for me b/c of the insane amount of stock based comp.

6

315

Jun 11

This investment has a huge margin of safety in my opinion.

/ If their equity interest in a non-consolidated minority stake is valued at 7x EBITDA (which I view as close to market), they're a 3x

To say nothing of:

/ Real estate that is worth 40-50% of EV (net of debt).

/ The operating business: 1x EV/sales. The business is solidly profitable and has a great margin profile. They should be able to easily grow this in the current market (oilfield services not in the ME).

/ Huge off balance sheet tax losses that are 10x MC (gross, not net). If properly utilized, they should be looking for a reverse takeover.

This is my largest holding as a % of ownership - hence, small and illiquid.

May 19

Post Q1 earnings, I have this investment trading under 2x EV/EBITDA. With a huge amount of off balance sheet tax losses, everything points to being a prime RTO candidate.

As an oil servicer, their inflection to profitability was achieved before the rise in prices and should be further enhanced in this environment.

Disc: Small and illiquid.

5

850

May 19

Post Q1 earnings, I have this investment trading under 2x EV/EBITDA. With a huge amount of off balance sheet tax losses, everything points to being a prime RTO candidate.

As an oil servicer, their inflection to profitability was achieved before the rise in prices and should be further enhanced in this environment.

Disc: Small and illiquid.

May 15

Q1 results add more color and beat my expectations:

-- Annualizing Q1 profit run rate: EV/NI sub 4x

-- Look through quarterly earnings: up over 40%

-- Tangible BV: now under .5x

-- Large off balance sheet assets will hopefully be leveraged for shareholder value

Expect some future quarter to quarter choppiness, but I love the industry tailwinds and positive management comments.

1

1

1,346

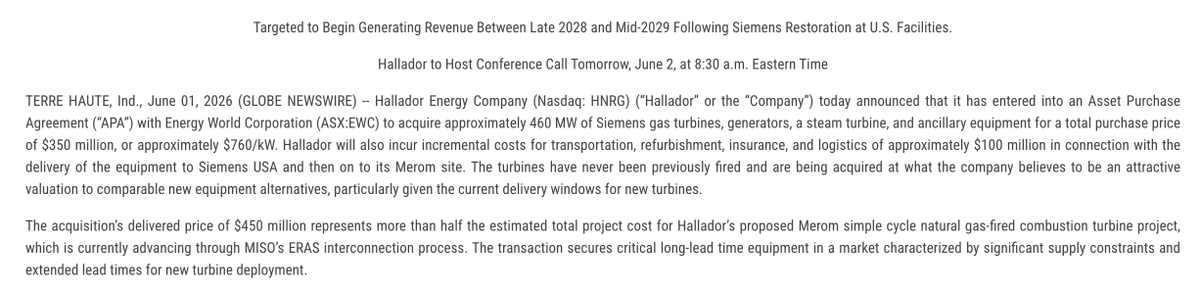

Jun 10

Evidence of a serious energy bottleneck… ten year old nat gas turbines selling for 4x their original cost from Energy World Corp (EWC.AX), then getting shipped half way around the world from the Philippines (can't imagine the shape they're in after being in that humidity) to Indiana.

~460MW combined-cycle for $350M ~$100M for shipping and refurbishment… meanwhile, they will not fire for another 2.5 years…

3

304

Jun 10

I like to find investments that prioritize shareholder returns (preferably, money in my pocket via dividends). A couple I'm either invested in, or following:

-- Frontline (FRO): One of the largest crude tanker fleets in the world. New fleet, strong management, majority of the fleet operates on spot with a tendency to return a high portion of that back to shareholders. Global energy insecurity will keep their fleet busy over the foreseeable future at what I expect to be elevated rates.

-- New Lake Capital Partners (NLCP): Cannabis REIT w/ 30 single-tenant, triple-net cultivation and dispensary properties. Debt-free Gradual Federal acceptance of cannabis is a tailwind I think will continue, further lightening the significant industry financial burdens. The discount in shares is justified due to the large rental yields they get relative to what the properties would rent to a non-cannabis user - due to a combination of regulatory restraints and large buildout costs. However, I think the 11.5% adequately compensates for this risk (good AFFO coverage at the moment).

-- Marcellus Trust (ECTM): Owns interest in nat gas wells operating in the Marcellus basin (mostly PA). Importantly, they don't have lease expenses. Gas supply in the region should be tight, buoyed by increased energy demand (data centers!). Trades at a trailing yield > 20%. The right frame is PV of ~15 remaining quarterly distributions plus terminal value against the price, and on my numbers that math works at conservative gas prices. The entity will sell / dissolve by the end of Q1 '30, at the latest.

2

207

Jun 9

M&F Bancorp ($MFBP) is my second favorite ECIP themed investment.

I believe the market is still underpricing their already signed option to repurchase $80M ECIP preferred from Treasury at a deep discount (~20–30¢ on the dollar) after clearing 60% of the Deep Impact lending threshold over 16 consecutive quarters, exercisable in H2 2026.

Retiring $80M of par at that price crystallizes a ~$55–65M gain straight into common equity, taking a bank that trades ~1.6x stated book today to ~0.5–0.6x pro-forma book, sitting on ~30% Tier 1.

Their profitability has been suppressed as they lent less to meet the Deep Impact thresholds (which had to be a % of overall lending), as a ~$1.6M/yr preferred dividend ate into earnings and credit write-off tied to a church customer. Strip those out and the P/E falls under 10x. Attractive takeout opportunity post ECIP redemption.

May 20

Community bank recipients of ECIP funds got a massive windfall in 2022. Cheap, indefinite preferred shares carrying just 0-2% dividends. In late 2024, Treasury published a Disposition Policy allowing recipients to repurchase their preferred at roughly 20-28% of face value (or as low as 0.5% via a "Mission Aligned Nonprofit Affiliate" if they're CDFI-certified).

Per Treasury's October 2025 update, dispositions are scheduled to begin in late summer 2026, once the first wave of recipients hits the 16-quarter Deep Impact Lending threshold ending Q2 2026. The Trump Treasury has confirmed the framework and is providing operational guidance, but is not taking new Option Agreement signatures.

For several of these banks, the resulting equity accretion is a multiple of current market cap (chart below). Be careful: bank quality varies enormously, timelines diverge by threshold path (Deep Impact vs Qualified Lending vs rate-reduction), and Treasury retains sole discretion over threshold determinations.

The cleanest setups: small-cap banks that (a) signed Option Agreements in late 2024 / early 2025, (b) are tracking toward Deep Impact threshold by Q2 2026, and (c) trade well below post-redemption tangible book value (d) have consistently demonstrated themselves to be profitable stewards of capital.

Once they are no longer impacted by Deep Impact thresholds, I suspect several recipients will be able to ramp up loan growth.

1

6

994

Jun 8

$100K buys you 1% of a $10M company or 0.000002% of a $5T one.

I search for the former. The value of a company is correlated to the number of people you're competing against. I like small, illiquid and uncovered. These are characteristics that can persist for a long-time, so you had better know management, be patient and have a clear perspective on what the market is getting wrong (esp. to know when to exit if the thesis is not coming to fruition).

Small business is messy and that thesis doesn't always work out, but spread amongst multiple bets and given time to compound - I think it brings the highest probability of long-term reward.

Act like an owner.

7

801

Jun 7

Aimia: After years of mismanagement, Aimia is positioned to compound book value for a long-time to come. With a great, shareholder friendly Chairman with skin in the game, ~C$150M in net HoldCo cash and over C$1B of tax assets off the balance sheet - the ingredients are finally in place. Expect them to target cash rich, deep value opportunities they can use to begin some serial acquirer platforms.

I will be surprised if they do not pursue one of the companies I've identified as an acquisition candidate within the next six months.

1

15

1,301

Jun 6

You can learn a lot asking management teams to talk about their largest investors.

It's important to understand how they view owners of the company if you're going to become one:

-- First, do they know who their top five holders are? If they don't, this is normally a red flag in micro-cap land where the cap table isn't a bunch of passive institutions.

-- Has a shareholder ever changed your mind on capital allocation? Walk me through it.

-- What are some of the top concerns of shareholders? How are they being addressed? This is critical in any turnaround. Too often you find a business being poorly managed and it's because all the largest shareholders are passive and management doesn’t have skin in the game.

-- Who do they consult for strategic and operational direction. 'What was the biggest decision you made in the past year? Who helped you solve it and what was the outcome?'

2

11

2,283

Jun 4

Aimia (TSX: $AIM.TO ) sub is now live.

During their AGM they shared a slide entitled 'Sample target investments.' Who might these targets be? I did my best to follow the trail and ended up investing in two of them.

Jun 3

New writeup is out tomorrow: Aimia (TSX: AIM).

A permanent capital vehicle trading below book with ~C$267M of fresh cash to deploy and over C$1B of tax losses sitting off balance sheet.

Run by Rhys Summerton (45%/yr at Milkwood). If he runs his playbook, they'll target cheap, cash-rich businesses in fragmented markets, built into serial-acquirer platforms.

I reverse-engineered the ones they could be hunting.

1

10

1,058

Jun 3

New writeup is out tomorrow: Aimia (TSX: AIM).

A permanent capital vehicle trading below book with ~C$267M of fresh cash to deploy and over C$1B of tax losses sitting off balance sheet.

Run by Rhys Summerton (45%/yr at Milkwood). If he runs his playbook, they'll target cheap, cash-rich businesses in fragmented markets, built into serial-acquirer platforms.

I reverse-engineered the ones they could be hunting.

10

2,334

Jun 2

Over the next week, I will be releasing an article on AIMIA ($AIM.TO).

They are a company undergoing a transformation as Rhys Summerton's permanent capital vehicle. Rhys is an incredible allocator few know or follow.

Lots to be excited about. More soon.

4

426

Jun 1

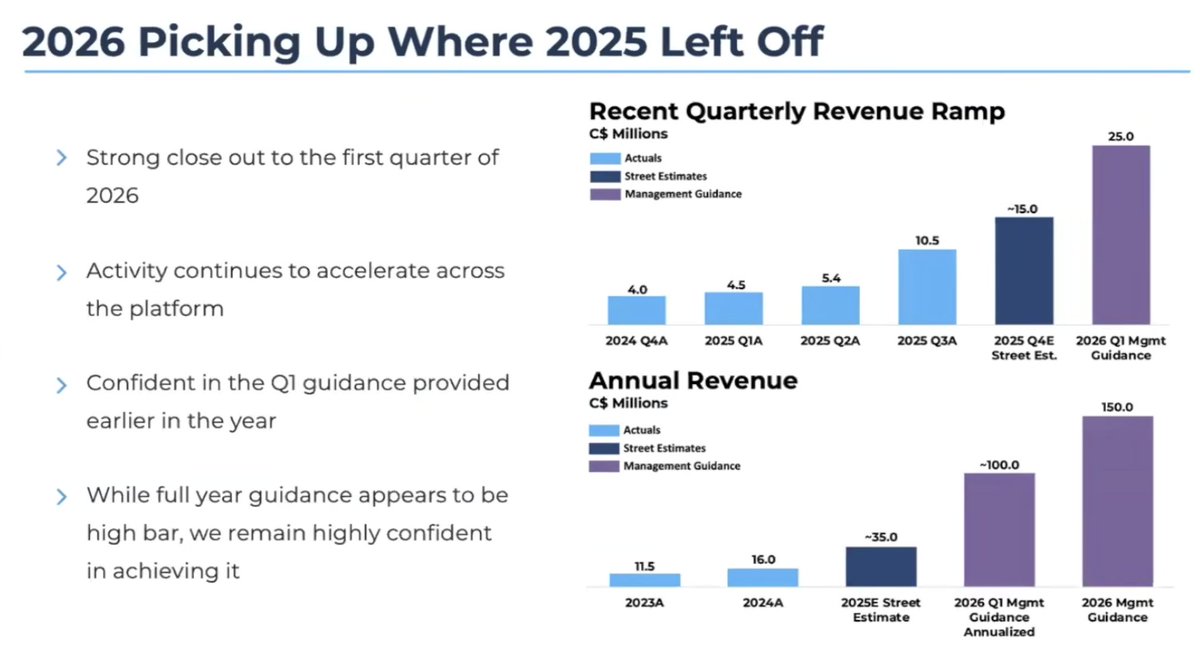

Hydreight ( $NURS.V ) Q1 earnings report will be one to watch after the bell.

It has guided to revenue of C$25M-C$28M for the quarter. C$25M implies growth of 67% QoQ and 450% YoY. This should be profitable growth, with operating income scaling ~20% on incremental sales due to relatively flat OpEx.

Victory Square Technologies trades at a significant discount to their ownership interest and has a 10% profit royalty on the VSDHOne product - where the explosive growth is being generated.

1

10

1,570

May 31

Illumina ( $ILMN ) is one of the few large cap companies still in my portfolio. They are the gene sequencing market share leader (~90% of clinical) - enabling tools that are essential for preventatively addressing longevity.

The operational turnaround by the new management regime has been incredible. It's a case where a great horse found the right jockeys.

> Operating income went from -$222M in '22 to $862M in the TTM

> Now that they've returned to growth, they're able to further flex their operating leverage.

> After a Q1 beat, guidance is for revenue of $4.52-$4.62B and EPS of $5.15-$5.30.

509

May 29

It feels like a good opportunity to add to my oil exposure.

210

May 27

There is no margin of safety for terrible management.

You can still wreck a Ferrari.

1

212