Get Latest Updates, Detailed Analysis and Reviews of Unlisted Shares at unlistedzone.com. Featured in 5 Financial Websites. Fund Raising via Pre-IPO

Joined June 2018

- Tweets 9,178

- Following 721

- Followers 14,134

- Likes 1,087

1,748 Photos and videos

Pinned Tweet

Apr 21

Most companies in India are unlisted. That doesn't mean they're invisible anymore. 👀

Datafin.in ( A Product by UnlistedZone ) gives you AI-powered deep intelligence on any of India's 3,26,000 registered companies —

✦ MCA filings analysis

✦ Financial health scoring

✦ Red flag detection

✦ Credit analysis

✦ Funding history

✦ Shareholding pattern

✦ Valuation report

Everything you need to make an informed decision — in one place. No more digging through MCA portals for hours.

Built for Bankers, CAs, Analysts & Investors.

This is what modern due diligence looks like.

Visit; datafin.in

#Datafin #UnlistedCompanies #DueDiligence #MCA #Funding #Shareholding #Valuation #Fintech #India

4

28

3,691

Jun 9

1/ In 2006, a Danish company walked into India to take on Kingfisher.

At the time, United Breweries had 60% of the Indian beer market. A near-monopoly.

19 years later, in FY25, that Danish company just made more profit than Kingfisher did.

This is the Carlsberg India story 🧵

—

2/ Carlsberg entered in 2006. Bought a small brewery in Alwar. Started selling Tuborg Green and Carlsberg Elephant in 2007.

Nobody took them seriously.

Then they did something nobody expected, they launched Tuborg Strong. Cheap. High alcohol. Aggressive shelf presence.

North India fell first. Then the East.

—

3/ Here's what makes their playbook insane:

You can't just build ONE brewery in India and ship beer everywhere. Alcohol is on the State List. Every state has its own excise law, its own licences, its own labels, its own price approvals.

Moving beer from Rajasthan to Haryana needs an export permit, an import permit, fresh state-specific labels, and a second round of duties. At scale, the math doesn't work.

So Carlsberg built 8 breweries. One per major market.

—

4/ This is the real moat in Indian beer.

- Manufacturing licence: 2–4 years per state

- Brand registration: separate, every state

- Price: set by state regulators (you don't decide)

- Distribution: in many states (TN, AP, TG) the govt is the SOLE buyer

- Excise duty: ₹25–150/litre, collected at brewery gate

Carlsberg paid ₹5,342 Cr in excise in FY25.

That's 59.8% of gross revenue gone before COGS.

—

5/ Now the crossover moment.

FY25 PAT:

• Carlsberg India: ₹449 Cr

• United Breweries: ₹442 Cr

2-year PAT CAGR:

• Carlsberg: 49%

• UBL: 21%

And Carlsberg did this with HALF the market share (22% vs 50%) and 2.5x less volume.

The profit machine is built. The scale is still coming.

—

6/ Which brings us to February 2026.

Carlsberg A/S appoints Kotak, JPMorgan, Citi for an India IPO.

Target raise: ~$700M.

Structure: Offer for Sale. 100% of proceeds go to the Danish parent.

No new money comes into the India business. Why?

Because it doesn't need any. ₹1,598 Cr cash. Zero long-term debt.

—

7/ The pitch in one line:

India drinks 2 litres of beer per person per year.

The global average is 27.

There is no comparable growth runway in global brewing right now.

At a likely valuation of ₹30,000–38,000 Cr (vs UBL's ₹35,007 Cr mcap), the IPO will price the #2 player at a discount to a slower-growing #1.

That's usually how the good ones start.

—

8/ Full breakdown, FY25 audited financials, brewery footprint, shareholding, the UBL vs Carlsberg comparison table, and valuation math.

datafin.in/blog/carlsberg-in…

1

1

6

1,025

Jun 7

Zepto will likely require significant capital to sustain itself in the ongoing quick-commerce (QC) battle. An IPO is crucial for the company, not only for growth but also for strengthening its balance sheet. The bigger question, however, is whether the market will support the valuation Zepto is seeking.

The competitive landscape has become increasingly intense, with both Flipkart and Amazon aggressively expanding their quick-commerce operations and bringing substantial financial firepower to the segment. This has further heated up an already crowded market.

At the same time, public market sentiment toward the sector remains cautious. Zomato has delivered virtually no returns over the past year, while Swiggy is trading nearly 30% below its last year price. Investors continue to be concerned about persistent cash burn, limited visibility on sustainable profitability, and rising competitive pressures.

Overall, while the quick-commerce market continues to grow rapidly, the sector faces significant challenges. Zepto's ability to achieve its desired IPO valuation will depend heavily on market conditions, investor appetite, and confidence in the company's path to profitability.

5

1,042

Jun 3

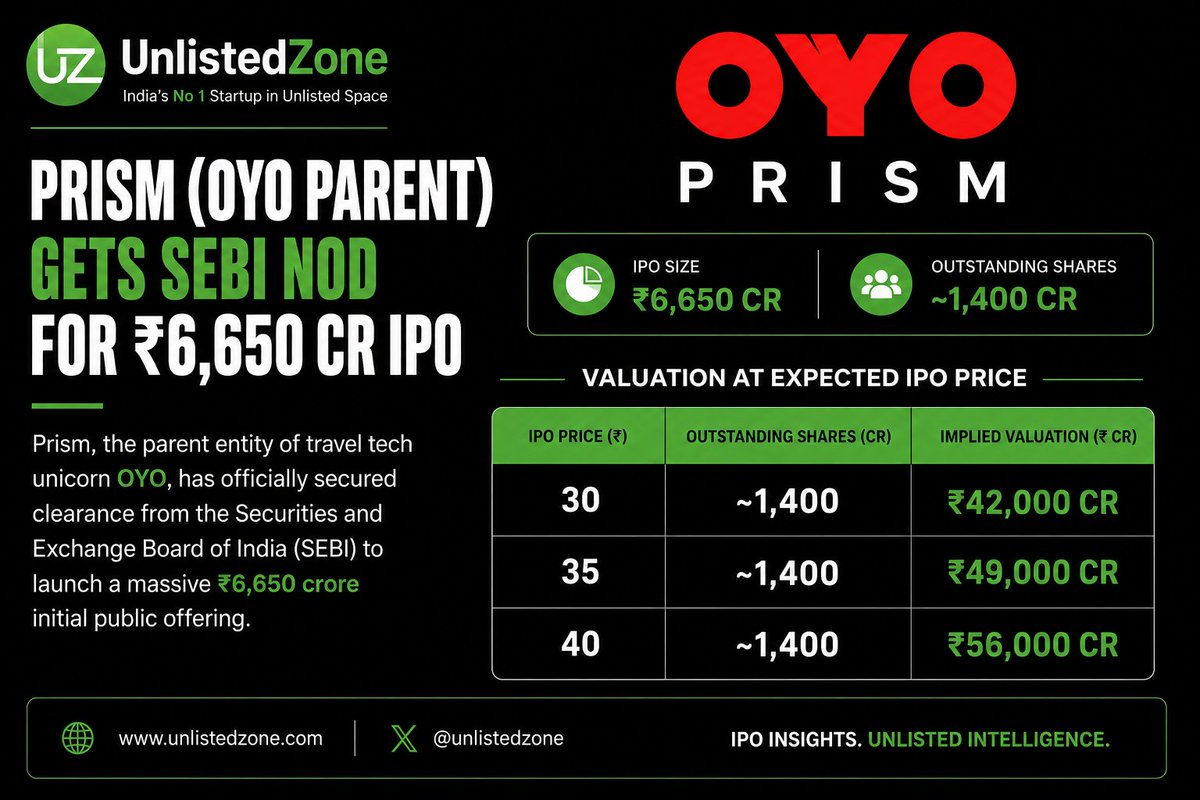

OYO has filed a Confidential DRHP with SEBI and received its approval yesterday, which means the IPO process has formally cleared its first major hurdle. This is a significant milestone, but it is important to understand what it does and does not mean for investors.

1. The share count problem

Because the DRHP was filed confidentially, the exact number of outstanding shares post-conversion of CCPS is still not publicly known. Any price being quoted in the unlisted market right now is based on incomplete information. If the actual share count after CCPS conversion turns out to be higher than assumed, the per-share price will come down proportionately. Take every unlisted price you see today with a large pinch of salt until the full public DRHP is out.

2. SEBI approval is just step one

SEBI's approval clears the regulatory gate, it does not mean the IPO is imminent. The actual launch timing will depend entirely on market conditions and what valuation institutional investors are willing to pay at that point in time. There is no fixed date. The gap between SEBI approval and IPO opening can stretch from a few months to well over a year.

3. The valuation question

What ultimately matters is not what unlisted buyers are paying today, it is what public market investors will be willing to pay at IPO. That price will be set by market conditions, comparable listed peers, and institutional demand at the time of the offer. The IPO price will likely land in the same zone as where unlisted shares are trading today. You are not getting a meaningful discount by buying early in the unlisted market.

4. The math people are ignoring

If you buy unlisted shares today, work through the full holding period honestly:

a) Time from SEBI approval to actual IPO launch — unknown, typically 6 to 18 months

b) 6-month post-listing lock-in for most unlisted shareholders

c) Total illiquidity window could easily stretch to 12–24 months from today.

Discount your expected return across that entire period. When you do this honestly, the unlisted price rarely looks as attractive as it first appears.

Our view

SEBI approval is good news for OYO, but it is not a signal for retail investors to rush into the unlisted market. Wait for the public DRHP, study the actual share count and dilution, watch where institutional investors price the IPO, and decide then. There is no urgency. Patience will serve you far better than FOMO here.

Disclaimer: This is the editorial view of UnlistedZone and does not constitute investment advice. Please consult your financial advisor before making any investment decisions.

2

7

1,303

Jun 2

The world is quietly registering in India.

In the last 6 months:

1. 58 foreign companies. 24 countries.

2. J.P. Morgan in February

3. University of Surrey in March

4. Mouser Electronics in April

5. Two Taiwanese banks in May — same week

April alone:

14 registrations. One every two working days.

We pulled every FC-1 filing from MCA and built the full picture.

datafin.in/blog/the-world-kn…

11

1,258

Jun 2

Anveshan Series B Decoded: ₹813 Cr Valuation, ₹89 Cr Raise datafin.in/blog/anveshan-ser…

2

5

1,046

May 29

Zoho has never taken a single rupee from investors.

But last year, they quietly wrote an ₹87 Cr cheque into a tiny startup in Thiruvananthapuram.

Here's the story nobody is talking about 🧵

_____________________________________________

1. First — understand what this startup actually does.

Netrasemi builds chips.

Not apps. Not SaaS. Not AI wrappers.

Actual silicon. That you can hold in your hand.

_____________________________________________

2. Most people don't know how hard this is.

When a software startup ships a bug → fix it tomorrow.

When a chip startup ships a bug

a) 6-18 months of delay.

b) ₹10-50 Cr to try again

c) Start from zero

d) No patch. No hotfix. No second chances.

_____________________________________________

3. Here's how a chip actually gets made:

a) Years of writing code (not the kind that runs on laptops)

b) Send a file to Taiwan for manufacturing

c) Wait 3-6 months

d) Open the package

e) Find out if 5 years of work was right or wrong

That's it. That's the whole process.

_____________________________________________

4. The three founders?

All ex-Intel. Ex-Conexant. Ex-Hitachi Japan.

60 years of combined semiconductor experience.

They could've stayed at their comfortable corporate jobs.

They didn't.

_____________________________________________

5. Their chip — the A2000 — runs AI directly on the device.

No cloud. No internet. No latency.

Think:

a) Drones patrolling borders

b) Factory robots detecting defects

c) Defence cameras that work offline

This is what "edge AI" actually means.

_____________________________________________

6. And the kicker?

The chips that currently run India's surveillance cameras and defence drones are made by:

a) Qualcomm 🇺🇸

b) MediaTek 🇹🇼

c) HiSilicon 🇨🇳

India has zero leverage over any of them.

Netrasemi is the first real alternative.

Now back to Zoho.

Sridhar Vembu built a $10B company without taking a single dollar from VCs.

When a man like that writes ₹87 Cr into someone else's startup —

you pay attention.

_____________________________________________

7. The numbers from MCA filings:

Valuation → ₹521 Cr Series A

→ ₹107 Cr total Zoho's stake → 13.8%

Founders still hold → 54% post-funding

Zoho is the single largest external shareholder.

Bigger than the VC that invested across two rounds.

79 engineers. ₹125 Cr raised.

India's first edge AI chip is real.

The next 18 months will decide if it becomes a business.

Full deep dive with cap table, valuation breakdown, and how the chip gets made 👇

🔗 datafin.in/blog/zoho-backed-…

2

2

5

1,771

May 28

You're holding a Vivo, OPPO, Realme, or OnePlus?

Congratulations — all four are owned by the same Chinese company.

And together, they've quietly built a ₹1 lakh crore business in India.

Nobody is tracking this.

Thread 🧵

━━━━━━━━━━━━━━━━━━━━━━━━━

1. The company is BBK Electronics, Dongguan, China.

In India it runs 4 completely separate legal entities — different boards, different auditors, different offices.

But MCA filings don't lie. Based on FY25 Numbers.

• Vivo India ——— ₹41,395 Cr

• OPPO India ——— ₹31,981 Cr

• Realme India —— ₹17,597 Cr

• OnePlus India — ₹12,983 Cr

Combined: ₹1,03,956 Cr

━━━━━━━━━━━━━━━━━━━━━━━━━

2. For context — Samsung India does ₹1,11,183 Cr.

So Samsung wins on total revenue.

But strip out Samsung's ₹45,930 Cr in exports and non-phone products…

In domestic India sales? In smartphones only?

BBK has already left Samsung behind.

━━━━━━━━━━━━━━━━━━━━━━━━━

3. But here's where it gets interesting.

Samsung earns ₹10,915 Cr in EBITDA at 9.8% margin.

All four BBK brands combined? ₹2,639 Cr at 2.5%.

Same revenue ballpark.

Samsung earns 4.1x more profit.

BBK is winning market share.

Samsung is winning margins.

━━━━━━━━━━━━━━━━━━━━━━━━━

4. Realme is the wildest story in this whole thing.

₹17,597 Cr in revenue.

Zero factory. Zero long-term debt.

Only 296 employees.

Revenue per employee = ₹59 crore.

It's not a phone company.

It's a trading entity wearing a brand jersey.

━━━━━━━━━━━━━━━━━━━━━━━━━

5. OPPO's balance sheet should give you pause.

Peak revenue FY22: ₹57,160 Cr — bigger than Samsung phones.

FY25 revenue: ₹31,981 Cr — down 38% in one year.

Net worth: still NEGATIVE ₹2,931 Cr.

Trade payables: ₹18,763 Cr.

Operationally profitable.

Structurally running on supplier money.

━━━━━━━━━━━━━━━━━━━━━━━━━

6. In 2022, the ED froze ₹465 Cr from Vivo's bank accounts.

Allegation: ₹22,842 Cr remitted to China via shell companies and inflated invoices.

Vivo's customers?

They just shifted to OPPO or Realme.

Same parent. Different jersey.

India barely flinched.

━━━━━━━━━━━━━━━━━━━━━━━━━

7. The regulatory blind spot nobody talks about:

Combined they likely hold 40% of India's smartphone market.

But because they file separately, no regulator sees the full picture.

BBK is playing four hands at the same table.

And winning most of them.

━━━━━━━━━━━━━━━━━━━━━━━━━

8. BBK didn't beat Samsung in India.

It surrounded it — from four directions, wearing four different jerseys.

Samsung still earns 4x more profit.

Has 14,000 employees.

Exports ₹46,000 Cr worth of phones globally.

But in your pocket?

It's already BBK's world.

━━━━━━━━━━━━━━━━━━━━━━━━━

Full deep dive — financials, business model, import/export flows, ED case, margin gap, and who's actually winning:

datafin.in/blog/bbk-vs-samsu…

5

1,542

May 27

🧵 Subway India has 963 stores, ₹480 Cr revenue & a ₹1,596 Cr valuation.

It has never made a profit under its current owners.

Here's the story nobody told you 👇

__________________________________________________

1/ Until 2021, Subway India was 100% owned by Subway International B.V. — a Dutch entity.

For nearly two decades, Subway International B.V. (SIBV), the Dutch holding arm of the American sandwich chain, held 100% of that entity. India was, in the global Subway lexicon, just another market to license.

In Dec 2021, quietly, Indian investors took over.

No press release. No announcement. Just an MCA filing.

__________________________________________________

2/ The new owner: Everbrands India Ltd.

They signed a fresh 20-year Master Franchise Agreement with Subway International — giving them rights to operate Subway across India, Sri Lanka & Bangladesh till Dec 2041.

__________________________________________________

3/ Then they renamed the company. Twice.

Subway Systems India → Eversub India → Culinary Brands India Pvt. Ltd.

The Subway brand stays. The Indian entity? Completely new ownership, new name, new playbook.

__________________________________________________

4/ The old playbook: Pure franchise model (FOFO). Franchisees run stores. Company collects royalties. Zero capex risk.

The new playbook: Build company-owned stores (COCO). ₹0 COCO stores in FY21 → 522 COCO stores by Oct 2025.

__________________________________________________

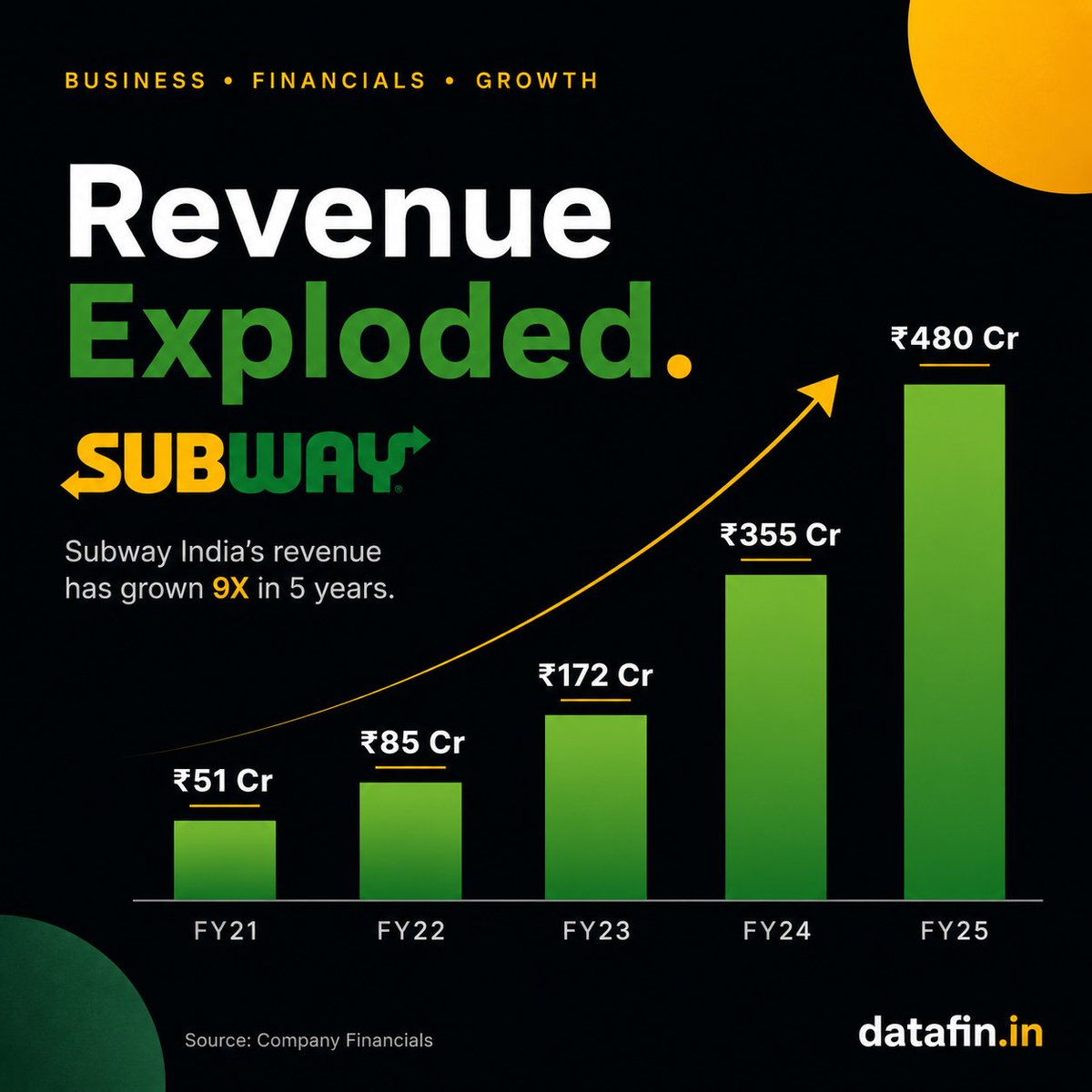

5/ Revenue exploded.

FY21: ₹51 Cr

FY22: ₹85 Cr

FY23: ₹172 Cr

FY24: ₹355 Cr

FY25: ₹480 Cr

Nearly 10× in 4 years. EBITDA turned positive. Looks great, right?

__________________________________________________

6/ Now look at the bottom line.

FY22: -₹21 Cr

FY23: ₹69 Cr ← one-time income, ignore this

FY24: -₹34 Cr

FY25: -₹38 Cr

₹400 Cr raised from investors. Not one rupee of real net profit.

__________________________________________________

7/ So where did ₹400 Cr go?

Dec 2022: ₹100 Cr raised @ ₹325/share → implied equity ~₹91 Cr

Jul 2023: ₹100 Cr @ ₹768/share → ~₹316 Cr

Jan 2024: ₹50 Cr @ ₹772/share → ~₹367 Cr

Aug 2024: ₹50 Cr @ ₹806/share → ~₹433 Cr

Jan 2026: ₹100 Cr (pref shares) → ₹1,596 Cr (EY Dec'25)

Store build-out. Pure capex.

__________________________________________________

8/ EY valued Subway India at ₹1,596 Cr in Dec 2025.

Method:

50% DCF 50% peer multiples.

The DCF assumes revenue will 7× by FY31 and EBITDA margins will hit 13.2%.

Ambitious? Very. Impossible? Not quite.

__________________________________________________

9/ Peer comparison (FY26):

a) Jubilant (Domino's): 3.45× EV/Revenue

b) Westlife (McDonald's): 3.48×

c) Devyani (KFC/PH): 3.18×

d) RBA (Burger King): 2.10×

e) Subway India: 2.20×

Cheapest in the peer set. Because it's still losing money.

__________________________________________________

10/ The real question:

963 stores. ₹480 Cr revenue. ₹400 Cr of capital deployed.

Can Subway India hit profitability before its investors run out of patience?

The 20-year franchise clock is ticking.

For full financials, cap table, EY valuation report & all funding rounds 👇

🔗 datafin.in/blog/subway-india…

16

1,919

May 26

India just placed a ₹1 Lakh Crore bet on deep tech. 🇮🇳

And 4 startups quietly made the first cut.

Not SaaS.

Not delivery apps.

But rockets, battery cells, ICU robotics & heavy-lift drones.

_________________________________________________

India’s new RDI Fund is designed to solve one of Indian deep tech’s biggest problems:

The gap between:

₹50 lakh prototype grants ➝ and ➝ ₹50 crore VC rounds.

That “funding desert” has killed countless hardware & frontier-tech startups.

Now the government wants to bridge it.

👇

_________________________________________________

The first private startups selected under the ₹1L Cr RDI push:

🚀 Dhruva Space — satellite & launch systems

🔋 e-TRNL Energy — lithium-ion battery cells

🏥 Noccarc Robotics — ICU & medical robotics

🛩️ EndureAir Systems — heavy-lift UAVs

This is India’s strategic-tech roadmap in one cohort.

Read full breakdown:

datafin.in/blog/india-1-lakh…

2

14

1,607

May 25

𝑻𝒉𝒊𝒔 𝒎𝒊𝒍𝒆𝒔𝒕𝒐𝒏𝒆 𝒓𝒆𝒇𝒍𝒆𝒄𝒕𝒔 𝒕𝒉𝒆 𝒔𝒕𝒓𝒐𝒏𝒈 𝒄𝒐𝒏𝒇𝒊𝒅𝒆𝒏𝒄𝒆 𝒐𝒖𝒓 𝒄𝒖𝒔𝒕𝒐𝒎𝒆𝒓𝒔 𝒑𝒍𝒂𝒄𝒆 𝒊𝒏 𝑲𝑰𝑵𝑬𝑪𝑶’𝒔 𝒄𝒂𝒑𝒂𝒃𝒊𝒍𝒊𝒕𝒊𝒆𝒔. 𝑰𝒕 𝒎𝒂𝒓𝒌𝒔 𝒂𝒏 𝒊𝒎𝒑𝒐𝒓𝒕𝒂𝒏𝒕 𝒔𝒕𝒆𝒑 𝒊𝒏 𝒐𝒖𝒓 𝒋𝒐𝒖𝒓𝒏𝒆𝒚 𝒕𝒐 𝒃𝒆𝒄𝒐𝒎𝒆 𝒕𝒉𝒆 𝒅𝒆𝒇𝒊𝒏𝒊𝒏𝒈 𝒓𝒂𝒊𝒍 𝒊𝒏𝒕𝒆𝒓𝒊𝒐𝒓𝒔 𝒑𝒂𝒓𝒕𝒏𝒆𝒓 𝒇𝒐𝒓 𝒏𝒆𝒙𝒕-𝒈𝒆𝒏𝒆𝒓𝒂𝒕𝒊𝒐𝒏 𝒎𝒐𝒃𝒊𝒍𝒊𝒕𝒚 — 𝒊𝒏 𝑰𝒏𝒅𝒊𝒂 𝒂𝒏𝒅 𝒈𝒍𝒐𝒃𝒂𝒍𝒍𝒚. 𝑶𝒖𝒓 𝒐𝒓𝒅𝒆𝒓 𝒃𝒐𝒐𝒌 𝒕𝒐𝒅𝒂𝒚 𝒊𝒔 𝒏𝒐𝒕 𝒐𝒖𝒓 𝒄𝒆𝒊𝒍𝒊𝒏𝒈; 𝒊𝒕 𝒊𝒔 𝒕𝒉𝒆 𝒇𝒐𝒖𝒏𝒅𝒂𝒕𝒊𝒐𝒏 𝒐𝒏 𝒘𝒉𝒊𝒄𝒉 𝒘𝒆 𝒃𝒖𝒊𝒍𝒅.”

by Vivek Srivastava, Group CEO & Executive Director, KINECO Group

5

1,454