Essential news & analysis for agribusiness leaders◾️◾️◾️ |⬇️Weekly Newsletter|

Joined March 2020

- Tweets 566

- Following 15

- Followers 1,649

- Likes 2,283

13 Photos and videos

Upstream Ag retweeted

Jun 1

AgbioInvestor's latest crop protection R&D survey for CropLife International came out last week.

The cost to bring a new active ingredient to market hit $307 million, up from $301 million over the previous time period - it is the smallest increase in the 30-year history of the survey.

Time to commercialization also decreased for the first time, from over 12 years to just over 11. The next report will be interesting to watch on this front given AI capabilities only came out towards the end of the reporting period.

The composition of spend is interesting to look at: Synthesis and formulation jumped 17.4% to $75 million (of the $307 million) and are now the single largest line item. Large-scale field trials are up 22.9% while broad biological screening is down 9.9%. The industry is moving away from brute-force discovery toward hypothesis-driven chemistry and working to overcome Eroom's Law.

Proprietary product share of the total CP market has fallen to roughly 10%. When looking at that data ijn conjunction with the data on proprietary off-patent dynamics, including how prices erode about 50% in the first decade post-patent on top of the 11.4 years from synthesis to first sale and a commercializer has 5-6 years of real pricing power to earn back $307 million plus a return on capital.

The math explains a lot of what we are seeing today in terms of start-up partnerships, spin-outs and even how companies are emphasizing only very large scale molecules markets.

Lastly, biological R&D allocation now sits at 10% of the total, though the line between biological and synthetic is getting fuzzy depending on how companies label naturally derived molecules.

Full breakdown available at @UpstreamAg

1

2

5

644

Upstream Ag retweeted

May 25

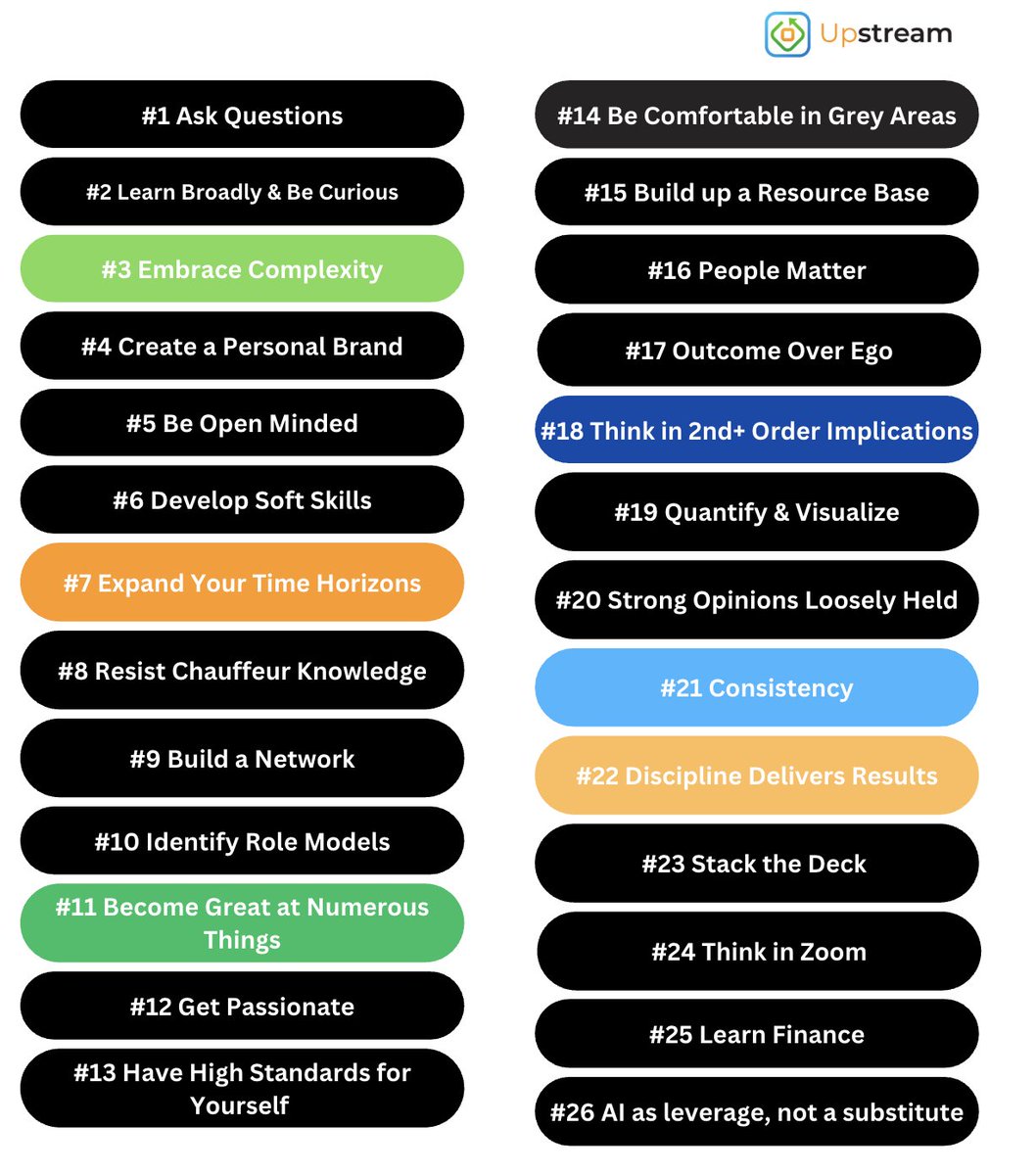

26 Principles for the Modern Agribusiness Professional

◼︎◼︎◼︎

Since 2020, I have published an annual “professionals tips” article for new College grads entering the agriculture industry, aimed at amplifying their ability to get up to speed and improve professionally.

One of the most common pieces of feedback I received around it was that it shouldn’t be emphasized to just new grads, but all agribusiness professionals.

Taking that into account, I have re-positioned it beyond students and new grads towards agribusiness professionals of all experience levels.

Some of these were stumbled on myself, others are borrowed from reading and listening to other much more experienced individuals from agriculture or other industries.

I think this year these concepts are especially important to call out as we see AI increase in prominence.

Today, intelligence, and action are increasingly becoming commoditized — automated by AI or handled by systems which means the real edge lies not in simply doing, but in knowing what is the most high leverage action to take.

When everyone has access to the same tools, technologies, and playbooks, advantage shifts to those who can think clearly, prioritize wisely, and act with conviction.

That means leaders who develop discernment and improved judgement — the ability to cut through noise, choose the right path, and anticipate second and third order consequences, will outperform those who simply move faster or “do more.”

I hope highlighting these concepts can help individuals build better judgement, make higher-quality decisions, and improve career prospects.

These 26 examples have been a constant source of leverage for me and while I won’t claim the principles to be novel for industry veterans, I think they can be a useful reminder for everyone striving for professional and personal development.

@UpstreamAg

1

3

6

932

Upstream Ag retweeted

May 4

Do you like the new Corteva SpinCo (Seed company) name, ‘Vylor’?

4%

Yes

65%

No

31%

Indifferent

151 votes • Final results

2

5

2,346

Upstream Ag retweeted

May 4

A look at the AgBiTech Acquisition by @BASF.

In Q1 2026 BASF announced the acquisition of AgBiTech.

One thing to note from their report is the “Investments” line. The AgBiTech acquisition was finalized in Q1 and investments were up ~€120 million YoY, and about the same above the 5-year average for the same period.

In looking at the cashflow commentary there is a call out of the acquisition:

Payments were made in the amount of €124 million in connection with the acquisition of AgBiTech, Brisbane, Australia, and for a purchase price adjustment of €33 million relating to the sale of the global pigments business in 2021.

The statement is confusing to me given the second half of the sentence. However, given the investment and acquisition line item suggesting a ~ €120 million price for AgBiTech, and the line seemingly suggests €124 million in deal price, it seems safe to assume €124 million is the price that was paid.

I speculated on the price paid, and I was way off. But since we roughly know their revenue, and now the value, we can look at revenue multiple paid, which gives a base barometer for other future acquisitions:

AgBiTech seemingly had ~$20 million USD in revenue. Using a USD to EURO of 0.85 we get a revenue of ~€17 million, which means a revenue multiple of 7.3x. Higher than I expected. For context, Corteva acquired Stoller (not biocontrol) for ~3x revenue, Syngenta acquired Valagro for around the same and BASF’s previous large acquisition, Becker Underwood, was for around 4x.

1

1

7

1,459

Upstream Ag retweeted

“The most successful incumbents in agriculture are not trying to act like software companies. They are leveraging slow-clockspeed realities to their advantage.” 🔥🔥🔥

2

2

697

Upstream Ag retweeted

Apr 27

Clockspeed, Capital, and Conviction: Considerations for R&D and M&A in Agribusiness

There is a recurring critique that incumbent agribusinesses are "asleep at the wheel" because they do not spend higher percentages of revenue on R&D like big tech or pharma, or don't acquire like other industries. The framing, while well-intentioned, doesn't consider the structural dynamics of large companies and the greater industry incentives.

I believe there are frameworks that can help us understand why we don't see more.

One of those is industry "clockspeed" — a concept coined by Charles Fine in his book by the same name.

Industries have different rates of evolutionary change. Software and semiconductors sit at the fast end, where hesitation is fatal. Agriculture, however, is a slow-clockspeed industry.

In fast-clockspeed industries, the cost of being wrong is high, but the cost of inaction is higher. In agriculture, premature commitment can be destructive.

This is why simply asking for more M&A or R&D is a tactical oversimplification. The most successful incumbents in agriculture are not trying to act like software companies. They are leveraging slow-clockspeed realities to their advantage. They observe market traction, identify "consensus bets" and then leverage their distribution moats to scale these technologies in ways startups cannot.

Capital allocation is not just about spending; it is about disciplined orchestration across all potential uses of capital.

The CEOs who deliver long-term returns are those who resist the pressure to chase growth for its own sake and instead deploy capital based on competitive positioning and internal cash flow. These also tend to be the companies that deliver the better products and outcomes to customers long term, too.

In my latest breakdown, I look at the intersection of clockspeed, capital allocation, and why the disruption narrative often misses the mark in agriculture.

Check out a brief overview of Clockspeed in the video below. @UpstreamAg

2

1

5

1,090

Upstream Ag retweeted

Apr 21

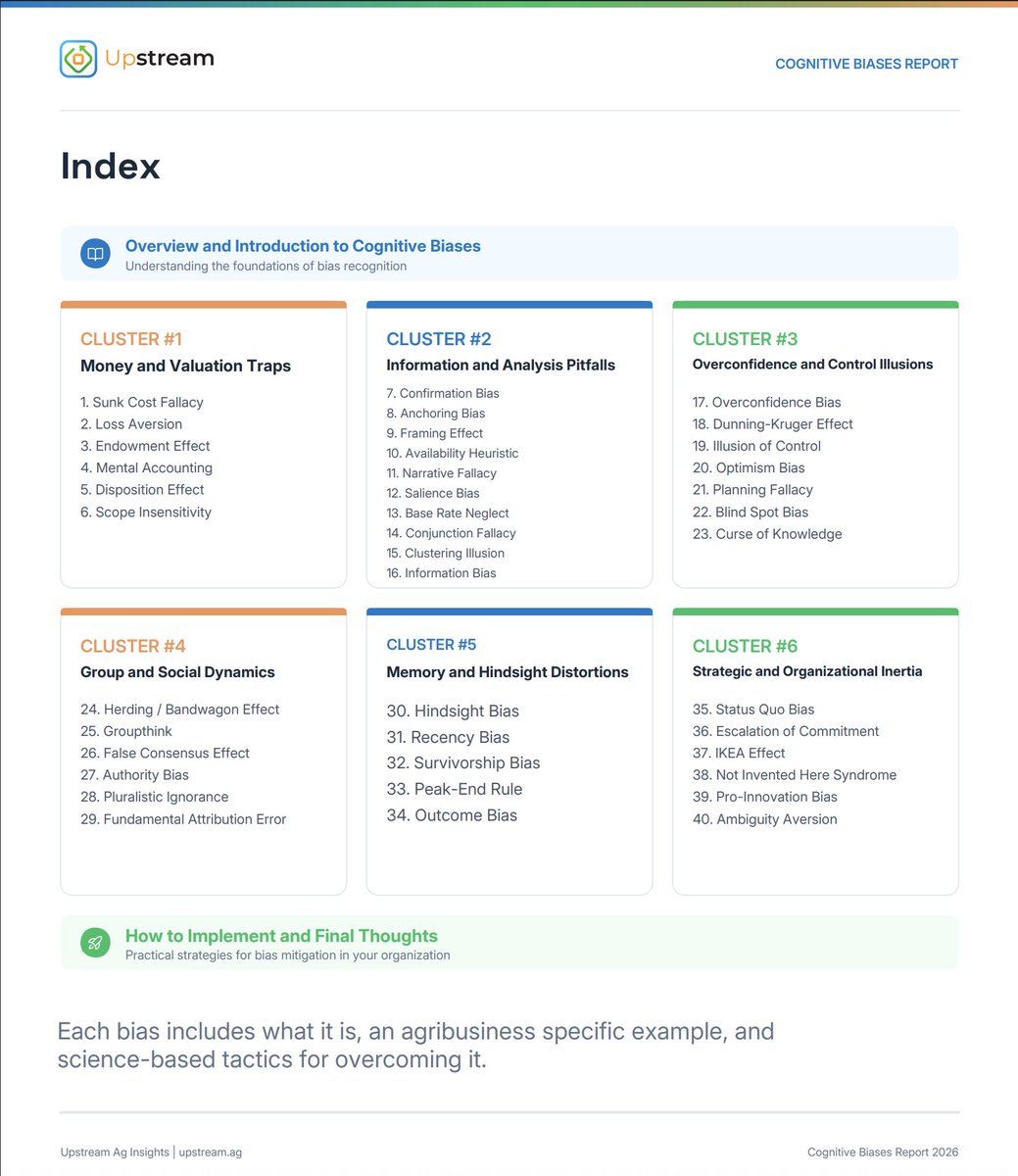

Cognitive Biases and Improved Decision Making for Agribusiness Leaders

◼︎◼︎◼︎

A cognitive bias is a systematic pattern of deviation from rational judgment. It's a predictable way our brains diverge from effective reasoning when processing information, evaluating risk, or making decisions.

I believe understanding them can vastly improve decisions making, along with influence.

So I put together a breakdown of 40 biases I find relevant, across 6 related clusters.

Every one is framed around actual agribusiness situations, including capital allocation, M&A, trading desks, R&D pipelines, selling, product launches, marketing, or board dynamics.

A few examples from inside:

- The ag retailer who sunk $4M into a proprietary digital platform because walking away felt like "wasting" the spend. The $7M budget was gone either way. The real cost was 18 months of delayed partnership revenue.

- The seed company that kept funding a declining $80M legacy platform because visible revenue felt more real than a next-gen pipeline. Clayton Christensen's disruption theory in action.

- The boardroom spending 90 minutes on an $80K break room and 30 minutes on a $12M acquisition.

Each bias includes what it is, the agribusiness example, and science-based tactics for overcoming it.

I also recorded a podcast on 7 of the biases, with an overview of one of my favorites, The IKEA Effect.

Researchers showed people value what they build themselves far more than identical items built by others — even when the self-built version is objectively inferior.

In agribusiness, this is the custom-built CRM defended against a superior commercial alternative, or even less tangible things like strategies or initiatives. I think it is worth paying attention to.

@UpstreamAg

2

1

8

1,194

Upstream Ag retweeted

Apr 19

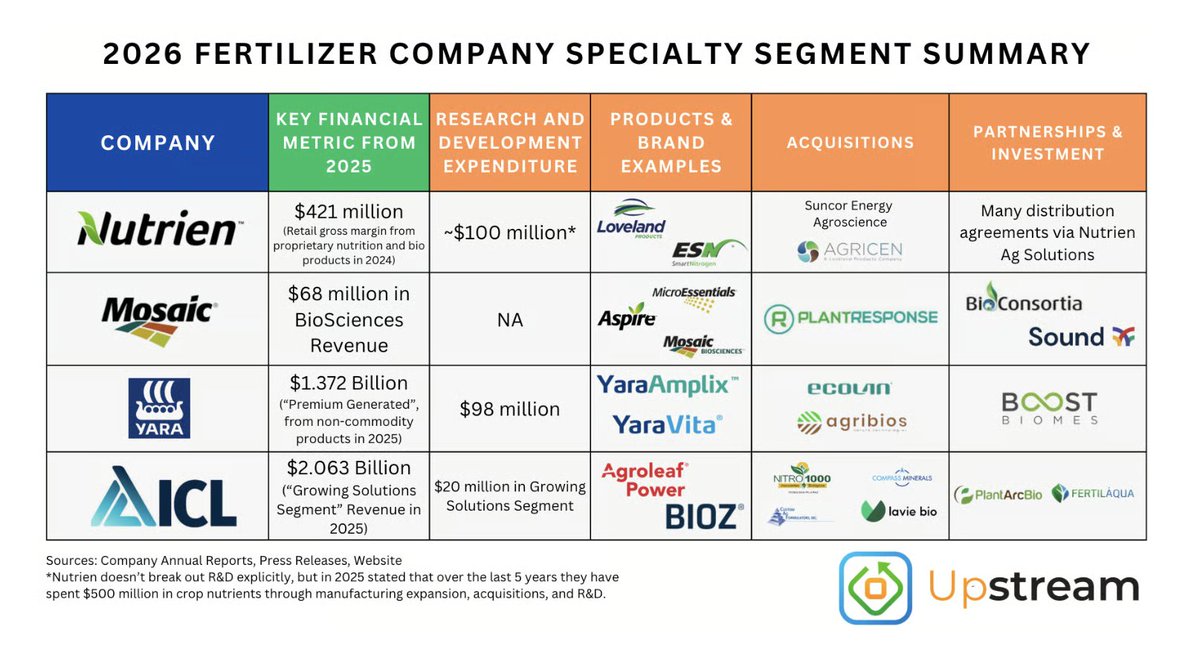

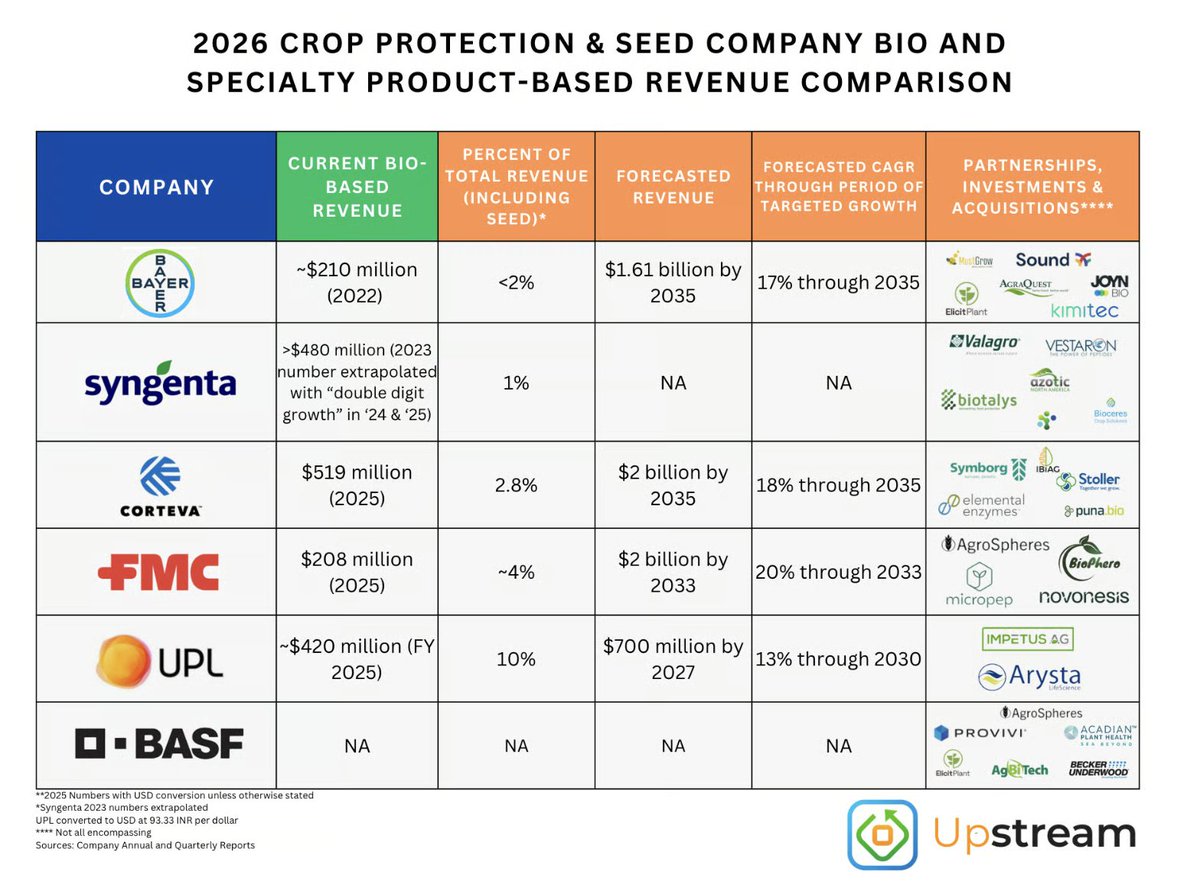

Every major crop input company now has a biologicals strategy. The question is how are they progressing and what specifically are they doing?

I just published an updated report that tracks the biologicals and specialty nutrition strategies, revenues, acquisitions, partnerships, pipelines, and commercial progress of 16 companies across crop protection, fertilizer, and the independent biologicals landscape.

Crop protection: Corteva, BASF, Bayer, Syngenta, FMC, and UPL.

Fertilizer: Yara, Mosaic, Nutrien, and ICL.

New to this edition are profiles on six scaled independent players that rarely get this level of coverage: Rovensa Next, BioFirst Group (formerly Biobest), Verdesian Life Sciences, Koppert, Acadian Plant Health, and DE SANGOSSE.

A few things you'll find inside:

Mosaic's Biosciences business doubled revenue to $68 million in 2025, hit EBITDA positive in 2025, and is targeting $200 million in EBITDA by 2030. How they're applying the MicroEssentials playbook to biologicals, and where their nitrogen fixation go-to-market approach may get challenged.

Corteva posted $519 million in biological revenue in 2025. What the planned Corteva split means for the biologicals portfolio, and why the NEXTA launch through Pioneer dealers is an important initiative.

BASF acquired AgBiTech in early 2026, their first meaningful bio acquisition since Becker Underwood in 2012. The report looks at why NPV-based bioinsecticides are a fit, and what the coming Ag Solutions IPO means for their biologicals investment appetite.

Nutrien's proprietary crop nutrition and biostimulant gross margins are approaching $500 million, with 70% of future proprietary product growth expected from biologicals and nutritionals.

The report also includes side-by-side comparison snapshots across segments, the largest bio-based and specialty acquisitions to date, an acquisition timeline since 2010, the key market drivers behind the growth of this segment and images illustrating acquisitions and partnerships, along with future considerations for the companies.

@UpstreamAg

2

9

28

5,638

Upstream Ag retweeted

Apr 13

DunhamTrimmer Biostimulant Report Highlights and Analysis

◼︎◼︎◼︎

The global biostimulant market hit $4.47B in 2024 and is projected to reach $7.88B by 2030.

But the headline number obscures what's actually happening structurally in the category.

Latin America and Asia-Pacific have overtaken Europe as the largest biostimulant-using regions. North America crossed $1B for the first time. Humic and fulvic acids dominate North American sales, driven by access to high-quality leonardite deposits, but amino acids and protein hydrolysates are gaining ground fast.

Meanwhile, commoditization is accelerating. Low barriers to entry, shared raw material suppliers, weak IP, and undifferentiated go-to-market strategies have put much of the industry on a path toward price-based competition. The companies that built this category now face the most pressure from it.

The most important forward-looking concept in the DunhamTrimmer report is Single Biostimulant Molecules. Rather than working with complex blends and differentiating purely through marketing, SBM players are identifying specific molecules with defined modes of action on plant metabolism and rhizosphere pathways. More specificity means more consistent efficacy, more replicable results, and a defensible value proposition, similar to how crop protection efforts have been executed.

I recorded a full video walkthrough of the DunhamTrimmer 2025 Global Biostimulant Report covering:

- Drivers of Interest

- Regional growth dynamics and where the market is headed

- Commoditization pressures and strategic responses

- The Single Biostimulant Molecule opportunity

- What this means for companies and investors in the space

Check out the full video below. @UpstreamAg

1

1

8

1,348

Upstream Ag retweeted

Apr 12

Cognitive Biases and Improved Decision Making

■■■

Every strategic decision in agribusiness passes through a human brain before it becomes action. That brain, regardless of the education or the decades of experience informing it, is running on cognitive software that evolved to avoid predators, and prioritize short term constraints, like food management or safety, not to optimize for being different, thinking long term or building systems that create success in business.

These sub-optimal approaches to thinking and decision making are known as cognitive biases.

They are patterns deviating from rational judgment and are not occasional mistakes or signs of low intelligence, however, they are predictable, measurable, and universal tendencies that affect how we process information, evaluate risk, remember outcomes, and interact with others.

They have long been central to my considerations when decision-making — though I remain far from perfect at managing them.

I think anyone operating in agriculture should be even aware of these biases – for those farming, and allocating capital and resources, or at a company and managing a team, or setting strategic priorities.

The higher the stakes and complexity of a role, the more cognitive biases can distort our judgment in ways that are hard to detect in the moment.

The full breakdown examines 40 cognitive biases through the lens of decision-making, for the likes of boardrooms, R&D labs, commercial teams, and executive suites where strategic decisions can influence billion dollar outcomes.

For each bias, there are four main areas covered:

1. what it is

2. why it matters

3. a specific agribusiness example of how it distorts decisions (occasionally, I will highlight how they can be used inversely, as well).

4. science-based strategies for overcoming it.

The full report is available for subscribers at upstream. ag.

@UpstreamAg

1

1

8

792

Upstream Ag retweeted

Apr 10

Upstream Ag Professional - The Big Three Stories of the Week

◼︎◼︎◼︎

A look at what agribusiness leaders will find in this weekend's edition of Upstream Ag Professional:

1. Cognitive Biases and Improved Decision Making for Agribusiness Professionals

Often we focus on making smarter decisions, but as good of an opportunity to improve our decison making and effectiveness is to remove predictably bad ones.

Over a decade of collecting cognitive biases led me to build a practical guide with 40 biases I reference often, organized into six clusters, each with agribusiness-specific examples and science-based strategies for overcoming them.

The aim is to have a reference piece for agribusiness professionals to imrpove their decision making, or enhance their influence.

2. Biostimulant Sales: Like selling seed? Or something else?

Check out a small clip from this week's @UpstreamAg Professional audio coverage highlighting the similarities to crop protection, but it goes further than that and I dive in in this weekend's edition.

3. Mental Models for Agribusiness Leaders with Shane Thomas on The Future of Agriculture

This week I joined @timhammerich on The Future of Agriculture podcast to discuss 7 useful mental models that are directly applicable to agribusiness professionals. Models include some popular, and some lesser known ones: Jevons Paradox, Influence Erosion, Strategy Tax, Friction Reduction, Contrarian Decisions, Jobs to be Done and One-Way Doors vs Two-Way Doors

Plus much more in this weekend's edition.

2

2

9

1,177

Upstream Ag retweeted

Apr 7

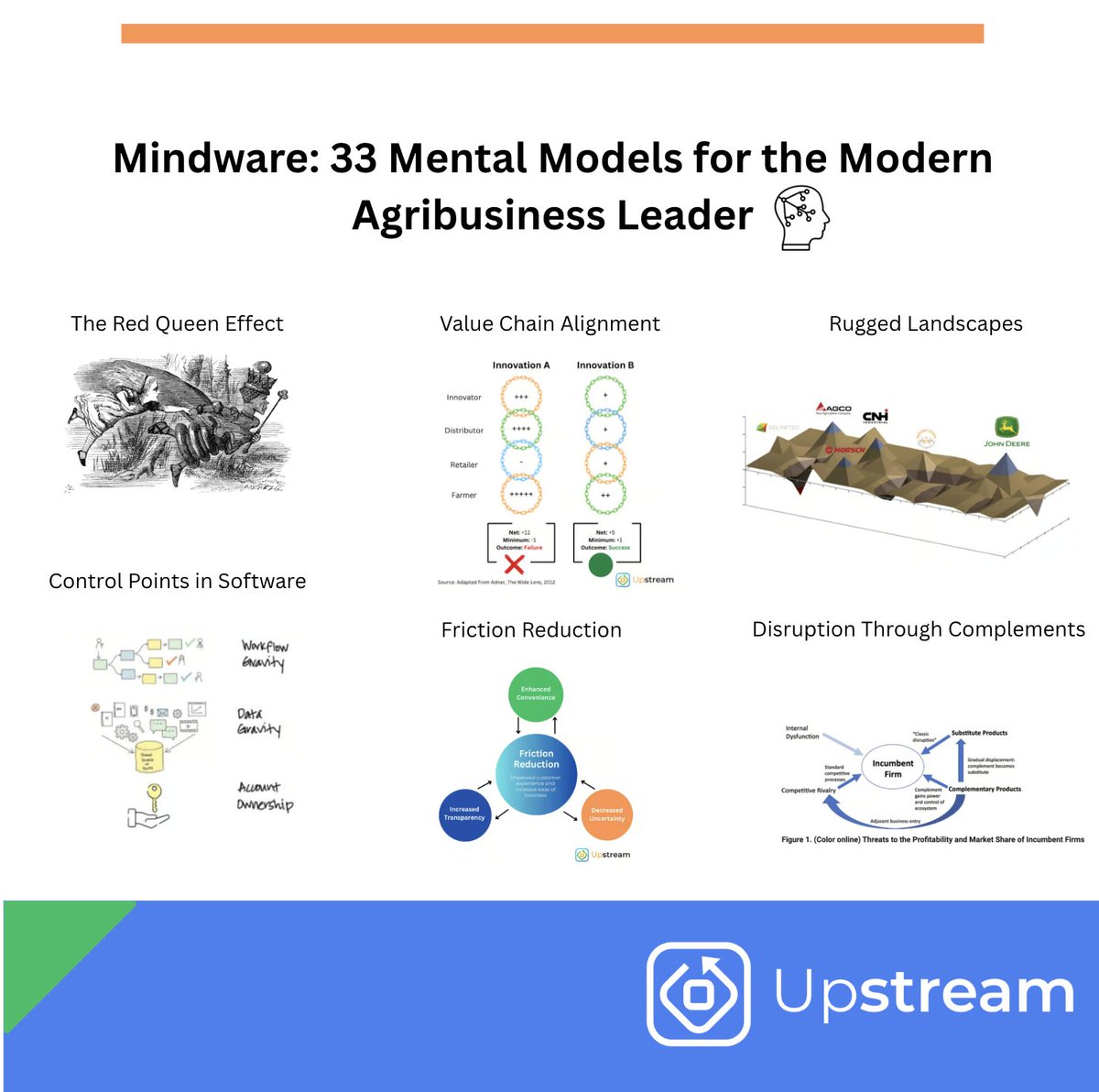

Mental Models for Agribusiness Leaders

◼︎◼︎◼︎

Recently, I talked with @timhammerich on The Future of Agriculture, one of my most listened to podcasts.

It was a ton of fun to join Tim and talk about some of the concepts that have been valuable to me over the course of my career.

In the conversation, we dive into half a dozen of the mental models I covered in the @UpstreamAg Insights e-book, Mindware: 33 Mental Models for The Modern Agribusiness Leader.

The basis of the concepts are that agribusiness professionals operate in a world full of volatility, complexity, and constant change. Commodity price swings, regulatory shifts, changing customer demands, and technological evolution create a landscape where uncertainty is the norm.

And ultimately, agribusiness professionals are knowledge workers and what separates the best in agribusiness from the rest is often how they think.

Thinking better, whether more strategically or quickly, requires mental tools.

Carpenters have a tool belt, golfers carry 14 clubs, a chef has more than just a spatula.

Every "tool" serves a specific purpose, depending on what is required.

Agribusiness professionals should operate the same way with mental tools.

These mental tools are what I refer to as Mindware - models and frameworks that help to gauge a scenario, find gaps in logic, or think long term, ultimately delivering improved judgement and better outcomes for careers and businesses.

Check out the full conversation where Tim and I discuss the concepts and apply them directly to agribusiness: futureofagriculture.com/epis…

3

9

922

Upstream Ag retweeted

Apr 6

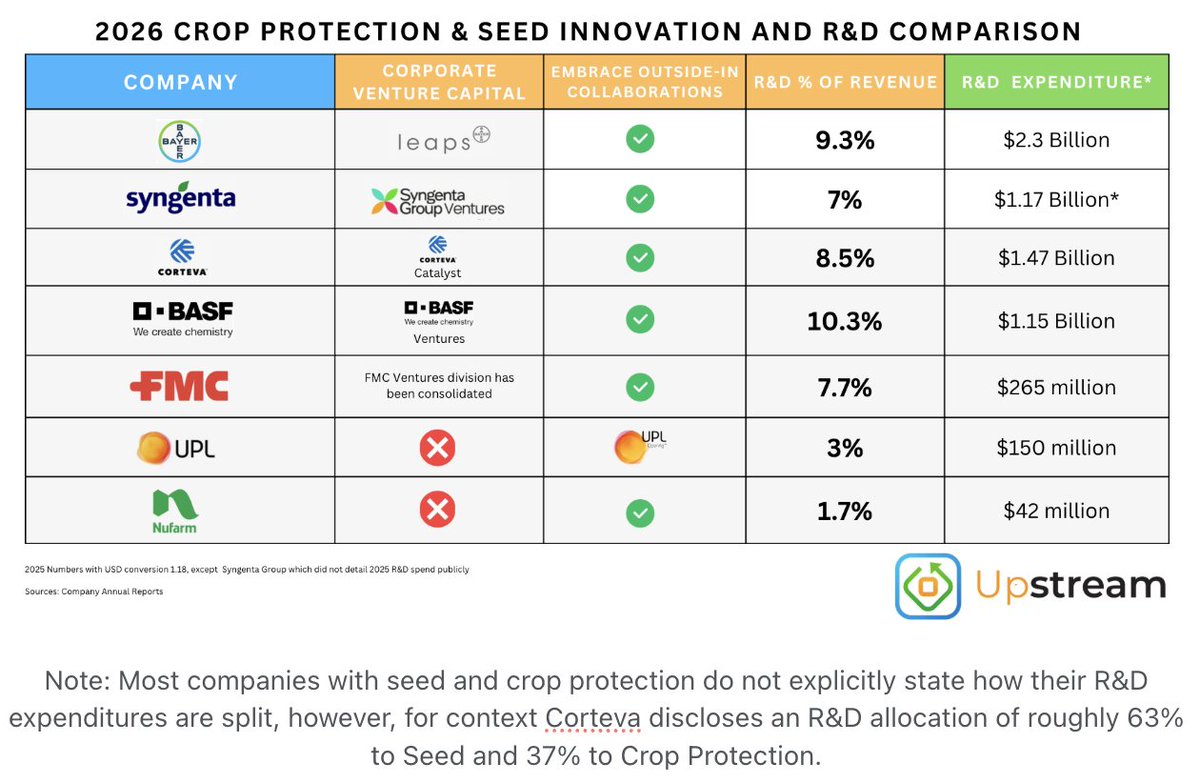

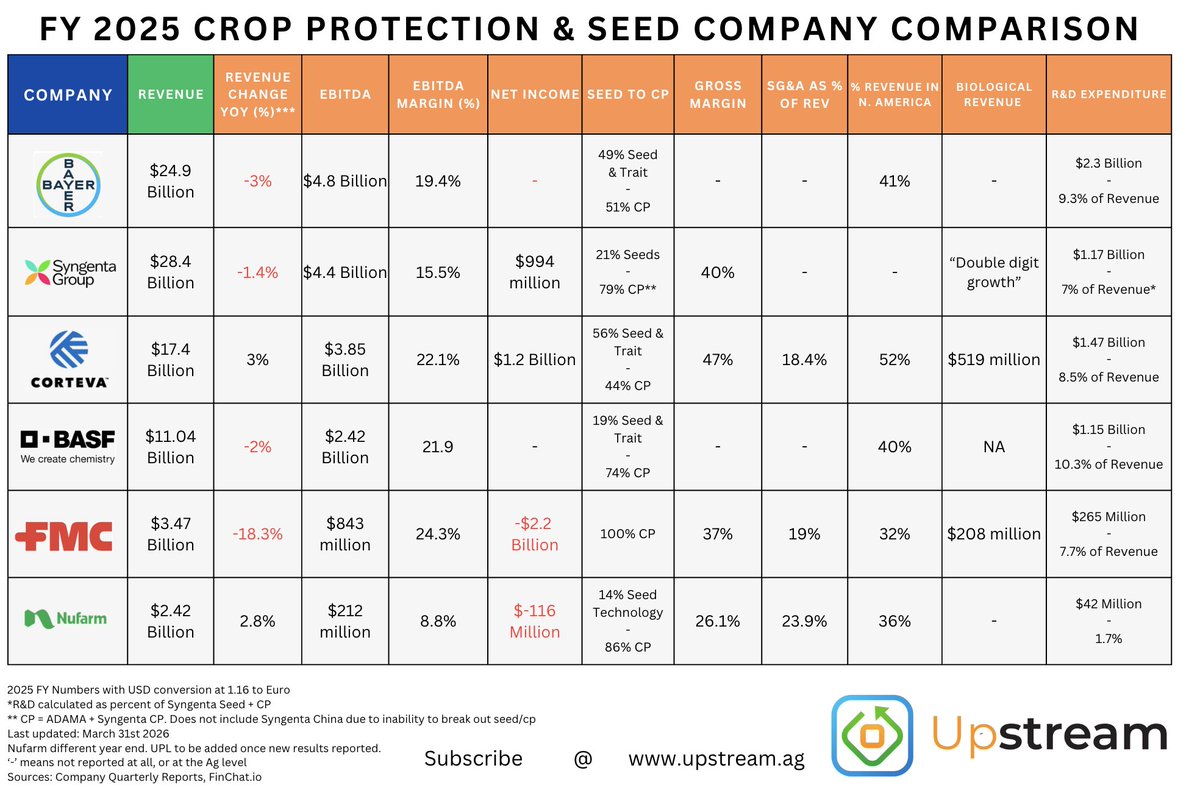

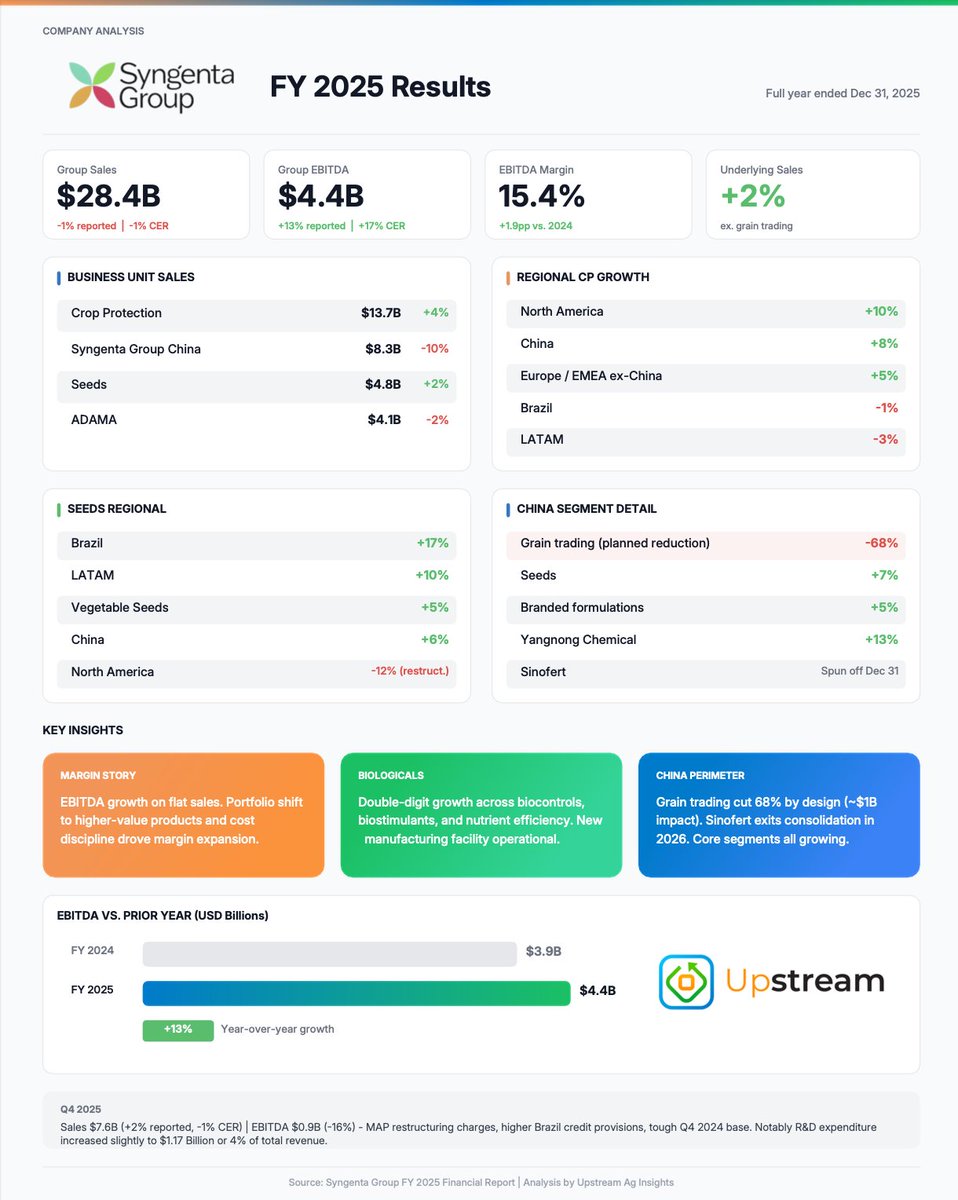

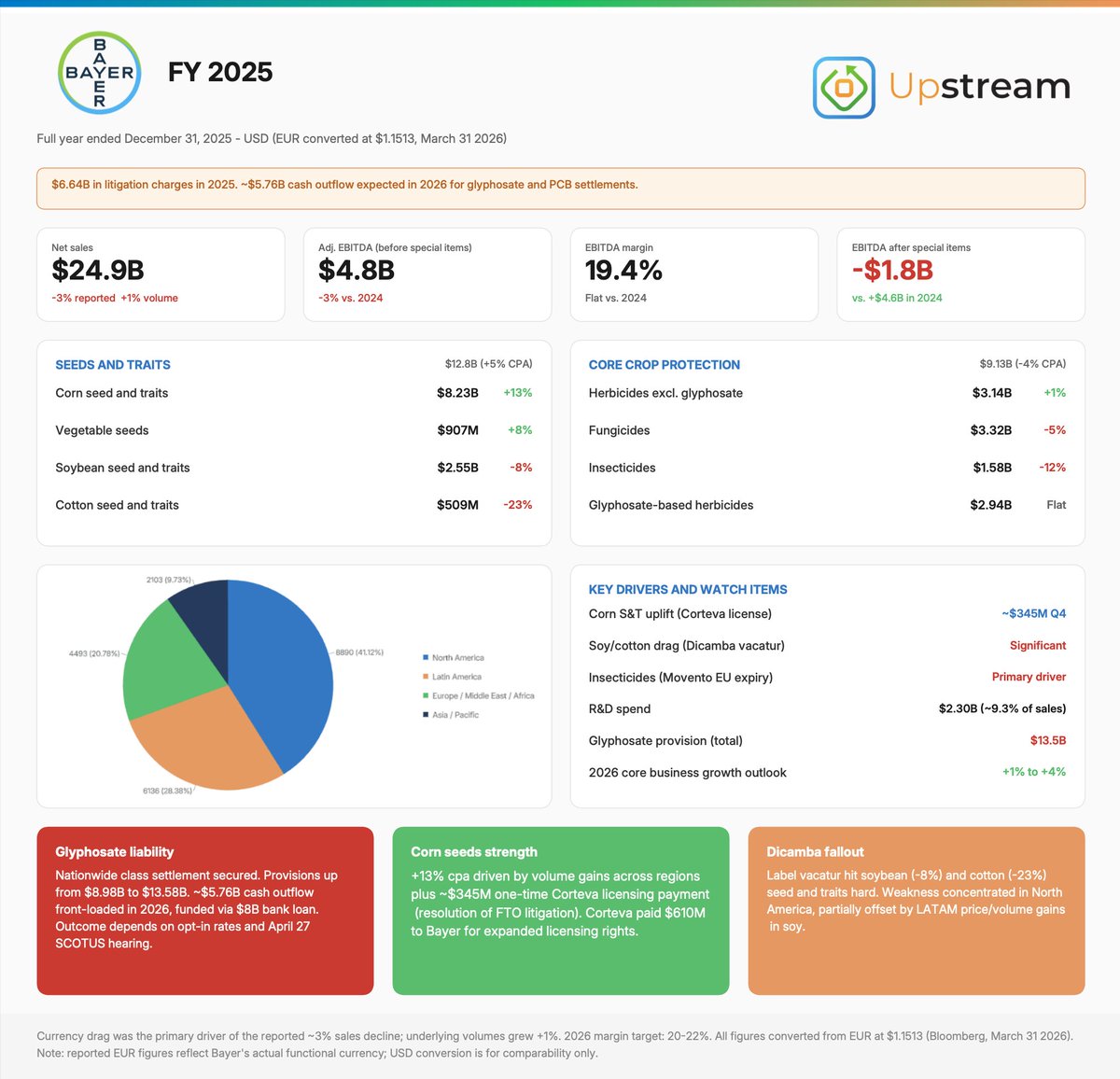

FY 2025 crop protection and seed results have all been reported, across @Bayer, @BASF, @corteva, FMC, @Syngenta, @UPLLtd, and @NufarmSeedsNA.

Several players were down, however, the crop protection market was viewed as more stable (before recent geopolitical events, anyways).

Channel inventories are normalized globally for the first time in a while, and for the first time in several years, the consensus view heading into 2026 is modest growth.

Volume is recovering, but generic competition has led to price challenges which have been more concentrated in Latin America and Asia Pacific, but seem likely to be a bigger concerns in North America in coming years.

A few other takeaways:

The major companies continue to emphasize biological capabilities on their earnings calls. Corteva hit $519M with 16% volume growth, but pricing hcallenged, particularly in LatAm, where 80 % of their bio rveneue occurs.

Syngenta delivered double-digit biologicals growth.

BASF acquired AgBiTech ahead of its planned IPO. FMC did not emphasize like they have historically, but shows how even though it is viewed as a growth priority, the core of their business is still chemistry and when challenges to the greater business arise, the focus remains on saving the core.

AI in discovery is continuing to be talked about, and I wil cover it more next week, but in the interim, Corteva described 1,000x faster active ingredient identification from molecular libraries. Regulatory submission preparation is also being compressed.

All companies flagged tighter farmer margins influencing purchasing behavior, even as underlying application demand stays consistent with historical levels.

For the full breakdown, check out the link below, or get quick hits for some companies in the @UpstreamAg images attached.

1

3

4

1,356

Upstream Ag retweeted

Mar 23

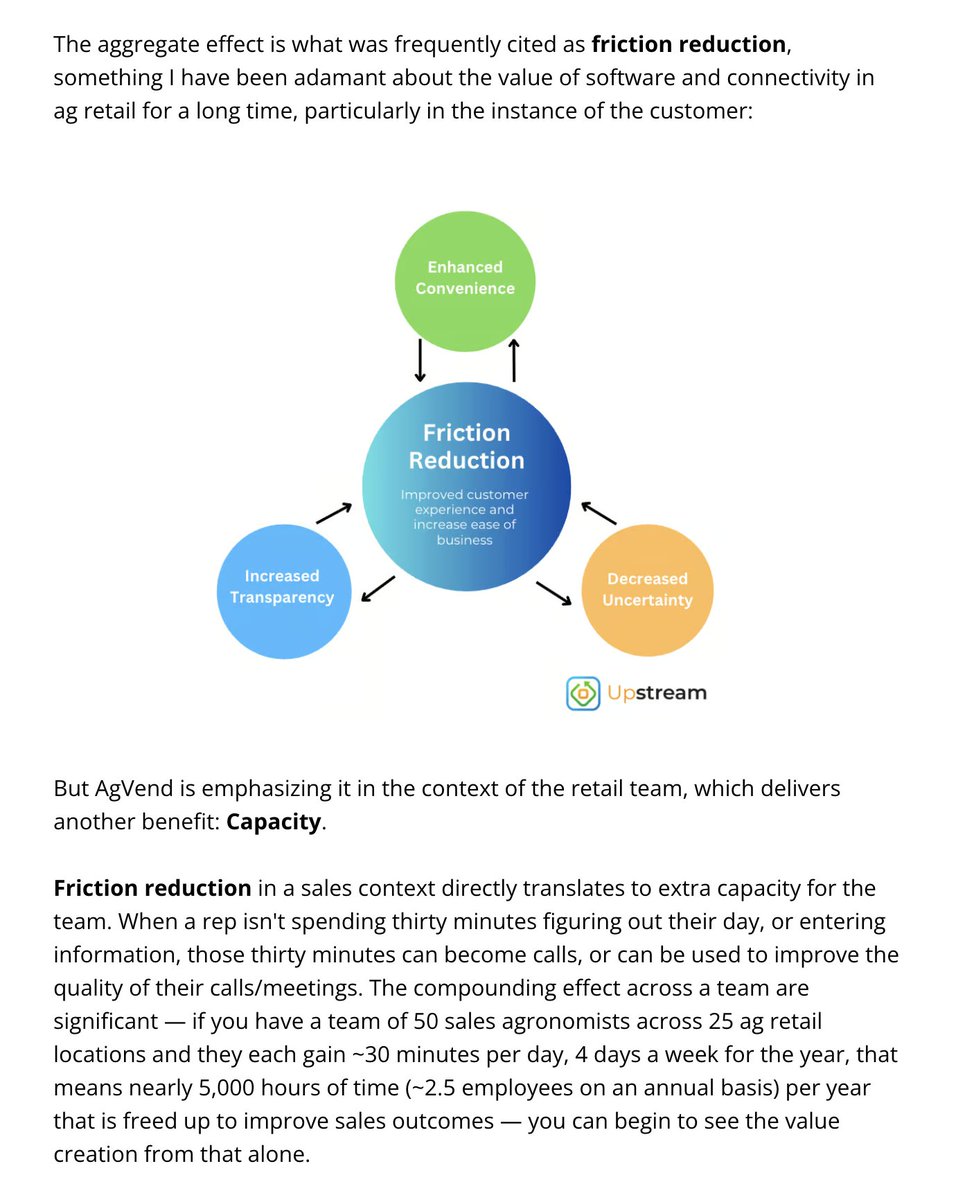

I recently spent time in Austin at the @AgVendHQ Partner Summit with over 250 industry leaders.

There was the usual talk of margin pressure and farmer profitability challenges, but what was most compelling to me was the sharing of the product roadmap.

I think the roadmap for a software company that penetrates 35% of the North American retail market provides an interesting signal into the future of ag retail:

What problems it believes are worth solving, where it's placing its bets, and if you read between the lines what it thinks the next chapter of ag retail looks like, including heavy emphasis on one of my favorite subjects, friction reduction, and team efficiency that leads to better outcomes for retails, crop input manufacturers and ultimately better results and experiences for farmers, too.

A few product components that caught my eye:

1. CRM and the Death of "Dead Time"

CRM initiatives in ag retail usually fail because data entry is tedious and the "next step" after entering data is never clear. AgVend is attacking this with a Voice AI Agent. Now, sales reps can now have a conversation with an AI agent while driving. The AI structures the notes, logs them, and creates tasks based on the conversation with the farmer, that is relayed to the agent.

2. Loyalty & Programming

Historically, retailer-led loyalty programs have been an Excel nightmare. By leveraging real-time transactional data, retailers can now embed incentives directly into the purchase flow and give customers an up to date understand of where they stand and how they can unlock further rewards. Interestingly, pilot results showed 25% higher agronomy spend among participants.

3. The Power of the "Control Point"

This is one of my favorite strategic concepts and I came across it a few years ago when I was trying to better understand what software strategy in agribusiness should look like. By owning the "Control Point"—the mission-critical software driving daily workflow—AgVend earns the right to integrate complex layers like Program Management (tracking those notoriously opaque manufacturer rebates) along with other capabilities, like their Nexus product suite, to be able to touch all points of the value chain.

When these products get utilized in ag retail, AgVend becomes what I would call Digital Infrastructure, for not only the retailers and cooperatives, but the value chain.

By solving for inefficiencies, such as misaligned forecasting, lagging incentive data, and slow reconciliation they can become an irreplaceable node between the manufacturer, the retailer, and the farm gate.

I’ve shared a full analysis of the roadmap, in the @UpstreamAg article.

1

3

6

830

Upstream Ag retweeted

Mar 2

Pivot Bio Releases 2025 Field Performance Data Demonstrating Consistent Yield Gains and Synthetic Nitrogen Displacement While Lowering Fertilizer Costs

◼︎◼︎◼︎

According to @pivotbio, In 134 field trials with 129 growers nationwide, corn producers using PROVEN® G3 replaced an average of 33 pounds of traditional nitrogen per acre and gained a 2.1 bushel-per-acre yield advantage as compared to the grower’s standard practices.

Overall win rates exceeded 90 percent, with consistent nutrition delivery at the plant root when the plants yield potential establishment is most critical, regardless of weather and soil type. This represents nearly a doubling of win rates in just two years.

I love when companies publish win rate data as a way to better understand product performance.

However, the win rate published in this release is higher than most win rates I have ever come across. That’s not inherently good or bad, but raises a few different possibilities:

Pivot Bio has become very good at understanding where their product works and where it doesn’t work, implementing trials and therefore, targets regions/fields accordingly.

In a high yield year like 2025, there may have been lot of farmers that did not fertilize enough given the yield potential.

There was a “cherry picking” of data points.

I reached out to Pivot Bio to learn more about what drove the results they published.

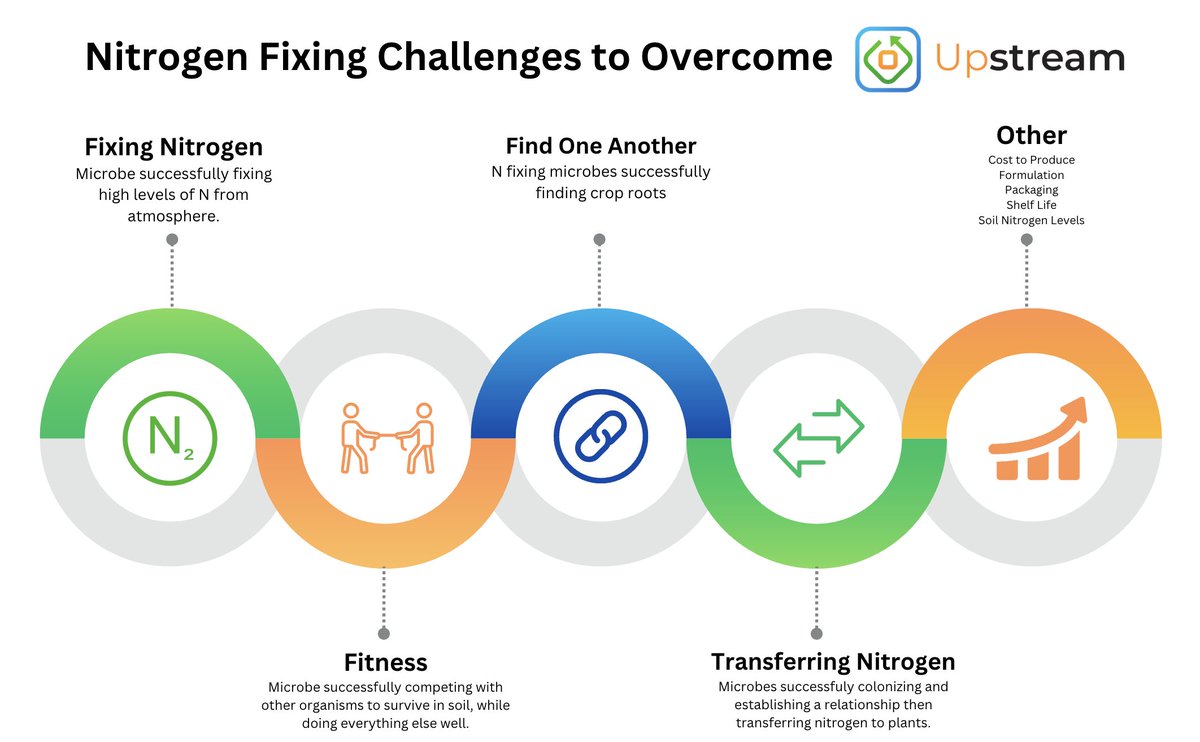

The Challenge

Nitrogen fixation from microbes involves multiple complexities to overcome, including some of the following (image attached)

That means a need to be diligent and thorough with everything from formulation, to packaging, to placement, to how it fits within the system context.

I have highlighted this across various publishings, including The Biostimulant Playbook and The Nuance of Biostimulants.

Once you have an understanding and positioning nailed down, the ability to effectively communicate that becomes crucial, along with having the discipline of saying “our products doesn’t fit there" when required.

When I reached out the first thing Pivot did was send me their Best Management Practices document.

The document gets into what is required to derive the best outcomes. I don’t think a piece of paper/bits is ever the sole driver of success as there is a need to set the expectations of staff, train staff, be disciplined to engage in the conversation, but I do think it shows there has been work and thought put in by the company itself, plus having a tangible document that drives conversations and can be referenced is a great ancillary tool to get farmers and agronomists thinking about the product in a way that is going to drive better outcomes.

What stood out to me after speaking with the Pivot team is that the win rate is not a story about a microbe suddenly getting better. What they changed was how they supported and positioned it.

Check out the link below for the full coverage. @UpstreamAg

5

3

6

1,626

Upstream Ag retweeted

Feb 27

A breakdown of @NutrienLTD, @corteva Agriscience, and FMC Corporation Executive Commentary from two major investor conferences this week:

The @BMO 35th Global Metals, Mining & Critical Minerals Conference and the @BankofAmerica 2026 Global Agriculture and Materials Conference.

These events these events are a goldmine of unique intelligence. Unlike quarterly earnings calls, which are often backward-looking and usually more tightly scripted, the conference Q&A sessions often surface unique commentary on things like demand trends, capital allocation priorities, and strategic efforts that don't make it into press releases or earnings calls.

Nutrien's Ken Seitz talked about retail efforts in Brazil, retail growth prospects in the coming years, targeted regions to expand, how they think about the financials behind tuck-in acquisitions, plus provides a prime example of reframing in a difficult situation.

Corteva Agriscience's Chuck Magro touched on biological ambitions, how the business is using AI internally beyond for discovery, business models for hybrid wheat and how he views competition from Bayer in soybean seed.

FMC Corporation's Pierre Brondeau clarified how they are thinking about licensing their technology and what their aspiration and targets for 2026 are even if there is no sale.

I break down all of their commentary, and more. Become an @UpstreamAg subscriber to get all of this direct to your inbox this Sunday.

3

1

4

1,932

Upstream Ag retweeted

Feb 25

There are a number of Banking Conferences this week in New York with public agriculture entities participating.

@NutrienLTD CEO Ken Seitz had an interesting question

surrounding Nutrien being “oligopolistic.”

In my mind, it isn’t really arguable that there is an oligopolistic structure in the industry. I have highlighted the dynamics in Monopolistic Inertia in Agribusiness (linked after)

However, I found his answer to the question to be a really notable reframe in a delicate situation where the CEO is needing to balance the perception of investors, meaning, Nutrien maintains being viewed as capable of delivering outsized returns, while not bringing on risk of unwanted government scrutiny.

I have highlighted this skillset from others within the industry previously in Control the Narrative, Own the Outcome: What Agribusiness Professionals Can Learn from Chuck Magro, David Friedberg and @JohnDeere (linked below as well).

Joel Jackson of BMO asked the following question:

"You talked about governments. There's a lot going on in the U.S. government, obviously, every day. But we see a lot of that impacting on the periphery of what you guys do, right? We see potash and phosphate, they're critical minerals. We see DOJ, USDA, let's go look at if there's oligopolistic structure, any kind of structures across crop inputs. Sometimes yourself and other peers get named. What do you think about all that? And does it mean anything for you?"

Ken Seitz said the following:

"Yes, it's definitely meaningful, and we take that all very seriously. I think what we say is that we exist in a highly competitive world. And that's just a fact. You see that in all of the work that we do on cost discipline and we can talk about mine automation in potash, for example, where we're making those investments so we can stay on the left of the cost curve because we need to compete."

Note that “competitive" and “oligopolistic” are not actually at odds with one another — an oligopolistic market structure can be intensely competitive. The key distinction is between market structure (how many firms) and competitive conduct (how they behave). An oligopoly is simply a market where a small number of firms control most of the market share, each usually very aware that their pricing and output decisions will trigger competitive responses, which means they react or strategize accordingly.

However, Seitz paints a picture that they are at odds with one another:

"We're talking about building a new terminal on the West Coast of North America, and that is related to costs and the need to compete. This is a highly competitive environment. It wasn't that long ago that if we're talking about potash prices, we're below that top producer at the end of the cost curve. Those things happen in a commoditized world. We go in when we get asked the question by any government go in and we say, here it is. This is a highly competitive market, a highly competitive world. We need to compete. These are the things that we do. And by the way, making investments to the tune of hundreds of millions of dollars every year to expand those volumes in a growing market, we make investments to add additional volumes to the market. And we can do that economically because of where we sit on the cost curve. So the story for us is you put that all together and you say, there's nothing in the form of anything untoward here. In fact, it's the opposite of that. We're doing everything in our power to compete."

That’s his job to do, and I think he does it well given the question effectively leaves him in a no-win situation. I think a lot of us can benefit from strengthening our ability to reframe a narrative.

My other takeaway: Everyone talks about summarization with AI being useful. I think it's really hard to derive the nuance of commentary if all one ever does is use AI to summarize everything. The edge and understanding is in the nuance.

@UpstreamAg

2

2

6

912

Upstream Ag retweeted

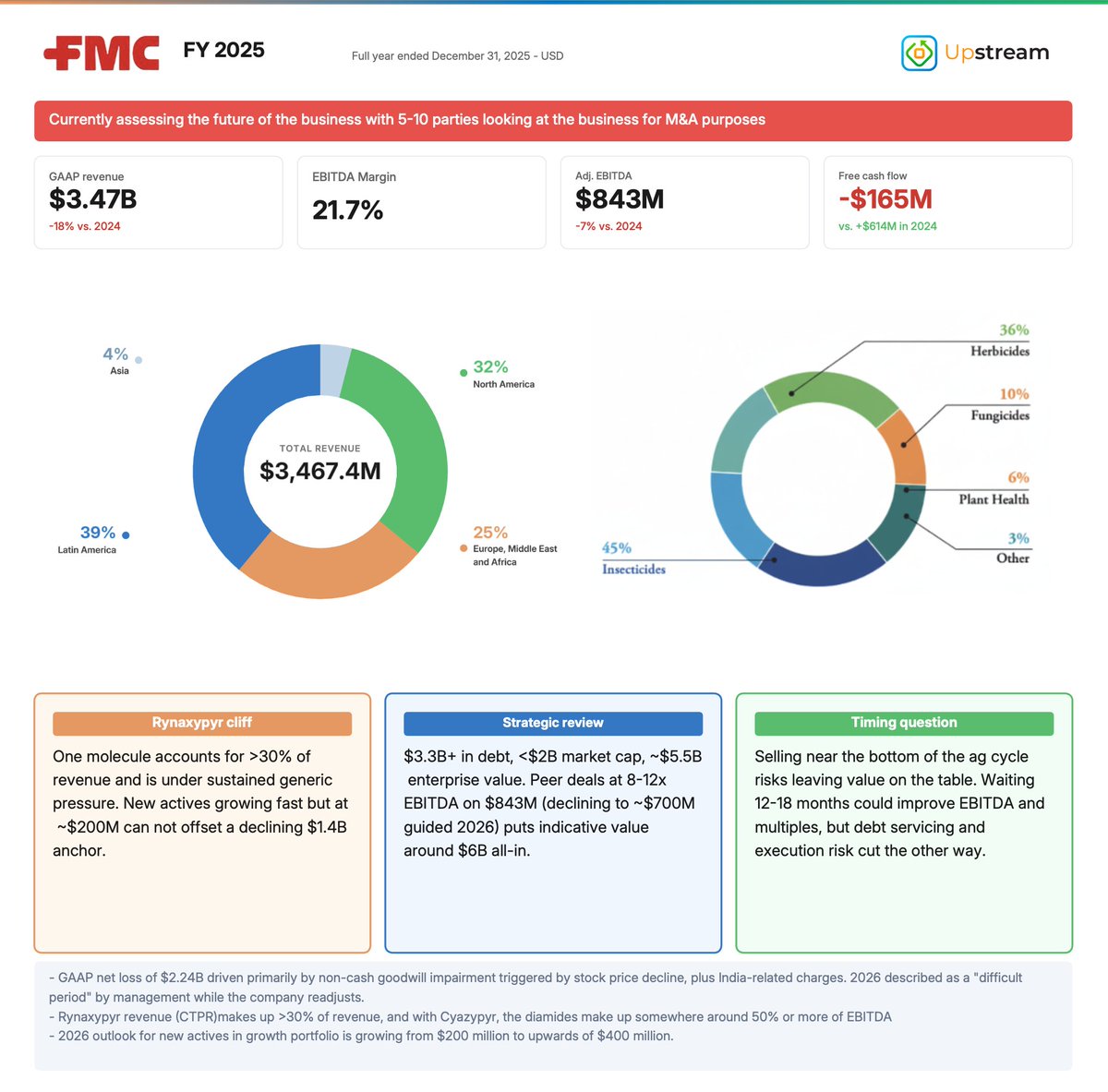

Feb 24

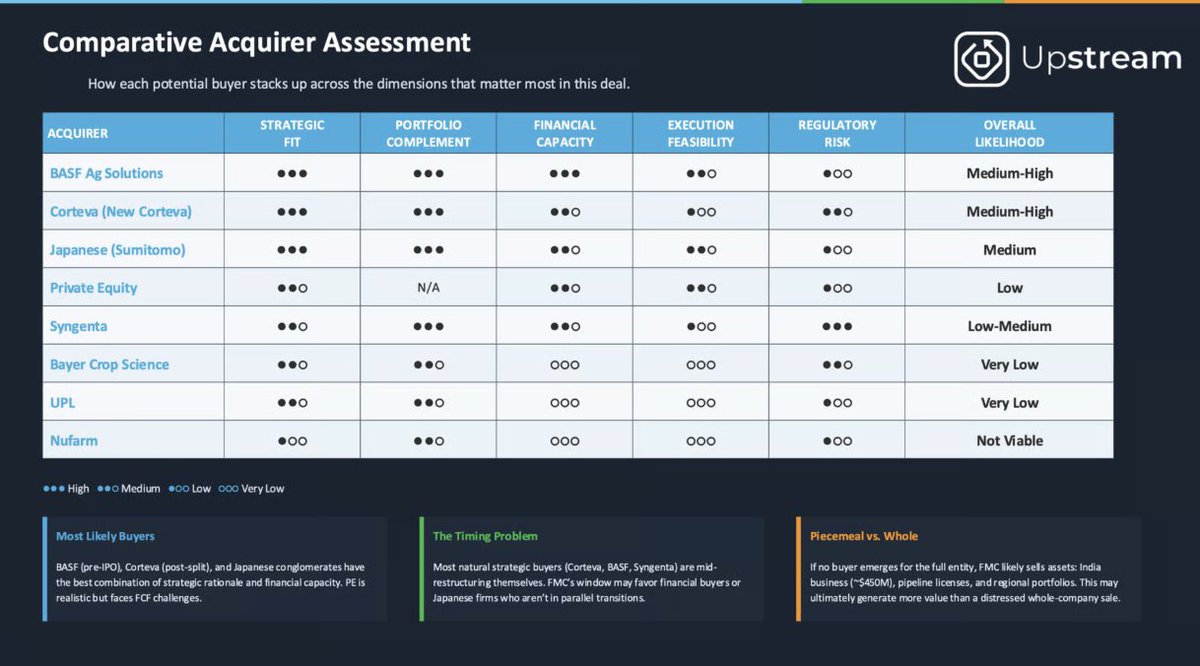

FMC's board authorized exploring strategic options, including a full sale of the business.

Here's a look at numerous different avenues for the business:

FMC generated $3.47B in revenue in FY25 (down 18% YoY).

The market cap sits at ~$1.8B, but enterprise value is ~$5.8B once you account for ~$3.5B in net debt for the full company or about ~8.3x EV/EBITDA. So it could take $6B to acquire the business outright.

What a buyer would get:

FMC has some strong assets in its portfolio and it's already the world's ~5th largest crop protection company with a pipeline targeting $2B in new revenue by 2035, a biologicals segment and new AI product sales growing 54% YoY.

The challenges are surrounding some of the off patent product segments, like Rynaxypyr patents expiringand significant chunks of the portfolio facing Chinese generic pricing pressure.

The other problem: nearly every natural buyer is in the middle of their own restructuring.

- @BASFCorporation is carving out its ag division for a 2027 IPO. One of the most logical fitson paper — FMC fills gaps across fungicides, herbicides, and insecticides, and strengthens the standalone innovation narrative for the spin. But bolting on a major acquisition mid-carve-out creates integration complexity.

- @corteva won't complete its split until H2 2026. Portfolio complementarity is strong, and there's already a fluindapyr collaboration. But buying FMC mid-separation is a big ask. Could they stomach it?

- @SyngentaGroup has portfolio fit but $24.8B in net debt, a pending Hong Kong IPO, and near-certain review given Chinese state ownership. @Syngenta

- @Bayer is financially nearly impossible. ~€32.7B net debt, 61,000 unresolved glyphosate claims (though getting closer to resolved), and a board with near-zero risk tolerance.

- Sumitomo Chemical is a dark horse. Their "Leap Beyond" strategy directs 80% of strategic spending to Agro & Life Solutions. FMC would make them a top-5 global CP player overnight, filling scale and geographic gaps in LatAm and North America.

- @UPLLtd has ~$2.6B net debt and the ongoing Advanta IPO process make taking on additional leverage unsustainable. They also announced a new structure for the crop protection segment. They could potentially participate in a piecemeal scenario, for example they may already be involved in FMC's India business sale (~$450M), but a full acquisition isn't realistic in their current financial state.

- Private equity has the fund sizes but FMC's negative FCF and regulatory complexity limit the typical LBO playbook.

The question goes beyond who should buy FMC strategically and really needs to focus on who's capable of it financially and can do something with it that FMC couldn't do on its own. That might mean accelerating the manufacturing restructuring, plugging the pipeline into a larger commercial engine, or absorbing the patent cliff with scale advantages.

If no buyer emerges for the full entity, a piecemeal breakup becomes possible.

Check out the full @UpstreamAg analysis with a downloadable acquirer overview and images.

1

2

6

852

Upstream Ag retweeted

Feb 23

Last week, @CNHIndustrial reported $244 million in technology related write-downs for 2025.

Two of them stood out specifically to me:

1. Raven Industries and a $123 million impairment (6%)

CNH acquired Raven for $2.1 billion in 2021. At the time, it was one of the largest bets in the industry, enabling them to bring various control and automation components in house while also acquiring novel autonomy capabilities. Now, CNH is writing down a meaningful chunk of that investment.

The other aspect around this too is that CNH competitor, @AGCOcorp, paid ~$2 billion for an 85% stake in @TrimbleCorpNews 's ag division and wrote that down by ~$350 million last year.

Even though the impairments come during a down turn, it sends a signal that product adoption in precision ag and synergy assumptions have not materialized at the pace that justified the investments.

It reinforces the challenges for all precision tech in the industry and likely signals apprehension to pay up for future acquisitions, whether from equipment manufacturers, or others in ag. A slide outlining some of the assumptions from 2021 attached.

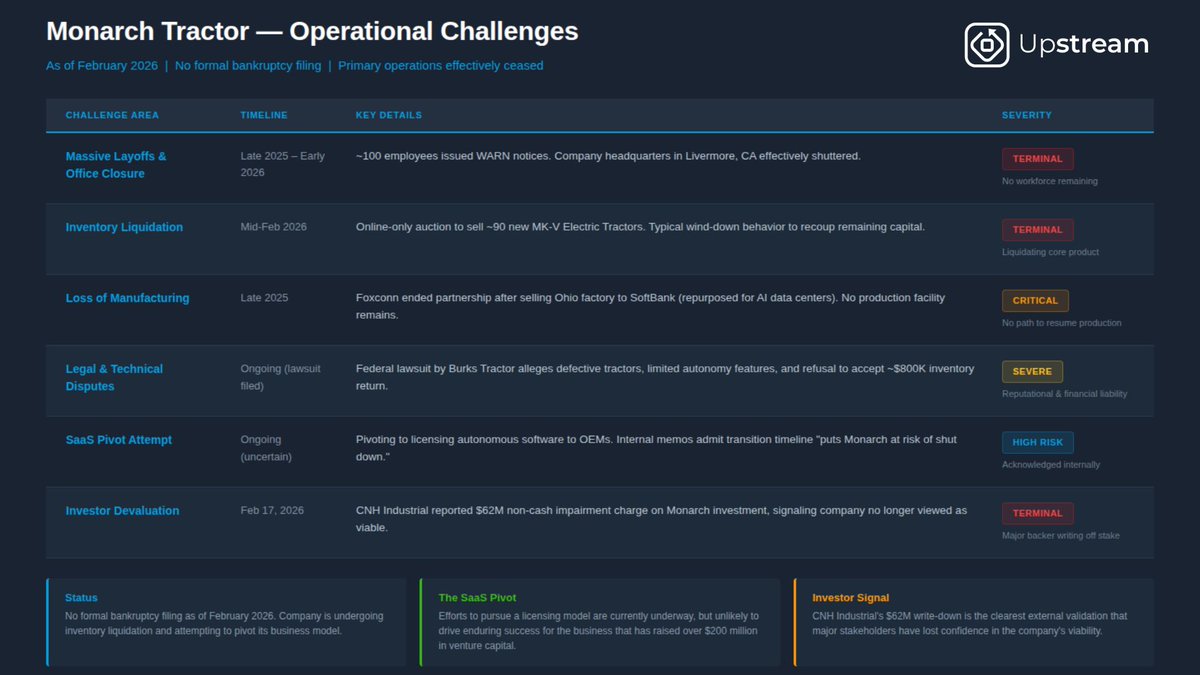

2. @MonarchTractor and a $62 million impairment

This one is notable given everything going on with Monarch, which confirms that Monarch is probably going to zero.

CNH's partnership with Monarch was comprehensive and was part of a multi-faceted tie up between the two companies.

It started with a minority stake in Monarch's Series A, followed by a Series B investment. Then CNH signed an exclusive licensing agreement, granting rights to integrate Monarch's electrification and autonomy technology into low-HP Case IH and New Holland tractors. In May 2023, they expanded the relationship further with a financing arrangement through CNH Industrial Capital, allowing farmers to purchase Monarch equipment directly.

This was the tightest partnership that CNH had in precision ag besides outright acquisitions, such as with Augmenta.

Monarch is now auctioning off unsold tractors, its manufacturing partner is gone, and the company is reportedly attempting a pivot to SaaS. On top, CNH is writing down the investment by $62 million.

The $244 million in technology write-downs also includes a Bennamann write-down of ~$50 million.

When we add AGCO's Trimble impairment we can effectively see ~$600 million in precision ag value destruction across just two companies in the last year, not to mention all of the other sells offs, such as Corteva Agriscience with Granular assets or Valmont Industries, Inc. with Prospera, or other now defunct entities beyond Monarch and VC dollars.

The challenges for precision ag as a value creator seemingly continue. While interviews of VCs on @agfundernews there is some optimism about the future, there is seemingly more signal of growing apprehension from potential acquirers to make large investments.

@UpstreamAg

6

11

38

12,017

Upstream Ag retweeted

Jan 25

@UpstreamAg shared a timely article about AI and ag retail today. I can only wonder if AAFC and other government departments have looked to these tools as a means for cost savings in their vast bureaucracies before shuttering infrastructure. Good idea?

1

4

287