Content Writer || Moderator || Community Builder || Ambassador of @GenesysChain || Crypto Trader || Empowering Web3 Communities || Airdrop Hunter ||

Joined December 2024

- Tweets 8,750

- Following 1,048

- Followers 1,279

- Likes 12,692

1,058 Photos and videos

Pinned Tweet

Feb 16

Hey Crypto Fam My Name is King Useeph I Joined Web3 Space to build real value not just to follow trends or noise.

I Working With Project like @MidnightNtwrk, @GenesysChain, and partnerships with @MGBX_Global I’ve contributed to growing communities that don’t just expand in numbers, but in trust, purpose, and long term vision.

My goal is simple to help projects turn ideas into strong onchain communities As a content Writer, Moderator, in the crypto space I focus on what truly matters clear communication authentic Moderator, meaningful content, and sustainable growth.

Web3 isn’t just about technology it’s about people, stories, and shared vision Let’s build strong and lasting projects together

DM @Useeph001 for collaborations, partnerships, or project promotion ✅

122

107

219

2,598

King Useeph 👑 retweeted

I've been thinking about the quiet frustration so many of us in crypto share.

You close a deal, deliver work, or trade your way into USDT or USDC. The payment lands and for a moment it feels like freedom. Then you actually need to use that money pay for tools, subscriptions, travel, support family across borders and the old system pushes back. Conversions, waiting periods, extra fees, random card declines, and banks that still treat crypto like suspicious activity.

It turns what should be borderless money into something that feels stuck behind legacy rails. For freelancers, creators, and Web3 builders receiving payments from around the world, this friction doesn’t just annoy it slows down real adoption.

That’s what stood out about @zerrapay Card.

WHAT ZERRA CARD DOES

Zerra Card lets you spend USDT and USDC instantly anywhere Visa is accepted without needing a traditional bank account or multiple conversion steps. You fund directly with stablecoins on BNB Chain (BEP20), and the balance converts to fiat in real time for spending.

• Works in 100 countries

• Apple Pay & Google Pay supported

• Virtual card available right after KYC

• Physical Black and Carbon tiers with ATM withdrawals

• High limits up to $40,000 per tap

THE REAL EARN & SPEND ADVANTAGE

What genuinely sets Zerra apart is the automatic Zerra Ventures membership that comes with every card.

Most crypto cards stop at spending. Zerra connects earning and spending in one flow you can participate in investment opportunities through their Ventures platform when you choose to, and any returns you generate are immediately spendable through the same card no extra bridging or delays.

There’s no obligation to invest. You only participate when you want to. But when you do generate returns, they don’t sit in another app. They flow straight into the balance you already use for daily life. This turns the card from a pure spending tool into infrastructure that lets your earnings and your spending reinforce each other inside one simple system.

TRANSPARENT PRICING NO HIDDEN MARKUPS

In an industry full of “zero FX” claims that don’t tell the full story, Zerra has been refreshingly direct. Standard network and bank fees on international transactions exist for any card. What they control and don’t add hidden markups to is their own issuer fees.

• Virtual — $100 one-time → 1% cashback (up to $100/month)

• Black (physical) — $500 one-time → 2% cashback (up to $150/month)

• Carbon — $1,000 one-time → 3% cashback (up to $200/month)

Straightforward tier pricing. No monthly charges. Transparency like this builds trust faster than any marketing slogan.

For anyone navigating Web3 earnings across borders or in markets where traditional finance moves slowly, this kind of practical bridge matters. Your stablecoins stop being something you only hold or trade. They become money you can actually live with instantly, globally, and with an optional path to make them grow while you spend.

If you’re looking for a cleaner way to connect on-chain earnings with real-world spending without the usual headaches, Zerra Pay is worth exploring.

For more information go to zerrapay.com

@zerrapay

I’m genuinely curious what’s the one thing that would make spending your crypto earnings feel truly seamless in your day-to-day life? Drop your thoughts below. The more we talk about actual usability, the faster we move past the friction. 👇

#ZerraCard #CryptoPayments #BorderlessPayments #Web3Utility #SpendStablecoins #EarnAndSpend

4

2

4

22

King Useeph 👑 retweeted

Jun 12

I have spent years analyzing crypto markets and observing how creators share their insights.

During this time, I noticed something important: most valuable content goes unrewarded.

What drives me most is helping creators turn their work into real rewards and new ways to earn online.

@clashoAi is a meritocratic advertising platform where the best content wins.

It transforms creator marketing into a measurable, competitive market where brands launch campaigns and creators compete by producing content.

The platform measures real influence across attention, engagement quality, sentiment, audience relevance, and verified outcomes.

Payouts are tied directly to performance, so the creators who generate the most valuable attention earn the most.

If you're the one of creators who post insights, predictions, and analysis, but they are not getting rewarded for what they have posted.

And you want to change that, Clasho offers the solution.

Earn from the content you’re already creating around crypto and markets?

Let me explain it simply.

@clashoAi backed by OpenAi, Starbuck, poly market and Arcadia which has already distributed millions $$ to creators.

How it works:

→ Creators earn upfront payments just for posting.

→ Additional rewards are based on performance (likes, shares, clicks).

→ No minimum follower requirement any active creator can participate.

Current opportunities:

→ $25K reward pool live.

→ Polymarket activations starting soon.

→ Early access is limited: only 1,000 verified spots versus 250,000 on the waitlist.

Why it matters:

→ Monetize the activity and insights you are already producing.

→ Build a track record of rewarded content in crypto prediction markets.

→ Early users get first-mover advantage in an attention-based economy.

If you create content in crypto, markets, or prediction spaces, this is a big opportunity to turn your influence into direct income while building your reputation on Clasho.

Learn more and join early access: clasho.com

100

3

181

3,440

King Useeph 👑 retweeted

Jun 11

⚽️ GIVEAWAY FLASH COUPE DU MONDE ⚽️

Saurez-vous prédire la minute du PREMIER BUT du match d’ouverture ? 👀

🎁 50 $ de récompenses

💰 5 gagnants × 10 $

Comment participer :

1️⃣ Suivez @WEEX_French

2️⃣ Repostez ce post

3️⃣ Rejoignez le Telegram : t.me/WEEXFrench

4️⃣ Taguez 3 amis qui ne nous suivent pas encore, puis commentez votre prédiction ci-dessous avec votre UID WEEX

Exemple :

👉 17’

👉 64’

📅 Fin du concours 10 minutes avant le premier but marqué.

📅 Heure du match : 20h CET

Seuls les vrais cerveaux du football seront assez rapides 🔥

#WEEX #WorldCup2026

96

97

108

1,156

Jun 12

GM ☕ Waking up healthy is something I never take for granted. Have a great day everyone h

3

Jun 12

GM ☕ Waking up healthy is something I never take for granted. Have a great day everyone.

1

King Useeph 👑 retweeted

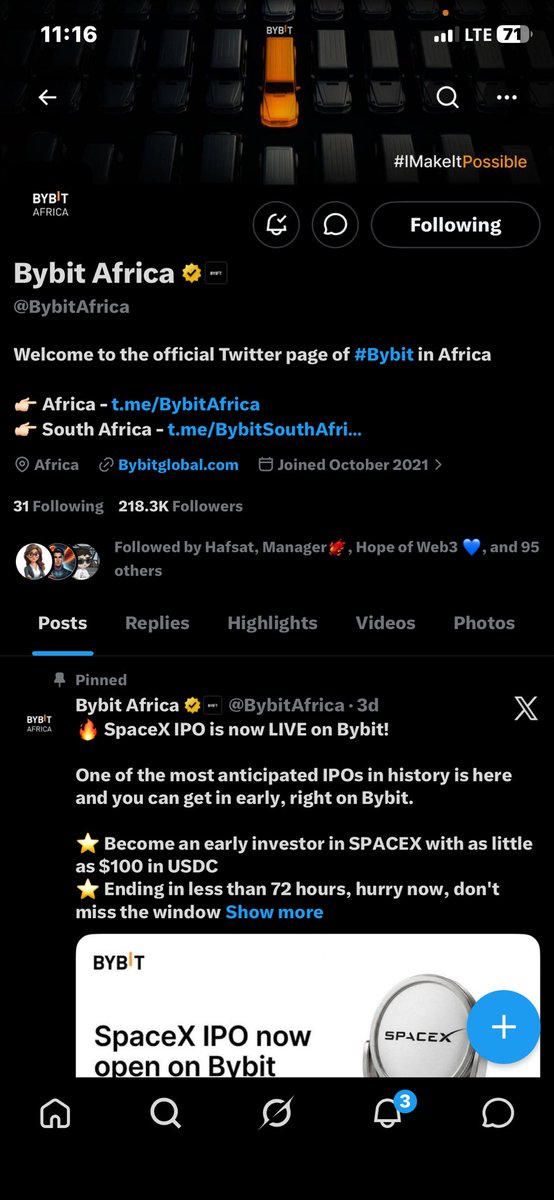

Jun 10

🥳 Your favorite stocks are now open on Bybit

Name all 10 and win from a 200 USDT prize pool 🎁

How to enter:

✅ Follow @BybitAfrica and turn on post notification

✅ Retweet this post & tag 3 friends

✅ Drop all 10 tickers UID in the comments

476

454

557

14,185

Jun 9

GM ☕ Waking up healthy is something I never take for granted. Have a great day everyone gs

1

Jun 9

GM ☕ Waking up healthy is something I never take for granted. Have a great day everyone h

6

Jun 9

GM ☕ Waking up healthy is something I never take for granted. Have a great day everyone g

5

Jun 9

GM ☕ Waking up healthy is something I never take for granted. Have a great day everyone

3

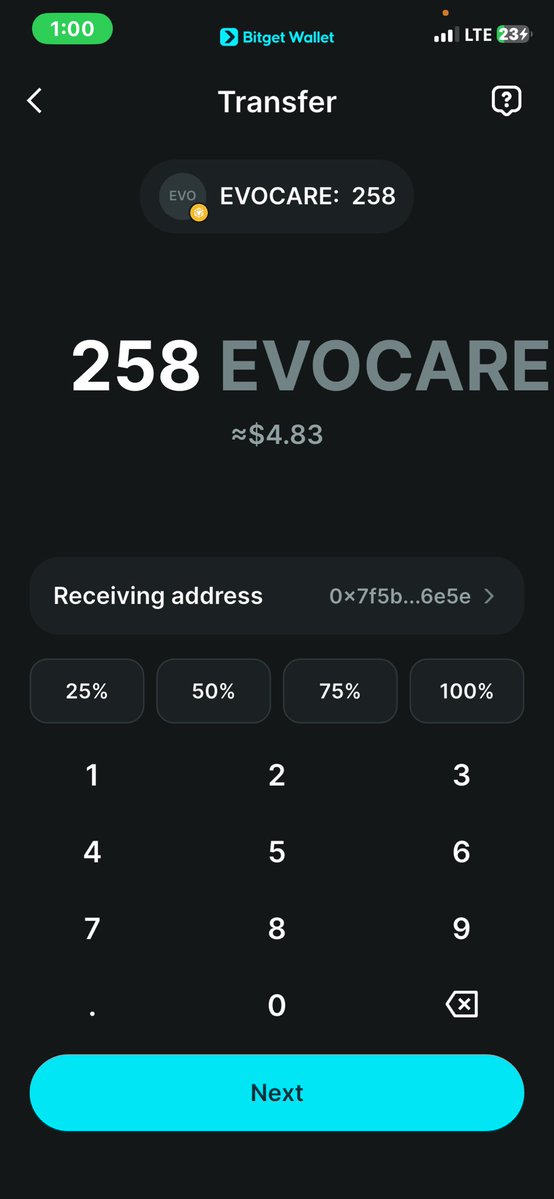

Jun 5

Congratulations to me ✅🎉

I won 258 $EVOCARE from a giveaway back in April, but it wasn’t listed at the time Today, I checked and saw that it has finally been listed so I sold my tokens

Thank you @Telemedizin ✅✅✅

5

Jun 3

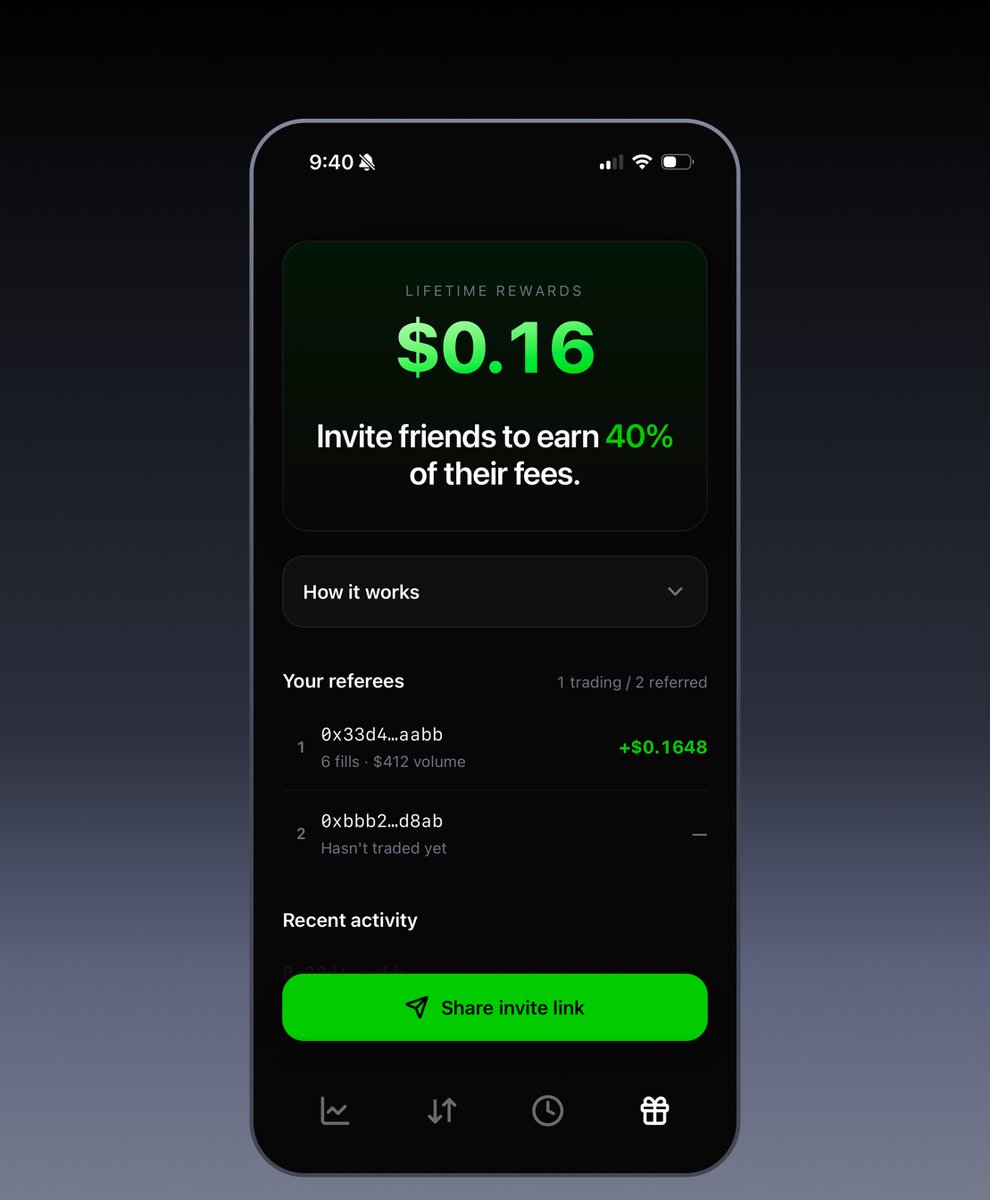

I’ve been using 10X Trading and it’s worth checking out. Sign up with my referral link: [YOUR REFERRAL LINK] 🚀

You’ll get access to the platform, and once registered, you can share your own link and earn 40% of the trading fees generated by your referrals. #10XTrading

Jun 3

Referrals are live, heres how it works:

Share your link anywhere. If folks click it and sign up you get 40% of their lifetime trading fees. Its that simple.

Share your link with friends, post it, or pin it to your bio to start generating a new stream of income!

Grab your link from the 10X Trading app now.

13

Jun 3

I’ve been using 10X Trading and it’s worth checking out. Sign up with my referral link: [YOUR REFERRAL LINK] 🚀

You’ll get access to the platform, and once registered, you can share your own link and earn 40% of the trading fees generated by your referrals. #10XTrading

x.com/i/status/2062033291541…

Jun 3

Referrals are live, heres how it works:

Share your link anywhere. If folks click it and sign up you get 40% of their lifetime trading fees. Its that simple.

Share your link with friends, post it, or pin it to your bio to start generating a new stream of income!

Grab your link from the 10X Trading app now.

5

Jun 2

- I’m 18.

- Muslim.

- Mom is alive.

- Dad is alive.

- Im not graduate.

- Im Single.

- I don’t drink.

- I don’t smoke.

- Not looking for government job.

- Earning from web3 jobs and trading.

Alhamdulillah 😊😊😊

- I’m 24.

- Muslim

- Mom is alive.

- Dad is alive.

- I graduated.

- I got married.

- I don’t drink.

- I don’t smoke.

- Not looking for government job.

- Earning from web3 jobs and trading.

Alhamdulillah.

1

21

King Useeph 👑 retweeted

May 27

🌙🕌 EID MUBARAK 🌜🕌

May Allah accept our prayer forgive our sins

and fill our lives with happiness peace and endless blessings 🤍

3

2

8

143

May 27

Why @ston_fi Deserves Attention in DeFi

In a space where many platforms rely heavily on hype STON.fi stands out by focusing on simplicity and real usability Built to make decentralized finance more accessible it provides users with a smoother way to swap assets explore liquidity opportunities, and interact with DeFi through a cleaner experience

What creates long-term value in crypto isn’t short-term excitement it’s consistency utility and user experience @ston_fi is gradually becoming part of the conversation among users who value speed simplicity and a more user-friendly DeFi environment

The crypto market moves fast, and experienced users understand that research matters more than hype Learning how platforms work understanding risk management, and exploring opportunities carefully will always be more important than chasing trends

As DeFi continues to evolve platforms focused on simplicity and accessibility may play a stronger role in helping more people participate with confidence

15

7

19

125

May 26

STON.fi Trade Smart Earn More

Crypto is evolving, and @ston_fi is making the journey smoother than ever

✅ Fast and seamless swaps

✅ User friendly experience

✅ Built for the $TON ecosystem

✅ Smarter way to explore crypto opportunities

Why settle for complicated when you can keep it simple with STON.fi ?

The smarter move starts here

20

8

23

145