Investor, Entrepreneur, Lifelong Learner. Founder of VMF Research, delivering institutional-grade research tailored for self-directed investors.

Joined April 2024

- Tweets 293

- Following 210

- Followers 149

- Likes 238

119 Photos and videos

Pinned Tweet

30 May 2024

VMF Research is an independent, evidence-based investment research company dedicated to helping self-directed investors find their edge. Empower your Investment Process and expand your Financial Literacy. (Not Investment Advice)

7

2,892

In May, almost everything we published at VMF Research revolved around one uncomfortable question: What should investors do when the market has already discovered the obvious winners of a great theme?

In this case, the theme was AI.

The first stage of the trade has been increasingly well understood: semiconductors, memory, data centers, power, grid infrastructure, cooling systems, and the physical capacity required to sustain the AI buildout. These areas still matter enormously, but the market is no longer ignoring them. In many cases, it is already paying a very visible price for them.

So May became less about asking whether AI is real, and more about asking where the mispricing may still live.

That trail took us from the visible AI bottlenecks to the forgotten application layer; from broad China internet exposure to PDD as a direct stock-level expression; and finally to Alpha Tier’s “Tulip Test”, where we asked whether the first AI trade had become crowded enough to justify a different risk budget.

To make that progression easier to follow, we just published a new “Inside VMF Research” piece.

Think of it as a reading guide to our May work.

It connects the public Substack excerpts we released during the month (from “The Visible Side of the AI Boom” and “The Forgotten Application Layer” to “PDD: China Price, Temu Optionality” and “A Pattern Recognition Exercise”) and shows how they fit into one coherent investment process.

For free readers, it is the best place to understand the arc of our thinking.

For paid subscribers, May included the full implementation behind that arc: vehicle selection, position sizing, valuation work, portfolio changes, liquidity adjustments, and the monitoring framework we will use from here.

May was not a retreat from AI.

It was a rotation inside AI... away from what the market can now see clearly, and toward the areas where judgment still matters most.

marketview.vmfresearch.com/p…

35

Our Weekly Update is OUT! 🛎️

One of the strongest pillars supporting our Great Acceleration thesis has always been the labor market. And last week, it delivered another important piece of evidence.

The latest employment report came in far stronger than expected, with nonfarm payrolls rising by 172,000 versus consensus expectations of just 88,000.

Better still, previous months were revised higher and wage growth remained relatively contained. In other words, the economy appears to be accelerating without the kind of wage pressures typically associated with an inflationary boom.

Yet the market’s reaction was anything but constructive. Virtually every major asset class sold off as investors rushed to price in a more hawkish Federal Reserve. Treasury yields jumped, equities fell, precious metals weakened, and Bitcoin, one of the hardest-hit assets of the day, retreated sharply as traders suddenly began entertaining the possibility of additional rate hikes later this year.

The reaction was severe enough to draw a response from President Trump himself.

And while we rarely focus on political commentary, his remarks reveal that he understands exactly what happened….

Read it in full:

marketview.vmfresearch.com/p…

23

This…

Jun 12

Occasionally I get shit for being so pro-Elon.

3 big reasons why:

#1 He's done more for free speech than Congress who swore to defend it -- both parties.

This matters because America sets the global Overton. And without free speech humanity are sheep to the slaughter.

#2 He's our greatest innovator since Thomas Edison.

When I used to teach MBA Steve Jobs was the ultimate innovator. Jobs -- who invented nothing -- can't touch Elon.

#3 The problems Elon's tackling are among most important.

A lifeboat for humanity, existential risk from AI, the survival of truth, demographic collapse. This isn't colored Macs.

1

17

The SpaceX IPO will create a thousand instant experts today. Valuation experts. Space experts. Starlink experts. IPO experts. People who had almost nothing to say about the company six months ago will now have fully formed opinions on its market cap, its growth runway, its risks, and its place in the future of the global economy.

That is how markets work...

The crowd usually arrives after the story becomes impossible to ignore.

At VMF Research, we try to do the work before that happens.

Back in January, we framed SpaceX as one of the probable highlights of 2026.

Not after the IPO headlines.

Before them.

We published in-depth research on how investors could gain exposure to SpaceX before the public listing, through a listed vehicle that, at the time, was trading at a meaningful discount to the value of its underlying private holdings.

That same vehicle also offered exposure to other exceptional private businesses that may define the next wave of mega IPOs, including Anthropic and Revolut.

That is the bigger story.

The world of alternative assets is no longer reserved for endowments, sovereign wealth funds, venture capital insiders, and billionaire family offices.

Self-directed investors can now build exposure to some of the best private businesses in the world.

But access alone is not enough.

You still need to know where to look, how the vehicle works, whether you are buying at a discount or a premium, how to size the position, and how it fits inside a broader portfolio.

That is the rise of the self-directed investor.

Not chasing every headline. Building a more sophisticated portfolio before the headline arrives.

Today, SpaceX is the story.

In January, it was already part of our research process. That is the work we do at VMF Research.

Good investing!

BREAKING: SpaceX priced the biggest-ever U.S. initial public offering at $135 per share, raising $75 billion on the sale of 555.56 million shares, valuing the space, satellite and AI provider at $1.77 trillion, a record for an initial offering reut.rs/4gfBJ6P

1

204

Jun 10

You will live in the pod, eat the bugs, use the only AI, and live on UBI.

2

31

This...

Jun 10

There are three vitally important components to each trade

-Timing

-Direction

-Sizing

Get any one of these wrong and the trade is wrong

All three need to be correct

1

29

Our new Leaderboard update is live, and the headline is simple: we acted. A position that more than tripled in less than 18 months has now been fully exited from our Model Portfolios. Final result: 238%

That is not a typo.

A position that more than tripled in less than 18 months has now been fully exited.

And the reason is no mystery.

We have been writing about it both in front of and behind the paywall: the visible side of the AI Trade is getting crowded.

Semiconductors have gone parabolic.

EWY’s heavy exposure to South Korea’s AI-linked hardware champions (including SK Hynix and Samsung) has been an extraordinary tailwind.

But markets have a way of changing character...

What begins as a differentiated thesis can eventually become consensus.

What begins as a powerful trend can turn into a crowded trade.

And what begins as opportunity can, at the wrong price and sentiment extreme, become risk.

Check our top 10 positions on the link below.

marketview.vmfresearch.com/p…

1

44

When I launched @VMFResearch , the biggest challenge was avoiding being confused with just another newsletter. The goal was never to comment on daily market chatter, but to build an independent research platform with institutional standards and a global scope. Credibility isn't something you claim. It's something you earn through consistency and absolute accountability.

The market doesn't have a data problem. The real problem is separating the signal from the noise. Information is just raw material. An actual insight is information filtered through a strict process, tested against reality, and turned into an actionable judgment.

--- (PT)

Quando fundei a VMF Research, o maior desafio foi não ser confundido com mais uma newsletter. A nossa ambição nunca foi comentar o ruído do dia, mas sim construir uma plataforma com padrões institucionais e vocação global. O mercado não sofre de falta de dados. O problema é distinguir o sinal do ruído. Informação é apenas matéria-prima. Insight é informação organizada por um processo, testada contra a realidade e transformada em juízo acionável.

1

32

This…

Novice and aspiring market speculators think the magic is found in trade identification.

The "what" and "when" components of trading -- while necessary -- represent only about 5% of a trader's "edge."

Yet aspiring traders spend 80% of their time, energy, hopes and fears on trade identification and the next trade.

The real landmine in trading is self-sabotage. Dealing with human emotions is the battle line that matters.

You want to know yourself, I mean really know yourself -- the good, the bad and the ugly?

Become a trader.

This is why all the trading services who talk about their last trade (made 250% on XYZ) is such an absolute joke.

Trading services who talk about their winners are trading services you must avoid at all costs.

The real enemy in trading is self.

You want to know your biggest enemy to trading success? Well, just look in a mirror. It is you, not what you know or don't know, that keeps you from gaining traction in trading.

After three to five years of experience a person should know what they need to do to be profitable. The challenge is actually doing what you know you must do.

The task is overcoming self.

1

31

This...

Jun 6

The jobs report was a barnburner. Nonfarm payrolls increased by 172,000 versus expectations for 88,000, while prior months were revised higher by 93,000. Wage growth came in at roughly 0.3%.

Yet the market sold off.

In our view, the market is misreading the signal. It is assuming that stronger than expected employment and growth will cause a an acceleration in inflation. History would suggest otherwise.

Productivity growth is running near 3%, while unit labor costs are hovering around 0.5%. Those are not the hallmarks of an inflationary boom. They are the hallmarks of healthy, productivity-driven growth that will lower inflation.

Meanwhile, the yield curve continues to flatten despite a roughly 55% increase in oil prices year-over-year based on a three month moving average. In past cycles, an energy shock of this magnitude steepened the yield curve when the Federal Reserve was accommodating it. Instead, the bond market appears to be discounting something much more powerful: the deflationary impact of technological innovation, particularly artificial intelligence, which is beginning to increase productivity across broad swaths of the economy.

If tensions with Iran ease and oil prices retreat, we believe inflation could move into negative territory before year-end.

In our view, the Fed made a historic policy error when it raised rates aggressively into what was largely a supply-driven inflation shock in 2022. We do not believe the next generation of monetary policymakers will be eager to repeat that mistake.

Notably, gold peaked on the day Kevin Warsh was appointed. The inflation trade may already be behind us.

If our research is correct, the next phase of this cycle could be characterized by accelerating growth, declining inflation, falling interest rates, and a strengthening U.S. dollar. That combination would create a remarkably supportive backdrop for innovation-led equities and the technologies driving the next productivity boom.

I discuss this framework in greater detail in this month’s episode of In The Know.

1

30

Our Weekly Update is OUT! 🛎️

The market focused almost entirely on who AI might replace. It paid far less attention to who would help companies deploy, manage, govern, and monetize AI at scale.

That distinction is now becoming visible in price.

$IGV

marketview.vmfresearch.com/p…

1

40

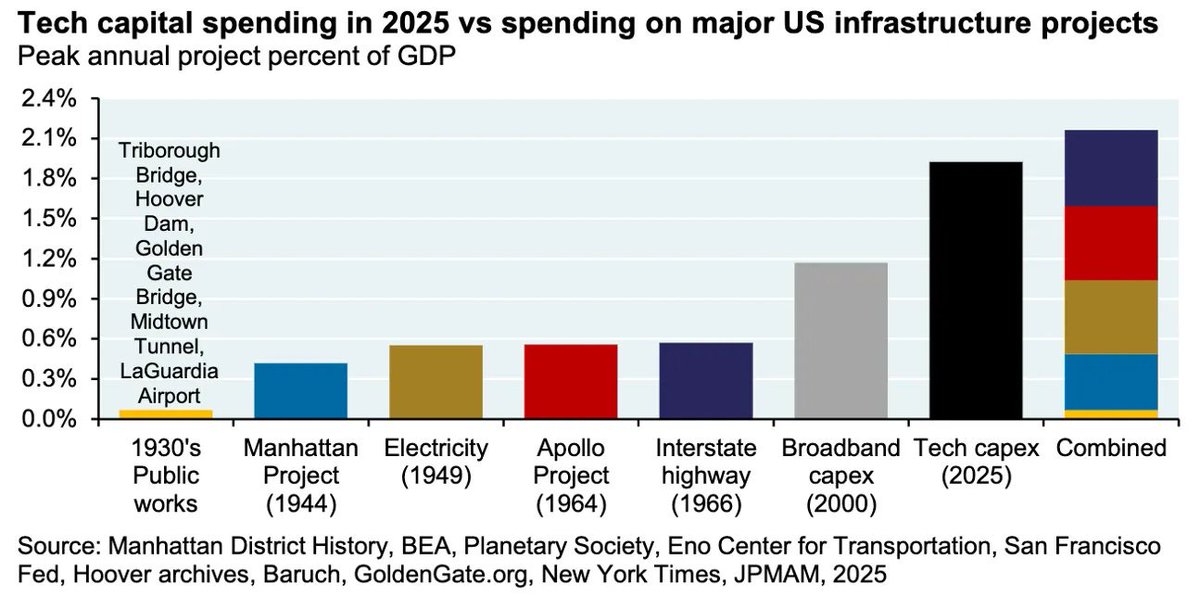

The scale is striking… 💥 Measured as a share of GDP, today’s technology capex boom already exceeds the peak annual spending of some of the most famous infrastructure and innovation projects in modern American history: the Manhattan Project, the Apollo Project, the Interstate Highway buildout, the electrification wave captured in 1949, and even the broadband capex cycle of 2000.

But that last comparison is especially important:

The broadband buildout was the physical layer behind the internet revolution. It was real. It was necessary. It helped create the digital world we now inhabit. But it also became one of the great capital-allocation mistakes of the late 1990s and early 2000s. Too much money chased the right idea too quickly, at the wrong price, with too little discipline...

The current AI buildout is already operating at a larger annual share of the economy than that cycle.

PS: My last article is already on Market View - and it's about the Three Historical Capex Trajectories That Tell Us When the Current AI Buildout Might Risk Reversing ...

1

39

The first phase of the AI trade was easy to understand. More AI required more compute. More compute required more chips, more memory, more power, and more data-center infrastructure. The market could see the earnings bridge.

So it paid for it.

The next phase is less obvious. It is not only about building the AI machine. It is about using that machine to improve real economic activity:

Commerce.

Search.

Discovery.

Pricing.

Advertising.

Logistics.

Merchant tools.

Consumer behavior.

Transaction flows.

That is where AI stops being a demo and becomes monetization.

And that is where $PDD sits.

1

31

This 👇 (and this is exactly why, earlier this year, we recommended an investment vehicle uniquely positioned to benefit from the SpaceX IPO)

May 31

FOURTH TURNING: Hard not to feel disgusted after watching this gem from @camharvey: youtu.be/rUcb4NCIXd4?si=a6YD…

The SpaceX IPO offers robust evidence of our Socialism for the Rich (SpaceX insiders and accredited VC investors) & Capitalism for the Poor (non-accredited Main Street investors) theme. Yikes.

Two things I must say about this:

1. The restricted float (4%) relative to the MASSIVE market cap (a top-10 NDX constituent on day one) makes it likely that SpaceX stock bubbles in response to passive flows—which will be MASSIVE and MASSIVELY pulled forward by NASDAQ, Russell, and S&P bending their index-inclusion rules to facilitate this IPO.

2. The Cantillon effect from this IPO alone might go down as the single most regressive transaction in human history. VC LPs benefit from a carefully manufactured post-listing bubble. Main Street retail investors get left holding the bag. Yikes. If you think it’s a good idea to own a bunch of bonds in a country where this kind of corruption is not just occurring, but being encouraged by the people in charge, you’re drunk, high, or both.

Either get in on the stock market bubble game (we are; KISS features 60% Stocks), prepare for a societal unraveling (we are; KISS features 30% Gold and 10% Bitcoin), or both. We are. KISS features 60% Stocks, 30% Gold, and 10% Bitcoin when it’s max invested and 100% Cash when it’s min invested.

Our risk-management overlays, which determine how much to allocate to each asset at each interval, will come in handy throughout the upcoming secular bear market.

If you disagree, then buy as much SpaceX as you can afford to buy 90 days after the IPO and remeasure your wealth 18-24 months later.

—Skipper 💜

1

49

🥹👇

May 29

Lost a subscriber today because I wasn’t recommending any AI stocks in the newsletter.

He’s 74.

1

48

This…

May 29

He owns the new Blockbuster.

And, just like Netflix and the Internet, stablecoins and the blockchain isn't going way. Blockchain technology completely eliminates the entire structural reason banks exist, as it eliminates the need for financial intermediaries.

Good riddance! There's no industry that deserves technological destruction more than the fucking assholes at the banks.

1

54

Who doesn’t love tulips? 🇳🇱

The “Price of the Obvious” is out, and I really like the main infographic tracking "The Last Buyer."

Whether it's seventeenth-century tulips or twenty-first-century infrastructure, fragility always arrives when acceleration peaks!

(you have to read my last post on Market View)

1

31

The best stock ideas usually make you uncomfortable. If they do not, the discount probably is not large enough. This week, I’m publishing Part Two of our Substack series based on May’s issue of VMF’s Security Selection.

Part One explained why the index can be expensive while the opportunity set remains attractive.

Part Two goes company-specific.

We disclose one of our newest recommendations: a controversial, cash-rich Chinese technology platform with a powerful domestic profit engine and a global option through Temu.

Cheap for real reasons.

But possibly cheaper than those reasons justify.

Read it here:

marketview.vmfresearch.com/p…

1

1

51

$PDD is large.

It is profitable.

It is cash-rich.

It sits directly in the application layer of the AI economy.

It is held by sophisticated growth investors.

It is held by highly respected value investors.

And yet the market values it like a business carrying a very large warning label. The obvious question is:

Why?

(you have to read my last post)

2

135

Wall Street is losing its mind over AI chips and frontier model benchmarks, but they are completely blind to the physics of the trade.

Intelligence requires electricity. A massive, unyielding amount of it.

Look at the chart.

Since 2019, China has expanded its power generation by roughly 2,500 terawatt-hours. The United States? Just 221. Europe actually contracted.

You cannot run the ultimate application-layer economy if your grid is choked and your peak load growth is hitting a structural wall! The West is underwriting immaculate software narratives while ignoring the literal plumbing under the floorboards.

If the next leg of the technology race is won by deployment rather than training budgets, who actually possesses the physical capacity to scale??

1

52