All value. No advice | Stock Newsletter valuedontlie.com | all write-ups tinyurl.com/2r3hyvfn | HoldCo circlecitycapitalgroup.com

Joined July 2014

- Tweets 10,288

- Following 899

- Followers 12,092

- Likes 11,620

2,495 Photos and videos

$CPB

Shares aren’t cheap enough yet. Durable brands, but headwinds still here no hard catalyst yet.

I see a few paths here:

1) Super boring 10%ish IRR deleveraging story (assuming earnings stabilize)

2) Dividend reduced or eliminated to speed up deleveraging which kills the stock price (I’d get interested after this event)

3) Dramatic portfolio simplification / divestiture announcement (again, I’d get interested with this announcement)

Wrote about it here (free):

valuedontlie.com/p/quick-val…

Beaten down idea:

$CPB trading at 11.5x NTM earnings and ~7% yield... EPS stabilizing at $0.50 past 2 quarters... levered 4x, but perhaps the earnings bottom is in?

Durable brands with cost private label headwinds... maybe optionality for dramatic portfolio shake-up?

8

1,456

Beaten down idea:

$CPB trading at 11.5x NTM earnings and ~7% yield... EPS stabilizing at $0.50 past 2 quarters... levered 4x, but perhaps the earnings bottom is in?

Durable brands with cost private label headwinds... maybe optionality for dramatic portfolio shake-up?

4

2

8

3,906

Jun 12

Thanks for joining to those who could make it!

Jun 11

Hosting a live call tomorrow at 1pm ET (via s_stack)

1) Walkthrough active ideas

2) Recap recently closed ideas

3) Quick look at the on-deck list

All of this will be “PTI-style” (Pardon the Interruption)… quick hits, on the fly charts financials, and discussion

1

5

1,577

Jun 12

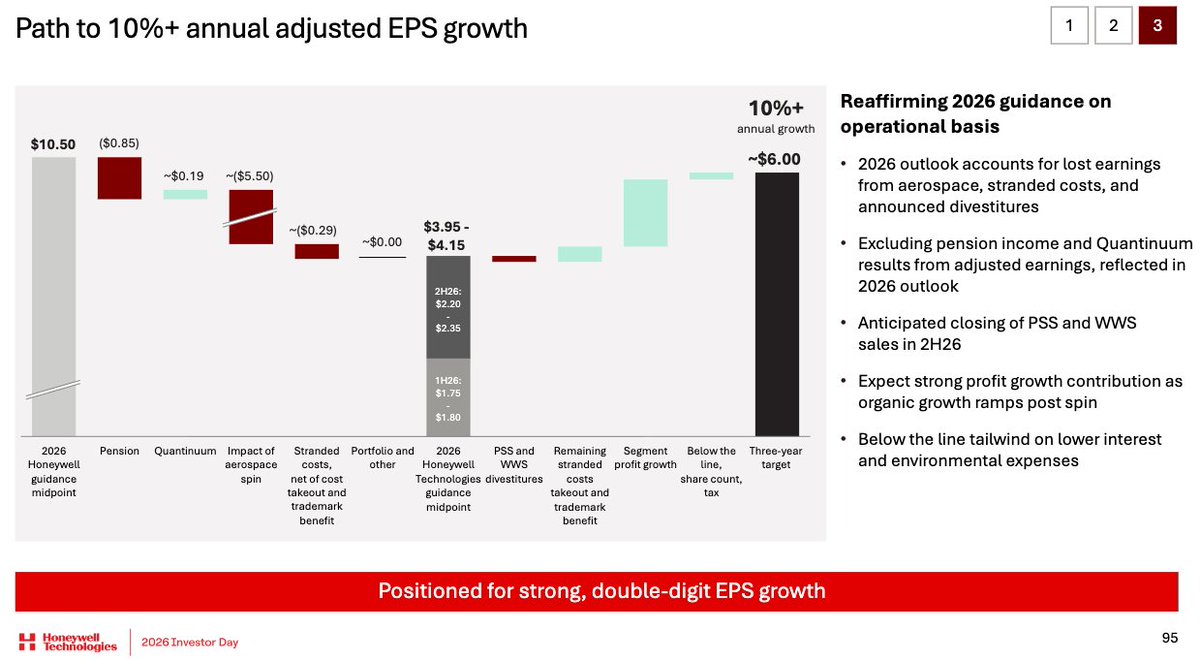

Spin-off idea:

$HON trades at $220

Spinning off aerospace biz this month w/ peers at 25-30x earnings (at $5-6 EPS = $125-180/sh)

implies $40-95/sh for remaining businesses doing $4 EPS in 2026 and growing to $6 by 2029

A-class industrial w/ low leverage

Jun 9

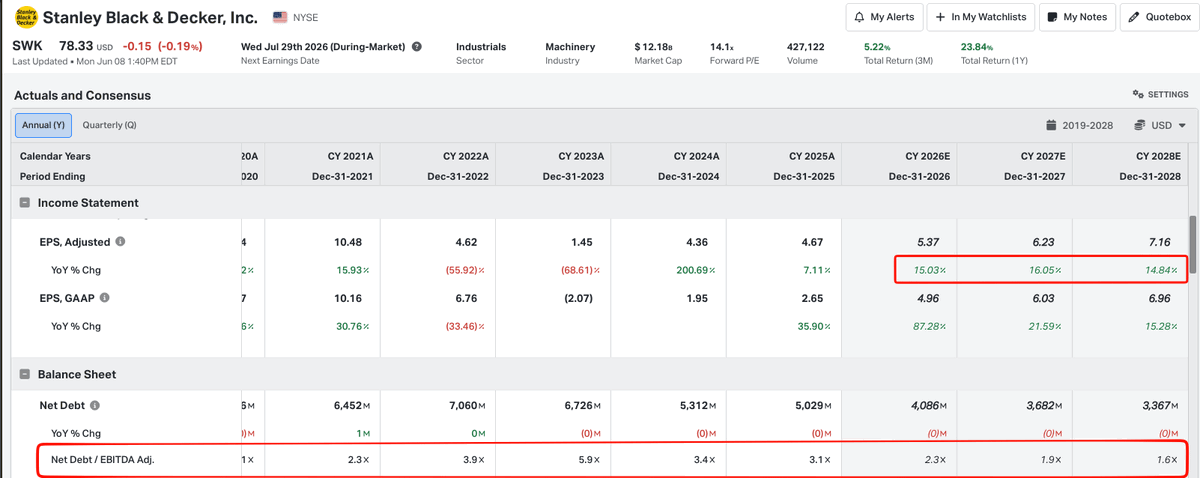

Turnaround Idea:

$SWK trades at ~11× 2028 EPS (14-15x current year) with 15% EPS growth and low leverage (recent divestiture gets them below 2.5x)

Not a bad setup for a collection of iconic tool brands and a potential housing recovery next 3-5 years?

7

4

41

13,455

Jun 11

Hosting a live call tomorrow at 1pm ET (via s_stack)

1) Walkthrough active ideas

2) Recap recently closed ideas

3) Quick look at the on-deck list

All of this will be “PTI-style” (Pardon the Interruption)… quick hits, on the fly charts financials, and discussion

1

6

2,369

Jun 11

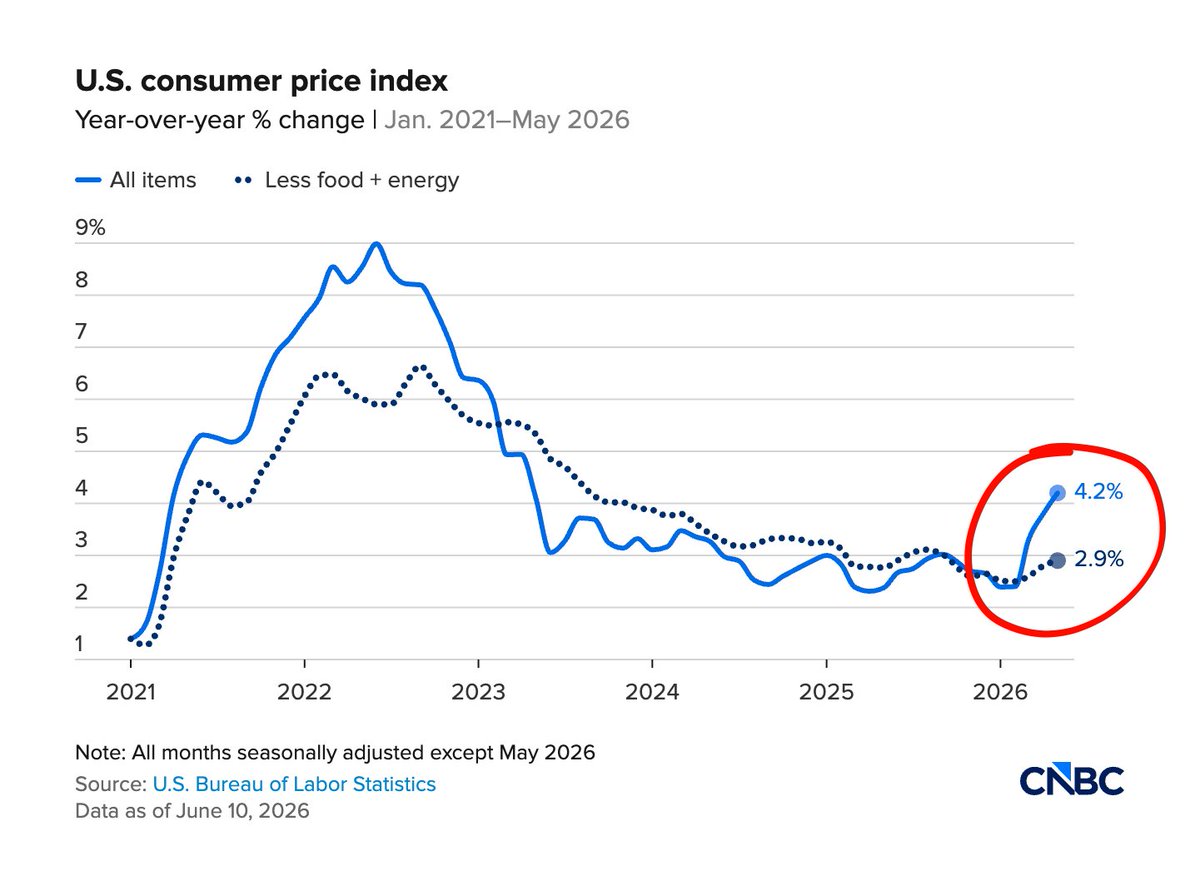

Inflation picking back up... still feels like we're battling cost creep everywhere in our businesses

2

719

Jun 9

Turnaround Idea:

$SWK trades at ~11× 2028 EPS (14-15x current year) with 15% EPS growth and low leverage (recent divestiture gets them below 2.5x)

Not a bad setup for a collection of iconic tool brands and a potential housing recovery next 3-5 years?

2

10

16,175

Jun 9

Who's attending @PlanetMicroCap conference next week?

I'll be in Vegas June 15-18 if anyone wants to meetup

3

1

8

2,956

Jun 8

I went to 2 Pacers games during last year’s NBA finals for a combined $500

It's official.

Game 3 of the NBA Finals between the New York Knicks and San Antonio Spurs is now the most expensive NBA game in history.

The cheapest ticket available? $10,622 per seat.

This game will shatter every previous record by a mile.

11

10,206

Jun 8

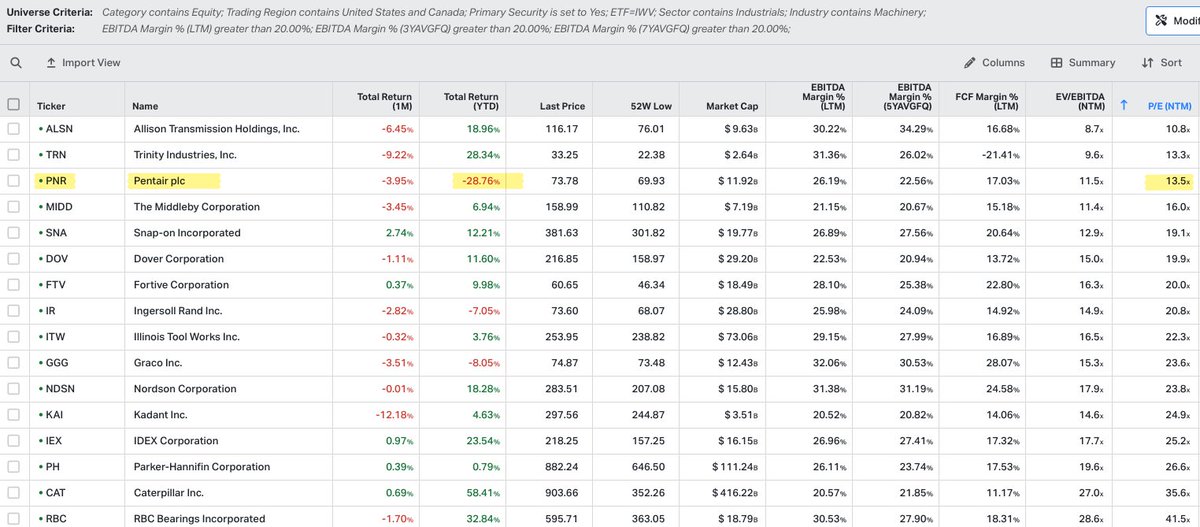

What's the story at Pentair $PNR?

Down ~30% YTD... one of cheapest industrials w/ 20% margins

5

26

14,509

Jun 8

As an owner of a bunch of different companies (personally)... I'm appreciating different "go-to-market" strategies as a legit reason to separate a business via spin-off

2

968

Jun 7

Occasionally I’ll find companies that don’t add back practical items like intangible amortization

And in super rare cases you find companies pegging to straight GAAP results

Jun 7

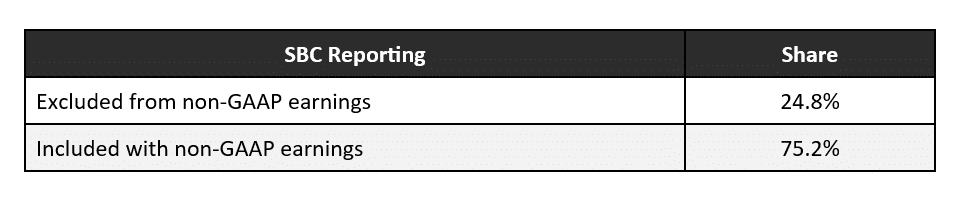

Only 25% of S&P 500 companies "add-back" stock based comp to non-GAAP earnings?

This feels way too low...

5

2,504

Jun 7

Only 25% of S&P 500 companies "add-back" stock based comp to non-GAAP earnings?

This feels way too low...

3

16

7,379

May 31

A case study from a stub investment in symmetry medical back in 2014…

Every single one of these stub situations is worth a look when they come around.

6

1,854

May 29

Have an inbound acquisition I’m looking at… trying to gauge AI risk

Very niche market research, contracted revenue, most work regulatory driven

Survey, data analysis, report/presentation are key aspects of the work product

Is this toast?

6

1

5,675