Joined October 2022

- Tweets 11,295

- Following 151

- Followers 8,840

- Likes 19,768

5,696 Photos and videos

Pinned Tweet

May 30

$SPCX $SPX

Pretty incredible treatment Elon is getting regarding the index inclusion rules (currently making the rounds here); gotta giver him credit, the world does bend on his will…

1. Buy twitter for a stupid price. Doesn’t matter as Twitter debt got rolled into SpaceX and refi'd at half the rate.

2. Twitter on the margin wins Trumps presidency, gets him special access / treatment and even Trump’s support for Tesla stock price when it was $230 in early 25. Special access ensures the IPO / index inclusion rules fall in SpaceX’s favour.

3. Twitter debt now will be paid off with a 100X's sales IPO that everyone is fast-tracked forced to buy.

Essentially, he will be the first trillionaire and to big credit of his Twitter acquisition (which was essentially free).

Anyway— kudos to him, what I really want to discuss is the following:

There is lots of chatter (flip-flopping) with respect to implications of the impending mega IPOs this year… we have gone from:

1: “SpaceX IPO will be the most obvious market topping event”…

and as equities march higher many have recently shifted to:

2. “SpaceX IPO would be way too obvious of a top, that’s too easy”…

I think you just play somewhere in the middle of those two conclusions.

I think over the next two months sentiment will shift between 1. And 2. Three times over.

It’s somewhat ironic that the IPOs (and Iran & Mid terms) were a good reason to sit back and take it easy for 2026, and now everyone is forced to stop back in, chase, and lever up in the IPO.

It’s this behaviour that will result in the oscillating behaviour between 1. And 2. IMO

We’re pretty much blowing out every record possible during this historic rally, COR1M, skew, put-call ratio, etc.

One scenario I have in mind is a repeat of July 2024 (Yen Carry Trade Unwind). We ended up seeing a -10% drawdown over 20 days, and we weren’t making new ATHs until the Fall when Trump won the election. What draws me to this is implied correlation is lowest it’s ever been on record, only July 24 has been lower.

It could look like this:

1. Profit taking days in advance of the June IPO, and initial continuation post-IPO (“holy shit maybe it’s actually the top, time to sell”).

2. We start marching back higher again into July, making new highs and the chase continues (“nvm that wasn’t the top, too obvious of course, time to rebuy!”).

3. Everyone feels like a genius for a week, then index inclusion hits (which is fast tracked into July), among likely unrelated catalyst(s) and we put in our first real drawdown (7-10%) of this rally out of March 30th (“ok that was stupid of me to chase and rebuy on an obvious market topping event”).

4. The correction wraps up, positioning (the leveraged, extreme chase /speculative type) is cleaned up and we begin marching higher.

Who really knows… I think the big takeaway is to expect our first real bout of volatility over the next two months, and risk of getting chopped up is high, but it also doesn’t mean it’s the intergalactic top either.

Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

5

6

102

57,067

Jun 14

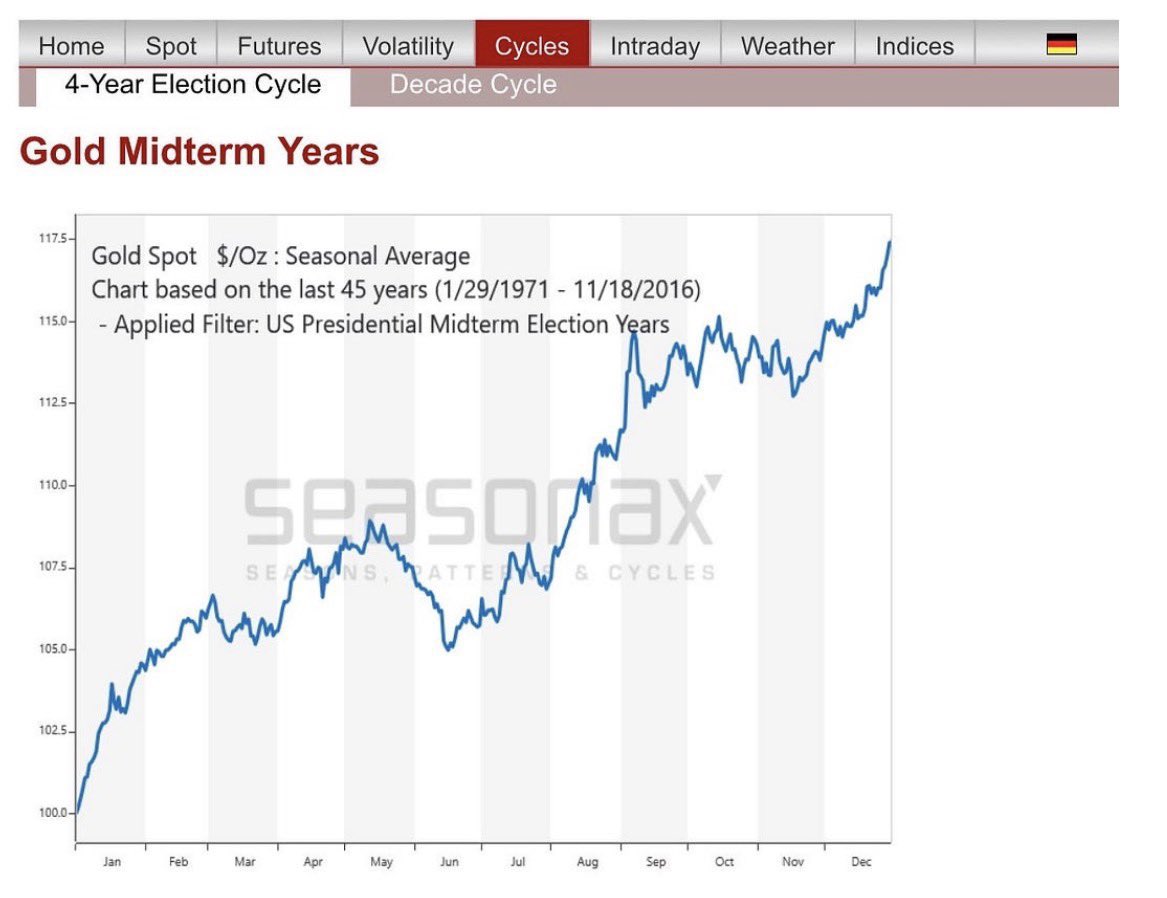

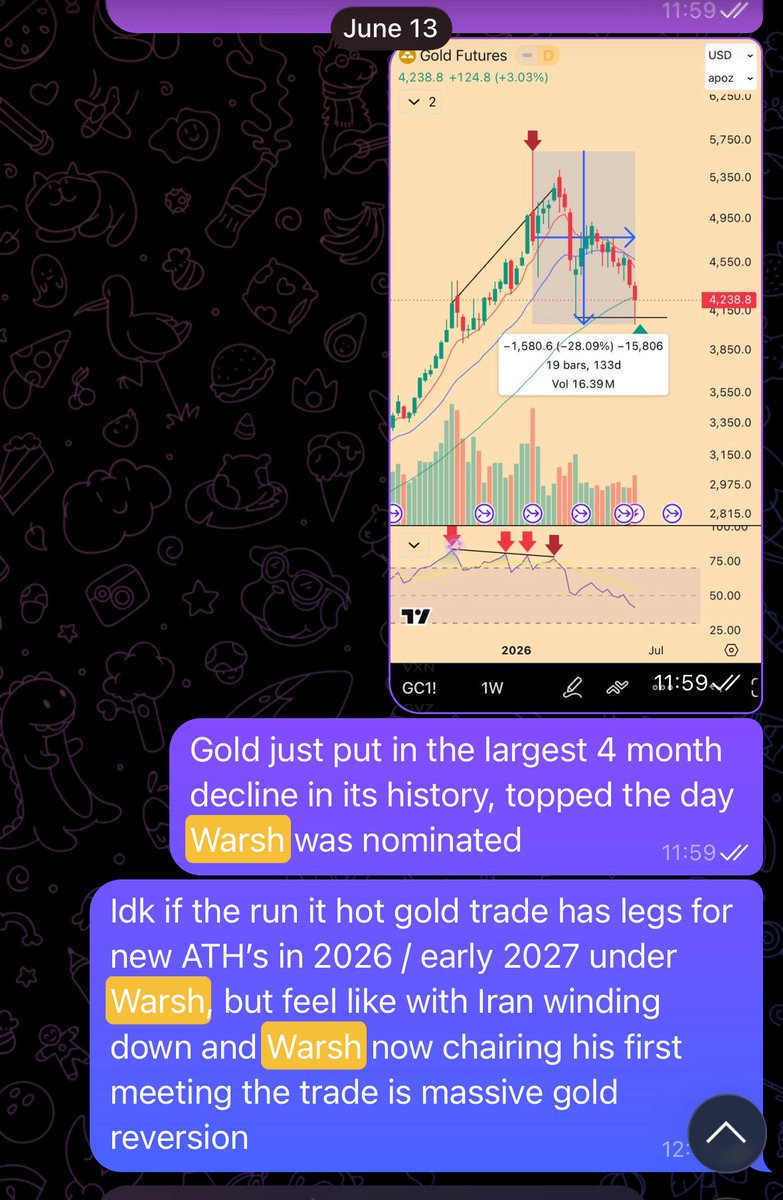

$GOLD

If Warsh (& BOJ) say the right things this week…

Your 2026 gold low is already in.

-28% over four months, from warsh’s nomination to warsh’s first meeting as Fed chair.

That simple…

5

3

68

15,983

There it is…

10

69

9,554

Jun 14

$GOLD

If Warsh (& BOJ) say the right things this week…

Your 2026 gold low is already in.

-28% over four months, from warsh’s nomination to warsh’s first meeting as Fed chair.

That simple…

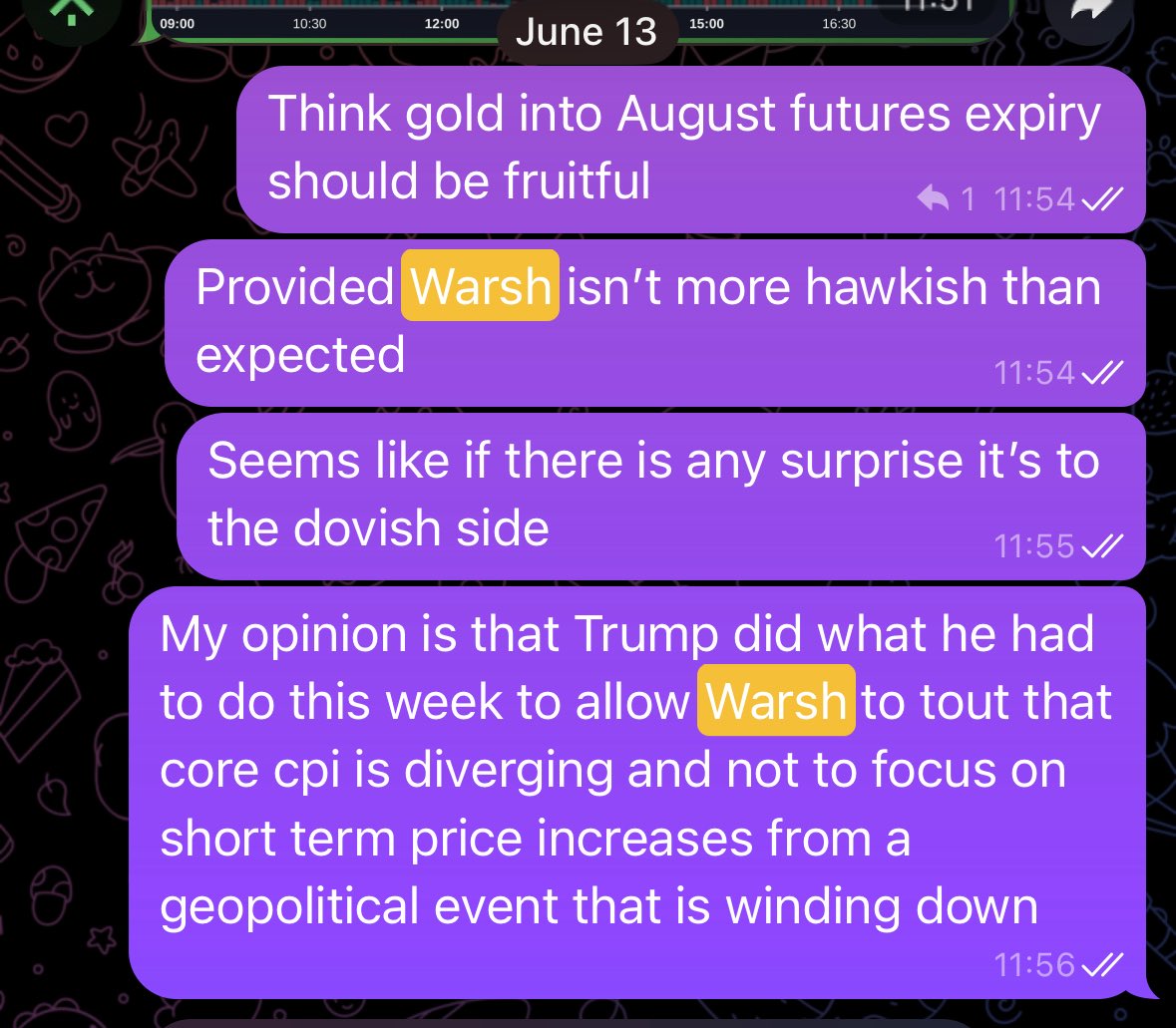

Jun 11

$GOLD

Will be paying special attention to gold from now into FOMC.

Gold topped at $5600 the moment the Trump Admin surprised the market with the Warsh nomination.

Down only ever since.

A low on his first FOMC would be poetic.

RSI most cooked since 2023 treasury tantrum…

8

1

69

23,807

Jun 14

Timely…

Hoping for continuation this week.

5

47

7,575

Jun 13

Tesla July calls are 36%

Have fun with your space stock

(Jinx)

1

19

1,865

Jun 13

Anyone operating at a higher level right now?

Jun 1

$NOW

TP’d $136.50 average

Coming into a pretty big confluence, probably just gaps up but you know me, I just play the chart.

3

1

54

7,257

Jun 13

(This is rhetorical, and yes this probably catches a bounce off the anthropic news)

1

8

1,431

Jun 13

Any questions?

Jun 11

Failed breakdowns are the most bullish setup

Tech loves failed breakdowns

6

54

17,675

Jun 13

Thanks for the tweet, Donny

1

25

3,813