There are two kinds of people. Those who are humble and those who are about to be.

Joined June 2021

- Tweets 3,909

- Following 174

- Followers 7,088

- Likes 2,721

1,104 Photos and videos

Pinned Tweet

27 Mar 2024

Simple thesis: Buy well run, well financed, efficient capital allocators, market leaders that are available cheap at the trough of the market cycles.

How often do you find this combination? Frequent buying/selling makes very little sense.

17 Dec 2022

Some of Kenneth Andrade's top picks and the rationale behind each-

1) Page Ind (2007-08): when it launched IPO, 3 yr cash flow was sufficient to fund capex. Was available at 15 P/E

2) Bata India (2009): Deleveraged, positive cash flow, was available cheap

1/n

3

6

48

26,772

PB Fintech: After QIP proposal was shelved following market reaction, founders ended up selling shares worth 665 Cr ;)

This is not the first instance. PB Healthcare was incorporated in Jan 2025 as 100% subsidiary, company invested 540 Cr into it. Shortly, external investors and ESOP pool were brought in and PB Fintech ownership fell from 100% to 40%. Shareholders funded the incubation and ended up with less than half of the business.

PB Fintech was planning a QIP to fund M&A while having 5000 Cr cash in the books (never disclosed the amount so it raises obvious questions when the company has ample liquidity). Market punished the stock and they immediately cancelled the QIP.

Strong business but management compensation is tied to stock performance via massive ESOPs. Near term stock price management seems to be the priority.

2

6

43

8,740

How does a government EPC business end up with FMCG like profitability? Can someone explain tender level economics?

2

15

1,597

Jeena Sikho⚠️

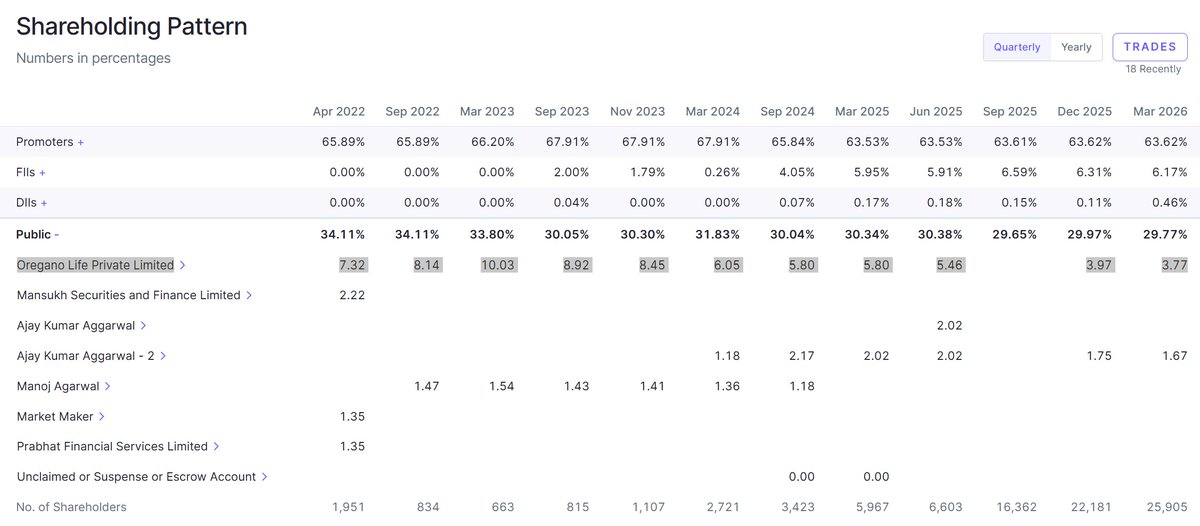

1) 70 Cr acquisition in slump sale to acquire ayurvedic business of Oregano Life Pvt Ltd, amount exceeding entire year's operating cash flow. Net tangible assets acquired are worth 8 Cr and 88% of purchase price is booked as goodwill.

Oregano Life Pvt Ltd is the largest public shareholder of the company. Nothing disclosed in related party notes, so an arm's length transaction with zero disclosures on any independent valuation to justify the price tag. On top of that, this entity is systematically liquidating its equity stake in Jeena Sikho.

There is more..

12

28

178

94,520

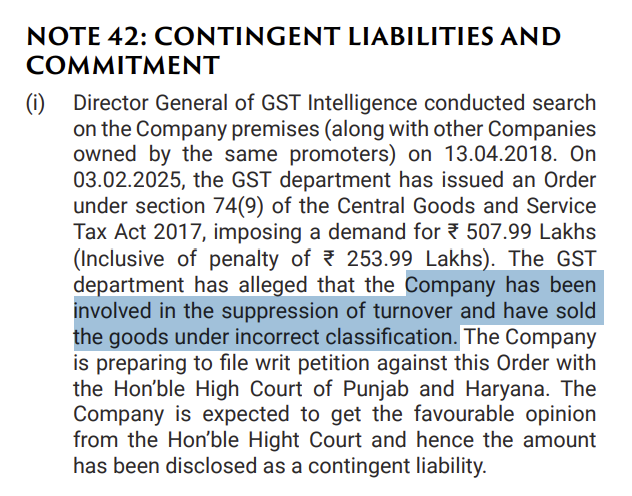

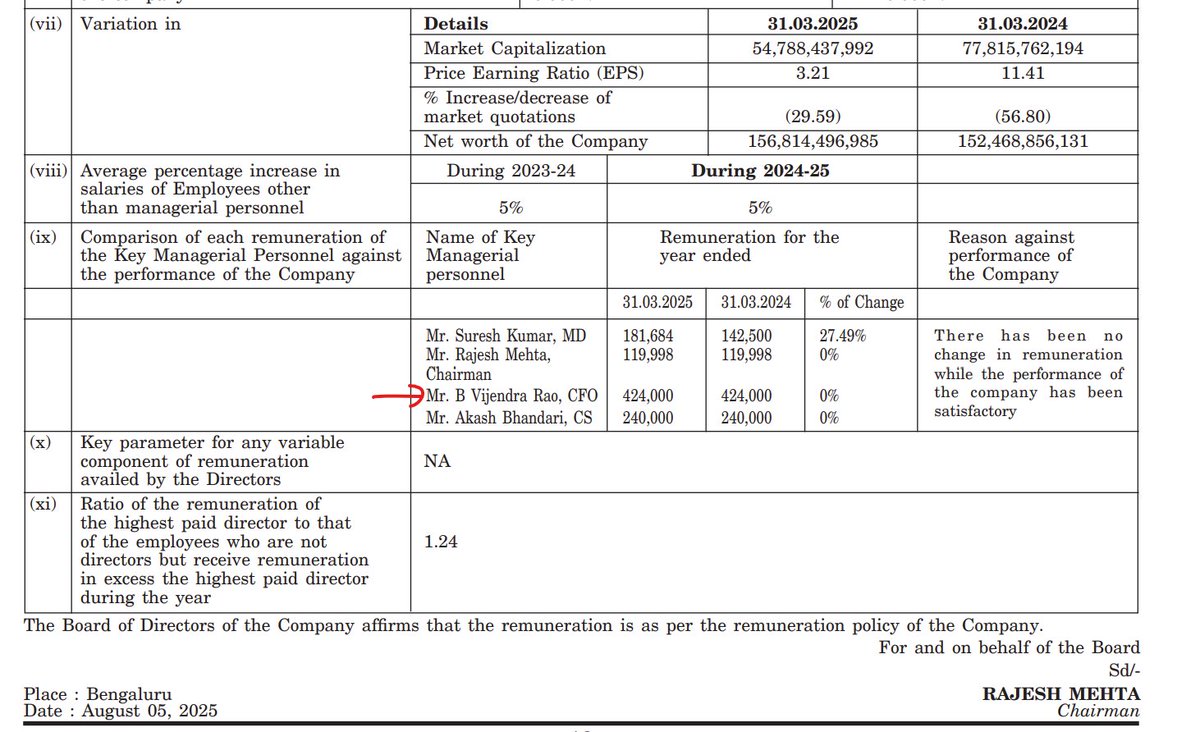

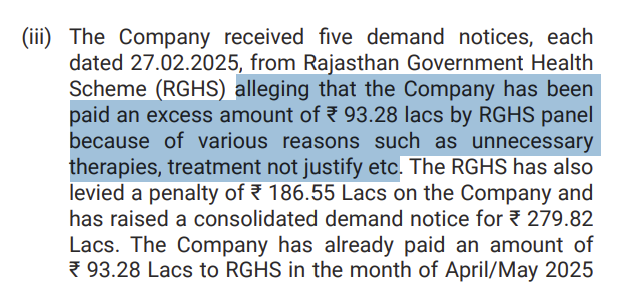

4) GST intelligence raid and 5 Cr demand order

&

RGHS demand notice (total demand 2.8 Cr, 93 lakh already paid) :

1

1

20

5,555

Lack of DII ownership is also worth noting. Can't just be a free float thing. Much smaller, less liquid companies have substantial DII ownership.

3

27

4,807

Unknown Market Wizards retweeted

Jeena Sikho⚠️

1) 70 Cr acquisition in slump sale to acquire ayurvedic business of Oregano Life Pvt Ltd, amount exceeding entire year's operating cash flow. Net tangible assets acquired are worth 8 Cr and 88% of purchase price is booked as goodwill.

Oregano Life Pvt Ltd is the largest public shareholder of the company. Nothing disclosed in related party notes, so an arm's length transaction with zero disclosures on any independent valuation to justify the price tag. On top of that, this entity is systematically liquidating its equity stake in Jeena Sikho.

There is more..

12

28

178

94,520

Unknown Market Wizards retweeted

Jun 13

I wonder how Anthropic researchers and engineers who aren’t US citizens but were on the Fable team would be feeling right now.

They can’t access the very thing they helped create.

225

411

7,414

332,228

Interest payment alone is eating up ~19% of US tax revenue but nobody wants to raise taxes, cut expenses or tolerate higher rates. Easiest way out is to print money, buy bonds and bring yields down. When dollar is weakened by money printing, gold tends to rise.

@akshat96jain, something feels familiar from our conversation the other day ;)

4

12

1,202

If a business grows EPS 3x over 10 years (from 10 to 30, only 11% cagr which most would dismiss right away) and P/E multiple also expands 3x over the same period (from 10 to 30), your stock price return is 9x not 6x.

Compounding is multiplicative, not additive.

3

27

1,787

Tata Steel: Metals have massively outperformed broader market lately. China production cuts should create a floor for Indian flat prices but higher coking coal cost and new capacity additions could also cap spreads.

Through cycle EBITDA/tonne ~ 12500 Rs.

On ~25 MTPA utilized capacity (including Kalinganagar 5 MTPA ramp, assuming Europe ~0), normalized EBITDA ~ 31250 Cr.

Less:

Maintenance capex ~ 10000 Cr (3-4% of gross block)

Interest ~ 7500 Cr

Tax ~ 25-30%

Owner's earnings ~ 9500 Cr

At 250000 Cr Mcap, that's 3.5-4% yield, not compelling for a levered cyclical. Same theme across sectors, great industry setup but very little margin of safety.

2

14

1,362

Stay away from hot tips, leverage and unsolicited advice from "ace investors".

3

6

1,100

HV T&D: Todays earnings embed supernormal pricing from a temporary demand supply mismatch. Forward P/E can be extremely deceptive when normalized earnings are materially lower than peak cycle earnings.

1

2

14

1,772

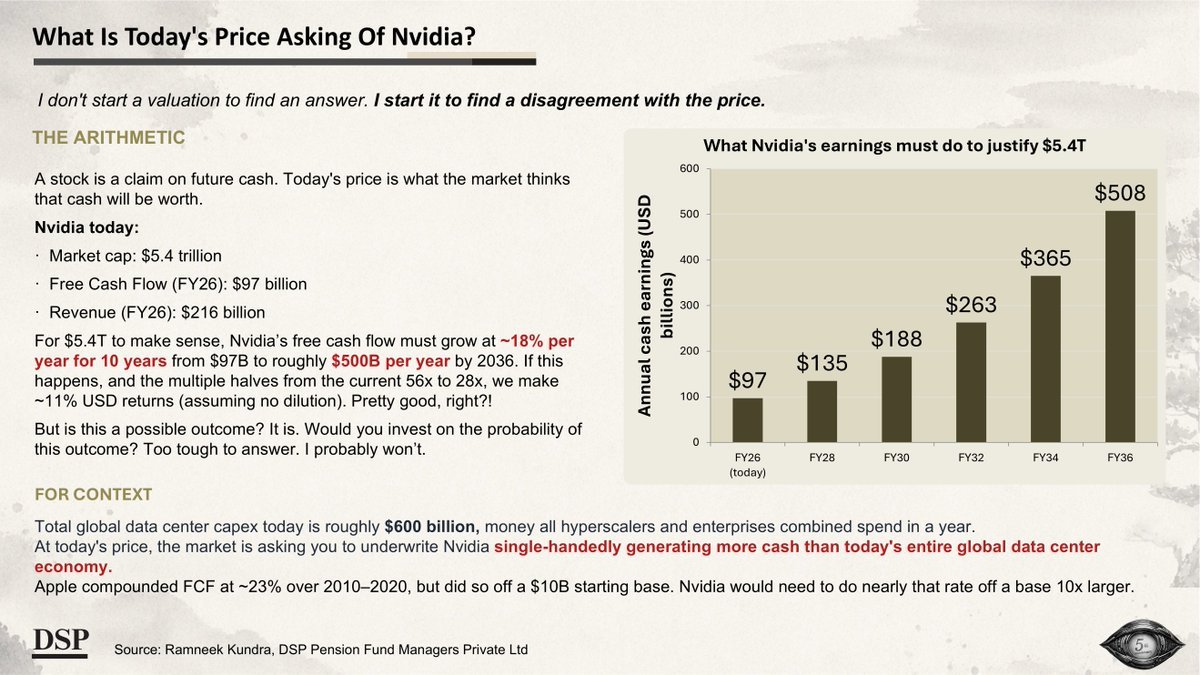

Growth rates required to justify these prices are historically unprecedented. No company has ever grown that fast at that scale. Doesn't mean it's impossible. Its just that you're betting on something that has never happened before.

2

13

998

Unknown Market Wizards retweeted

Math of portfolio construction -

Which one is a better bet?

Bet A- Flip a coin, heads you win 15 Rs, tails you lose 5 Rs

Bet B- Roll a dice, if it shows 6 you win 15 Rs, if not you lose 3 Rs

Expected value-

Bet A: 50%*15 - 50%*5 = 5 Rs

Bet B: 17%*15 - 83%*3 = 0 Rs

What mattered here was the base rates. In Bet A one wins 50% of the times, in Bet B one wins 1/6th of the times.

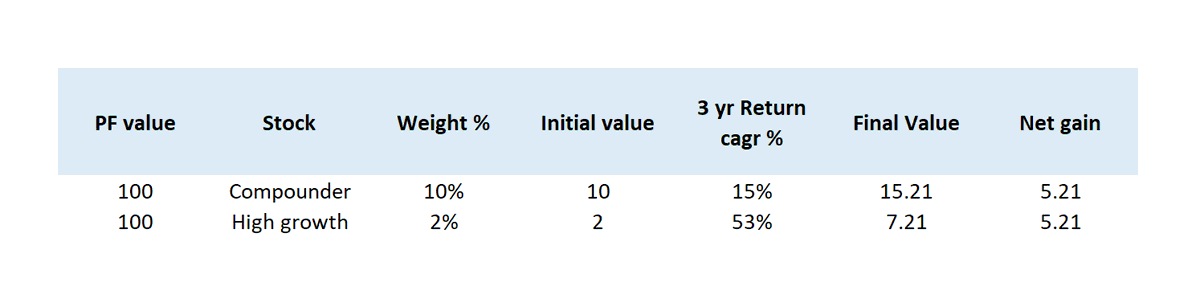

Now take this to actual businesses: Higher the return, higher the risk and higher risk means violent downside when you're wrong. So its hard to size a very high upside, high downside bet at 10% of your PF in my view. 40% downside would cost 4% of PF. So generally these high growth bets sit at lower sizing (say ~2%). To achieve same net gain as a 15% compounder, this bet needs to deliver 53% return cagr (and good luck if you're betting on many such 2% bets going right at the same time).

Base rates? Roughly half the stocks (with Mcap > 1000 Cr) have delivered 15% cagr over 3 year period. Only about 12.5% of the same universe have delivered over 53% cagr over 3 years.

3

15

2,104

Watch out for lenders with high microfinance exposure.

MOSL write up:

Economy Note - FY27 Consumption Risk and opportunities

El Nino (92-96% probability during core monsoon) West Asia energy shock = a convergence not priced by markets.

MOFSL sees FY27 CPI at 5.7% vs RBI's 4.6% — a 110-120bp gap.

Rural India bears the brunt (food is 42% of rural CPI vs 30% urban). The earnings hit lands in corporate results Q1/Q2FY27 well before it shows in GDP prints.

Urban premium consumption is the hide; while

Tractors, Entry 2W, Rural FMCG, and MFIs are the pain trade.

Key Monitorable ahead is Reservoir level to assess how Rabi crops will be.

1

10

4,976