Macro research for investors who know politics moves markets. Covering Asia, energy, gold, currencies, global capital flows, and geopolitical risk.

Joined March 2024

- Tweets 8

- Following 18

- Followers 73

- Likes 3

7 Photos and videos

China Internet Stocks Just Completed a 13-Year Round Trip

In August 2013, the KraneShares CSI China Internet ETF — KWEB — traded around $26.

Today, more than a decade later, it is still around $26.

During the same period, the U.S. produced an AI boom, a cloud boom, a mega-cap tech boom, and one of the greatest wealth-creation cycles in modern market history.

China produced Alibaba, Tencent, Meituan, JD, Pinduoduo, ByteDance, electric vehicles, mobile payments, and one of the most sophisticated digital consumer ecosystems on earth.

And yet the broad China internet trade went nowhere.

This is the central lesson investors keep ignoring:

A great company is not always a great stock.

A great industry is not always a great investment.

And a great growth story can be completely destroyed by governance risk.

KWEB did not fail because China lacked talent, scale, technology, or consumer demand.

It failed because the market learned that in Xi Jinping’s China, equity holders are not the senior claimants. The Party is.

The last five years made this brutally clear.

The platform crackdown crushed valuation multiples.

The tutoring ban vaporized an entire listed industry almost overnight.

Evergrande exposed the property model.

Youth unemployment surged.

The population began shrinking.

Foreign capital started asking a question it should have asked earlier:

What exactly do I own when I buy a Chinese equity?

In Western markets, investors debate earnings, margins, interest rates, and competition.

In China, investors must also price in one more variable:

political permission.

That variable has no terminal value model, no clean discount rate, and no reliable hedge.

This is why the KWEB chart is so important. It is not just a stock chart. It is a 13-year case study in how political risk can eat innovation, growth, and index inclusion alive.

The old China trade was simple: buy growth, ignore politics.

The new China trade is different:

Respect the innovation.

Fear the governance.

And never confuse national ambition with shareholder return.

3

6

20

3,362

China’s flexible employment workforce rose from 120 million in 2015 to 280 million in 2025, which means it more than doubled in a decade.

That is a huge structural shift: what is often presented as “labor flexibility” can also be read as a sign that stable, traditional jobs are giving way to gig work, part-time work, and more precarious forms of employment.

320 Million “Flexible Workers”: China’s Job Market Is Breaking in Plain Sight

China calls it “flexible employment.” But behind the nice-sounding phrase is one of the biggest labor-market crises in the world.

In 2025, China had around 280 million flexible workers. By 2026, that number could reach 320 million, nearly half the workforce. Beijing presents this as dynamism. But for many people, it means unstable income, no long-term contract, no career ladder, and little real social security.

In this video, I explain why China’s flexible employment boom is a warning that stable jobs are disappearing, the middle class is being pushed downward, and millions of workers are being relabeled rather than rescued.

4

8

26

3,630

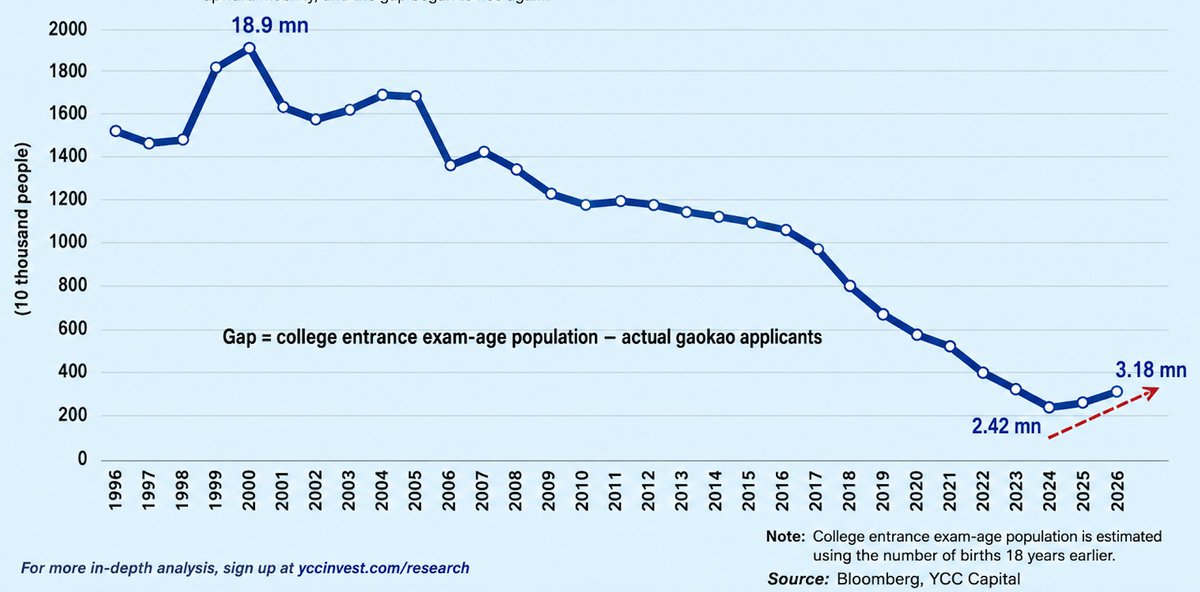

China’s gaokao chart may be one of the clearest pictures of China’s rise - and decline in confidence.

The gap between China’s college-entrance-exam-age population and actual applicants collapsed from 18.9 million in 2000 to just 2.42 million in 2024. In the boom years, families believed education was the ladder to upward mobility, so more students stayed in the game. That was the optimism of the WTO era.

But now the trend is turning. The gap is projected to rise again to 3.18 million in 2026.

That matters. It suggests more young people are questioning whether the gaokao, and the credential treadmill behind it, still leads anywhere. When faith in education weakens, it usually means faith in the economy is weakening too.

This is not just an education story. It’s a confidence story.

5

12

52

7,301

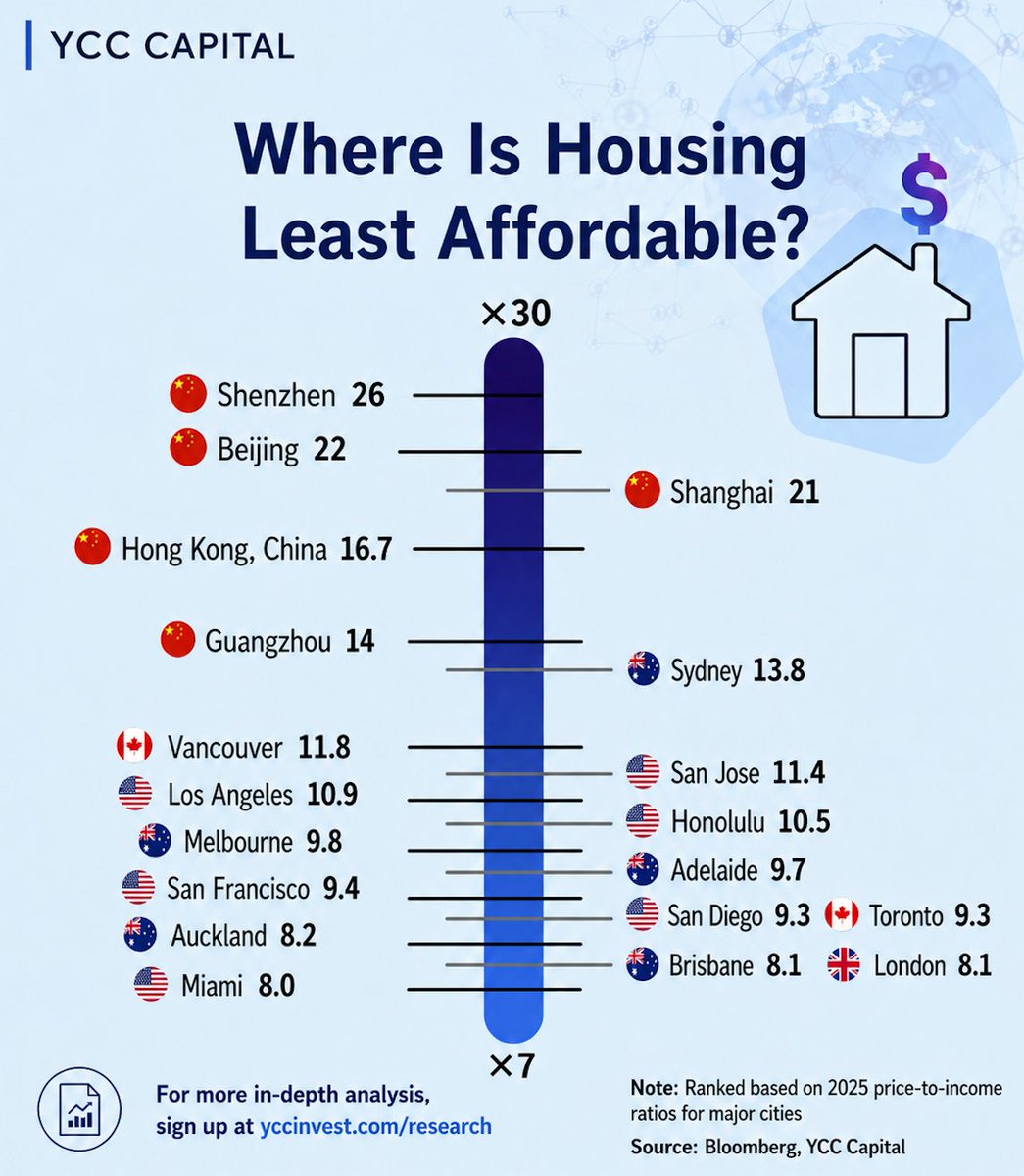

Housing affordability in China’s top cities is completely broken.

Shenzhen now tops the list at 26x income.

Beijing: 22x. Shanghai: 21x. Hong Kong: 16.7x.

That means even compared with famously expensive cities like Sydney (13.8x), San Jose (11.4x), Vancouver (11.8x), and London (8.1x), China’s biggest urban centers look far more stretched.

This is what happens when housing stops being shelter and becomes the core speculative asset of an entire economic model.

The real story is what this says about distorted capital allocation, crushed household balance sheets, and why the property downturn is such a structural threat to China’s economy.

3

9

34

36,971

For more in-depth analysis: yccinvest.com/research

2

447

High Oil Prices Have Elevated Inflation Across Multiple Economies.

The US-Iran conflict, which erupted earlier this year and entered a protracted stalemate by early June, has now persisted for approximately three months without a durable de-escalation agreement. Throughout this period, maritime transit volumes through the Strait of Hormuz—the critical chokepoint for roughly 20% of global oil trade—have remained severely depressed. Average daily transits have fallen into the single digits, representing roughly 5% of pre-conflict throughput. There are no clear signs of normalization.

Constrained supply has kept international crude prices elevated and structurally higher than the pre-conflict equilibrium of approximately 66 USD per barrel. The post-conflict midpoint has shifted to around 101 USD—a 53% increase. This sustained deviation is transmitting directly into global inflation via higher energy input costs, creating a classic imported inflation shock.

In the three months since the conflict intensified, energy CPI has materially outpaced both core and headline measures in most major economies (April 2026 data). The United States recorded energy inflation of 17.9% against headline CPI of 3.8%. Canada saw similar extremes in the 17–20% range. The Eurozone and broader Europe registered energy inflation between 10% and 15%, well above their respective core and headline prints. The United Kingdom followed a comparable pattern.

Japan stands apart: its energy CPI remains in negative territory, though the pace of deflation has narrowed meaningfully versus the pre-conflict baseline. This divergence largely reflects Japan’s aggressive fiscal response—most notably the 3.11 trillion JPY supplemental budget that established a dedicated Middle East emergency energy reserve to cushion domestic price pass-through. Without such buffers, the inflationary impulse would likely have been more uniform globally.

The key takeaway is that a geopolitically induced oil price regime shift—rather than a transitory spike—has already embedded a durable inflationary pulse into multiple large economies. This is not merely a headline effect; it is feeding into core inflation expectations and, critically, into central bank reaction functions. Markets are now pricing higher-for-longer policy rates in several jurisdictions, with the Euro area appearing particularly sensitive.

1

3

3,247

The Hidden Force Crushing the Japanese Yen Is About to Reverse.

Japan’s yen problem has a hidden driver: household capital flows.

Since the expansion of NISA, Japanese households have been sending roughly ¥10 trillion a year into overseas investment funds, adding pressure to the yen and reshaping Japan’s capital account. Now, policymakers are turning their attention back to retail Japanese government bonds as a way to strengthen domestic savings channels, stabilize the JGB market, and give households a safer yen-denominated alternative.

In this video, I explain why Japan’s “boring” government bonds suddenly matter again, how household money is influencing the yen, and why this shift could become an important signal for investors watching Japan’s next macro cycle.

1

1

12

3,244