Financial Literacy| Passionate about Psx Investing, Executive Producer The inside Scoop show Channel 365 | 🇨🇦🇵🇰

Joined February 2020

- Tweets 1,728

- Following 686

- Followers 807

- Likes 10,312

155 Photos and videos

Pinned Tweet

Jan 6

Current update: 185,000 points

Target of 180,000 pts hit.

✅ Next stop 200,000 pts

1

7

633

Jun 15

SBP holds rate at 11.5%.

Last meeting was a 1% hike.

Today market was 50/50 on hike vs hold. Hold won.

Inflation cooling. Oil off its highs. Tightening cycle looks done.

Bullish signal for KSE-100.

🚀Position accordingly.

55

May 19

Service long march Tire biggest IPO of 🇵🇰 oversubscribed within 5 seconds

✅ Huge participation from investors in Pakistan stock market shows investor confidence

• if you applied 100,000 shares at Rs19.95 due to over subscription you get only 8000 shares

1

143

Finance Minister Muhammad Aurangzeb left Habib Bank Limited in March 2024. Within twenty-six months, the ministry he now runs had completed three major sovereign financing transactions. The same two banks appeared in all three. Neither HBL nor Standard Chartered has disclosed what they were paid. Neither the ministry nor Aurangzeb has explained how they were selected. What Aurangzeb did instead, at a ceremony in Beijing on May 15, 2026, was thank HBL by name.

Transaction One: The $1 Billion Syndicated Loan, June 2025

Fifteen months after Aurangzeb took office, his ministry signed a $1 billion syndicated term finance facility backed by an ADB policy-based guarantee. The guarantee was the instrument that brought commercial lenders to the table. Pakistan's credit profile could not have attracted the lending on its own terms. With the ADB covering the credit risk, the question of which banks were appointed to arrange the loan becomes worth asking.

Standard Chartered was named mandated lead arranger and bookrunner. HBL was named as an arranger alongside Sharjah Islamic Bank and Ajman Bank. The arranger fee pool on a facility of this size, at standard market rates of between one and two percent, runs between $10 million and $20 million. HBL's share has not been disclosed. The ministry did not explain how HBL was selected, fourteen months after its former CEO became the minister approving the transaction.

Transaction Two: The $750 Million Eurobond, April 2026

Twenty-five months into Aurangzeb's tenure, his ministry returned to international capital markets for the first time in four years with a Eurobond priced at 6.975 percent. Standard Chartered was sole bookrunner. There was no competitive bidding. The bond was placed privately with institutional investors. After a greenshoe clause was exercised, the total issuance reached $750 million, with Standard Chartered remaining sole bookrunner throughout. The underwriting fee on a transaction of this size, at standard market rates, runs between $7.5 million and $15 million, paid entirely to one bank, selected without disclosed competition, by a ministry that had already awarded that same bank a lead arranger role ten months earlier.

The day after the Eurobond closed, the ministry issued a formal request for proposals inviting competitive bids from international consortia to manage future sovereign capital market transactions over the next three years. Competitive selection arrived the morning after the fees were paid.

Transaction Three: The $258 Million Panda Bond, May 2026

One month later, HBL reappeared. Pakistan's inaugural Panda bond required ADB and AIIB credit-enhancement guarantees totalling $285 million to achieve a domestic AAA rating in China's investment-grade-only bond market, because Pakistan's sub-investment-grade credit standing barred entry without external cover. The guarantees backed 95 percent of principal and accrued interest, paid directly to bondholders. The oversubscription that followed reflected appetite for multilateral paper. It reflected nothing about Pakistan's standalone creditworthiness in Beijing.

HBL was named financial adviser to the Government of Pakistan on the transaction. China International Capital Corporation was lead underwriter. Bank of China, Standard Chartered, and Hongta Securities were joint lead underwriters. The advisory and underwriting fee pool on a bond of $258 million, at standard market rates of two to four percent of proceeds, runs between $5 million and $10 million, shared across the fee-earning institutions. HBL's specific advisory fee has not been disclosed.

The Express Tribune had reported in February 2026, months before the bond closed, that the finance ministry's own external wing formally objected to being bypassed in the Panda bond negotiations and in the hiring of consultants and foreign firms, with specific concerns raised over the process used to appoint transaction underwriters. The ministry did not respond to the Tribune's requests for comment. The bond closed anyway. HBL collected its fee.

At the Beijing ceremony, Aurangzeb thanked HBL by name. He did not mention that HBL was his former employer. He did not mention that he had run it for six years. He did not mention that its appointment had not been subject to disclosed competitive selection, or that the ministry's own officials had objected to the process.

Question

Across three transactions in fourteen months, the ministry awarded sovereign mandates worth a combined $2 billion in face value to two banks, Standard Chartered and HBL, through processes that were either explicitly non-competitive, internally contested, or unexplained. The total undisclosed fee exposure across all three transactions, estimated at standard market rates, sits between $22 million and $45 million. The precise figure is unknown because neither the ministry nor the banks involved has published it.

This is not a criminal allegation but simply a governance question with a documented answer gap. When a finance minister's former employer collects undisclosed fees on sovereign transactions his ministry structures, and when the same bank appears in all three major deals completed under his watch, and when competitive selection is introduced only after those deals close, the public is owed an explanation.

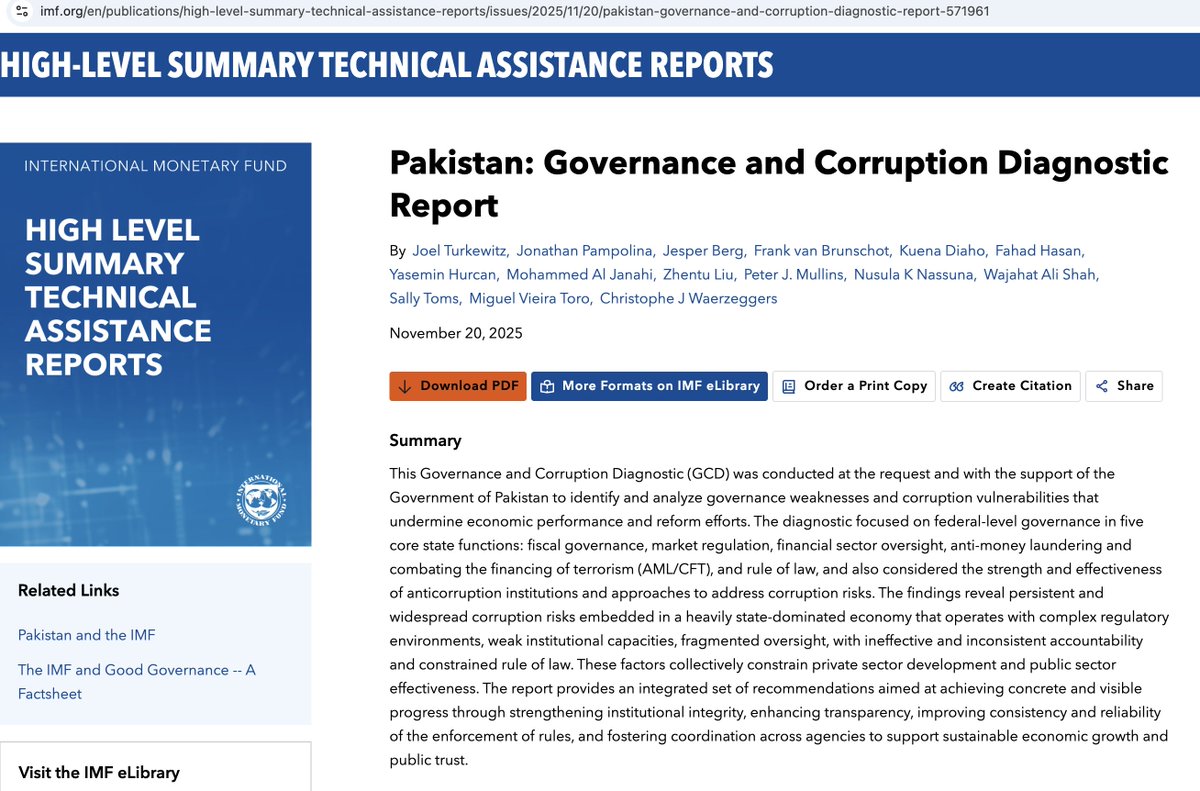

The IMF's Governance and Corruption Diagnostic, published in November 2025 as a condition for loan disbursement, identified influential elite networks steering key economic sectors to their advantage and found persistent weaknesses in public procurement. Aurangzeb called it a catalyst for reform.

Pakistan's Panda Bond Victory

Let's dig in.

Finance Minister Aurangzeb returned from Beijing this week calling Pakistan's inaugural Panda Bond a "new chapter" in economic ties with China. The markets agreed. The $250 million, yuan-denominated instrument was five times oversubscribed. What he did not mention is that the guarantees underwriting the bond totalled $285 million, which is $35 million more than the bond itself. Investors were not betting on Pakistan. They were, quite literally, covered beyond the principal.

Pakistan could not access China's investment-grade-only bond market on its own. Its sub-investment-grade credit rating barred entry. ADB and AIIB together covered 95 percent of the principal and any accrued interest, paid directly to bondholders, at a combined guarantee fee of between 0.8 and 1.25 percent charged back to Islamabad. The oversubscription reflects appetite for AAA-rated multilateral paper. It reflects nothing about Pakistan's standalone creditworthiness in Beijing.

China already holds roughly 22 percent of Pakistan's total external debt. Adding yuan-denominated bonds to a balance sheet already heavily weighted toward Chinese bilateral and commercial exposure is not diversification. It deepens the same concentration while appending a new currency risk: the rupee has lost substantial ground against the renminbi over the past decade, and yuan-denominated obligations grow costlier in real terms every time it does. The bond was also placed privately on the interbank market, offered only to qualified institutional investors. There was no public price discovery. Nobody knows what Pakistan's unsupported borrowing rate in Chinese capital markets actually is, because it has never been tested.

On scale: $250 million against an external debt load exceeding $96 billion is arithmetic noise. The full $1 billion program, once complete, covers just over one percent of total obligations. Planning Minister Ahsan Iqbal, while approving the guarantee structure, warned that new foreign loans should not be signed without rupee cover in the PSDP, cautioning that delays could produce another circular debt crisis. His cabinet signed this one the same week.

The "reform-minded technocrat" framing that follows Aurangzeb deserves scrutiny on its own terms. For six years he ran the largest bank in Pakistan and delivered lower returns on equity, higher cost-to-income ratios, and dividends that lagged both the pre-Aurangzeb period and every comparable peer institution. HBL's sharpest performance recovery came after he left for Q-block. A man whose primary credential is banking, and whose banking record is one of value erosion, now manages the sovereign balance sheet. The Panda Bond he is celebrating, a $250 million instrument requiring $285 million in external guarantees to get in the room, is consistent with that record.

The guarantee fees go to multilateral banks, the interest goes to Beijing, the debt stays in Islamabad, and the minister who arranged it spent six years doing the same thing at a smaller scale, this is not a new chapter, it is the same elite driven extraction model Pakistan has been employing since 1958.

7

123

240

48,883

May 16

🚨PSX ACCOUNT OPENING MADE EASY

• Open your Pakistan stock market account today within 24hours.

• Get Premium customer Care services mon-Fri

✅CLICK THE LINK IN BIO to open your ACCOUNT

1

122

Sherdil Ismail retweeted

May 13

The Supreme Court upheld the Sindh High Court decision that the board of TRG has committed a $150 million fraud against TRG’s 13,000 public shareholders. A business that once managed over $2 billion in assets now has only $100 million, with the rest destroyed by the present management, while they have paid themselves and their lawyers tens of millions of dollars. We look forward to removing them in the upcoming board elections now endorsed by the Supreme Court, and rebuilding the business, hopefully to even greater success than before.

89

244

1,204

155,855

Sherdil Ismail retweeted

Apr 29

🚨 Those Who Have Palaces In Dubai And London Cannot Solve The Problems Of The People. Today Corruption Is At Its Peak In 🇵🇰 Pakistan. Public Money Looting Has Never Been Worse.

- Shahid Khaqan Abbasi.

19

351

1,028

22,979

Sherdil Ismail retweeted

وزیر اعظم شہباز شریف آج اپنا گھر پروگرام کے تحت پیکج کا اعلان کریں گے ایک کروڑ روپے 20 سال کی مدت کیلئے فراہم کیے جا سکیں گے، 25 لاکھ 50 لاکھ اور 75 لاکھ یا 1 کروڑ قرض حاصل کیا جا سکے گا، پہلے دس سال میں ٪5 فکس مارک اپ ہوگا اگلے دس برس نارمل مارک اپ ہوگا۔25 لاکھ کی ساڑھے 16 ہزار ماہانہ قسط ہوگی، جب کہ 50 لاکھ کی 33 ہزار ماہانہ قسط ہوگی۔75 لاکھ پر 49 ہزار اور 1 کروڑ کی ماہانہ قسط 66 ہزار ہوگی۔

25

159

453

165,759

Sherdil Ismail retweeted

Apr 28

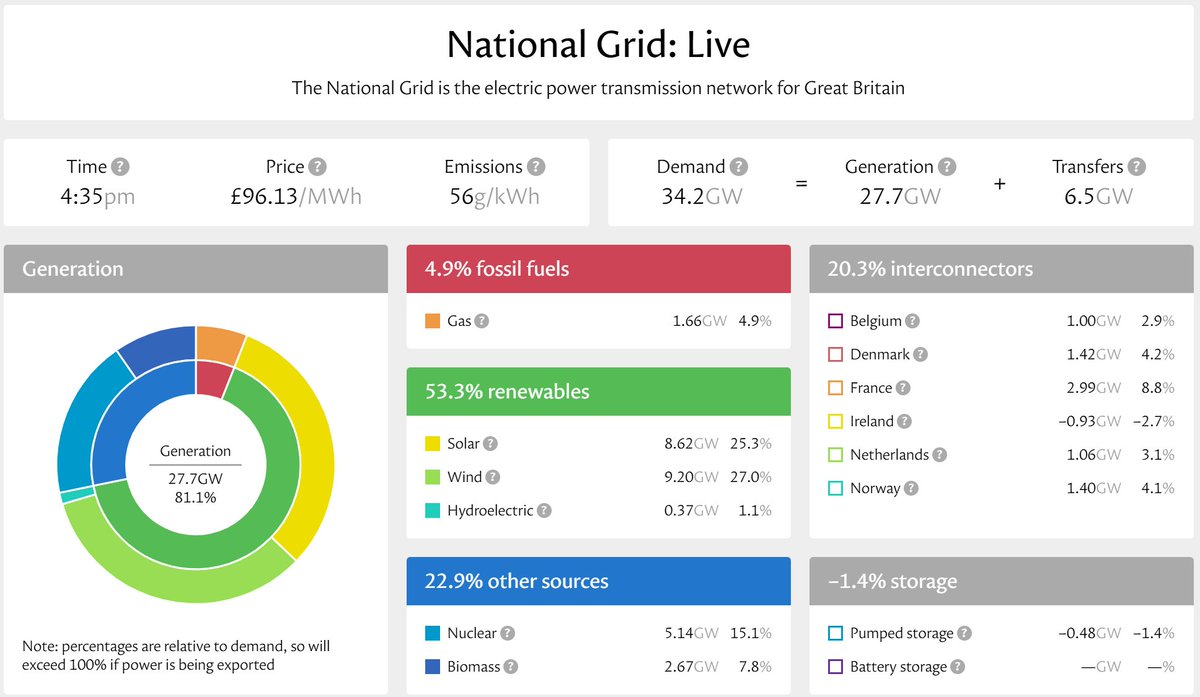

Pakistan installed so much rooftop solar that it broke its own grid.

Daytime demand collapses when the sun comes up. Evenings? 4,000–6,000 MW shortfall.

Load shedding is back — not because of too little power, but wrong power at the wrong time.

Meanwhile in the UK right now:

→ 67.6% clean electricity

→ Carbon intensity: 56g CO₂/kWh

→ Importing 7.85 GW via interconnectors to Norway, Belgium & Ireland

That last point is the lesson Pakistan needs.

The UK doesn't just generate — it trades. Cables to 4 countries mean surplus gets sold, shortfalls get filled. The grid becomes a market, not a silo.

Pakistan is landlocked from friendly grids. No interconnectors. No storage mandate. No flexibility market.

Pakistan installed so much rooftop solar it broke its own grid.

87

140

713

83,168

Apr 28

State Bank just raised interest rates by 1%.

A missile fired in the Middle East just raised your borrowing cost in Pakistan.

Interest Rate ⬆️ = Stock Market ⬇️

market Market down.

The war didn’t stay in the Middle East. It followed your money home. 📉

#pakistanStockMarket

1

3

213

Sherdil Ismail retweeted

Apr 28

To those who still believe that raising interest rates will “cool demand” and tame inflation, just look around.

A one-way ticket on Fly Jinnah from Karachi to Islamabad tomorrow is now around Rs. 15,000. Lahore is 14,000.

This is in an environment where fuel costs have gone up, taxes on aviation are high, and the currency has already adjusted. If demand was “overheating,” ticket prices would be rising, not compressing.

What does this tell you?

Demand is already broken.

People are cutting back. Discretionary spending is shrinking. Travel, one of the most visible indicators of middle-class consumption, is clearly under pressure. Airlines are holding prices despite rising costs because they simply cannot pass them on.

And yet, we continue with the same textbook response: raise interest rates to suppress demand.

Suppress what demand?

Private sector credit in Pakistan is already weak. Investment is stagnant. Real incomes have been eroded by inflation and taxation. The informal economy continues to operate outside the documented net, while the formal sector gets squeezed further.

This is the core problem:

Our inflation is not demand-driven. It is cost-push, energy prices, currency depreciation, indirect taxation, and supply-side inefficiencies.

Raising interest rates in this environment does not reduce inflation meaningfully. It only:

Increases the government’s debt servicing burden

Crowds out private investment

Punishes the documented economy

Rewards passive capital over productive enterprise

The Rs. 15,000 airfare is not just a price point. It is a signal.

A signal that demand is already decimated and policy is still fighting the wrong battle.

22

32

206

20,872

Sherdil Ismail retweeted

Apr 28

🚨 The Sharif family has 28 IPPs, Other PML-N leaders have 16 IPPs.

Asif Ali Zardari has 16 IPPs, while Other PPP leaders have 9 IPPs.

- Esar Rana.

126

2,003

3,839

88,623

Sherdil Ismail retweeted

Apr 27

Argument is that Sitara Petroleum Service Limited (SPSL) IPO is available at a discount (between 4 to 6 PE) compared to OMC Peers having an average PE of 8.52.

Counter argument is that SPSL is a logistics provider, dealer and distributor of GO OMC and not an OMC in itself at the moment so comparing it with OMCs PE wont be an apple to apple comparison. If thats the case, what price would be a good bargain for such company?

Also if a company is so good that it has tripled its revenues in 2 to 3 years, why is it even valued at a discounted price?

All this and many other valuable insights are covered in this video 👇. youtu.be/qDt6Xmspvcc?si=lMzZ…

1

1

37

5,697

Apr 27

Saudi Aramco money is coming to the PSX. Sitara Petroleum Services Ltd is launching its IPO at Rs 13.50–18.90 per share, targeting Rs 4.8B in fresh capital. Book building starts May 4. Public subscription May 11.

1

2

307

Sherdil Ismail retweeted

Apr 23

If you are serious about options trading, this 1-hour Yale lecture is non-negotiable.

60 minutes lecture can teach you more about options trading than 99% of options trading courses.

Save this and watch it without distractions. 📌

67

1,153

5,819

756,387

Sherdil Ismail retweeted

107

105

722

110,589

Apr 14

High chances of @realDonaldTrump coming to Islamabad Pakistan for negotions.

If it’s true Pakistan Stock Market 200,000 points

1

7

301

Sherdil Ismail retweeted

2 Apr 2013

Time will tell who is Messi of Pak politics. I will let my feet/deeds do the talking :)

526

3,440

11,101