It’s easier to challenge an idea than to change a belief. GoS, 2026

Joined August 2012

- Tweets 21,461

- Following 1,260

- Followers 26,493

- Likes 173,806

3,662 Photos and videos

Pinned Tweet

Jun 8

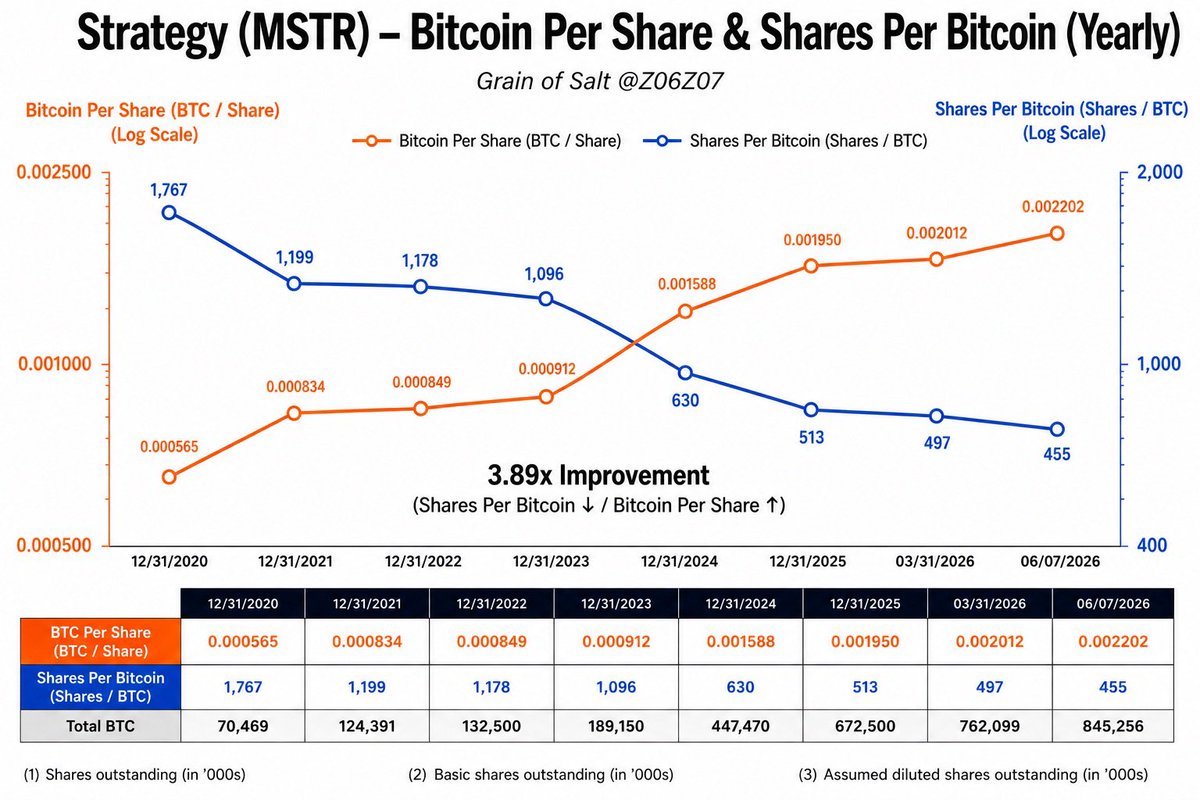

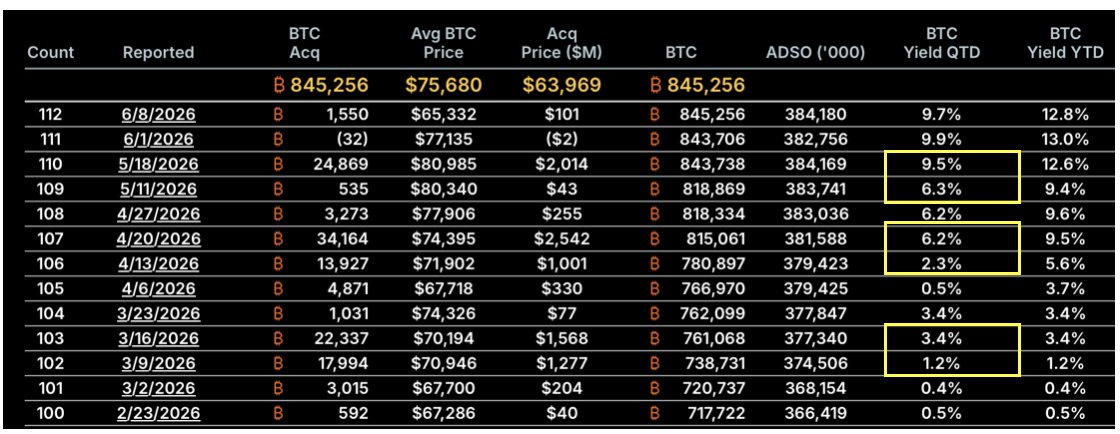

Here's the chart WITHOUT ratios for $MSTR, Bitcoin and Shares. The amount of Bitcoin that @Strategy has grown about ~4X the amount of share increase.

Any questions? @Saylor @phongle

Jun 8

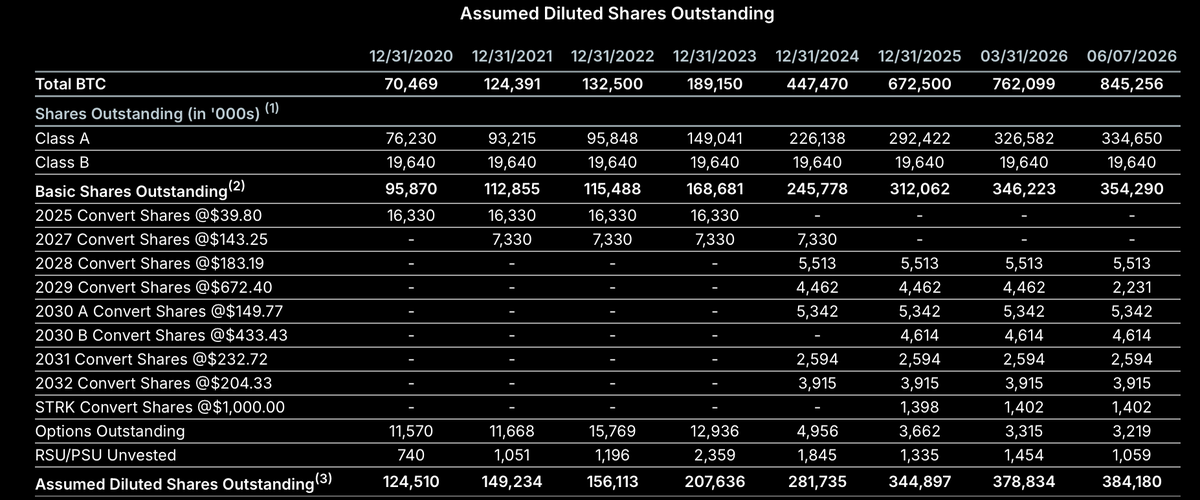

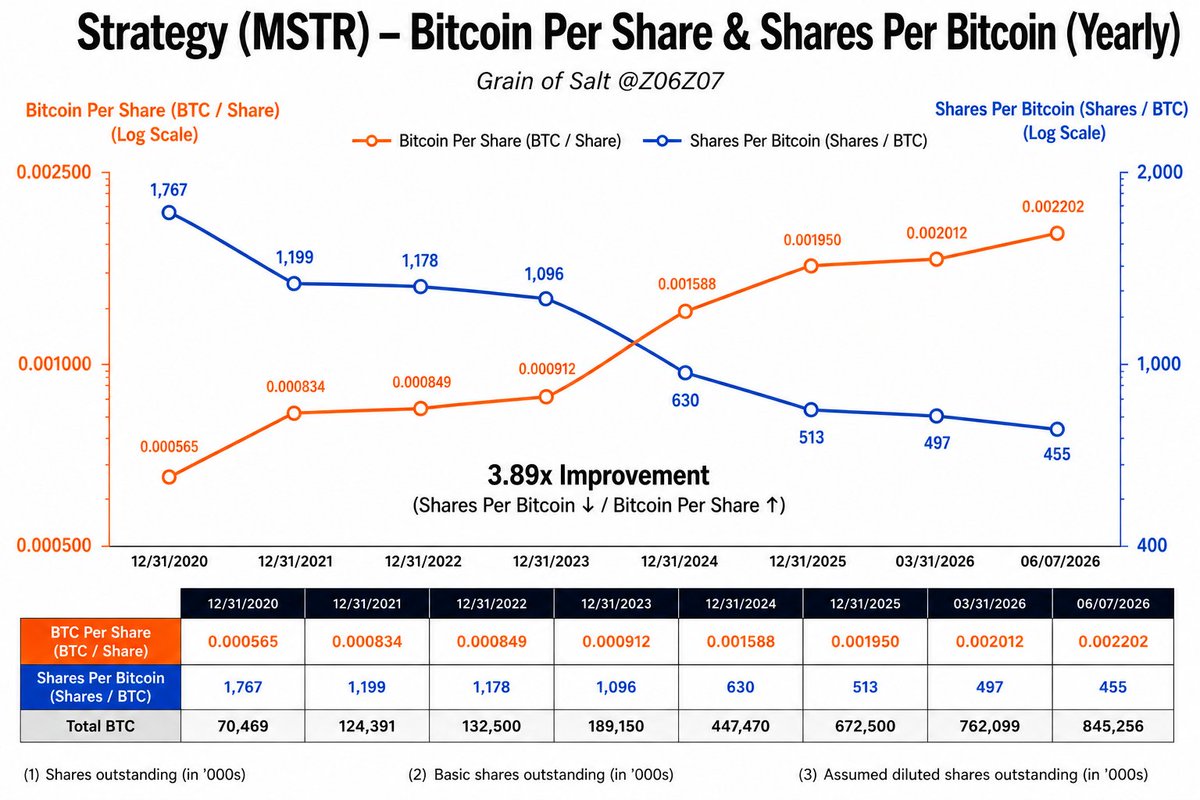

Strategy continues to accrete Bitcoin Per Share and inversely Shares per Bitcoin. It's been a 3.89X Improvement since the start of the Bitcoin Standard Era for $MSTR and @Strategy. @saylor @phongle @rohanhirani_

Thank you for attending my Grain Talk.

8

15

108

25,550

11h

Hey @jackmallers

mNAV is a snapshot metric.

Shares per Bitcoin (BTC Yield) is a path metric.

At 43,514 BTC, a Strategy-equivalent ownership geometry would imply ~19.8M shares outstanding for XXI.

Today XXI has ~346M shares outstanding (~17.5× more shares per BTC).

Not making a judgment here.

Just pointing out that mNAV measures valuation at a point in time, while Shares per Bitcoin measures ownership geometry over time. They answer different questions.

11

7

107

5,620

Grain of Salt retweeted

13h

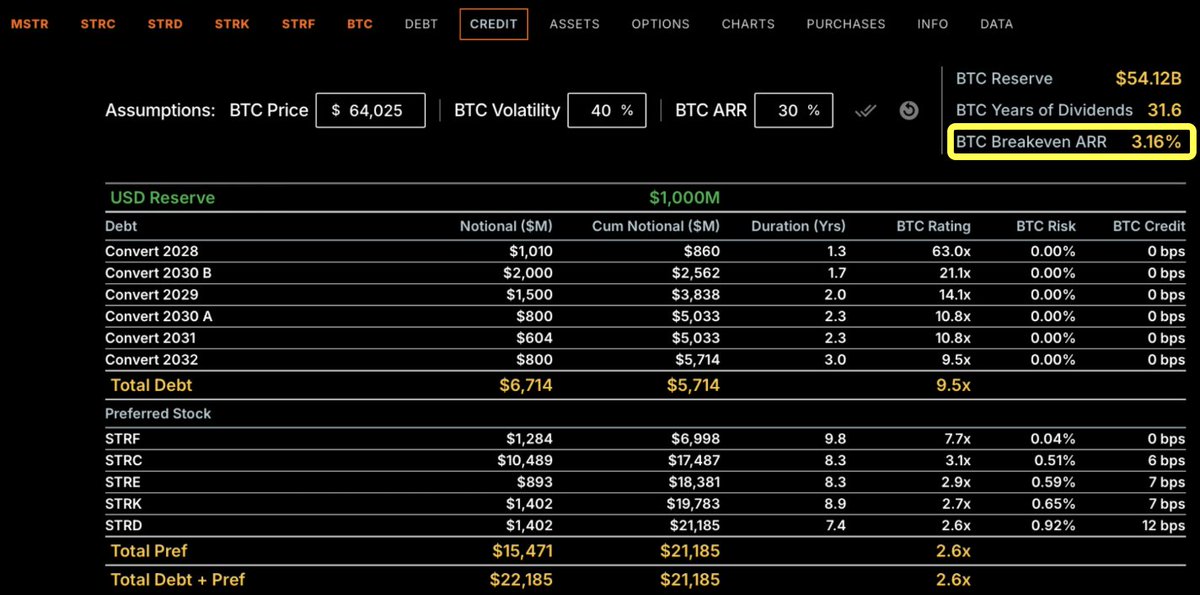

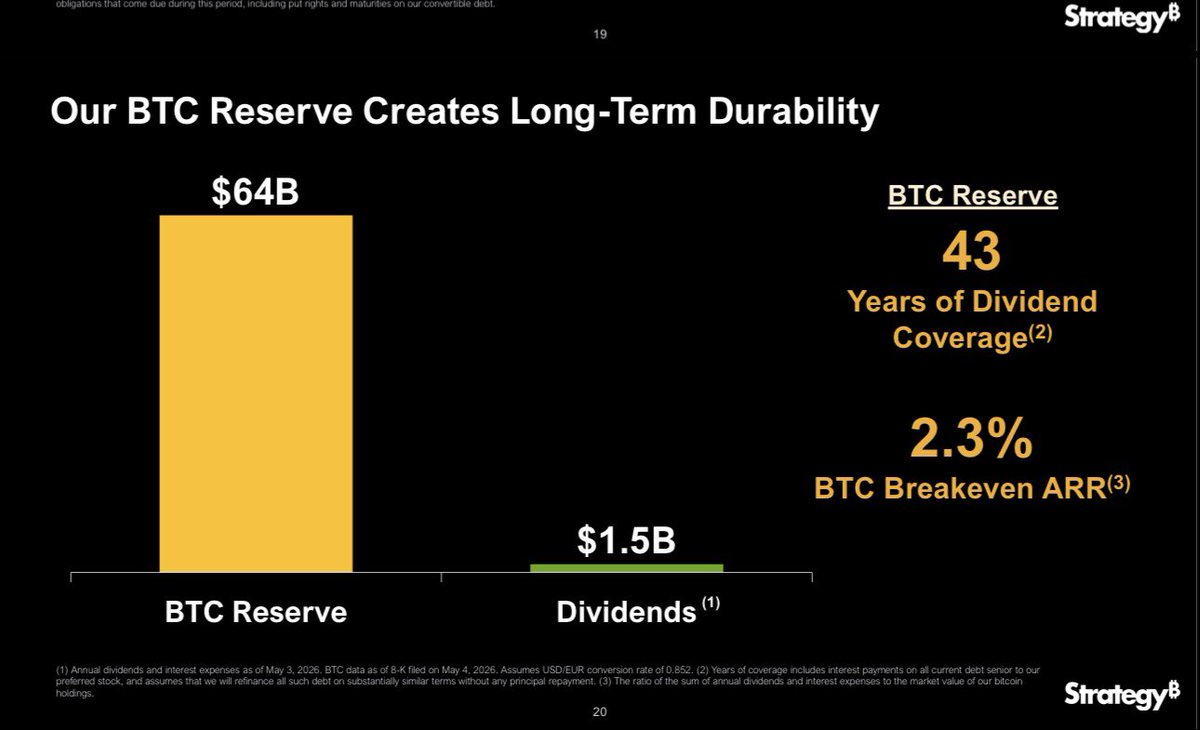

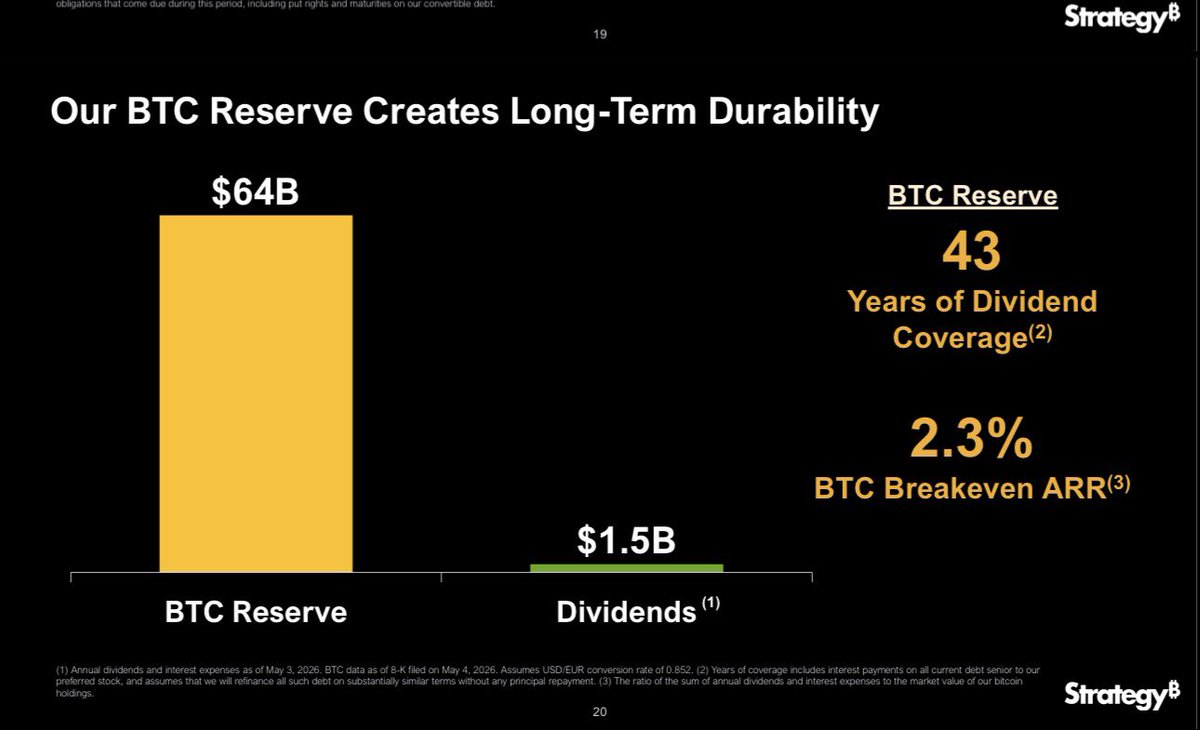

This was in the Q1 Strategy Preso, but just realized it now. For @Strategy, Bitcoin needs to go up 3.16% ARR not a ~11% because of the BTC Reserve at $54.12B for them breakeven on their dividend obligations. Updated every 15 seconds. @AdamBLiv

strategy.com/credit

4

4

57

3,479

Grain of Salt retweeted

13h

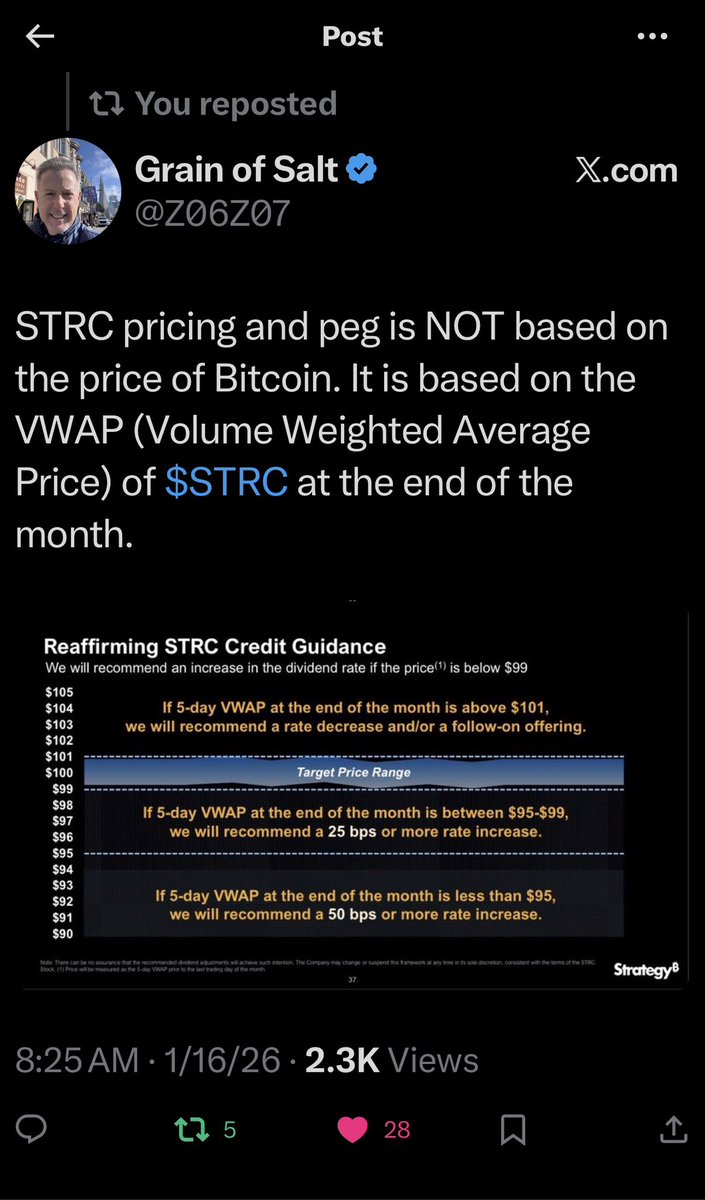

That's the problem. Three definitions of the word Yield.

1. BTC Yield as defined by Strategy is an increase in Bitcoin Per Share.

2. $STRC pays a fiat Yield of 11.50 APR funded from selling $MSTR.

3. Typical Yield on a stock is paid by income statement cash flow.

x.com/Z06Z07/status/20640921…

Jun 8

Strategy continues to accrete Bitcoin Per Share and inversely Shares per Bitcoin. It's been a 3.89X Improvement since the start of the Bitcoin Standard Era for $MSTR and @Strategy. @saylor @phongle @rohanhirani_

Thank you for attending my Grain Talk.

3

1

19

1,770

Grain of Salt retweeted

Bitcoin’s biggest buyer hasn’t left.

While ETF investors continue to sell, Strategy is still adding Bitcoin to its balance sheet.

The company now holds more than 845,000 BTC and remains one of the few large players still absorbing supply.

6

7

61

4,498

Jun 12

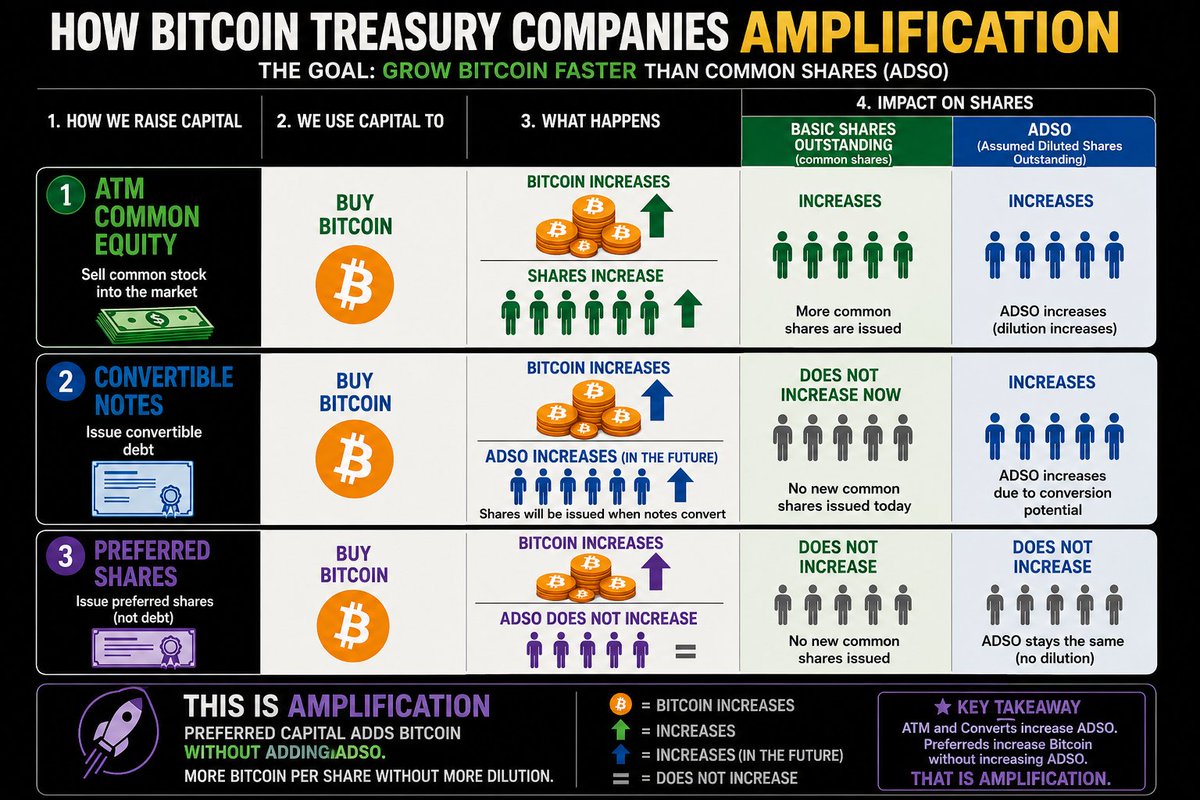

Bitcoin Treasury companies are balance sheet companies that use public equity markets (capital formation) to acquire Bitcoin in an accretive fashion. Right now, only @Strategy and @Strive are executing. I have written a book, done videos and consistently explain the situation and approach.

Anybody got an idea what I can do to get the point the across more effectively or should I just wait for Bitcoin price to go up and bull post?

Jun 12

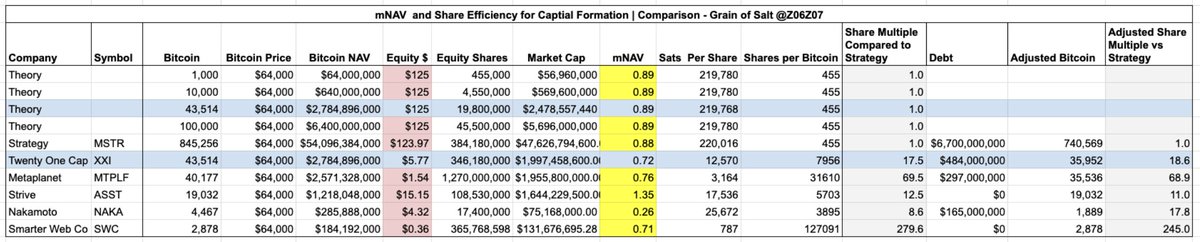

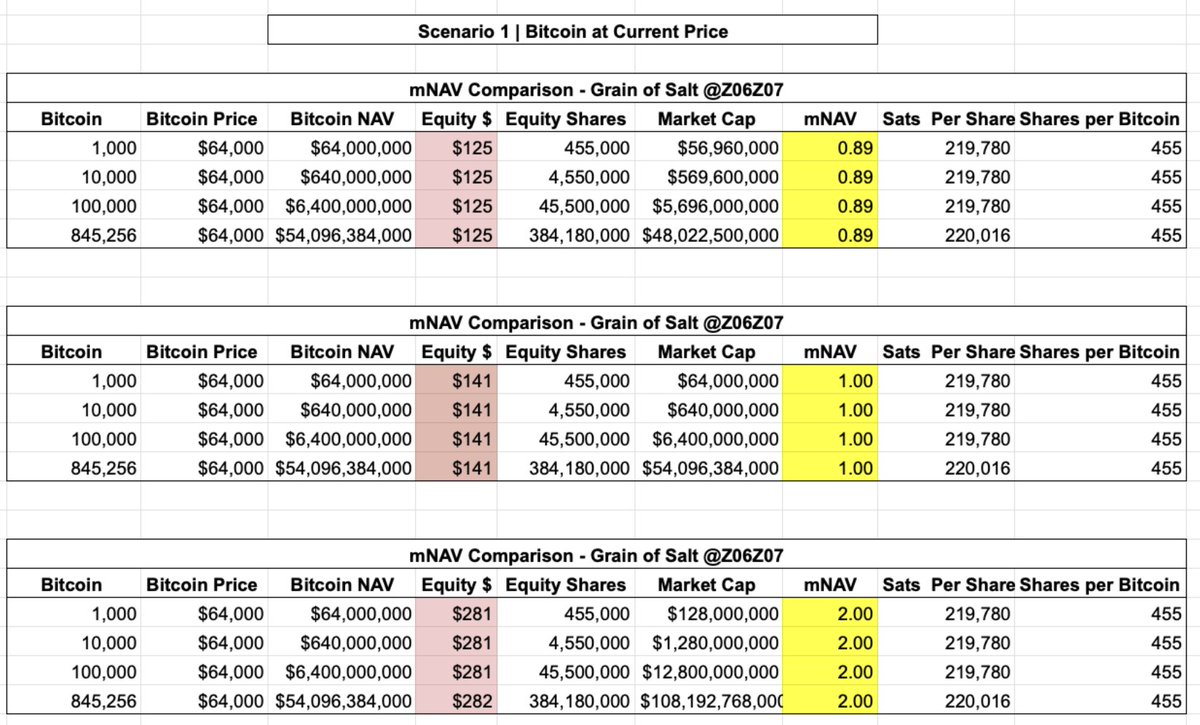

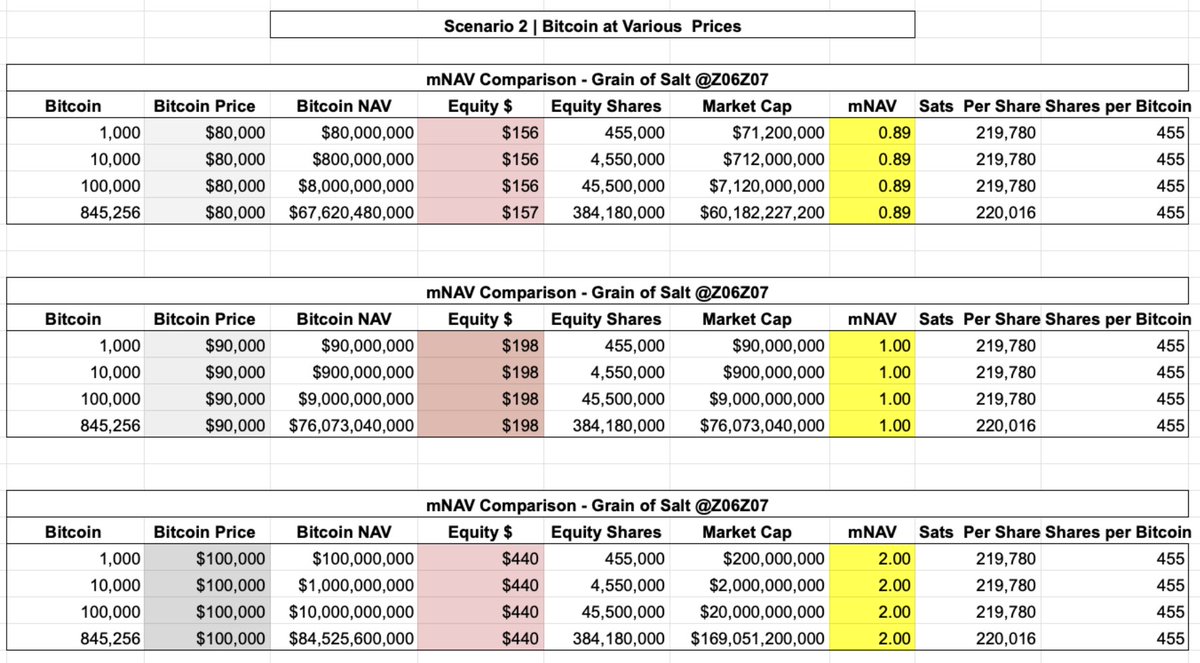

@jackmallers mNAV is blind to scale.

The four companies below have identical:

• mNAV

• Shares per Bitcoin

• Sats per Share

Yet one owns 1,000 BTC and another owns 845,256 BTC.That’s because mNAV is a ratio, not a measure of scale.

mNAV tells us how the market values equity relative to Bitcoin NAV.

It does NOT tell us:

• Treasury size

• Capital formation efficiency

• Ownership geometry

That’s why comparing mNAV alone never told us which Bitcoin treasury companies were actually creating shareholder value.

mNAV is useful. It’s just answering a different question than most people think.

14

4

84

11,673

Jun 13

Before we can discuss BPS, amplification, preferreds, or ownership geometry, we need to establish a simpler point:

mNAV is scale-invariant.

The two tables below hold constant:

• mNAV

• Shares per Bitcoin

• Sats per Share

Vary

• Treasury size

• Bitcoin price

A few observations:

A company with 1,000 BTC and a company with 845,256 BTC can have the SAME mNAV.

A company with 1,000 BTC and a company with 845,256 BTC can have the SAME Shares per Bitcoin.

A company with 1,000 BTC and a company with 845,256 BTC can have the SAME Sats per Share.

Changing Bitcoin price changes equity value. It does not change ownership geometry. That’s the point of the exercise. mNAV is a valuation ratio.

It is not a measure of:

• Scale

• Capital formation (durability vs. one time)

• Ownership geometry

• Scarcity

Those are separate concepts.

Once people understand why all six tables can be simultaneously true, then we can discuss why some Bitcoin treasury companies ended up with vastly different ownership geometries despite being built on the same Bitcoin.

2

1

25

2,815

Grain of Salt retweeted

Jun 13

Before we can discuss BPS, amplification, preferreds, or ownership geometry, we need to establish a simpler point:

mNAV is scale-invariant.

The two tables below hold constant:

• mNAV

• Shares per Bitcoin

• Sats per Share

Vary

• Treasury size

• Bitcoin price

A few observations:

A company with 1,000 BTC and a company with 845,256 BTC can have the SAME mNAV.

A company with 1,000 BTC and a company with 845,256 BTC can have the SAME Shares per Bitcoin.

A company with 1,000 BTC and a company with 845,256 BTC can have the SAME Sats per Share.

Changing Bitcoin price changes equity value. It does not change ownership geometry. That’s the point of the exercise. mNAV is a valuation ratio.

It is not a measure of:

• Scale

• Capital formation (durability vs. one time)

• Ownership geometry

• Scarcity

Those are separate concepts.

Once people understand why all six tables can be simultaneously true, then we can discuss why some Bitcoin treasury companies ended up with vastly different ownership geometries despite being built on the same Bitcoin.

2

1

25

2,815

Jun 12

Bitcoin treasury companies are not ultimately a game of Bitcoin accumulation; they are a game of preserving and increasing the SCARCITY of claims on Bitcoin.

1767 claims -> 455 claims

Thank you for attending my Grain Talk.

@Strategy $MSTR $STRC

Jun 8

Strategy continues to accrete Bitcoin Per Share and inversely Shares per Bitcoin. It's been a 3.89X Improvement since the start of the Bitcoin Standard Era for $MSTR and @Strategy. @saylor @phongle @rohanhirani_

Thank you for attending my Grain Talk.

4

4

51

3,925

Grain of Salt retweeted

Jun 12

@jackmallers mNAV is blind to scale.

The four companies below have identical:

• mNAV

• Shares per Bitcoin

• Sats per Share

Yet one owns 1,000 BTC and another owns 845,256 BTC.That’s because mNAV is a ratio, not a measure of scale.

mNAV tells us how the market values equity relative to Bitcoin NAV.

It does NOT tell us:

• Treasury size

• Capital formation efficiency

• Ownership geometry

That’s why comparing mNAV alone never told us which Bitcoin treasury companies were actually creating shareholder value.

mNAV is useful. It’s just answering a different question than most people think.

6

11

102

16,682

Jun 12

@jackmallers mNAV is blind to scale.

The four companies below have identical:

• mNAV

• Shares per Bitcoin

• Sats per Share

Yet one owns 1,000 BTC and another owns 845,256 BTC.That’s because mNAV is a ratio, not a measure of scale.

mNAV tells us how the market values equity relative to Bitcoin NAV.

It does NOT tell us:

• Treasury size

• Capital formation efficiency

• Ownership geometry

That’s why comparing mNAV alone never told us which Bitcoin treasury companies were actually creating shareholder value.

mNAV is useful. It’s just answering a different question than most people think.

6

11

102

16,682

Jun 12

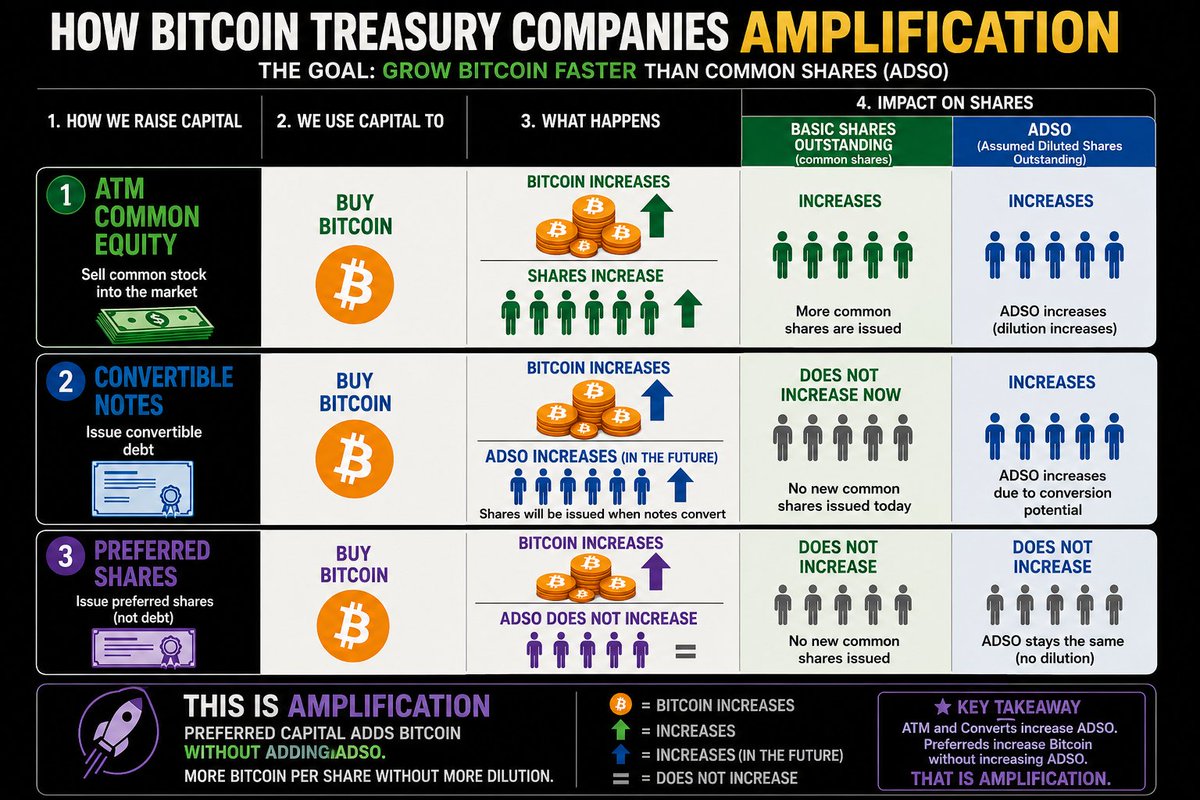

Here's my placeholder for the amplification debate we'll probably be having in June 2027:

Equity | Converts | Preferreds

BTC ↑ | BTC ↑ | BTC ↑

ADSO ↑ | ADSO ↑ | ADSO <->

Preferred: Bitcoin goes up. ADSO stays the SAME.

That's amplification.

Saving this now so I can reference it next year.

@Strategy $STRC @Strive $SATA

2

2

34

1,929

Jun 12

Here's my placeholder for the amplification debate we'll probably be having in June 2027:

Equity | Converts | Preferreds

BTC ↑ | BTC ↑ | BTC ↑

ADSO ↑ | ADSO ↑ | ADSO <->

Preferred: Bitcoin goes up. ADSO stays the SAME.

That's amplification.

Saving this now so I can reference it next year.

@Strategy $STRC @Strive $SATA

1

1

17

1,454

Jun 12

Here's my placeholder for the amplification debate we'll probably be having in June 2027:

Equity | Converts | Preferreds

BTC ↑ | BTC ↑ | BTC ↑

ADSO ↑ | ADSO ↑ | ADSO <->

Preferred: Bitcoin goes up. ADSO stays the SAME.

That's amplification.

Saving this now so I can reference it next year.

@Strategy $STRC @Strive $SATA

2

1

21

1,581

Jun 12

Here's my placeholder for the amplification debate we'll probably be having in June 2027:

Equity | Converts | Preferreds

BTC ↑ | BTC ↑ | BTC ↑

ADSO ↑ | ADSO ↑ | ADSO <->

Preferred: Bitcoin goes up. ADSO stays the SAME.

That's amplification.

Saving this now so I can reference it next year.

@Strategy $STRC @Strive $SATA

2

19

1,546

Grain of Salt retweeted

Jun 11

16

8

82

4,739

Grain of Salt retweeted

Apparently the bear case for bitcoin is that someone bought too much of it.

147

49

1,072

47,891