Joined January 2011

- Tweets 5,235

- Following 592

- Followers 1,120

- Likes 33,562

1,421 Photos and videos

Pinned Tweet

Jun 5

📉 Credit spreads are just 16% of global IG corporate bond yields.

The lowest reading since July 2007 😱

The other 84%? Pure govies.

Meanwhile EUR IG just traded in a 4.5bp range over the past month — a decade low for realised vol 😎

Record supply. Record ECB QT. Primary NICs at March wides. Book covers at 2-year lows. Inflation picking up, PMI going down.

And secondary refuses to move 😅

My full weekly breakdown 👇

open.substack.com/pub/zegood…

3

5

482

ZeGoodTrader retweeted

Jun 3

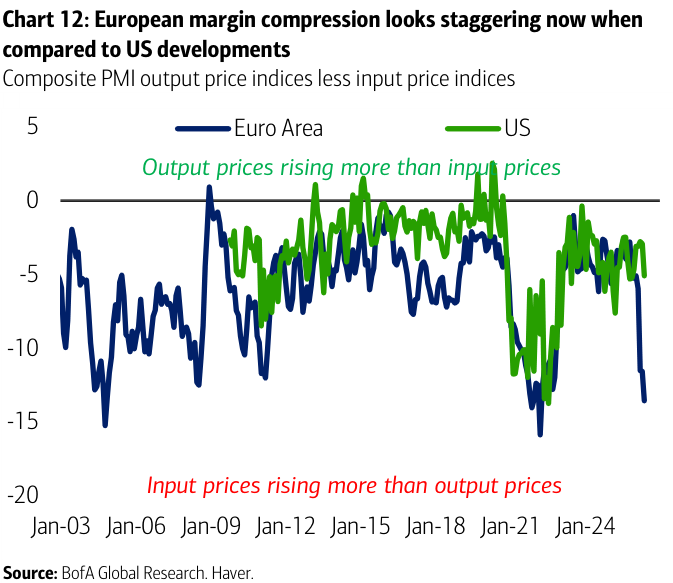

🔍 The chart European credit investors should be staring at.

PMI input prices are rising faster than output prices — the textbook signal for margin compression.

And in this cycle it's worse for European corporates than US ones.

Faster than 2022/2023. Bigger gap than ever 📉

→ Own pricing power. Avoid margin victims.

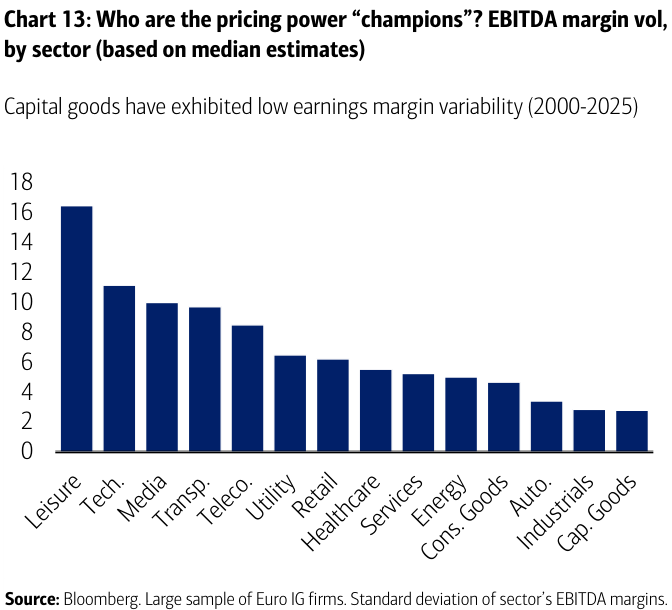

Capital Goods has the lowest EBITDA margin volatility in EUR IG since 2000. The sector to anchor portfolios in this regime.

2

3

170

Jun 12

Well long time no see !

Jun 12

Blackrock's Private Credit Fund Gates Investors Again After Redemption Requests Surge zerohedge.com/markets/blackr…

130

ZeGoodTrader retweeted

Jun 9

⚽ Citi's latest rates volatility hedge: the FIFA World Cup 😂

No seriously — the bank just reiterated its short vol trade because traders will be too busy watching football to move markets 😅 (and some people still believe "Markets are efficient"...)

The thesis:

📊 US and EUR short-dated rates vol HISTORICALLY stays low or grinds lower during the World Cup (June 11-July 19)

📊 2y-10y yield curve moves tend to be more modest than current market pricing implies

📊 "Traders potentially devoting more attention to matches than markets" = liquidity drain

🇫🇷 Note that @BofA_News picks France as the future winner ! 🥐

So, Are you shorting curve vol or do you think a macro surprise ruins the party? and more importantly: Who is your favourite?!

#FifaWorldCup #WeAre26 #CDM2026 #Somos26

3

5

182

Jun 11

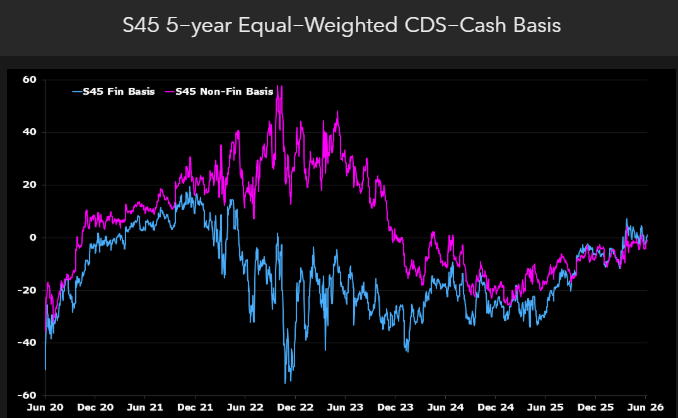

📊 CDS-cash basis back near par as cash bonds catch up to the March CDS rally — post-Iran war dislocation reversing

The moves:

🔵 Financials basis: -2.3bp (early May) → 1.3bp now

🔵 Nonfinancials basis: -4.4bp (early May) → -1.3bp now

🔵 Cash spreads rallied FASTER than CDS during peace deal wait, erasing the lag

What happened: CDS led the tightening in March during the conflict-driven hedging spike, cash bonds lagged. Now cash has caught up as volatility stays contained and index hedging demand normalizes.

The context: Both segments still BELOW the positive peaks seen during March war-driven hedging, but near-par basis = tighter alignment between cash and synthetic markets.

The technical setup: S45 5-year equal-weighted basis shows the convergence — financials now in POSITIVE territory while nonfinancials nearly flat.

👉 The takeaway: Cash-CDS convergence signals market stabilization post-conflict. Basis trades that worked in March/April compressed hard as volatility dried up and cash caught the synthetic rally.

❓ Are you still playing basis trades or is the dislocation opportunity gone?

2

141

Jun 11

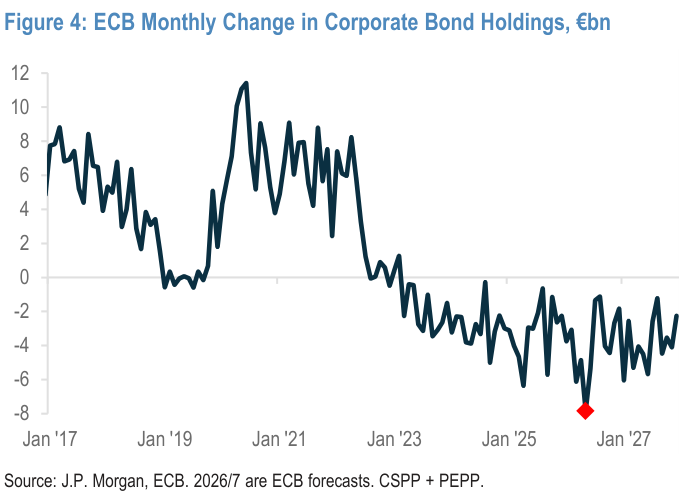

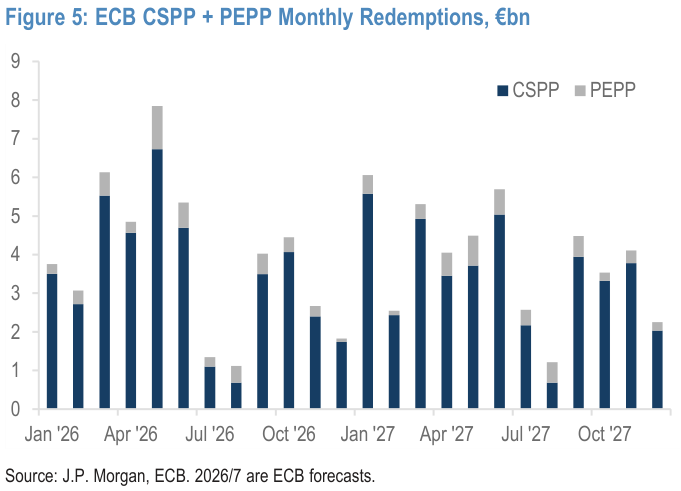

Credit IG continue to be strong YTD BUT... 📈

🔺 Investors are buying anything across IG world and realized volatility has dropped

🔻 Even though ECB isn’t buying bonds anymore but it’s still actively shrinking its balance sheet via Quantitative Tightening.

This month, corporate bond holdings under the CSPP and PEPP fell by ~€7.9bn, marking a record monthly drawdown!

That pace should ease into the summer, meaning this record drawdown is likely to stand through the end of next year.

Anyone surprised by an environment where ECB is doing QT but investors are behaving like it's QE all over again? 😅

1

4

163

Jun 10

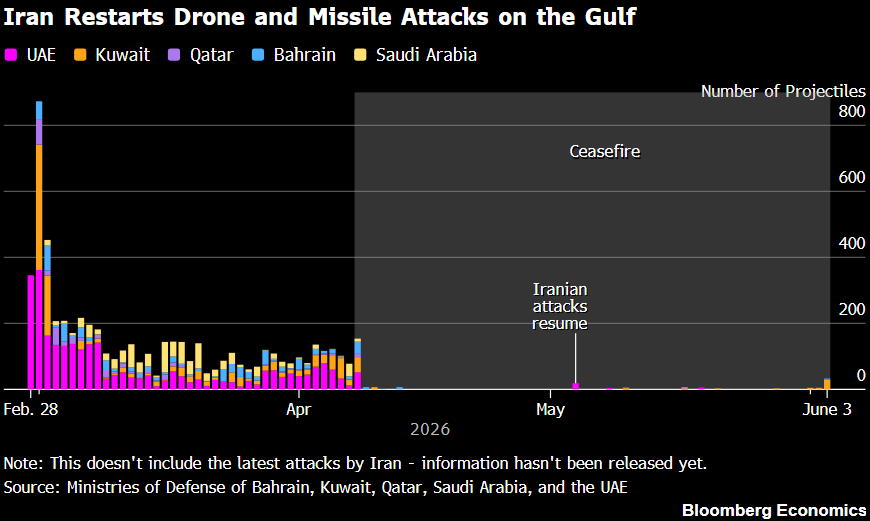

🚨 Iran-US truce ISN'T over despite latest strikes — Bloomberg Economics says this is the "new normal" of a ceasefire constantly being tested

What happened last 24 hours:

🔴 June 8: Iranian drone downed US Apache helicopter off Oman coast (Iran claims accident, 2 US soldiers survived)

🔴 US retaliated with 3 waves: hit ground control stations, air defense systems, radar sites civilian water infrastructure in southern Iran

🔴 Iran fired back at US bases in Jordan, Bahrain, Kuwait threatened Gulf Arab states hosting US bases

Why the truce holds:

✅ Trump's goal: reopen Strait of Hormuz lower oil prices ahead of midterm elections later this year

✅ Iran's goal: sanctions relief access to frozen assets after securing regime survival stronger deterrence

✅ Fighting intensity still LOWER than pre-April 8 levels

The strategy: Both sides using "escalate to de-escalate" — kinetic action to uphold red lines and gain negotiating leverage. Iran took a page out of Trump's playbook 📖

The takeaway: No lasting resolution = periodic cycles of violence with varying intensity. Iran clearly not defeated, retains means to retaliate against US assets in the region.

Are oil markets pricing this correctly or underestimating the tail risk?

1

1

138

Jun 10

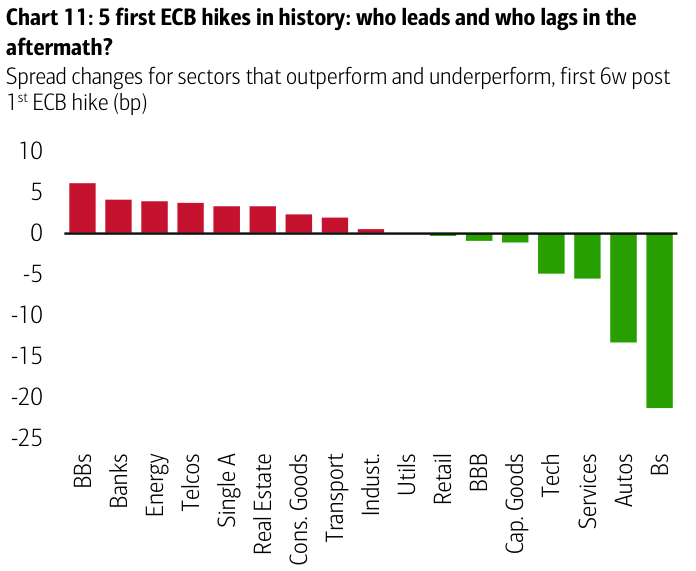

⚡ ECB hikes 25bp next week — first hike in 3 years

History says don't panic. Looking at 5 prior first ECB hikes since '99:

✅ Single-Bs rally 21bp average

✅ Autos -13bp

✅ Tech -5bp

✅ BBBs -1bp

🔴 Banks, telecoms, BBs leak wider

First hike = fuel for compression trade.

You positioned for this or fading it?

#ECB #EURCredit #RatHikes

2

1

128

ZeGoodTrader retweeted

Quand je regarde le graphe du pétrole, et que je constate que le Brent est à peine à 91$ avec tout le bordel qu'il y a, à peine 10% au dessus de prix qu'on connaissait début 2025, on se rend compte du pouvoir des mots et de la narration

4

1

8

1,005

Jun 9

🚨 BofA just flashed the warning: 70% of bear-market signals triggered — time to TAKE PROFITS

The red flags:

🔴 S&P 500 statistically expensive on 17 of 20 metrics

🔴 8 metrics richer than tech bubble levels

🔴 High P/E stocks crushing low P/E = excessive speculation

🔴 Tech spread between best/worst performers WIDEST since Feb 2000

🔴 Top vs bottom decile returns: post-Covid era HIGH

🔴 Hyperscaler capex hitting 100% of operating cash flow (vs 40% in 2023)

🔴 Cash flow conversion flat-lined, buybacks slowing, IG/equity supply surging

🔴 Fed SLOOS: consumer demand softening, credit stress rising

BofA Subramanian: "Extreme price action may signal rising instability" but S&P 500 year-end target still 7,100 (vs 7,406 now)

🟢 On the other hand, S&P trading THAT far above its 50MA is historically a strong BULLISH Signal (2.62 sharpe ratio ❗ ) so Are you taking profits or fading the bear call?

1

3

170

Jun 8

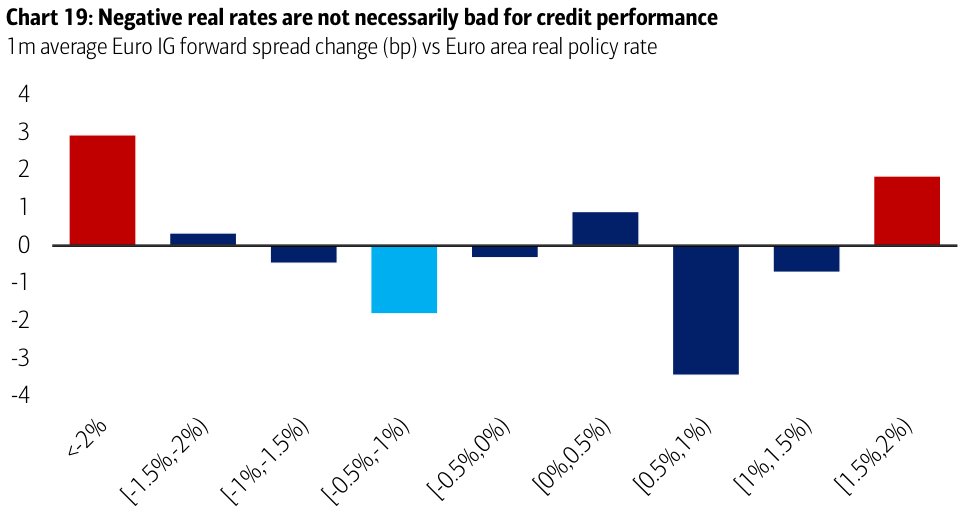

📉 Real ECB rates at -1% after next week's hike = the SWEET SPOT for credit

30% of developed economies have negative real rates right now. That's not a bug, it's a feature 💡

Too negative = ECB behind curve (bad)

Too positive = financial conditions too tight (bad)

-1% = Goldilocks for spreads

Do you agree with this framework?

#Inflation #CreditStrategy #Macro

4

6

287

Jun 7

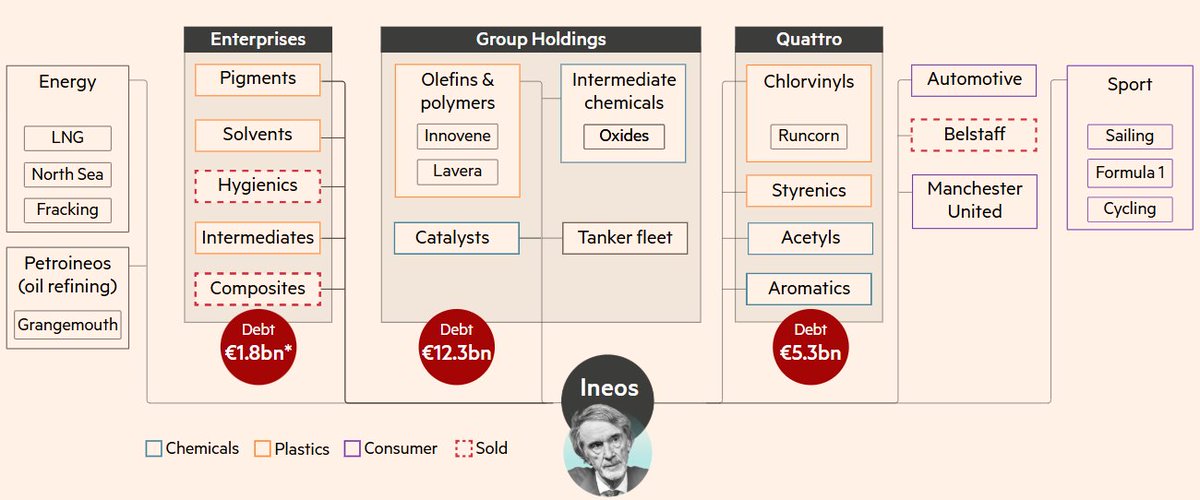

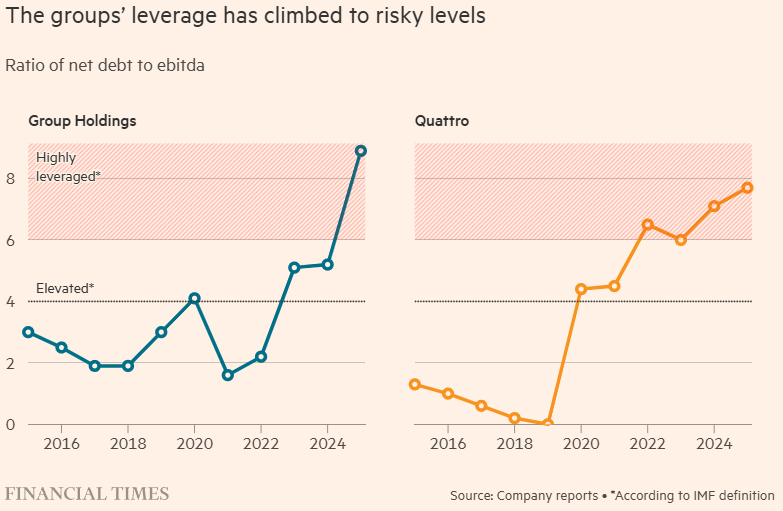

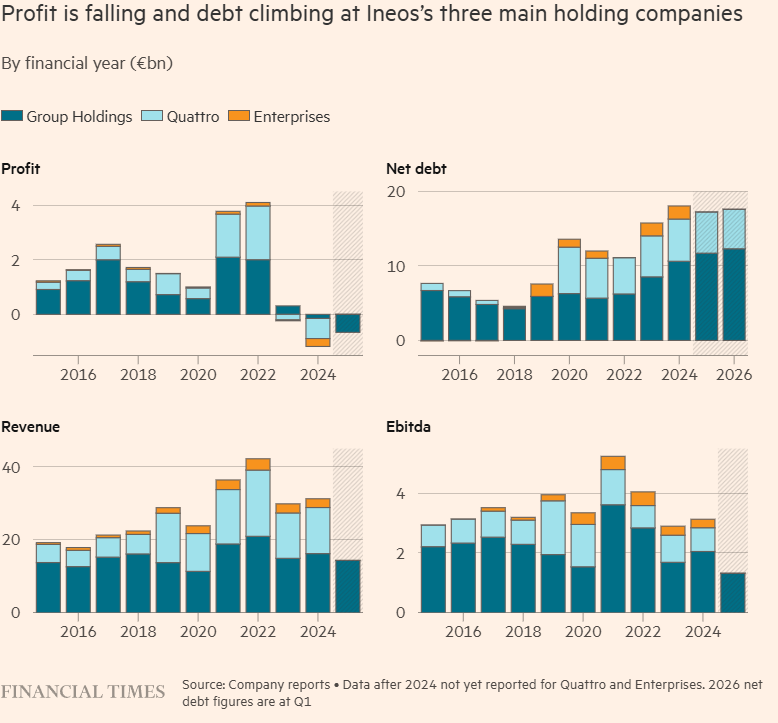

🔥 INEOS credit: hedge funds shorting it got SQUEEZED by the Middle East war — now investors are sharply divided on whether Ratcliffe's $19bn debt pile survives

The setup:

🔴 BOTH main divisions lossmaking — Group Holdings -€650mn, Quattro -€800mn in 2025

🔴 Leverage surging as debt nearly DOUBLED since 2021 (Project One capex)

🔴 €1.35bn maturities coming 2027 across both entities

🔴 Annual interest: €1.33bn combined

The reprieve:

✅ Group Holdings just refinanced €700mn OVERSUBSCRIBED last month

✅ Iran war disruption reversed capacity overhang — olefins/polymers prices surging in North America while feedstock stayed cheap

✅ Q1 2026: €421mn EBITDA €400mn expected in April (war boost)

✅ Hedge fund shorts forced to unwind positions

The make-or-break bet: Project One €4.8bn Antwerp plant (Europe's first new cracker in 20 years) completes end of 2026. Expected to add €700mn annual EBITDA from 2027. Designed to exploit US gas/EU chemicals price spread 💰

The problem child: Quattro can't access primary bond markets per multiple credit investors. Structurally cash flow negative, closing plants, selling assets. Has €2bn cash cushion (equity injection inventory financing) but bleeding 🩸

Credit investors DIVIDED:

🐻 "Debt unsustainable, Quattro heading for restructuring"

🐂 "Scale and competitive edge will carry it through, Project One fixes the balance sheet"

💭 My View: This is a war-driven reprieve on borrowed time. The fact they got €700mn done oversubscribed is impressive, but both divisions are STILL lossmaking with €1.33bn annual interest expense. Project One better deliver that €700mn EBITDA boost in 2027 or Group Holdings joins Quattro in restructuring territory. The olefins price surge is 100% driven by Iran war supply disruption — when that fades, spreads compress and you're back to structural overcapacity in Europe competing with cheap Middle East/Asia supply. Quattro is toast without asset sales or a restructuring. The shorts got squeezed but the fundamental credit story hasn't changed.

Are you buying the war bounce or fading this as temporary?

1

3

180

ZeGoodTrader retweeted

Jun 5

📉 Credit spreads are just 16% of global IG corporate bond yields.

The lowest reading since July 2007 😱

The other 84%? Pure govies.

Meanwhile EUR IG just traded in a 4.5bp range over the past month — a decade low for realised vol 😎

Record supply. Record ECB QT. Primary NICs at March wides. Book covers at 2-year lows. Inflation picking up, PMI going down.

And secondary refuses to move 😅

My full weekly breakdown 👇

open.substack.com/pub/zegood…

3

5

482

Jun 5

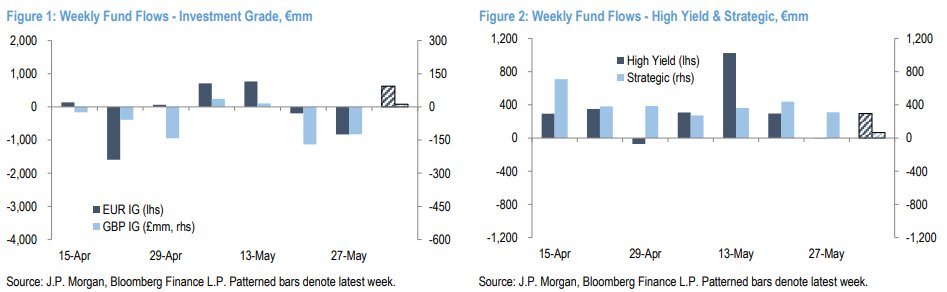

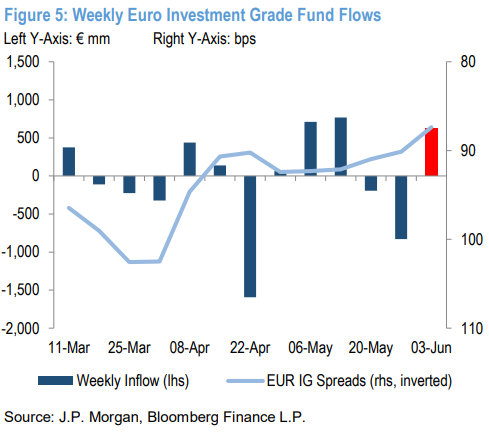

JPM says money is still entering Credit funds! 📈

Weekend 03 June flow check-in:

- 💶 Euro IG funds took in €624mm ( 0.2% of AUM).

- 💷 Sterling IG funds were basically flat: £12mm (~0% of AUM).

- 📈 European HY funds drew €296mm ( 0.3% of AUM).

- 🧠 European strategic funds inched up €66mm (~0% of AUM).

1

3

102

ZeGoodTrader retweeted

Jun 4

The giant sucking sound of retail money exiting private credit continues..

BCRED: 10% redemption requests, 5% cap

6

12

94

18,593

Jun 4

🏦 European bank bonds: AT1s leading with 2.2% excess returns YTD vs 0.6% senior and 0.7% T2 — but the carry story is compressing FAST

The setup:

✅ AT1 carry ~5.2% (vs sovereign bonds)

✅ Strong April/May reversed weak Q1

✅ Demand technicals strong, supply benign

The problem:

🔴 AT1 carry was 8% start of 2024 → 6% during Iran war March → 5.2% now

🔴 350bp of carry compression in 18 months = most gains already realized

🔴 Returns "highly sensitive to geopolitical risk and weaker macro" per @Bloomberg

1

6

105

Jun 3

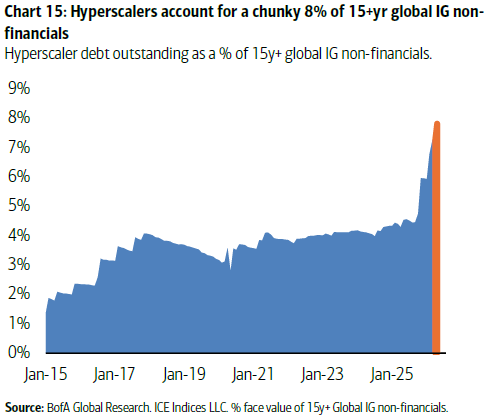

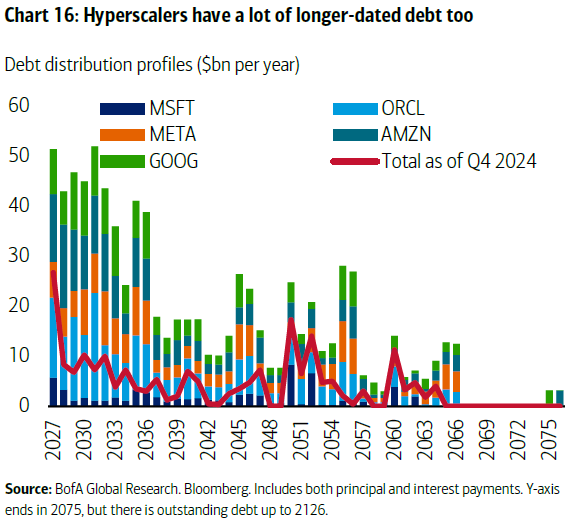

🤯 Hyperscalers are only ~3% of the global IG market.

But they're 11% of the Euro IG 15 yr non-financial market.

The whole AI capex debt binge isn't sitting evenly across the curve. It's piled into the very long end where Reverse Yankees live 🏗️

If 2H supply slows (frontloading done, cash flows strong), this corner of the market is set up for a rally.

Long-end Euro credit → the asymmetric 2H trade?

1

126

Jun 3

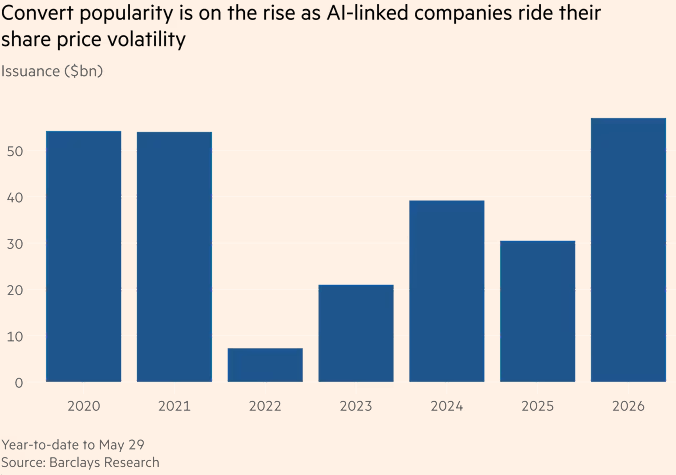

💥 US convertible bond issuance on track for RECORD year — $57bn YTD already, set to blow past 2025's $120bn total

The AI volatility play:

🔵 AI-related companies issuing converts at ZERO coupon — monetizing sky-high stock volatility instead of paying interest

🔵 CoreWeave: $3.5bn converts at 1.75% coupon vs 9.75% for regular senior notes (same company, same week) 📉

🔵 Akamai: $3.5bn at 0% coupon

🔵 ON Semiconductor: $1.3bn at 0% (initially marketed at 0.5%, demand so strong it got priced at ZERO)

Who's issuing? NOT the hyperscalers (Microsoft, Google, Amazon) — they've got cash flow pouring in. It's the secondary/tertiary AI beneficiaries with big capex needs and little cash flow tapping this market 💰

The mechanics: Higher stock volatility = more valuable conversion option for investors = companies can issue at lower coupons (or zero). Conversion thresholds set 75-100% ABOVE current stock prices, limiting dilution risk.

Who's buying? Convertible arbitrage hedge funds absorbing the surge — buying the bonds, shorting the stock, profiting from volatility swings either direction 📊

3

162