Tech/Autos analyst at Global Energy Transition L/S fund; Ex-HSBC analyst; IIT-B Nanyang MBA; In the long term, we're all dead!

Joined July 2009

- Tweets 15,392

- Following 1,491

- Followers 7,383

- Likes 25,371

2,554 Photos and videos

Pinned Tweet

10 Mar 2024

Guys, this profile has gone dead for a while as I morph into a new role.

Will be back with hopefully lot more - just a bit different. More focused on energy transition opportunities globally, particularly in tech & autos

Thanks for your participation so far, I appreciate it🙏

17

1

98

13,040

15 Mar 2025

If you are still able to prove them wrong, I won’t be surprised if @HDFCERGOGIC goes even further back and asks her to prove that she wasn’t born with cancer or heck! even born at all. This is an idiotic chase down a rabbit hole. Are there any avenues to address such grievances?

1

1

4

1,599

15 Mar 2025

Everyone knows that Corporate greed runs rampant in this country. Can still deal with it on Dalal Street but when it turns against honest tax paying middle-class citizens on the main street, its worth at least reporting the same. @HDFCERGOGIC is just one example of the same

6

1

9

1,566

4 Jul 2024

I think I will have to turn bullish for this market to fall😜

10

2

61

7,199

18 Jun 2024

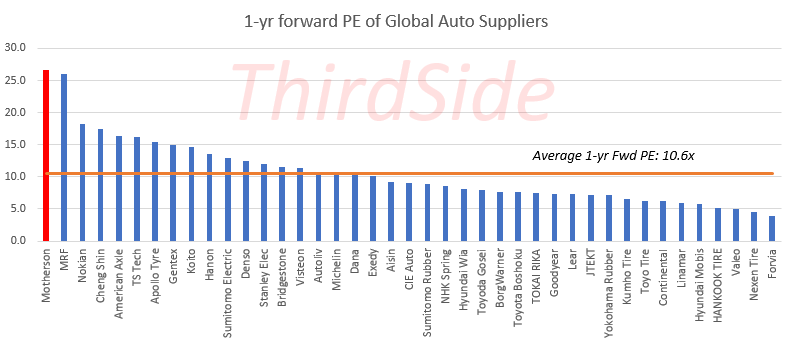

Motherson is a global auto supplier like the rest in this chart. You don't need rocket science to figure out the extent of overvaluation in India but let me give some colour anyways. (1)

18 Jun 2024

Bubble times so who cares about fundamentals but anyone interested in Motherson (Wiring Harness) should read this

techbriefs.com/component/con…

7

5

39

8,855

18 Jun 2024

Auto suppliers are driven primarily by Auto OEM volumes. S&P Global 2Q24 production estimates were downgraded last week from 2.6%YoY earlier to 0.5%. 2024 Light Vehicle production is now seen contracting 1.1% (2)

2

1

1

1,922

18 Jun 2024

Last but not the least, the outlook appear particularly dreary for European auto suppliers like Motherson since West Europe is likely worst hit with OEM production estimated at -6%YoY by S&P Global (China & America see modest growth).

1

1,256

18 Jun 2024

Globally, investors are nervous about auto suppliers due to likely OEM volume decline but recent comments from Stellantis on supplier cost savings are also creating margin worries i.e. margin squeeze by customers (3)

1

2

1,210

18 Jun 2024

Bubble times so who cares about fundamentals but anyone interested in Motherson (Wiring Harness) should read this

techbriefs.com/component/con…

3

1

25

11,637

8 Jun 2024

Looking for an intern equity analyst for global autos, auto ancs & semis coverage, preferably based in South Delhi, but NCR will also do. If anyone is interested, please DM me with your CV & pay expectations. This is a 6 month gig, but if all goes well, it can turn to FT position

7

2

17

5,477

28 Feb 2024

With AI, this will be possible but will it be as much fun?

1

4

3,419

ThirdSide retweeted

17 Feb 2024

I shall be tweeting on 8th edition of TIA 20-20 Ideas summit (2024 episode) today. This is organized by @TIA_Investors .

4

61

281

152,061

16 Feb 2024

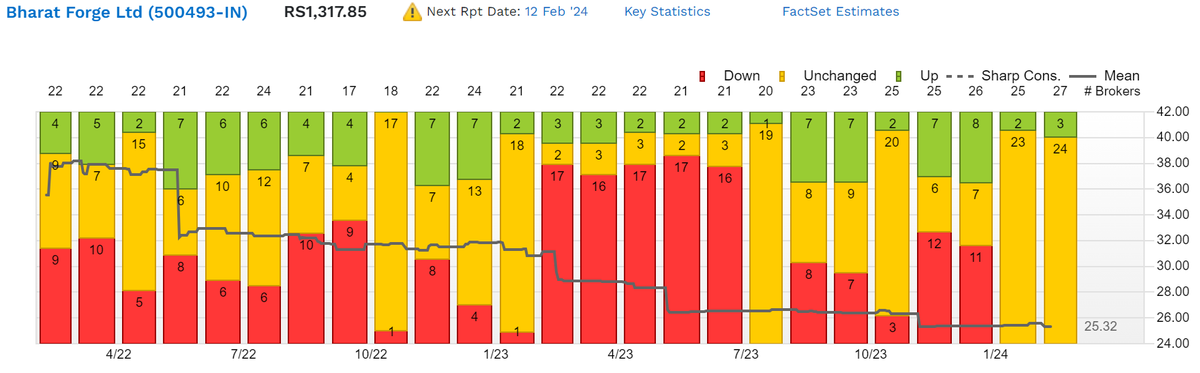

Longish post on two stocks that continue to confound me - TVS Motors & Bharat Forge. For some reason, market doesn't give a damn about their loss-making international ops which appear in their consolidated earnings but only on an artificially inflated parent numbers.

Consolidated EPS is 20-35% lower which makes these stocks are far more expensive on these earnings. Their parent-EPS based 1-yr fwd PE is 39x (TVS) & 34x (BForge) but true consolidated 1-yr fwd PE is 45x

It would have still been ok, had a turnaround in loss-making international ops been imminent but this is not the case. BForge has already said enough but think about TVS. It has two big businesses here 1) Norton bikes & 2) EU e-Bikes.

They have guided Norton to stay in "investment stage" i.e. loss making for next 6-8 quarters. As for e-Bikes, TVS has stayed mum but Yamaha Motors isn't saying very pretty things about their e-bike business with guidance of another loss-making year. So a turnaround looks very far from a done deal for TVS Motors. In fact, it very much gives the sense of being another M&M - dicking around here & there and burning cash....

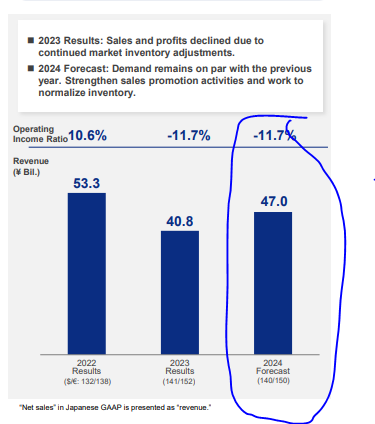

Insert from Yamaha Motors latest results PPT👇 on guidance about their e-Bike (SPV) business

3

2

11

4,456

16 Feb 2024

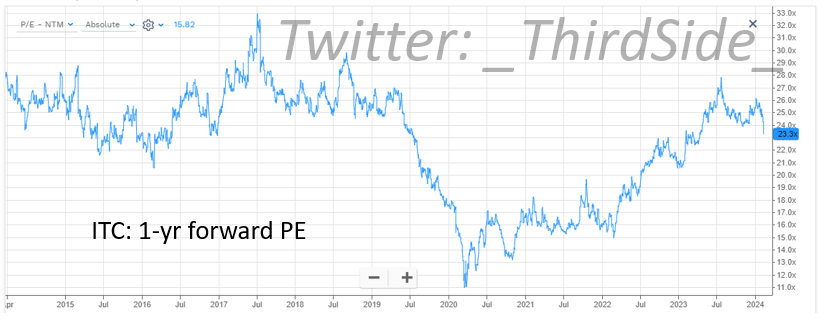

ITC at 400 prices the following on FY24 EV/EBIT:

Cigarettes at 18x (Godfrey/VST Ind @ 17x)

FMCG at 45x (HUL/Britannia/GCPL~47x/42x/40x)

Hotels at 30x (Indian Hot/Chalet/EIH~45x/39x/23x)

Agri/Paper at 7x (JK Paper~5x)

4% dividend yield

In other words, no premium for cigarettes' market share or faster growing FMCG biz

8 Feb 2024

Is BAT dumping 29% stake in ITC? Going by their con-call, looks more like 4% (29%-->25%) with no clarity on timing. Makes it similar to GSK sale of HUL stake during Covid trough (was done at about 5% discount to stock price). BAT comments from con-call👇

We want to keep a level of influence in ITC that is transforming itself based on local legislation there, we need to have a minimum 25% of shareholder to keep veto rights, veto rights we would like to do in the first phase. And this means that given the fact that we have above 29%, there is space for us to reduce our shareholding.

Very difficult. Very difficult for me to give you a timeline on that, other than to say that we are doing all we can to create this flexibility, so the board can make an assessment in terms of capital allocation decision moving forward.

Meanwhile, we are very supportive of our shareholding. ITC is a fantastic company, a well-run, well-managed, very fast growing company in a very fast growing market with the most populous country in the world and the contributing accretive for BAT in terms of earnings also in terms of cash, because they have a very good policy in terms of dividend payouts.

12

8

74

35,461