Propagating Halal Investments | Not an Investment Advisor

Joined September 2010

- Tweets 1,757

- Following 2,060

- Followers 2,302

- Likes 2,469

225 Photos and videos

Your tweet is internally consistent. Repeatedly saying “no real difference” and calling it just ‘semantics’ ignores key differences in how Islamic contracts actually work.

Interest and profit on a surface level mean two different things. You get profit from a business activity after deducting expenses. Interest is the charge you add to the money you lend. So first of all you cannot logically say it is semantics except you don’t know what you’re saying.

Going into details. Halal finance and interest finance differ in legal form, ownership transfer, contractual basis, approval process, and the type of business the money can even be used for.

Take a mortgage for example.

I go to Jaiz bank to get a mortgage in order to buy a house

You go to Zenith to get a mortgage to buy the same house.

Zenith gives you the money to buy the house and charges you interest of 10% on the money you borrowed. When you buy the house, you own the house and you owe Zenith the money you borrowed. If your house gets burnt by fire. You must still pay Zenith the money and interest

Jaiz bank doesnt give me the money. They buy 80% of the house and ask me to contribute the 20% to the house. We co-own the house (80/20 split). I then lease their share while gradually buying it out over time.” Every month I pay rent of N100 from which N80 goes to them and N20 is used to increase my share of the house and reduce their share of the house. When the house gets burnt I am responsible for my share of the house (e.g 20%). I dont need to pay back all the money used to buy the house

PS: Murabaha, the contract is a sale, not a loan, with different legal consequences.

It’s semantics, one is designed to be ethically acceptable for Muslims, the other is the conventional approach to borrowing.

There is really no difference, just softer approach and kinder attitude to the same principle for the halal banks.

You need a 1m naira loan to purchase an oven for your bakery, you go to zenith and they give you the million naira loan with a 35% interest per annum which you would pay back at a particular rate monthly, you sign your contract get your loan.

You need the same 1m naira loan, and an Islamic banks could decide to buy the oven on your behalf, give it to you, and allow you to start making money, but then you buy the oven back from them for 1,350,000 naira over the next 1 year.

You need a loan for your business and you go to a conventional bank and take money and they tell you the interest and you draw up a repayment plan.

You need a loan for your business and go to an Islamic bank, and they see themselves as an investor in your business and you as a partner. They give you capital and you put it to use. You then pay back in “profits” based on a percentage basis they give you.

Islamic banks are creative with their approach, they offer ease and play within the fine prints of what is permissible in Islam, but the principle of banking and making money is the same for both banks.

Mind you Islamic banks take collaterals also 🙂🙂🙂🙂

2

1

9

1,556

Most people call me Yaks.

Jun 11

Any nicknames for a boy named Yakubu ?

244

Very illiquid stock. Buying Airtel is like buying real estate. Takes time to sell

Jun 11

Does anyone here actually have AIRTELAFRI in their portfolio?

Because I never see anyone talking about it.

1

1

8

947

Yaks retweeted

Jun 9

Focus on improving yourself, not proving yourself.

2

3

30

326

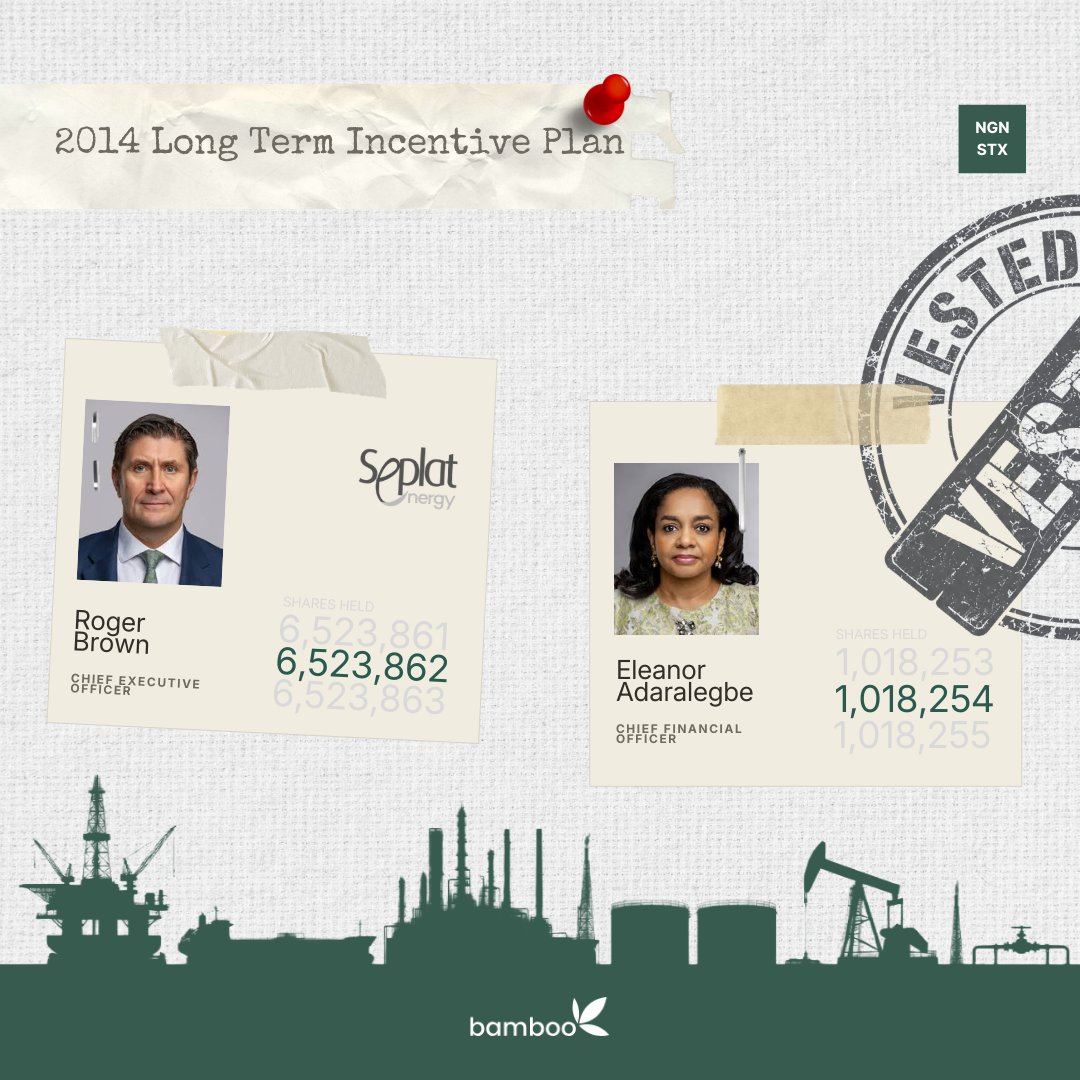

LTIPs are one of the best forms of compensation.

2.19m at share price of GBP5.6 per share is GBP12.3m into the pockets of Mr Roger Brown

May 30

Seplat Energy: CEO Roger Brown vested 2.19m shares and CFO Eleanor Adaralegbe 478k under its Long Term Incentive Plan.

After tax‑related deductions, they now hold 6.52m and 1.02m ordinary shares respectively.

2

2

330

I bought a house first.

It felt foolish but I preferred the sense of stability it gave me and my family.

Building back gradually. Do what works for you.

Jun 9

Big Question for Wealth Builders in Naija:

If you had ₦100 MILLION right now, what would you do?

Option A: Buy a house outright

Own your roof, stop rent stress, and build long-term equity for your family.

Option B: Keep renting and invest the full ₦100M let your money work harder and grow faster.

Drop your choice and reasoning let’s learn from each other

2

7

966

The country has been overrun at this point

Jun 8

BREAKING: Bandits Kidnap 50 Zamfara Elders On Reconciliation Mission

dailytrust.com/breaking-band…

1

154

The real question is where is the source of this video. Who posted it, and is the DSS able to trace, and intercept it?

This woman is speaking under duress and it doesn’t seem like the full weight of our resources have been deployed to apprehend the culprits.

“They are not asking for sharia law or money; they are only asking for the release of some of their men. Government should stop playing politics with our lives" — Abducted vice-principal of Oyo State school, Mrs Alamu Folawe, speaks in new video.

2

1

208

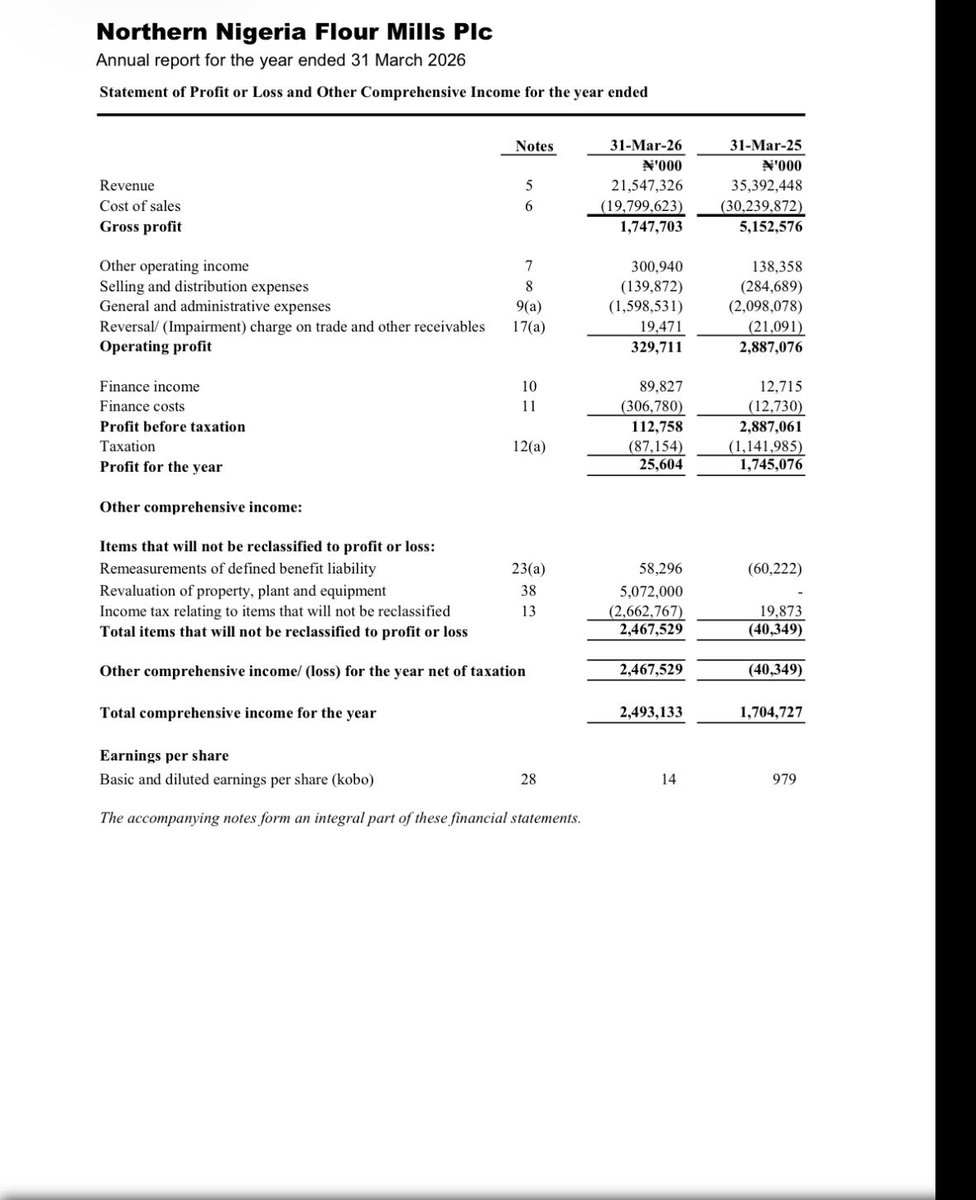

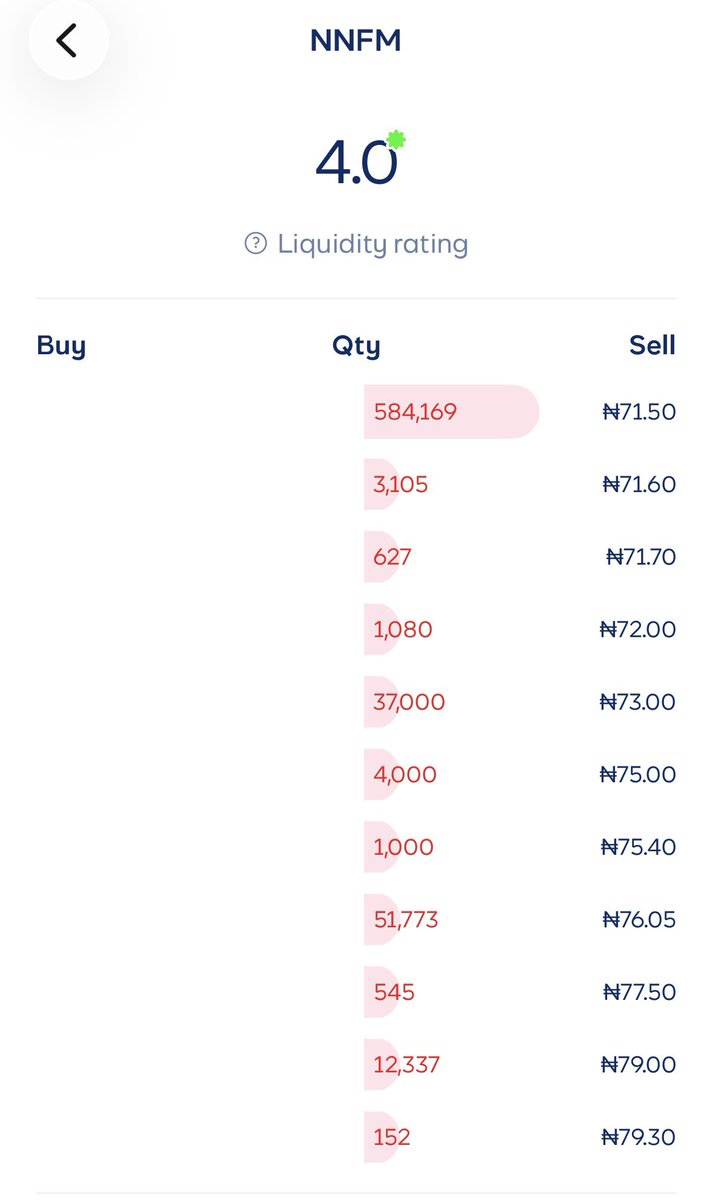

When companies are struggling to make profit and want to smoothen their income, one accounting trick is to revalue property.

NNFM did it recently. Added 5bn income revaluing PPE.

It’s not illegal and it makes perfect sense for them to do it. But it’s not operating income and often one-off.

Just thinking of what that company did in Q1 result to hide how shambolic results were.

Accounting is a crazy concept 😭😭😭

They can generate money from thin air.

4

1

8

1,880

NHS bank shift will give you this if you choose to work Friday, Saturday and Sunday Nights as your overtime

Jun 7

Please, I need someone to walk me through how you can earn £1100 after tax from overtime with a fixed salary of £1800 monthly, what kind of job role has this threshold and how can we arrive at this overtime pay, can anyone help ?

1

1

883

Yaks retweeted

Jun 7

Most people think halal investing is only about avoiding interest.

They're missing a huge part of the picture.

Islamic investing also rejects:

Gharar (excessive uncertainty)

Maysir (gambling and speculation)

If you don't understand:

• What you're investing in

• How profits are generated

• What risks you're taking

...you probably shouldn't be investing in it.

Halal investing is built on a simple principle:

Wealth should come from real economic activity, not from speculation.

That means investing in:

✅ Businesses

✅ Trade

✅ Ownership

✅ Leasing

✅ Profit-sharing ventures

✅ Productive assets

The goal isn't just making money.

The goal is making money through value creation.

Build wealth by participating in the real economy.

2

7

26

577

Yaks retweeted

Jun 7

When you buy a stock, you are not starting a journey from scratch.

You are stepping into a business that already has customers, products and a track record.

That is the power of investing, you can join progress that is already in motion.

7

11

38

2,070

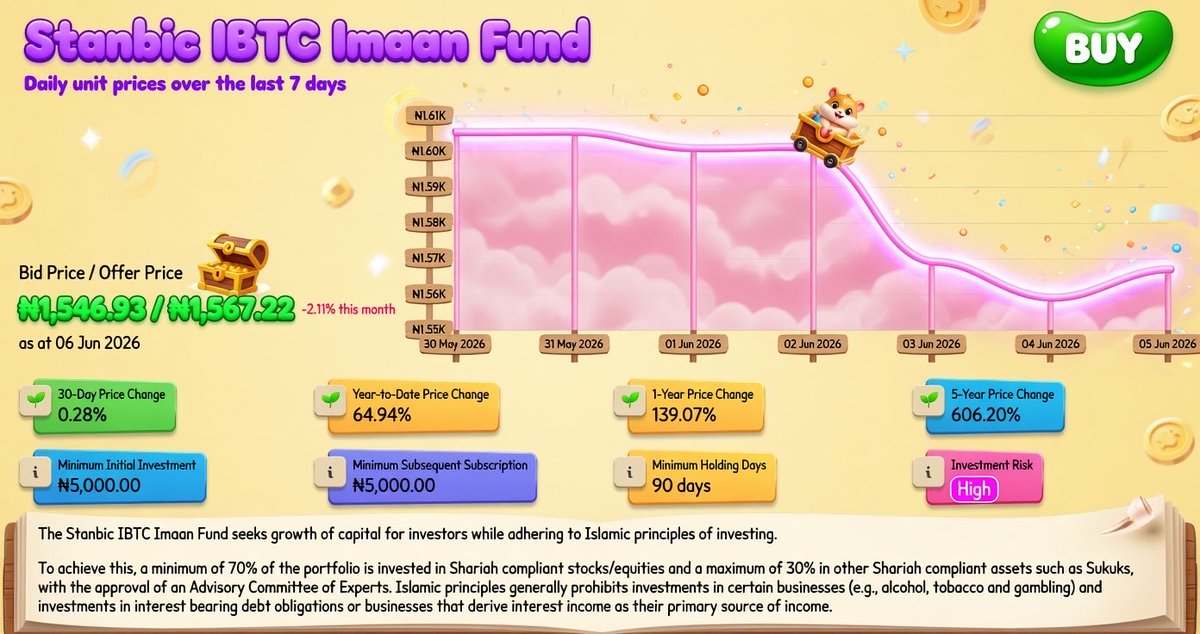

If you don’t know much about investing and you’re focused on Halal investments, mutual funds is one way to go.

Jun 6

Friendly reminder:

You can buy the dip in mutual funds and ETFs too

If the stocks I'm accumulating aren't offering attractive entry points, I check my mutual funds and ETFs.

A red day doesn't automatically scare me.

Sometimes it's a shopping day.

Especially if you're only holding 2–3 individual stocks and relying on mutual funds/ETFs for diversification.

For example, the Stanbic IBTC Imaan Fund is currently down -2.11%.

The market sees red.

I see discounted units 👀

7

568

Biggest red flag!

Money is a key player in marriages and most people realise they are not financially compatible only after marriage.

Do you know your partners spending habits, savings habits, risk tolerance, and financial drive.

Some people marry and discover their partner cant be bothered about accumulating wealth as long as they can eat and pay rent and afford the basics. Whereas they have more drive and want to accumulate more.

It is not enough that your partner has a good job or business, are you both comfortable with your relationships with money?

Jun 6

Quick question if your partner or future partner refuses to talk about money with you, is that a financial red flag 🚩?

4

13

955

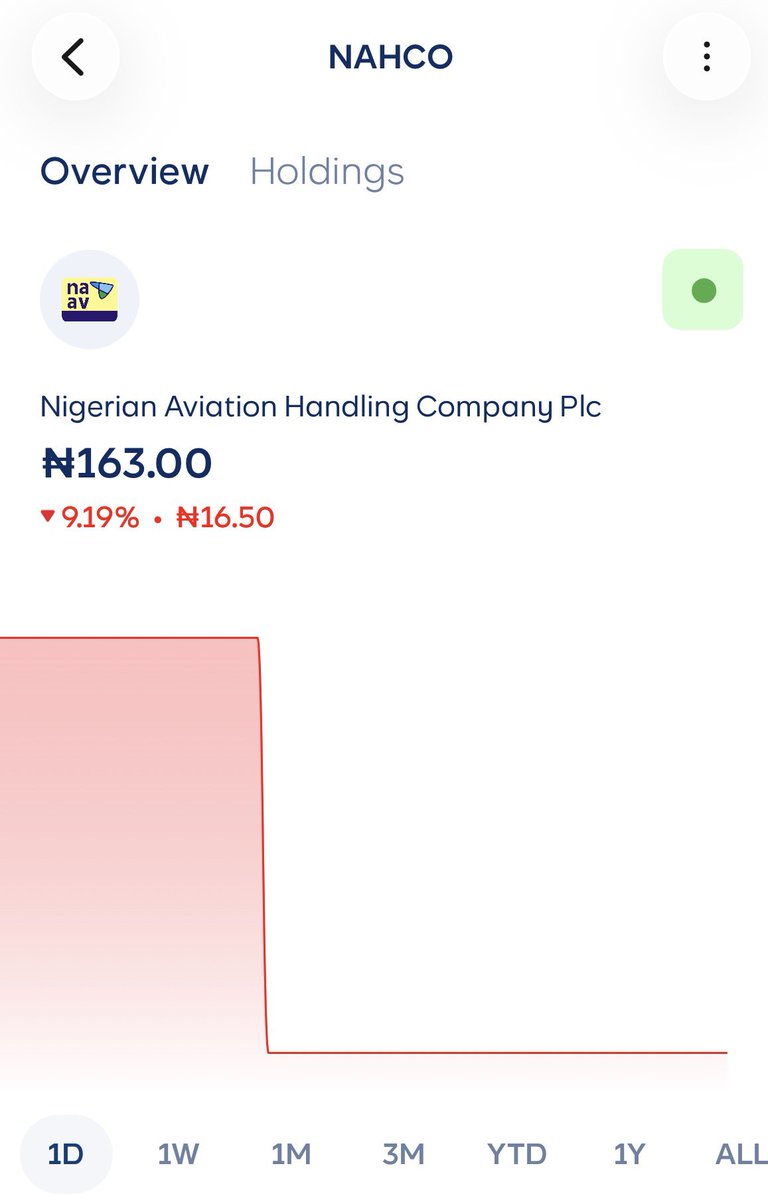

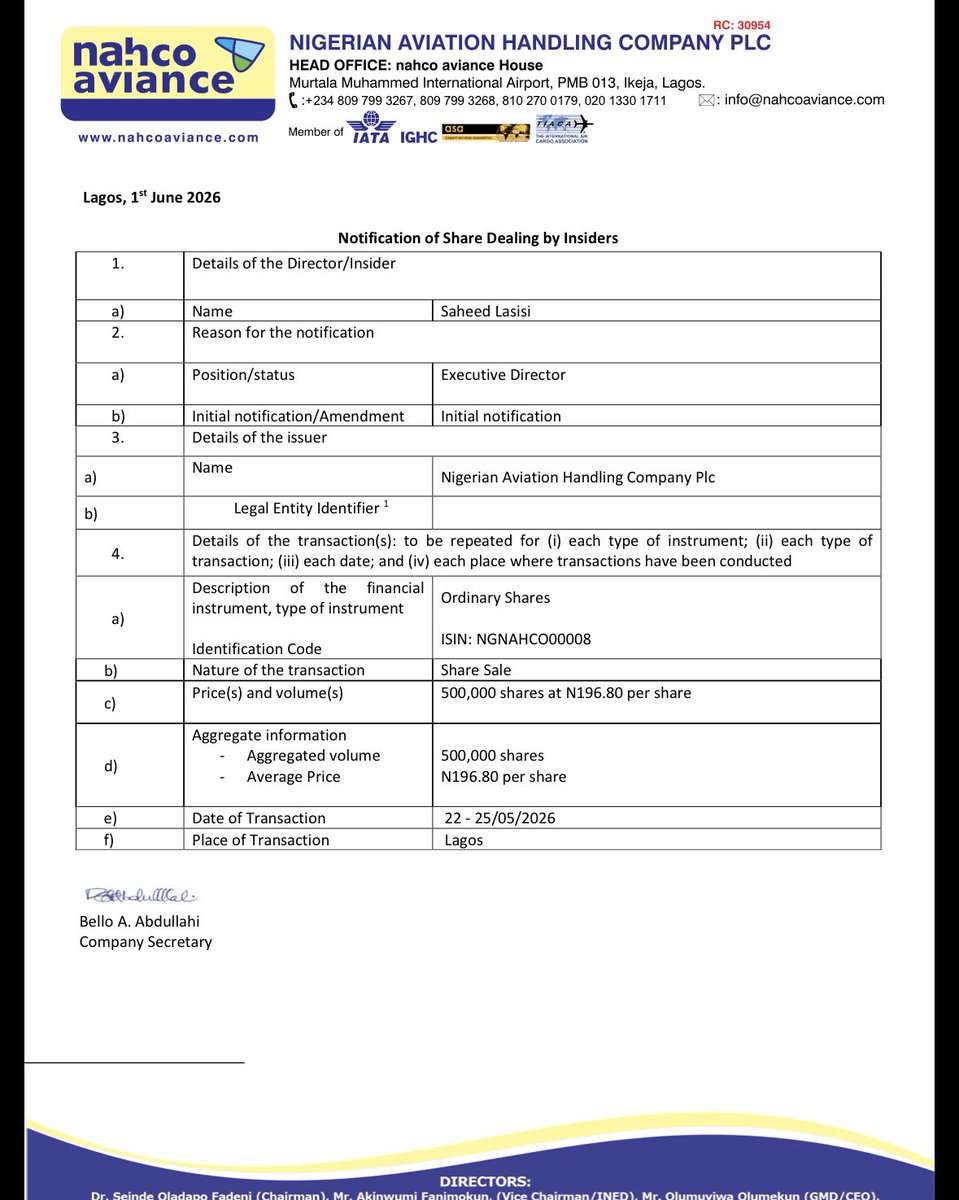

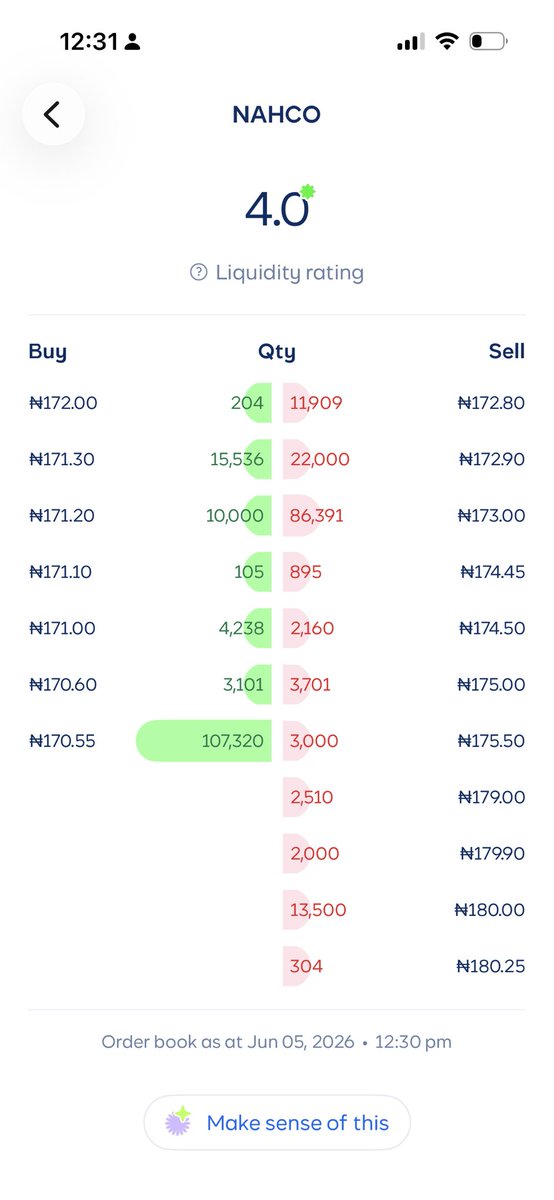

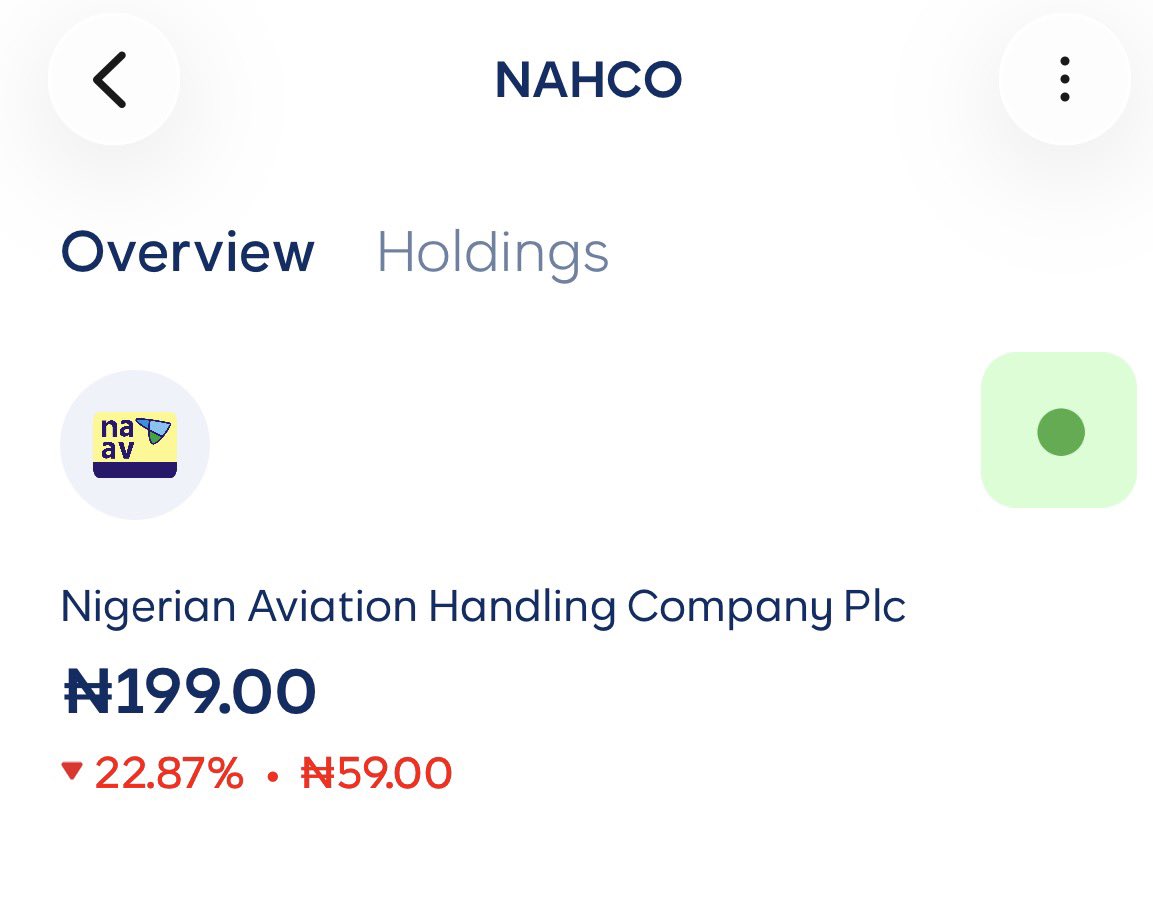

Prince Saheed Lasisi, Group Executive Director , Commercial of NAHCO sold 500,000 shares for N98million.

NAHCO share price has increased by 100% this year and the share price is due for correction. Profit taking is allowed, especially for EDs that do the ground work of running the company.

Does this mean NAHCO is not expecting much upside to their share price this year?

4

2

21

3,096