MD court jester @generalcatalyst | Running the customer value fund (CVF) | Sold cos to @palantirtech, @meta | @stanford | Strong opinions, very strongly held

Joined May 2012

- Tweets 631

- Following 669

- Followers 946

- Likes 2,687

42 Photos and videos

kvm retweeted

Jun 3

Huge congrats to the @factorialapp team on announcing their $150M Series D at a $2.5B valuation!

Ten years after being founded in Barcelona, Factorial has reset from a SaaS company into an AI Workforce Operations Platform, serving 16,000 businesses across 90 countries and becoming one of the most valuable scale-ups in Europe.

Having supported the company since the Seed round, it’s been incredible to watch this journey unfold.

Congrats to @jordiromero ,@bernatfarrero and the entire Factorial team. Onwards! 🚀

7

23

2,197

kvm retweeted

Jun 3

🚀Factorial has raised $150 million in Series D funding at a $2.5 billion valuation, becoming one of the most valuable scale-ups in Europe.

The round will support @FactorialEs's expansion and product development across Europe.

Congrats @jordiromero, @bernatfarrero & team!

tech.eu/2026/06/03/factorial…

3

15

682

kvm retweeted

Jun 3

BREAKING: Spanish @factorialapp has JUST raised a WHOPPING $150m Series D at $2.5bn valuation! 🇪🇸

The round was led by @generalcatalyst (@pranavsinghvi), who have also committed an additional $540m through its Customer Value Fund.

This is AMAZING news for one of the top companies coming out of Spain.

I spoke to Founder and CEO Jordi and discussed:

0:00 - Introduction

0:21 - General Catalyst invests $150m in Factorial

1:10 - Why raise capital now?

2:28 - The relationship with General Catalyst

3:55 - How the Customer Value Fund works

5:24 - From HR software to AI-native workforce operations

9:00 - Leading AI transformation inside a company

11:18 - Why Europe is a great place to build

13:16 - Barcelona’s startup ecosystem

15:52 - Lessons from Silicon Valley

18:21 - Building a company for the long term

19:57 - What Factorial looks for when hiring

Congrats @jordiromero, @bernatfarrero, Pau Ramon Revilla, and the rest of the Factorial team!

2

17

115

26,044

Another great post

May 31

The Silicon Valley I came to in 2016 -- once a low-status refuge for weirdos, naive tinkerers, and missionaries -- has been overrun by input-maxxing Kumon striver types.

Company-building for this class of “entrepreneurs” is an exercise in performative escalations between startups touting their inputs: who can burn the most tokens, who can work the most hours, who can get the most views on an over-produced launch video.

This is why even “ARR,” which should be (and once was) an output of an excellent product and sales engine, has become a noisy, somewhat fake input -- into a machine designed to capture the zeitgeist for 15 minutes, dupe VCs, and maximize fundamentals-agnostic capital flows into a business. Actual company-building is a sideshow for the “cracked” YC-backed founder-striver.

When you talk to many of these people, they have no idea why they’re building what they’re building in the same way that a 16 year old doesn’t really know why he joined 12 clubs or took 15 AP classes -- only that they desperately want to maximize their visible, measurable inputs, tell you about it, and collect their gold star.

It’s easy to place the blame on YC, and they surely deserve plenty of it, but YC’s turn towards performative, low-stakes, incrementalist entrepreneurship is really just another symptom of the broader problems plaguing Silicon Valley: the inevitability of industry maturation and the playbook-ization of startups, demographic change, financial nihilism downstream of bad policy and psychopathic rhetoric coming from some leaders, etc.

The real progress being made amidst all of this is astounding, but the increasingly absurd shenanigans won’t stop until the culture punishes bad behavior and we prosecute, literally, some of the criminals running these companies.

4

1,154

kvm retweeted

May 2

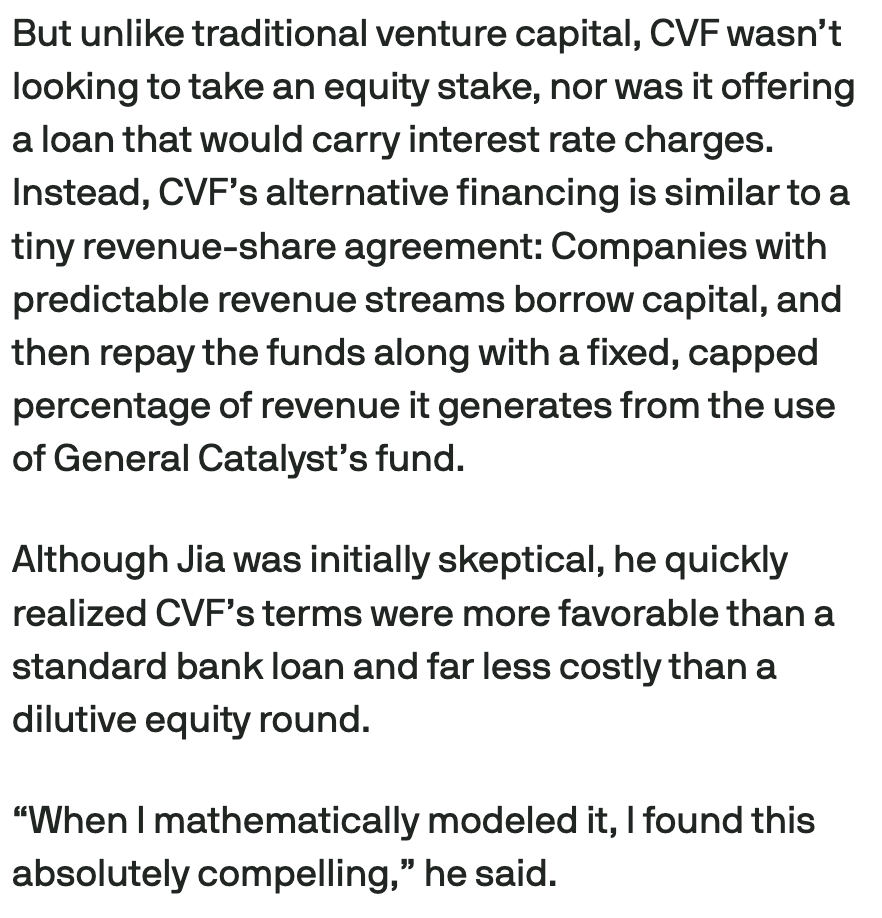

I've said it before, but CVF is one of the most interesting financials products that we offer founders at GC.

May 1

Musely secures $360M from General Catalyst without giving up equity techcrunch.com/2026/05/01/mu…

4

13

80

21,327

kvm retweeted

Apr 13

Thrilled to welcome @nikesharora as @generalcatalyst's first lead independent director. Nikesh brings the rare combination of investor thinking and operator execution and has led some of the most consequential tech orgs in the world. I've long admired the clarity and ambition he brings to everything he does. Nikesh joins me and our chairman @ChenaultKen on the board.

Look forward to our work together building GC and supporting the founders we back.

12

17

252

26,015

kvm retweeted

Venture capital evolved from featuring savvy research analysts like Mary Meeker and Bill Gurley to people who can’t define FCF because technology companies (for better or worse) generally rewarded the latter over the last few decades.

Consider the two big waves where VCs made most of their money in the last 15-20 years: mobile-first consumer social/internet and SaaS.

Mobile/social companies operated in largely permissionless markets that inherently favored young founders, who naturally are not particularly financially sophisticated. SaaS markets, while they generally favored slightly older and more mature founders, similarly didn’t reward financial sophistication; product and GTM chops were far more important.

Both internet and SaaS businesses ran relatively capital-light business models with high gross margins, which gave companies a lot of wiggle room. Financial optimization was just not a key driver of success. And these companies were all built against the backdrop of an enormous bull run and low interest rates post-GFC. Companies could generally raise cheap equity, and most felt like they just didn’t need to think too deeply about how to properly capitalize their businesses.

Silicon Valley became a place where engineering/design/product/sales skills were rewarded and finance was not. “Wall Street” was looked down upon, and people who cared about finance were derided as being slow, bureaucratic, extractive, negative-sum, etc.

These dynamics have obviously changed.

The frontier AI labs are extraordinarily capital-intensive. Some of the hottest applied AI companies have negative gross margins, where optimization on that front over time will make or break their businesses. The asset-heavy aerospace/defense/industrial companies in El Segundo naturally require capital structure sophistication. Technology as a broad industry has matured, and many winning founders are no longer whimsical Stanford types who spent their summers writing code, but Wharton grads who cut their teeth at banks and buyout firms. And, whether companies will admit it or not, the equity capital markets are essentially shut for all but a very small handful of companies, whose success will now depend on their ability to think even slightly outside the box on capitalization.

Finance is now a first-class citizen in Silicon Valley.

Apr 8

We lost financial literacy in VC with the rise of the “Deal Guy”

Deal guy doesn’t concern himself with understanding boring stuff like FCF. He would’ve stayed in banking if that was the case.

His job is simple.

Find the fire. Get close to the heat. Enjoy the warmth and get out before the fire burns you.

10

27

272

57,000

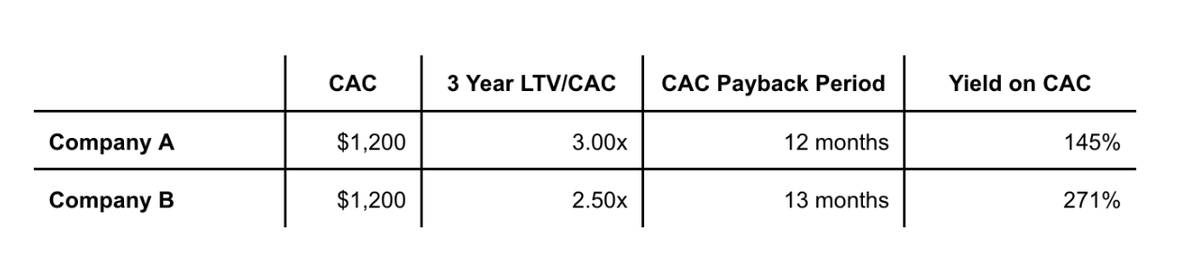

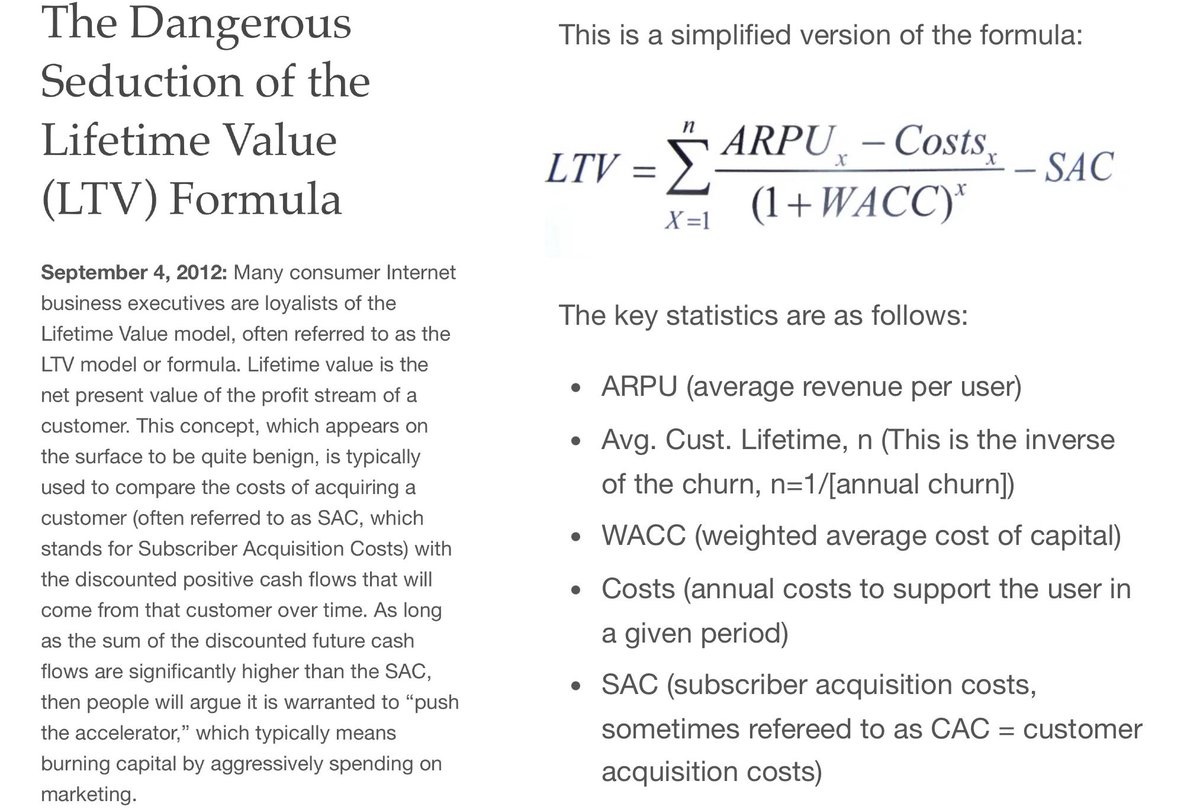

Bill Gurley’s article doesn’t conclude “paid marketing bad”, just “be very careful”.

Big outcomes have clearly come from paid marketing: Monday, Grammarly, Squarespace.

He himself concludes that it “has a very important place in business… that requires.. thoroughness in its implementation”

His 10 points on the pitfalls of CAC/LTV math (all true) boil down to:

- Organic channels are better economics with better user: social, virality and PR

- If you can’t track which customers came from LTV, you over count all new customers which you would’ve acquired anyway. Your equation is just wrong.

- Current LTV math does not hold in the future as you scale. Costs scale as the business scales. You might acquire worse customers who churn quicker. Raising ARPU can cause churn. Companies use dirty tactics to prevent churn (increase LTV) and you can see ensuing complaints in the BBB

- Spending it better on the customer to improve the experience and increase organic growth can be way better for long term business (eg Amazon)

- You have to keep running the treadmill to grow and if your balance sheet can’t hold it, your business slows down and the valuation dips from peak (thankfully instruments like GC’s CVF addresses this and many other points here)

Mar 22

Paid marketing is the crudest game you can play. It’s admitting you have no creativity. And actually restricts your creativity. Fire those that want to spend more. abovethecrowd.com/2012/09/04…

17

42

439

183,585

kvm retweeted

Feb 12

Simile is out of stealth!

At Simile, we have built the first AI simulation of society, populated by agents based on real humans.

We are building a foundation model that predicts human behavior in any situation, and a product that deploys it at scale.

Thrilled to be on this mission.

110

78

1,128

212,033

Bryan Johnson is fighting the ultimate boss. Some people spend 100% of their time or money. He’s spending 100% of his body so the rest of us don’t have to. A noble pursuit, if there ever was one.

Jan 17

A note of appreciation for those of you who stand with me. Who've taken the risk publicly or privately. I know the cost. I respect you for your intellectual sovereignty.

135

kvm retweeted

Jan 13

"You ask what was the supercharge over the last couple of years, well it was @GeneralCatalyst that changed the game for us, and their Customer Value Fund.

We realized the capital markets aren't funding CAC ... and General Catalyst solved that."

(at 51m)

youtube.com/watch?v=DcLy_VJH…

5

21

9,056

Finally, AI designs you can edit.

Moda - create brand assets on a fully editable canvas.

This is not another ChatGPT or nano banana wrapper.

We actually taught an agent layout, typography, and color. We gave it taste.

Use it for slides, social, infographics, e-books …

65

51

546

155,656

kvm retweeted

4 Dec 2025

This is less a commentary on Harvey and more a commentary on the general phenomenon of best-in-class growth companies raising successive rounds at higher and higher valuations: most of these financings make no sense.

Growth equity capital is very expensive. “Dilution is low” is not a good justification for these rounds — dilution is related to but decidedly not the same as cost.

To offer a crude example: if you believe your business is worth $5B, and a firm offers you $10M at a $1B valuation, you will tell that firm to pound sand. That dilution is only 1% is irrelevant; the implied cost of equity is simply far too high.

Maybe these companies believe their investors’ cost of equity is appropriate. Even still: the money is still expensive relative to the other forms of capital available, meaning it ought to be used for the most ambitious endeavors that present unstructured risks with unbounded upside (read: high-value product R&D and strategic M&A). Instead, companies at this scale typically deploy a substantial majority of their expensive equity dollars into highly predictable, relatively low risk GTM initiatives that offer range-bounded returns (or even worse, do nothing with these dollars, letting them collect dust in treasuries).

This is terrible capital allocation. In the worst cases, it’s directly value-destructive, yielding lower returns than the cost of capital. At best, it’s deeply inefficient: these activities consume capital that would be best deployed elsewhere.

Sometimes, these rounds involve secondary transactions between shareholders and no primary capital (so no dilution). This doesn’t solve the core issue. Shifting around who owns the most expensive form of capital doesn’t change the fact that this capital is being used inappropriately — and that these companies should finance their GTM investments differently.

Moreover, this conversation totally misses the point. The persistent liquidity and DPI issues that Silicon Valley faces aren’t only downstream of an an onerous regulatory/compliance regime or the broken supply/demand mismatch in private markets — they are downstream of busted balance sheets across the entire industry. If companies appropriately capitalized themselves with the right balance sheets, they could actively buy back stock in these transactions rather than simply shifting ownership between parties, offering liquidity with “negative dilution” and allowing shareholders to capture a greater share of value moving forward.

4 Dec 2025

Private markets are the new public markets.

It's notable that in many of these rounds, companies are only selling 2-3%, and it's likely secondary.

These rounds aren't really fundraising," they are valuation signaling and liquidity. Deep pools of private capital are desperate for allocation in top-tier assets, and founders are happy to oblige... we made it too difficult to be a public company with regulatory headaches and founders saw the opportunity to avoid the volatility of public markets, so here we are, and now retail misses out on the runups of these companies.

13

14

219

77,194

kvm retweeted

19 Nov 2025

.@generalcatalyst's Customer Value Fund, explained by Managing Director @pranavsinghvi:

"What the customer value fund does is it goes to companies and says instead of using your own cash to fund sales and marketing, we will provide you a dedicated balance sheet to fund your ongoing sales and marketing spend."

Full episode: thein.fo/4nYS3sN

3

6

3,345

kvm retweeted

19 Nov 2025

.@generalcatalyst's @__kvm on growth:

"We help putting fuel to the fire. We cannot create the fire ourselves. The best people to create that fire, to figure out how to grow are the founders."

"Most companies are massively under spending. What I mean by that is they need to run more experiments."

Full episode: thein.fo/48o0s4v

2

2

7

3,493

kvm retweeted

19 Nov 2025

Today on The Information’s TITV:

-The VC view of the creator economy | @Caspar_Lee, Co-Founder & Partner at Creator Ventures

-@generalcatalyst Managing Directors @pranavsinghvi & @__kvm discuss its CVF fund

-Finding margin with AI products | Shaown Nandi, @awscloud Director of Technology

-Introducing The Information Finance Newsletter with

@kenbrown12

19 Nov 2025

The Information | TITV | November 19, 2025 x.com/i/broadcasts/1mrGmBmWy…

1

4

2,801