founder @3janexyz. leverage is a God-given right

Joined January 2021

- Tweets 1,375

- Following 793

- Followers 4,809

- Likes 7,388

123 Photos and videos

Pinned Tweet

4 Sep 2024

The financial system will eventually converge on a hyperfinancial singularity — one in which anything that can be financialized will be, driven by zero overhead coordination costs enabled by universal on-demand programmable cryptoeconomic trust.

11

4

70

15,802

3Jane has executed an ~$8.5m whole-loan purchase with Slope, the credit infrastructure powering business lending for @slashapp & the Fortune 10

Phase 0 of a broader $50m forward-flow program

USD3 now directly funds SMB lines of credit embedded in major U.S. commerce platforms

2

10

87

10,025

We are excited to announce that we have completed our 1st forward-flow loan sale of $8.5M with @3janexyz, a cryptonative credit protocol. This is the 1st phase of a broader $50M program and one of the 1st whole-loan purchases of a U.S. fintech loan book by a DeFi protocol.

5

12

62

9,888

Jun 9

We are excited to partner with Slope as an anchor originator to scale their loan volume across their SMB line of credit & net terms products that power lending offerings for neobanks like Slash and several major U.S. e-commerce platforms in the Fortune 10.

We've purchased ~$8.5m from an initial backbook sale, which will transition into a $50,000,000 forward flow facility.

To my knowledge, this is one of the if not the first instances of a forward flow agreement between a crypto protocol & fintech lender. In this agreement, 3Jane commits to purchasing loans on a defined cadence, allowing the seller (Slope) to move loans off their balance sheet and achieve the capital-light economics that every fintech strives for (Affirm, SoFi, etc).

A few thoughts

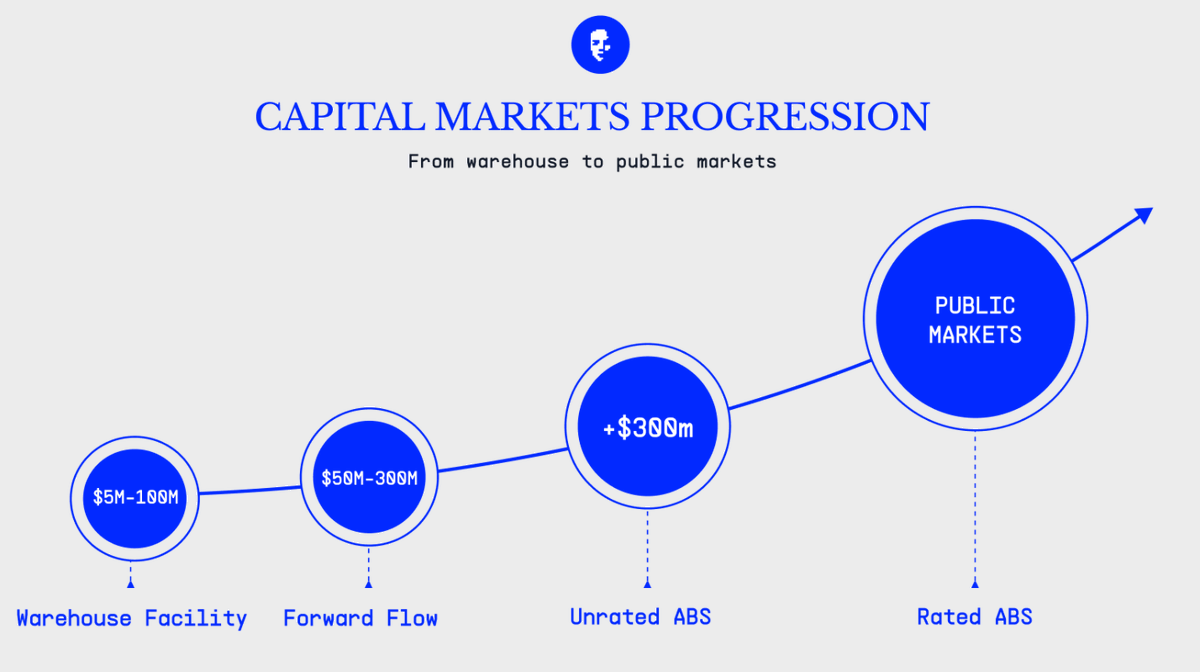

(a) I still believe that 90% of primitives and financial structures have not yet been discovered, disrupted, or reinvented by DeFi. DEX's/money markets in their current form only scratch the surface of the broader financial universe. It is bewildering to me that it took 6 years since DeFi summer for the terms "warehouse facility" & "forward-flows" to enter the mainstream vocabulary.

(b) I still believe that DeFi is in its experimentation phase for anyone who still wants to experiment. DeFi is not yet mature, contrary to popular opinion. A fish doesn't know its in water. Similarly, DeFi doesn't know that synthetic CDO's & ABCP conduits exist.

(b) 3Jane's vision has always been to finance the productive economy. We began as direct originators for yield farmers who operate on the furthest end of the productivity curve. This is largely an aggressive doubling down on that same vision through structured credit. We believe that crypto rails can deliver effective securitization economics by converting sophisticated structured financing into code, making native asset issuance distributable on a global scale, and amortizing those costs and liquidity premiums back down to the fintech lender.

We are still incredibly early.

3Jane has executed an ~$8.5m whole-loan purchase with Slope, the credit infrastructure powering business lending for @slashapp & the Fortune 10

Phase 0 of a broader $50m forward-flow program

USD3 now directly funds SMB lines of credit embedded in major U.S. commerce platforms

2

1

30

3,570

Jun 1

3Jane has executed the first of several credit facilities to scale U.S. fintech lenders, starting with a $10M warehouse line giving LendSwift a cryptonative balance sheet to grow its consumer installment loan product that thousands of Americans already use.

LendSwift keeps doing what it does best: customer acquistion, underwriting, origination, & servicing. 3Jane provides structured debt financing behind it, collapsing the multi-year bank warehouse -> forward-flow -> asset-backed securitization gauntlet into a single pooled, revolving conduit.

Suppliers mint USD3/sUSD3 on Ethereum, capital is lent to LendSwift to fund end-borrowers, newly originated consumer receivables are pledged into a bankruptcy-remote SPV to collateralize the facility with the originator retaining first-loss equity, loans are repaid through borrower cash flows swept into a DACA-controlled account, & yield is distributed back via report().

Cryptonatives now have access to the full raw economics of high-yield structured credit that historically accrued to funds and banks. No intermediary credit fund, no synthetic exposure, no tokenized claim on someone else's assets.

Native asset issuance will become the gold standard for funding fintech lenders within 3 years.

The entire structure is visible on 3Jane's backing page: app.3jane.xyz/info/pulls/fcc

3Jane has executed a $10M senior warehouse facility with LendSwift, a U.S. fintech consumer lender, to scale its loan portfolio

Funded by USD3/sUSD3 at a 15% coupon and secured by ~15,000 short-duration installment loans

Cryptonative capital now funds mainstream consumer credit

4

2

24

4,627

May 27

Crypto could really use a synthetic CDO on a megapool of 9,431 RBF loans to AI agent businesses run on @polsia, with maybe endogenous collateral & a cheeky CDP stable integration right now.

1

4

701

May 21

Native asset issuance has been postponed by 2 years until further notice.

12

1,215

May 18

Structured credit changed your life more than Michael Jordan, the iPod, & Youtube put together by shaving 200bps off your mortgage.

ABS, CDOs, synthetics are complex forms of financial engineering, and we believe they are the most fertile breeding ground for the next era of DeFi innovation.

Learn about the risks below.

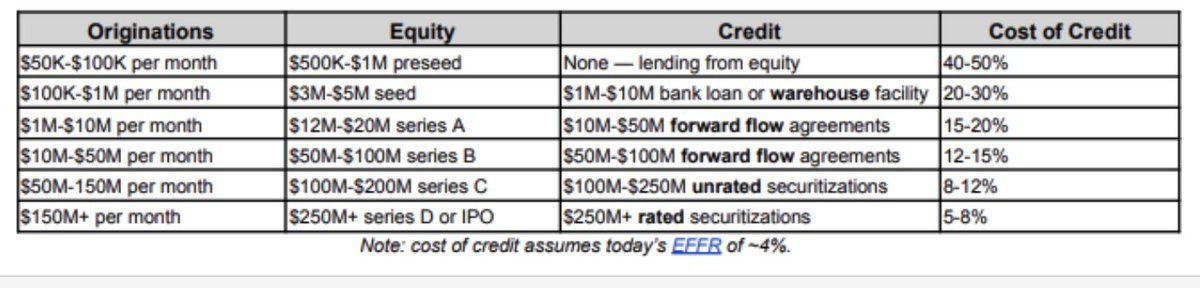

Structured financing for fintech lenders (ABF) is a $100B asset class with virtually no history of being exported into crypto markets, despite consistently generating 10% returns.

Releasing a deeper analysis ahead of public launch:

➝ ELI5 warehouse loans & forward-flows

➝ Where the yield comes from

➝ Structured credit risk profile & loss distribution

Full post below.

1

33

5,403

May 15

The quality of The Economist’s analysis - the supposed last bastion of ruthless empiricism - has dropped off a cliff over the past year. A once-sharp knife, devastatingly blunted . End of an era, @TheEconomist.

5

288

May 13

Barring civilizational collapse, at the current rate of financial innovation, many of the financial primitives that dominate 100 years from now probably have not been invented yet or will not exist in their current form-factor.

1

5

336

May 13

Index funds, ETFs, interest rate/credit default/currency swaps, structured securitizations, junk bonds, Bitcoin, and Ethereum were all invented in the past 50 years, more than 3,000 years after Hammurabi’s Code.

1

1

2

229

May 7

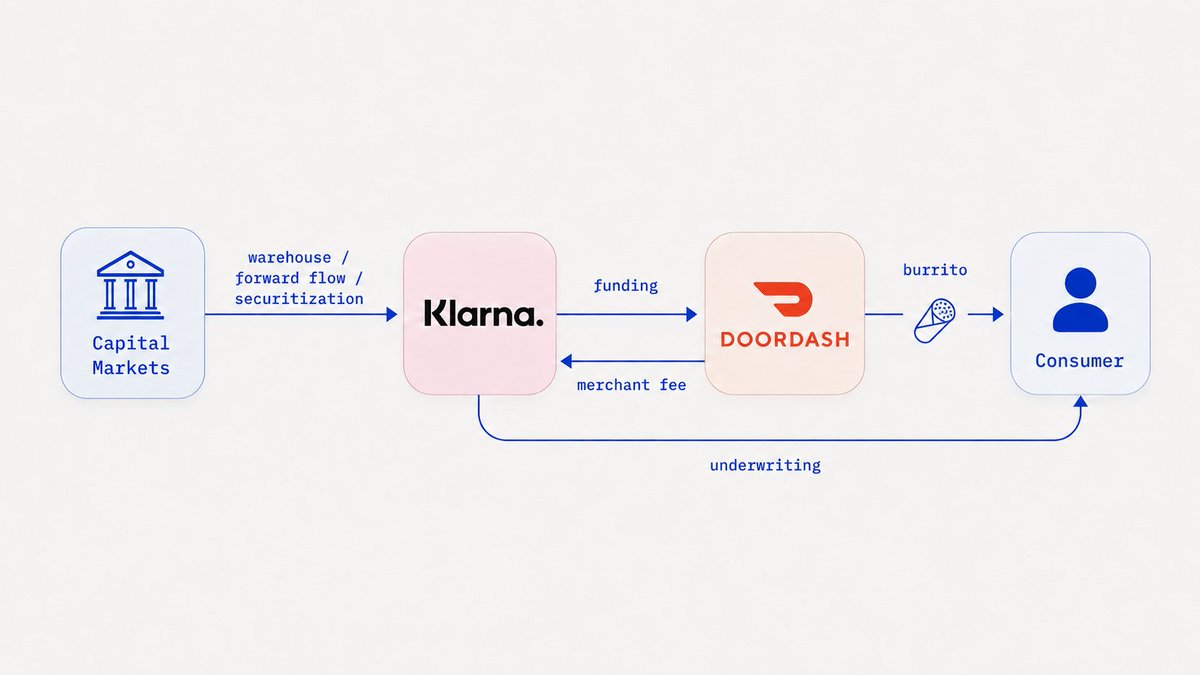

15/ This allows Klarna to significantly bring down their cost of capital as well as scale their portfolio orders of magnitude to $B's. In reality, this only works when you've bundled >$100m's of loans together, not $10.

1

2

409

May 7

16/ As the lender scales they converge on the originate-to-distribute (OTD) model. It moves a lender from balance-sheet-heavy growth to capital-light platform economics that produces high margins and in turn high valuation multiples.

1

3

420

May 7

17/ Your burrito bowl is financed by insurance and pension funds in the end.

2

7

681

May 7

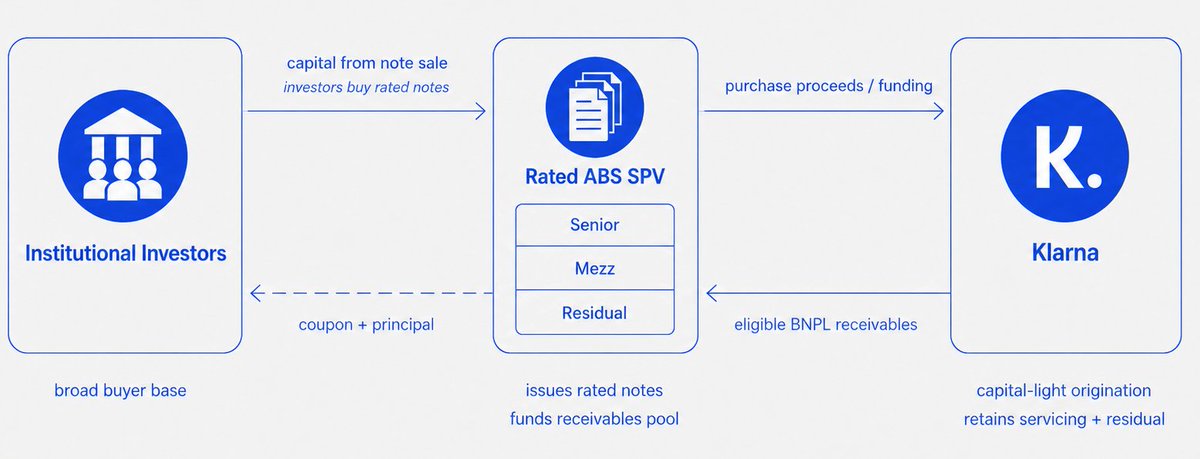

14/ Klarna invests time into having lawyers structure a tranched asset-backed securitization of burrito receivables, pay a rating agency to rate the tranches, and have bank sponsors pitch and sell the senior to insurance and pension funds at 5% coupon.

1

3

289

May 7

12/ The credit fund might offer to buy $10 worth of future burrito purchases for $9.85. Private credit fund gets their double-digit IRR and Klarna scales their loan book without tying up equity, keeps an origination/servicing fee, and recycles capital. Extremely capital-efficient

1

3

246

May 7

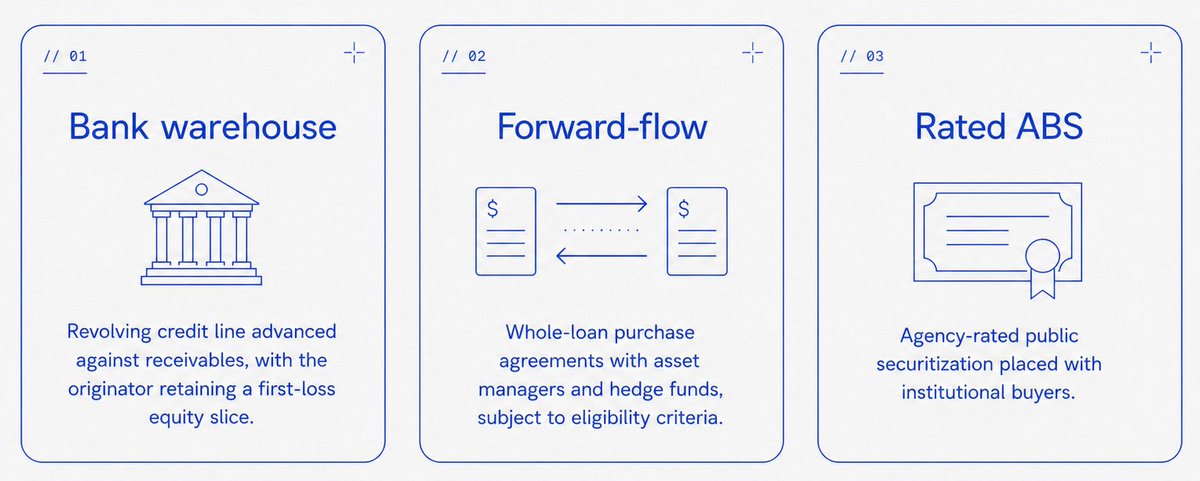

13/ Asset-backed securitization (ABS) // 3

Klarna is now several years in business, proved out their loan tape, scaled to $15 purchases and wants to engineer an even lower cost of capital for themselves to keep a larger spread.

2

4

256

May 7

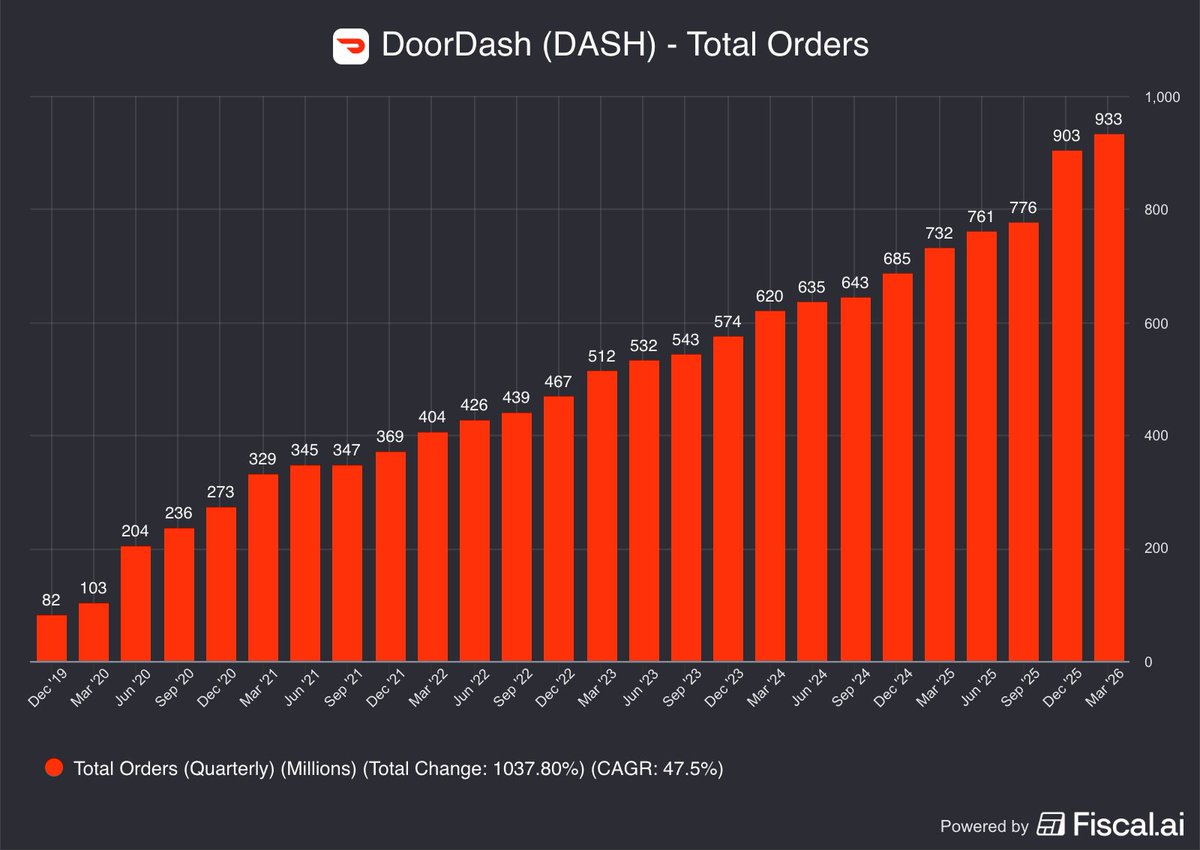

1/ DoorDash just reported 933M orders and $31.6B GOV in Q1.

In 2025 they added Klarna BNPL at checkout to drive growth. Most consumers still don't know who fronts the cash.

The capital markets rabbithole on how your burrito gets financed at 0% APR

1

2

27

8,150

May 7

11/ Forward-Flow // 2

Klarna has purchased $4 of loans, proved their performance, & wants to scale to $10 of burrito purchases without raising equity to fund the warehouse first-loss slice. Klarna gets approached by a credit fund for a forward flow whole-loan purchase.

1

4

236

May 7

10/ When Klarna started out in 2005, this was likely the only option they had given that it is the safest for the lenders/investors. Today, they still use this as a low-lift funding strategy to accumulate loans before reselling them in the broader ABS market (later).

1

6

267

May 7

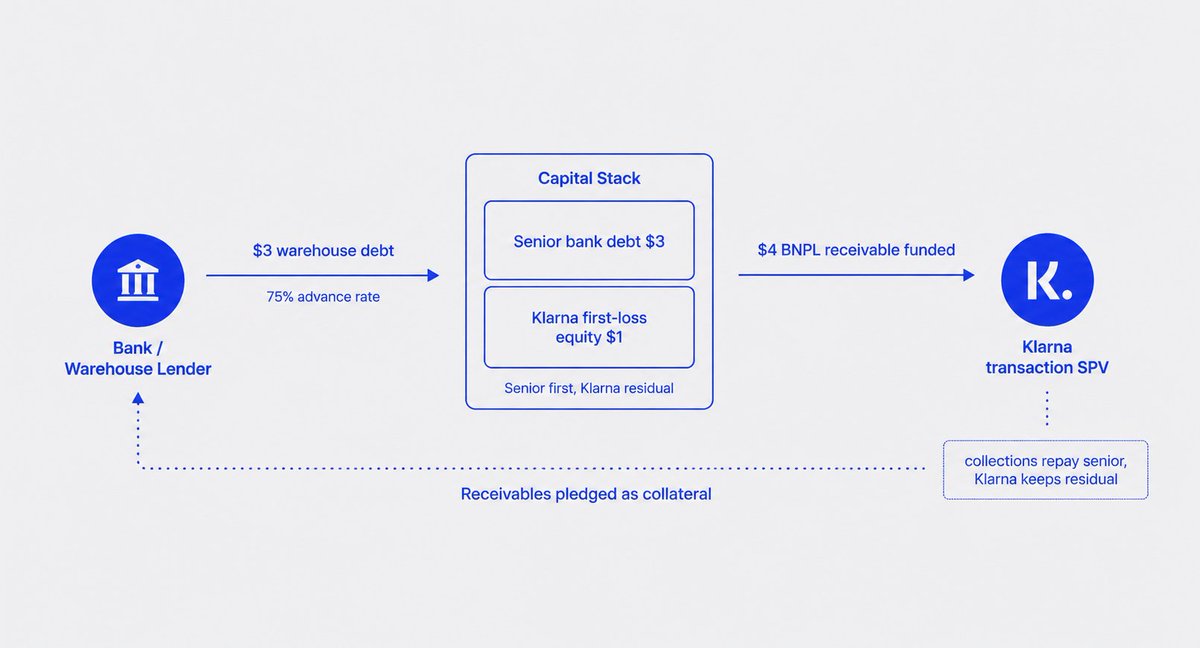

9/ Instead, Klarna approaches the bank and borrows $3 with interest, funds the $4 burrito order, & pledges the receivables as collateral with the bank at a 75% advance rate, keeping a first loss slice. Bank gets their yield and Klarna scales their loan book w/o giving up equity.

1

5

225