PR / Marketing at @Yellow @YellowMedia_HQ

Joined September 2024

- Tweets 164

- Following 160

- Followers 263

- Likes 525

26 Photos and videos

Yellow Media Weekly Crypto Wrap is already here - check it out 👇

From AI infrastructure to IPO dreams…

Governments backing compute,

AI agents trading on-chain,

OpenAI chasing an $85B valuation,

SpaceX eyeing history,

and fresh SBF pardon rumors.

Catch the full wrap via @alinaxyellow 👇🏻

10

Jun 12

AI agents trading crypto 24/7 is the obvious next step.

But centralized execution means agents still depend on custodial rails, human-style accounts, and no native settlement between them.

Jun 12

AI Agents & Tokenization in Crypto Banking

I think AI agents could reshape banking much faster than most ppl expect.

- AI agent traffic grew 7,851% in 2025.

- Financial services agent traffic was still only ~1% of total agent traffic in May 2026, but it grew 124% MoM.

- Only 2.4% of agent activity is touching checkout and payment flows today.

So agentic commerce is still tiny at the payment layer, but the infra is being built before the volume arrives.

- Visa launched Intelligent Commerce.

- Mastercard launched Agent Pay and already processed authenticated agent transactions.

- Stripe launched wallets for agents, has 250M users inside Link, and is plugging agentic checkout into a massive merchant network.

- Circle launched Agent Stack so agents can hold USDC.

- Coinbase turned x402 into a native internet payment protocol.

Banks are building their own machine-readable money through tokenized deposits.

- JPMorgan's JPMD gives institutional clients a bank-issued deposit token with near-instant issuance.

- Citi Token Services lets corporations move liquidity between participating Citi branches 24/7 using existing accounts.

- BMO plans tokenized cash and deposit products in H2 2026.

- JPMorgan, Citi, BofA, and other banks are working toward a shared tokenized deposit network for 2027.

Crypto and TradFi will probably work together, so I don't think one side wins outright.

Imagine an AI treasury agent keeping operating liquidity in tokenized bank deposits, converting some into stablecoins for cross-border payments, and parking idle cash in tokenized Treasuries.

But DeFi might get a much bigger demand source.

An AI agent receiving stablecoins has no reason to leave balances idle if it can automatically sweep excess funds into a tokenized money market fund.

The result is that agentic capital could increase DeFi TVL while reducing free yield.

→ Protocols will need to generate real borrower demand, trading fees, credit spreads, or offchain income instead of paying token incentives forever.

Whoever is building stablecoin rails, tokenized T-bills, low-risk lending markets, and automated yield routers will capture more value.

Crypto neobanks might not look like they do today either.

They're built to give humans a better interface to banking, but what happens when the main customer using the account is an agent?

A neobank that remains just a nice app plus a debit card will fade.

→ The valuable neobank becomes a wallet, policy engine, and financial operating system for both humans and their agents.

Projects building for that future 👇

1

4

103

The next wave of transactions won't have a human on either side.

Our @DiegoMYellow breaks down the agentic economy, state channels, and what trustless commerce actually looks like - in conversation with @Anewz_tv.

youtube.com/watch?v=58YtoQyR…

26

41

293

55,171

Jun 6

Your weekly crypto recap is here👇

Jun 6

From soaring tokens to soaring rockets…

HYPE hits new highs,

banks move closer to crypto,

gold loses its shine,

AI attracts another billion,

and SpaceX eyes a record-breaking IPO.

Catch the full wrap via @alinaxyellow👇🏻

3

61

May 21

So good to see Asia-Pacific setting the pace, and Yellow Media heading to @UnchainedSummit in Vietnam to cover it from the inside!

May 20

We’re excited to announce our official media partnership with @UnchainedSummit 🇻🇳

From founder conversations to ecosystem trends, we’ll be bringing you stories and insights from the forefront of Web3 innovation.

See you in Vietnam on May 28–29.

8

94

Alina Malysheva retweeted

May 18

I’ve been spending a lot of time in my @Tesla lately, and it’s shifted my perspective on financial technology.

When I press the button and let the car take over, my cognitive overhead drops by 99%.

I can think about my life and talk to my friends instead of stressing over traffic.

We are building that same level of automation for the global markets.

Bitcoin is the perfect example because it’s a system that is entirely automated, validates itself, and just works.

As we build more of this infrastructure, the efficiency makes everything cheaper.

We are moving toward a world where machines handle the driving of our financial systems, leading to a level of abundance that was previously impossible.

6

1

22

863

May 18

Interesting that the security conversation is still framed around human oversight capacity

The actual question is whether the underlying rails can enforce rules without humans in the loop at all

And @Yellow is building exactly that - programmable escrow where conditions either pass cryptographically or they don't

coindesk.com/tech/2026/05/18…

2

6

65

May 15

Love seeing the Ukrainian Web3 scene keep growing like this 🇺🇦

One month till the Incrypted Conference, and I'll be there

May 14

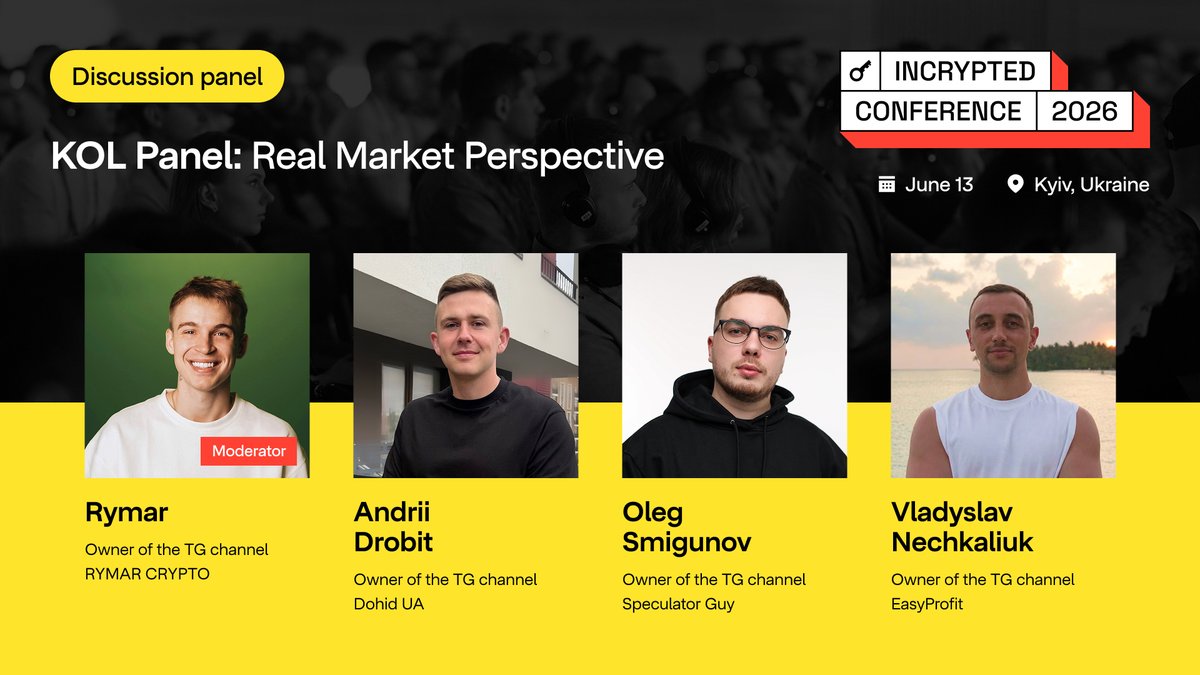

just one month until Incrypted Conference 2026 and the market takes are getting more interesting 👀

at the “KOL Panel: Real Market Perspective”, some of the biggest voices in the ukrainian crypto community will break down narratives, trends, and where this cycle could go next:

• @AndriiDrobit - DokhidUA (39.9k)

• Vladyslav Nechkaliuk - @VladNechkaliuk (26.3k)

• Nazar Rymar - RYMAR CRYPTO (20.1k)

• Oleh Smihunov - @oleg_smg (6.9k)

June 13

Parkovy Convention Center, Kyiv

Tickets - incrypted.click/s97

1

6

121

May 14

Any guesses? 👀

May 14

The team has been unusually quiet this week. Usually, that means something massive is about to drop. 🤫

If you actively trade and manage your own portfolio, let’s just say... we are preparing a very specific reason for you to stick around. Something about recognizing real volume and giving back.

Get your wallets ready.

Prepare your best setups.

Big news is coming in a few days. 👀

5

116

May 14

So many cool things going on at @Yellow all at the same time

One of them is @Nadmah_co joining our builders alliance and @DeFi_Pop’s talk with @MSkylion

Discover how @venturevaultvc is approaching Web3 startup support in 2026, what they look for in founders, and why joining the Yellow Builders Alliance made sense for their vision. Watch back as Yellow CMO @DeFi_Pop heard the details from @MSkylion

1

11

224

May 14

Companies cutting staff "because of AI" is a clear signal.

AI brings value and yes, it can replace roles. The question is whether you're using it to become 10x more valuable, or waiting to find out.

Make friends with the tools before they make you redundant.

May 14

Crypto data firm Dune cuts 25% of staff citing AI efficiencies theblock.co/post/401322/cryp…

1

6

98

Alina Malysheva retweeted

May 13

Narratives bring attention, but products that actually solve problems are what make people stay.

Attention creates the spark, product drives retention and community drives real growth.

In the long run, the brands that win are not the ones sustaining hype, but the ones relentlessly improving usability and product quality long after the attention arrives.

13

7

49

958

May 13

Joining the trend

Try and share yours 💛

May 12

A new trend from chatgpt prompt

Share what you came up with

my pfp my pfp as a lego

2

12

188

May 13

With @est3r_eth back at our Marbella content retreat from a few weeks ago

Hope you enjoy the videos on @Yellow (there’re definitely more to come) 💛

2

14

629

May 13

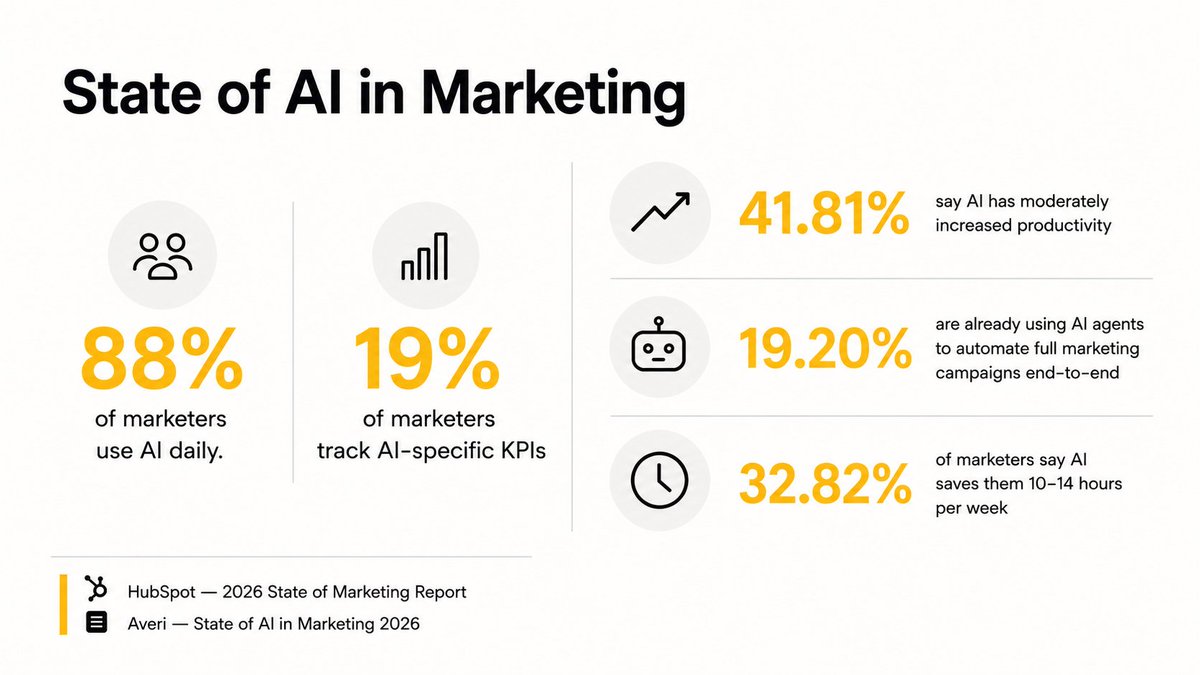

Nearly all marketers use AI. 88% use it daily.

Only 19% track whether it actually drives results.

And that's AI-flavored busywork.

Meanwhile, the teams getting it right:

- Save 10-14 hrs/week

- 1 in 5 already run autonomous campaigns end-to-end

- 41% report measurable productivity gains

AI won't replace marketers. But marketers who adapt and use AI in the right way will replace those who don't. Agree?

1

10

99

May 11

Thank you @zhannamanzyk and @JayaTalent team💛

Thank you Alina for your trust and kind words 🙏

Alina`s X @alinaxyellow & LinkedIn [linkedin.com/in/alina-malysh…]

Her first feedback: t.me/jayatalent/111

Retention is the best agency metric and this is exactly what Jaya Talent is proud of.

The right people, the right companies, still going strong 2 years later.

For more opportunities → follow @jayatalen

5

164

May 11

There are thousands of Web3 conferences and events happening around the world every single month.

And yet, most marketing teams still track them manually. Spreadsheets. Bookmarks. Messages saying "hey, did you see this one?"

That's not a workflow. That's chaos.

4

9

95

May 11

But it doesn't just collect info - it thinks.

Based on each event's audience and topics, it recommends who from your team should attend or speak.

At @Yellow: no more guessing. The right person, the right event every time.

2

2

54

May 11

Want to see how it works?

Drop a comment, and I'll share the guide & prompt behind it 👇

2

60