108 Photos and videos

LP 🐡 retweeted

Apr 24

Everyone else on Ethereum: "We are going to contribute ETH to help save Aave and DeFi"

Ethereum Foundation: 10,000 ETH sell

Apr 24

0/ Today, the Ethereum Foundation finalized the terms of a 10,000 ETH sale at an average price of $2,387 via OTC.

For this sale, our OTC counterparts was @BitMNR.

51

64

974

86,104

LP 🐡 retweeted

Apr 15

Back in the Grass 🌾 | Episode 28 | Million Dollar Pokemon Deals x.com/i/broadcasts/1dKrPEwbY…

38

80

139

6,352

LP 🐡 retweeted

Apr 15

Cypherpunk Jameson Lopp and other Bitcoin developers propose BIP-361 to freeze quantum vulnerable wallets.

This could lock dormant BTC like Satoshi Nakamoto’s 1.1M coins, now worth $74B, before quantum computers can steal them.

892

366

3,257

1,178,837

LP 🐡 retweeted

Apr 13

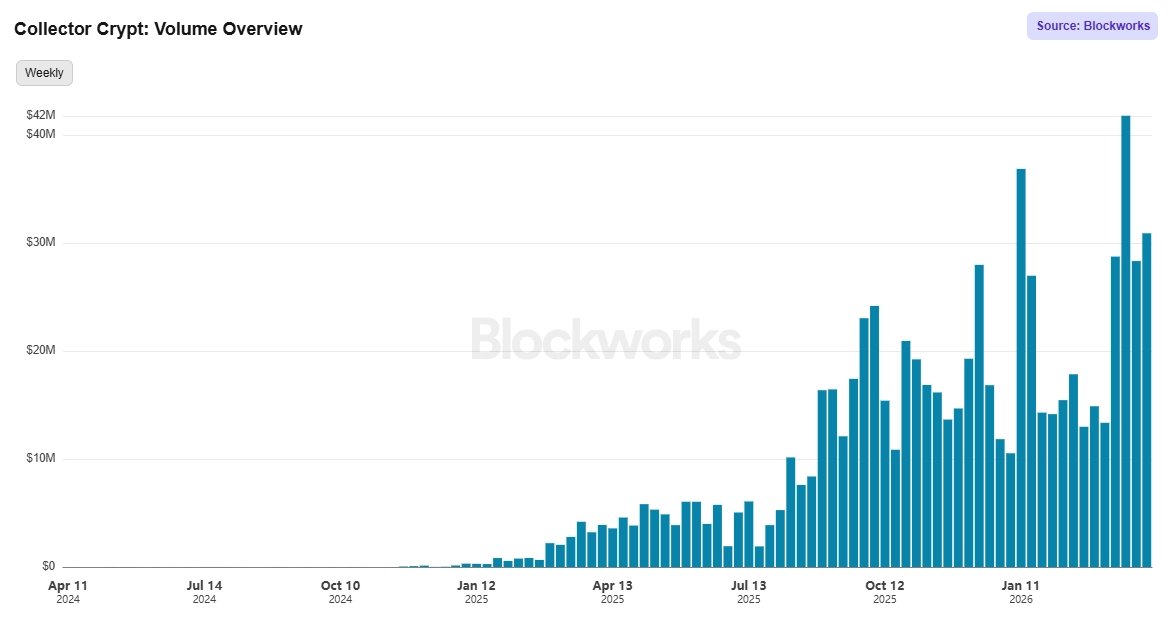

bullish on $CARDS

tldr: more profits than its marketcap buybacks coming

- Token has been going down/sideways while fundamentals have been improving

- 9M gross profit in Q1 (37M/yr)

- 146M gross revenue in Q1 (584M/yr)

- $14M (or $17M reported by others) treasury; collectible inventory USDC, backed by the token

- The marketcap is $13M

- Token buybacks are coming “pretty soon”.

- Chunk of profits will go to buybacks, along with percentage of each pack sale (including partner platforms via their API) will route directly into systematic buybacks (averaging $84M monthly volume past 6 months)

- Team is actively trying to buy back VC allocations (reducing sell pressure). Which are fully unlocked in a few months anyway.

- Team has already quietly bought back $1.5M worth of tokens. Creating a floor around 3c.

- FDV is effectively much lower; can remove 37% foundation 16% community (will take 10yrs to disperse) % they’ve bought back already. And this number goes up with upcoming buybacks

- Team is great, transparent, they keep shipping and innovating.

- They are opening up their own vaulting facility; vertical integration with same day shipping, no international repackaging, no reliance on 3rd party logistics. Better UX and will allow for product expansion like sealed gacha.

- Goal is building the infrastruture layer for the entire collectibles market.

- Pricing API, collateralized lending, expansion to other TCGs coming up. More in the pipeline the team doesn’t want to share as competition will copy.

- 0 ad spend so far, fully focused on hyper growth

What do you think happens when official/systemic buybacks get announced?

9

8

70

22,605

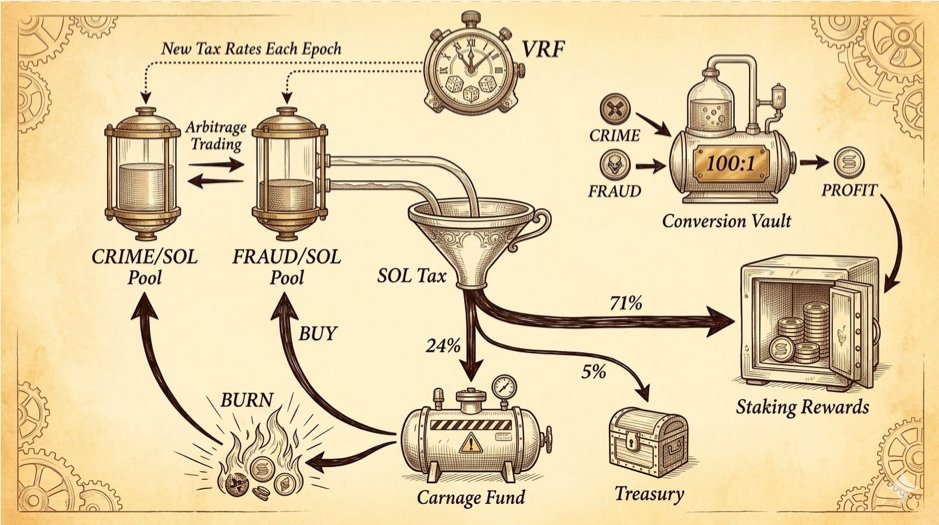

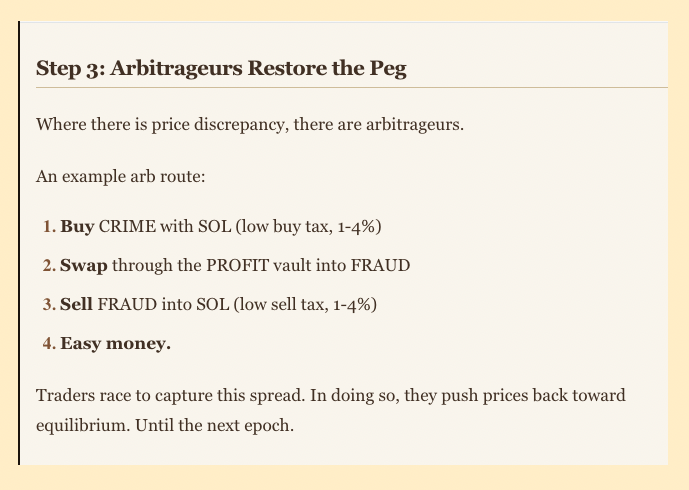

new ponzi study: @fraudsworth

I always appreciate looking at the technical / tokenomics side of a new ponzi, and this one on SOL is novel and they put in effort clearly

Three token system: $CRIME $FRAUD $PROFIT

CRIME and FRAUD are both pegged to PROFIT. Swap in 100 of either to get 1 PROFIT

CRIME and FRAUD each have their own SOL pools with high taxes that frequently change (ie 2% buy and 10% sell). The taxes go towards PROFIT stakers. PROFIT has no SOL pool. In fact, all 3 tokens don't appear on any terminal or dexscreener because they use custom AMM. Can only buy on their site

Because the buy and sell tax constantly vary on both CRIME and FRAUD, arbers can arb by using a PROFIT conversion as intermediary

The coin(s) is at 3.5M mcap right now. Disclaimer I don't hold any cause I think its kinda late but respect to the effort

30

11

180

32,356

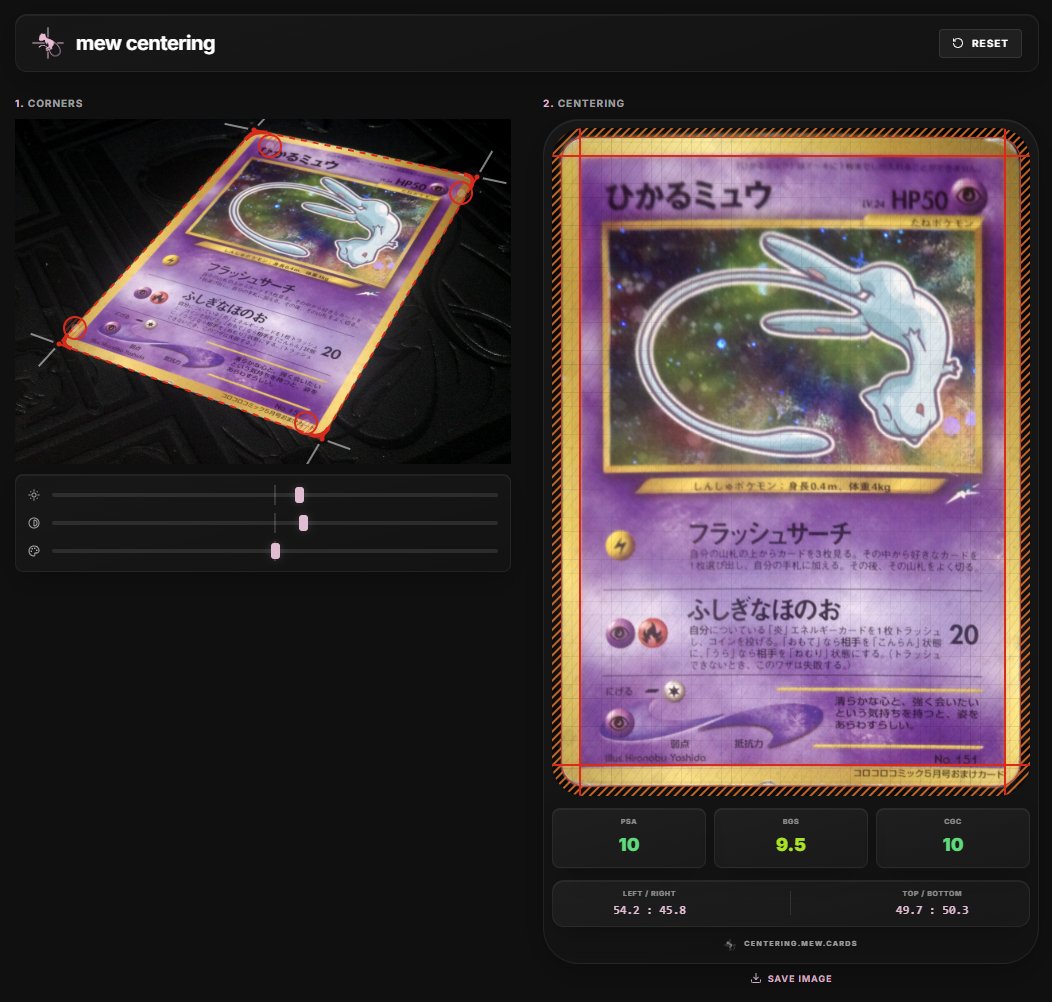

LP 🐡 retweeted

Apr 1

One of my go-to centering apps added a paywall, so I made my own free-to-use centering tool. By selecting the corners of the card, it will automatically account for perspective and flatten it for an accurate assessment!

centering.mew.cards/

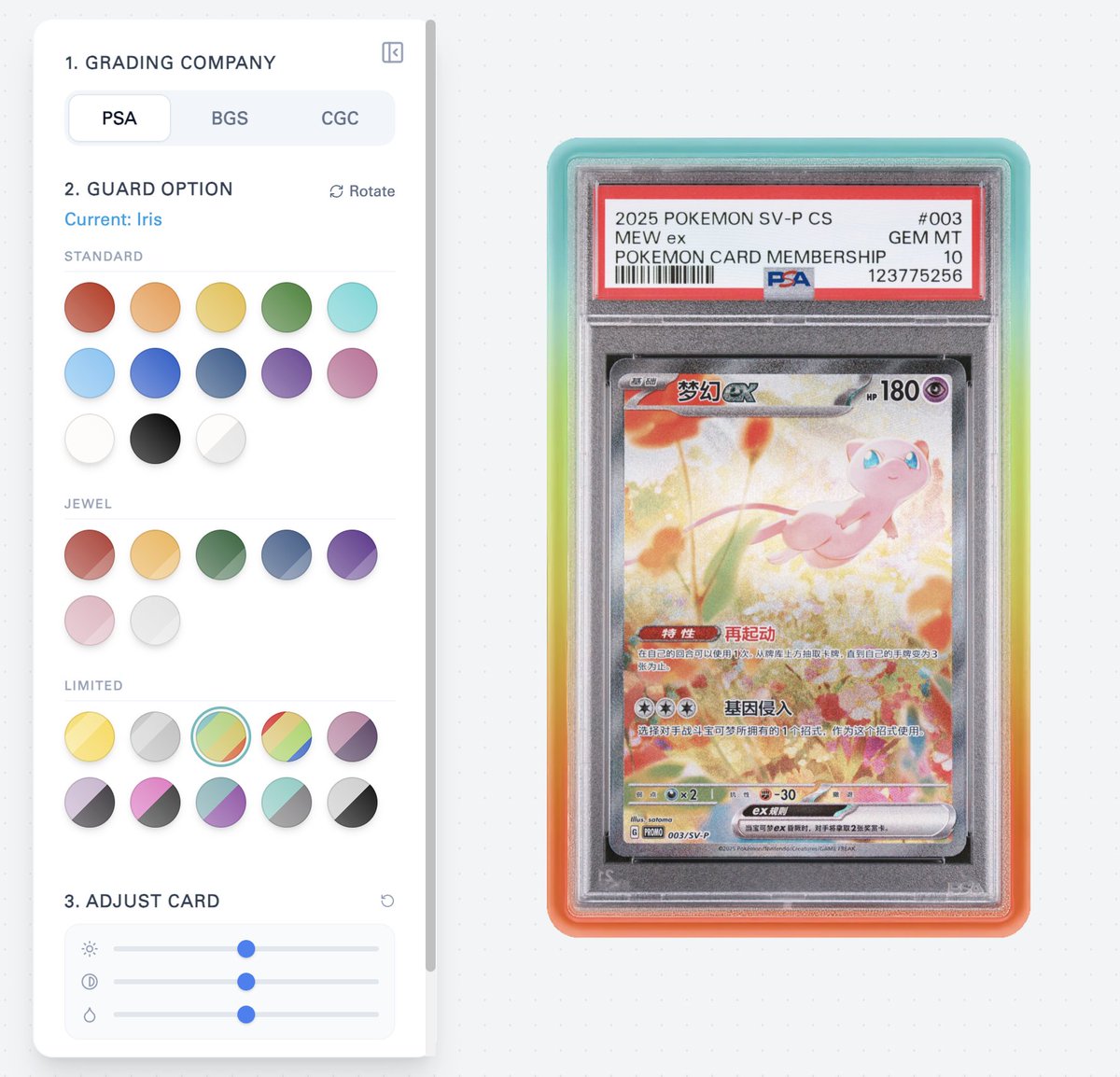

10 Dec 2025

I made a web app to try out different Graded Guard options! I’ll be adding more colors over time.

mew.cards/gg/

55

110

2,027

205,895

LP 🐡 retweeted

Mar 24

Built something @Collector_Crypt was missing.

Real-time pull analytics. AI advisor. Streak tracking. Live feed. Leaderboard.

Now let's double the fun.

gacha-terminal.com

2

3

18

23,176

LP 🐡 retweeted

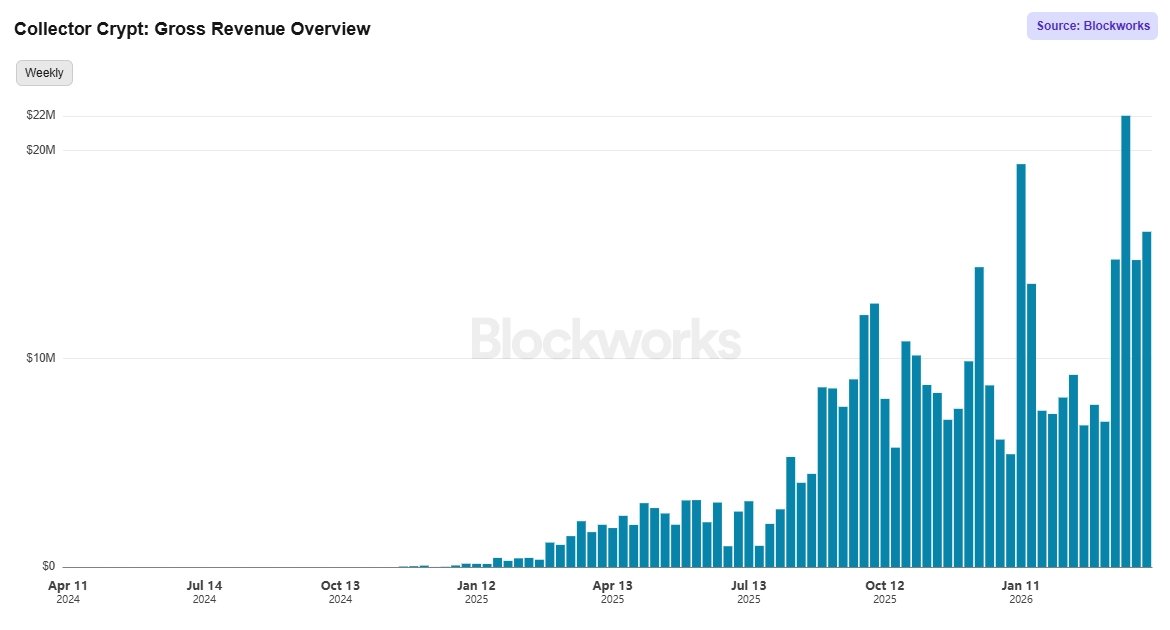

Mar 15

Market ignored the revenue of $Cards because none of it went back to the token. This will change pretty soon.

The CEO / Founder of Cards revealed some interesting insights in the last podcast:

-Generated over $13 Million in net profits over the last 12 months; he said they are likely gonna double that this year.

-So far most of the revenue went into growth, and some of that 'pretty soon' is going towards token buybacks.

-Also, a percentage of each pack sale, will be used to buy back the token (and the same applies to sales through their partner platforms).

-They are holding $10M worth of trading cards.

-Their new vaulting facility with 6k sqft opened, shows the scale they are operating at.

Won't speculate on the actual $ number yet, but even if it's only 10-20% of their revenue (whether existing or new) that goes back into the token, it will likely cause a repricing.

In these times it's prob better to bet on businesses that generate revenue outside of crypto last week Cards was again the project with the highest rev of all sub 100M mcap tokens on Solana... and soon a part of that flows back into the token.

So based on the revenue numbers and new information, building a pos in Cards seems reasonable at the current levels before they post an official buyback announcement.

Mar 11

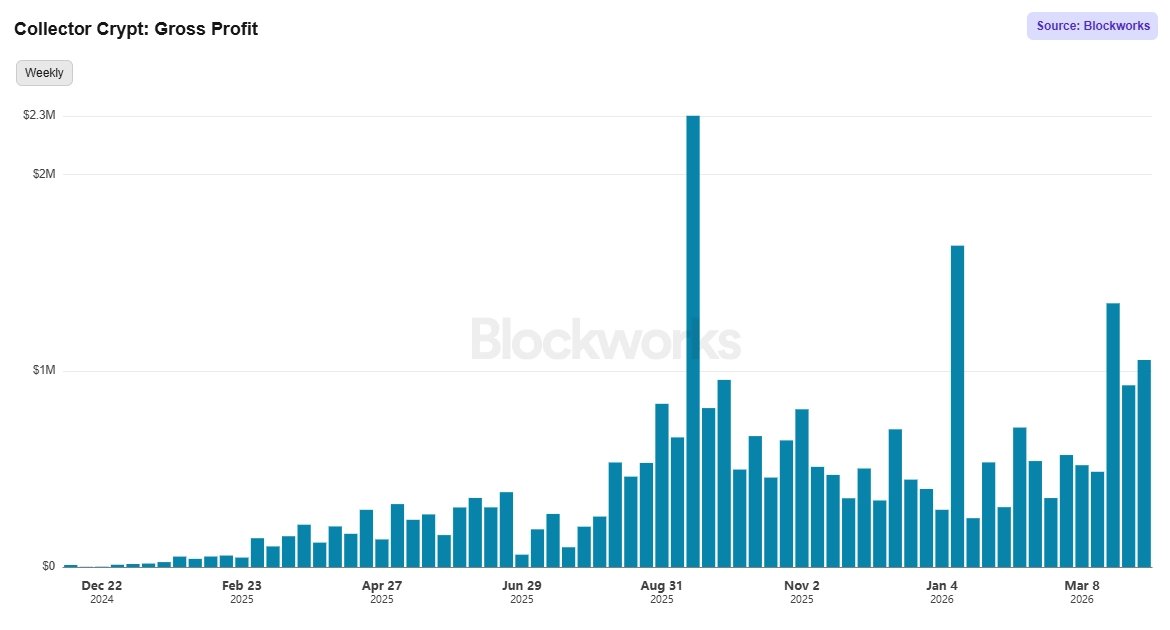

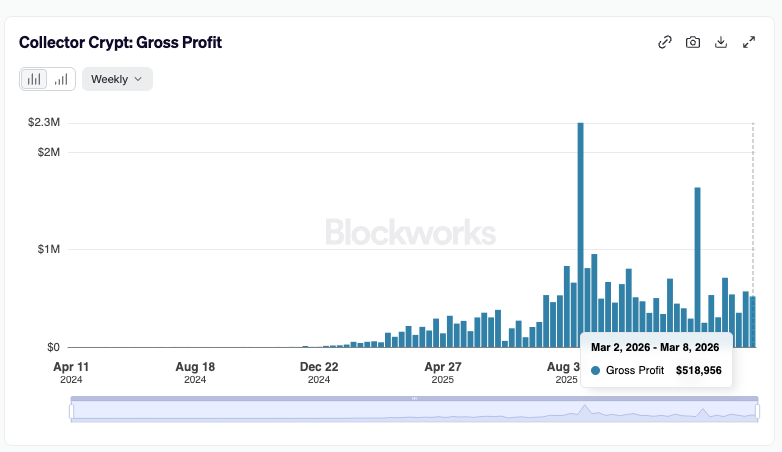

Doubling down on our $CARDS bags here on the liquid market.

@Collector_Crypt consistently ranges between $25-35M in annual gross profit, while the token FDV is currently hovering around $60M, which I largely attribute to tough market conditions and a complete lack of interest in altcoins by exhausted investors.

All of this doesn't even account for the fact that Collector holds a trading card treasury worth 8 figures, and is expanding both horizontally via @slabcash_, @renaissxyz and others, as well as vertically by integrating key parts of the supply chain.

This is the kind of opportunity investors will look back on sooner or later and realize how painfully obvious it was - and hate themselves for having ignored it purely because of fear in the market.

2

6

33

9,027

LP 🐡 retweeted

Mar 11

i built a Pokémon casino with AI

fully built with @openclaw Using @Collector_Crypt gacha packs — real graded cards tokenized on-chain as the prize pool

no dev team

no trad devs

just me, the vision, and an AI agent that handled the frontend, backend, smart contracts and deployment

the concept is simple

1v1 pack battles on solana

pick your packs

find an opponent

both sides rip at the same time

highest total card value takes everything

real cards

real stakes

no house edge on the outcome

this is either insanely cooked or the future of pokemon gacha packs!

collectorroll.com

70

13

319

55,683

红包来了 🧧

Just unsealed my @MezoNetwork Red Envelope (VXLUZYP). Phase II of the MEZO airdrop is here, and this is where allocations grow.

Unseal yours 👇

mezo.org/feature/rewards

3

1

76

After the last 30th anniversary promo post went viral @Pokemon reached out, gave me a slap on the wrist but also the opportunity to submit a few things for real consideration later in the year. Proof you can just tweet things into existence 🙏

88

906

11,401

502,709

LP 🐡 retweeted

Feb 14

Broke: tIeR oNe vCs pouring billions into the next shiny L1 or L2 that nobody will ever use.

Woke: Tier 3 VCs (= @MoonrockCapital) quietly picking up plays like @Collector_Crypt and @Beezie at ground-floor valuations while nobody believed in them.

Fast forward to today, all the circle jerk infra plays are down -95% or more, while the collectible card market has outperformed literally every other asset class. Not just crypto. Gold, S&P, AI, all of them.

And feels like it's not even slowing down anytime soon.

Imagine owning the emerging picks and shovels play of such a market. Collector & Beezie are going to be this cycle's PumpFun & Hyperliquid.

Much higher for Collectible Capital Markets.

45

17

147

11,164

LP 🐡 retweeted

Feb 4

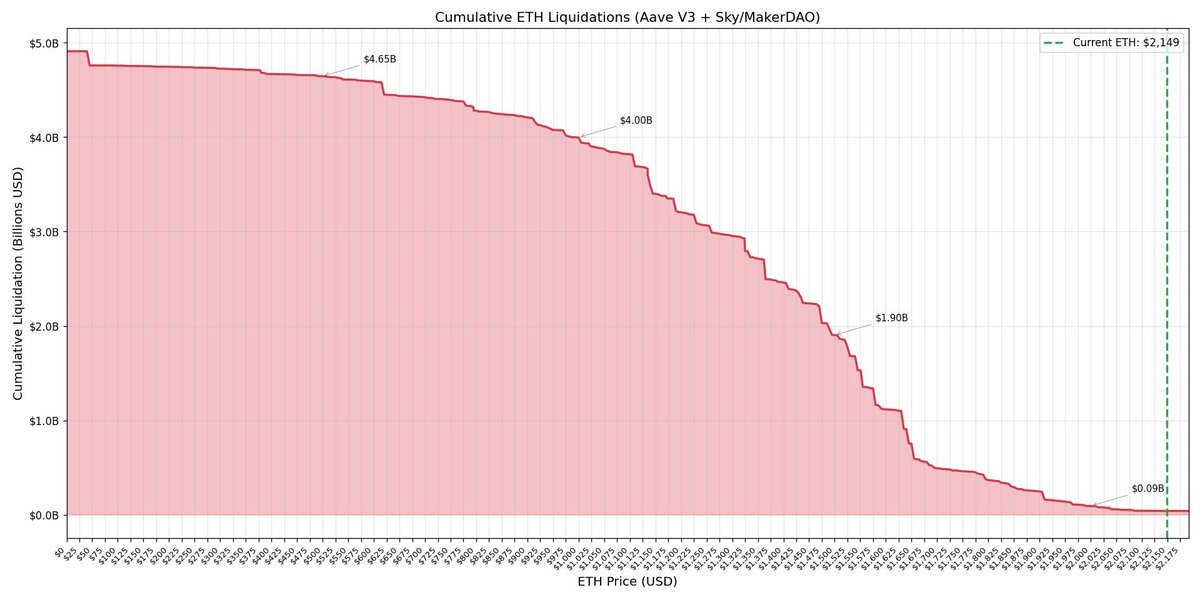

Over the last week two of the largest public ETH whales have capitulated the majority of their levered positions. This has caused ETH to decline over 20% also dragging BTC down to natural support levels at prior cycle ATH's. This began with Garrett's 200k ETH perp long liquidated over the weekend, bringing prices dangerously close to Trend Research's liquidation levels on leveraged ETH vs USDT Aave positions. However, Trend has now repaid mid 9 figs of their original position while Garrett has sold ~300m additional Spot ETH. We believe this puts ETH in a position where natural demand can fill the remaining forced sellers. As can be seen in the below chart, Trend Research's liquidation levels are now in the 1600s, roughly 24% away from current price. Once ETH bounces at all the reflexive loop will end. Market should realize this soon and the combination of powerful technical support makes now a logical point to call a bottom on ETH and crypto more broadly. We are long ETH outright.

47

48

705

111,540

LP 🐡 retweeted

Feb 4

Remember: they don't use $BTC as collateral and have a cash runway

x.com/MilkRoad/status/201877…

Feb 3

There's a persistent myth floating around that Strategy is one bad $BTC drawdown away from a forced liquidation.

That their Bitcoin is pledged as collateral and margin calls are looming.

Save this and remember: None of the above is true.

$MSTR’s Bitcoin is not collateral.

This is the single most important thing to understand.

Strategy's debt is primarily unsecured. There are no margin calls tied to Bitcoin's price.

If $BTC drops another 20%, 30%, or even 50%, no lender is showing up to demand they sell.

That's not how their debt structure works.

The maturity schedule is distant.

Most of their debt doesn't come due until 2028-2030.

Meaning there’s no near-term refinancing crunch, and no wall of debt maturing in the next 12 months that will force their hand.

$MSTR’s total debt: roughly ~$8.24B.

Current Bitcoin holdings: ~$53.26B at the time of this writing.

That's a ratio of about 6.5x coverage.

Even if Bitcoin dropped by 50% from here, they'd still have more than 3x their debt obligations in $BTC value.

And they've taken it a step further.

Strategy has set aside 2.5 years of cash runway.

This covers interest payments and dividend obligations.

So they do not need to sell a single satoshi to meet their financial commitments, even if $BTC trades below their cost basis for an extended period.

They're not leveraged long with a liquidation price.

They're a company holding an asset worth 6x their total debt, with years of runway, and no collateral agreements forcing sales.

If you want to worry, come back in 2-4 years from now and re-assess.

1

1

352