Joined March 2018

- Tweets 1,931

- Following 211

- Followers 457

- Likes 2,430

236 Photos and videos

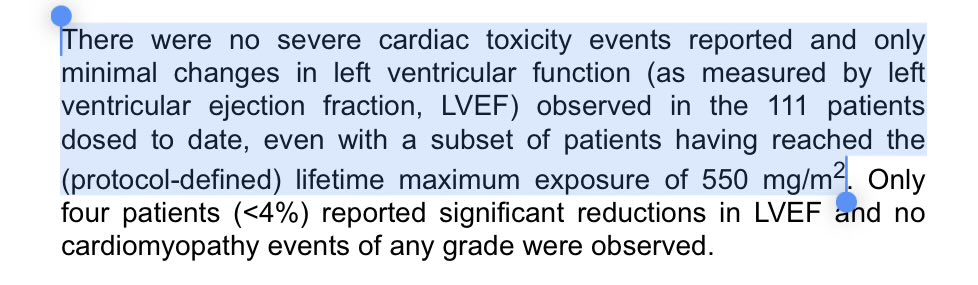

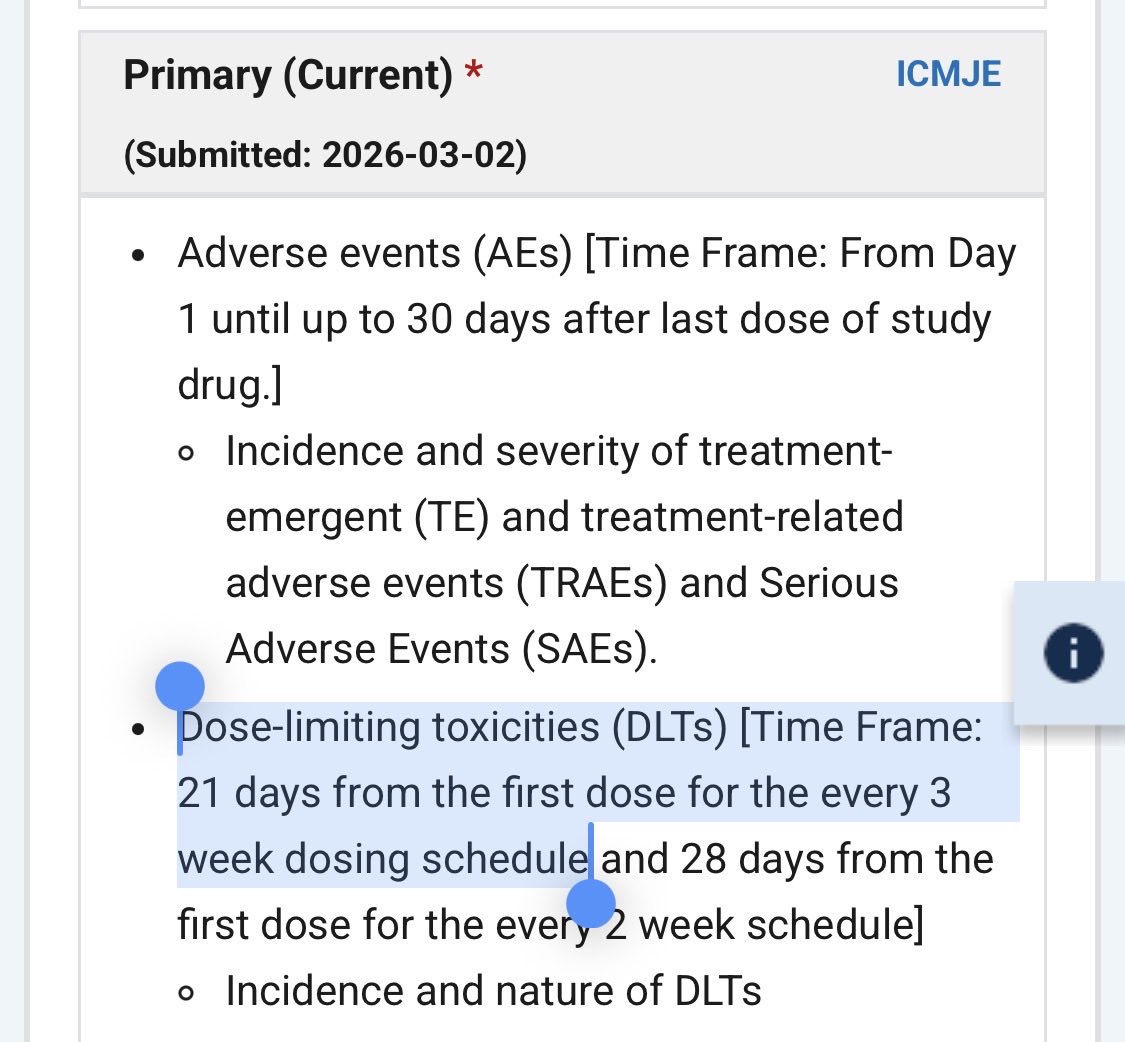

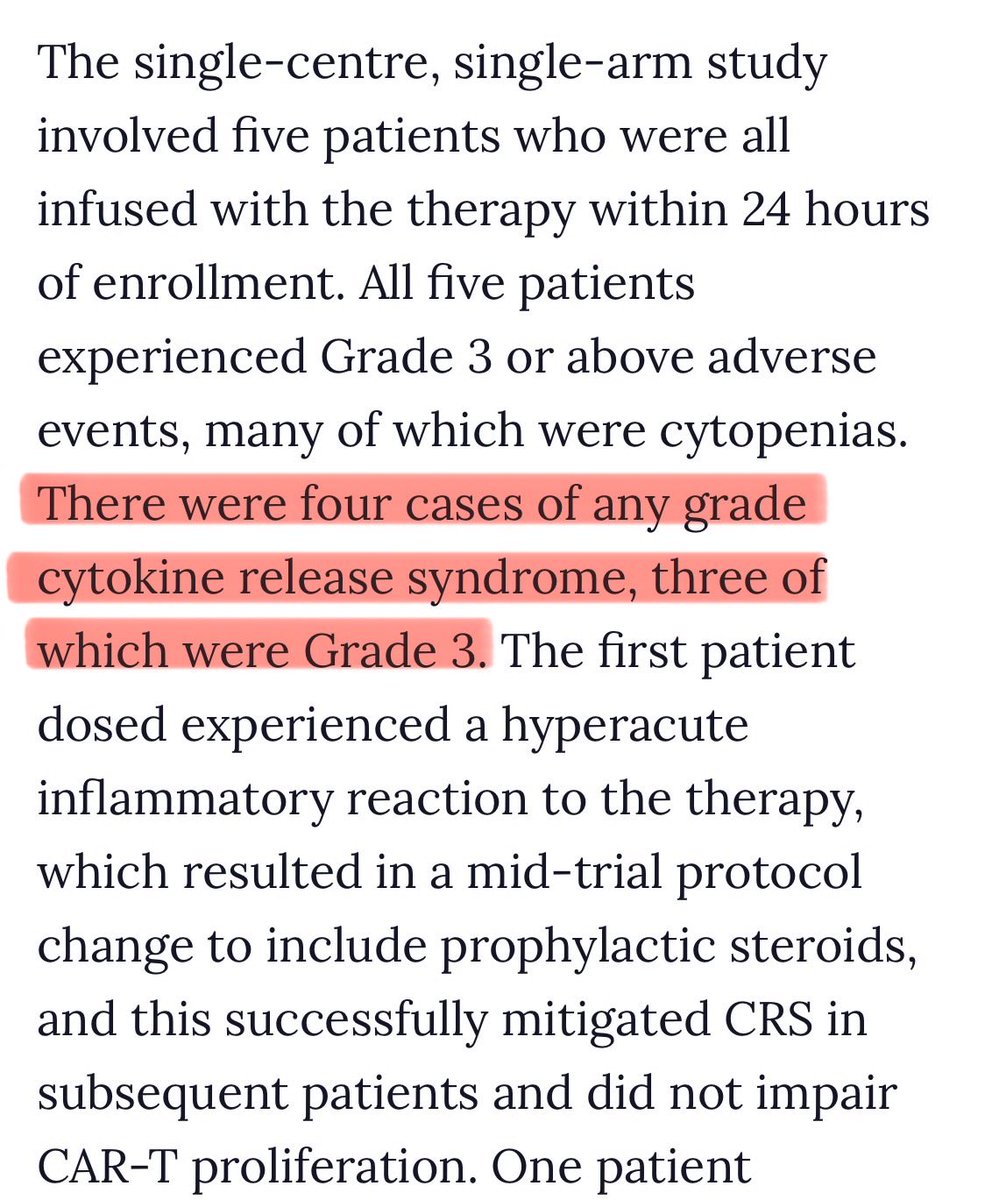

AVA6000 patient population is getting increasingly meaningful

Acknowledgment of this full ‘n’ group further supports my view that accelerated pathways for SGC (and maybe others) leverage the strong safety of the full trial, beyond just indication subsets

Very positive IMO #AVCT

1

3

45

2,292

Been busy with the day job recently but lots of positives coming from #AVCT now.

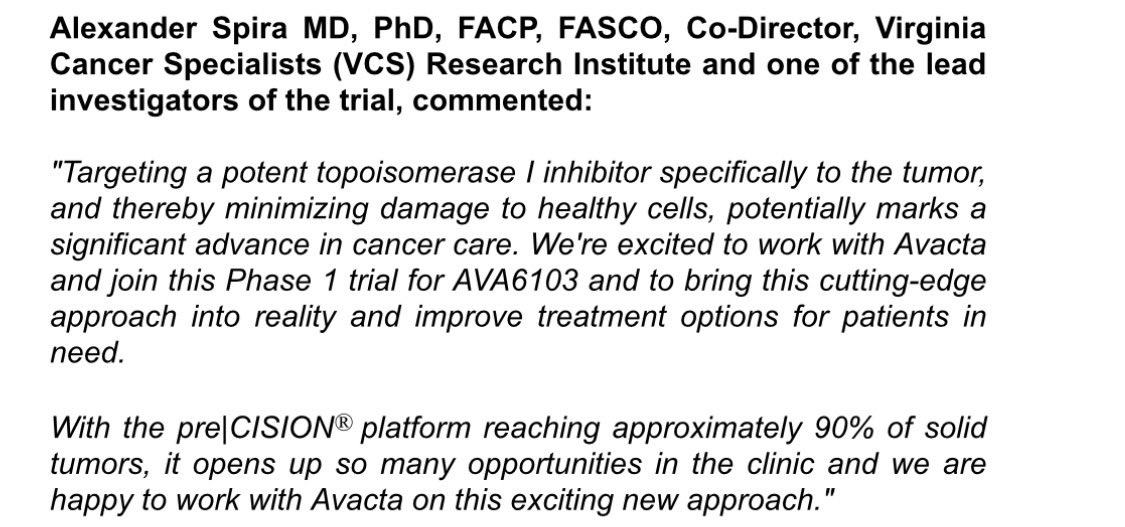

This CEO statement is incredible. Confidence abounds much to parse from these 4 paragraphs alone!

Growing IP, rapid development, multiple commercial opps, broadening application of the tech.1/3

1

5

61

2,316

However the root of all value is here:

“we believe [pre|CISION] is the only technology that is capable of delivering cancer treatment drugs directly to the tumor at the precise concentrations our payloads can achieve – and without triggering severe toxic side effects.” 2/3 #AVCT

2

4

42

1,405

Everything falls into place from this statement

Its built on lab data. Informed by the success of A6K. It points to AVA6103 doing what we, co, Drs patients all hoped

Its not over-confidence but an informed articulation of what #AVCT holds how it should be valued (by BP).3/3

44

1,473

Science day…

Same old, same old?

Maybe share price-wise but more meaningful in terms of intangibles, IMO.

My first time at an #AVCT investor meeting in person - I live at least one border away from Piccadilly!

Overall, lots of familiar content but some key additions. 1/6

2

3

67

4,141

- Richard Hughes was there facing off with investors… it’s a Science Day, he didn’t need to be.

Easy to tell ppl they should get to meetings in person but I know myself it’s hard for many.

So my somewhat independent take on #AVCT’s Science Day is:

5/6

1

3

45

3,167

✅ #AVCT’s tech is dynamite

✅ Team is absurdly talented

✅ there’s a maturity to (pre)clinical commercial progress

✅ taking time to do it right will pay back

✅ FDA = a friendly counterparty

✅ independent doctors are excited about 6103

✅ Nearterm: data IP ( deals?)

6/6

5

2

127

2,199

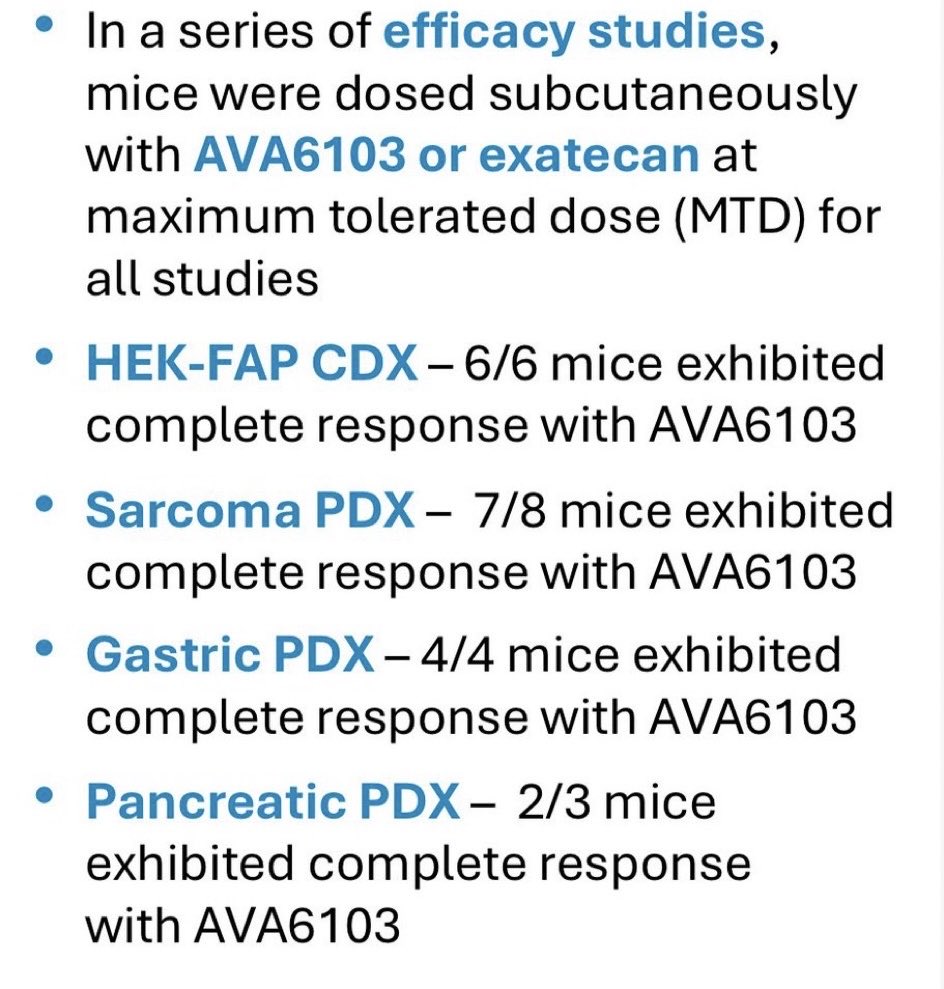

Its becoming more likely #AVCT is setting up for a Cancer of Unknown Primary (CUP) component to the AVA6103 trial in Ph2 IMO

Suite of indications proving broad efficacy supports that, coupled with in-scope adeno SC carcinoma histologies making up the majority of CUP cases.1/3

11 Aug 2025

It must be understood how critical tumour agnostic Tx is for rare cancer, cancer of unknown primary etc. As well as economic practical benefits

That preclin data shows the potential of 6103 across a range of indications, really bolstering those tumour agnostic credentials. 3/4

1

4

40

4,029

CUP has massive unmet need with no specific Tx. A drug with the ability to target a range of indications based on FAP a broad utility warhead like EXd is perfect for this.

Opens up ODD, accelerated pathways for AVA6103, plus a big Ph2 patient population.2/3 #AVCT

1

29

1,508

Interestingly, 6103 poster refers to DU145 prostate cancer; a PSA PMSA negative subtype, so traditional Tx dont work. AVA6103 presents opportunity for primary CUP

Staggering potential here - CUP success is both hugely lucrative the pinnacle of platform valuation. 3/3 #AVCT

1

1

40

1,570

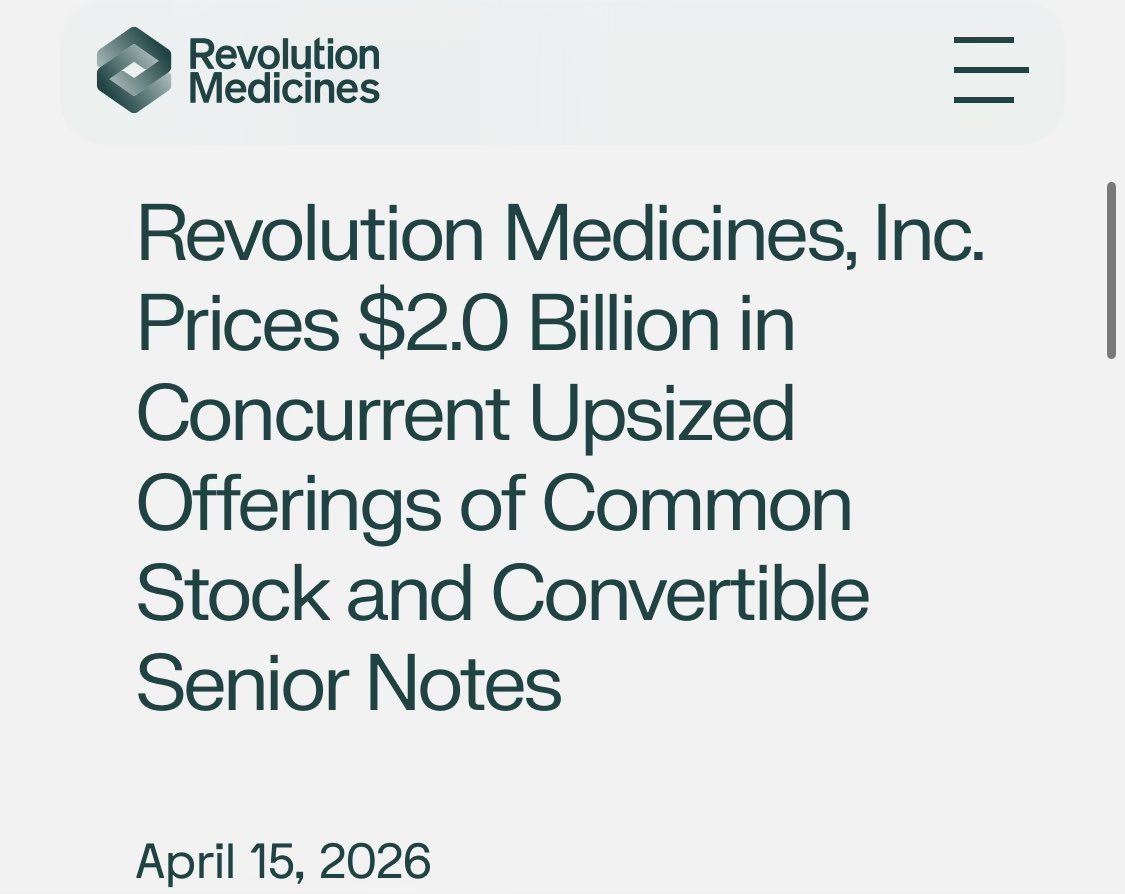

Revolution raises $2bn. Upsized 100% vs initial target of $1bn - placing shares issued at $142. Little to no discount.

Good data opens so many doors.

#AVCT

“Daraxonrasib achieved OS of 13.2 months compared to 6.7 months for chemotherapy.” - BioSpace

“PFS doesn’t matter”, “Pharma only wants cures” narrative going right out the window.

Giving patients more time really matters. Expect updated AVA6000 data this Q really shines.

#AVCT

3

31

3,206

Lilly acquire Crossbridge Bio for $300m.

Lead asset is a dual payload “potential best-in-class TROP2-targeting TOP1i/ATRi ADC”

PRE-IND stage tech.

Very straight forward read across for the value disconnect with #AVCT.

businesswire.com/news/home/2…

4

3

28

3,901

“Daraxonrasib achieved OS of 13.2 months compared to 6.7 months for chemotherapy.” - BioSpace

“PFS doesn’t matter”, “Pharma only wants cures” narrative going right out the window.

Giving patients more time really matters. Expect updated AVA6000 data this Q really shines.

#AVCT

3

1

48

6,785

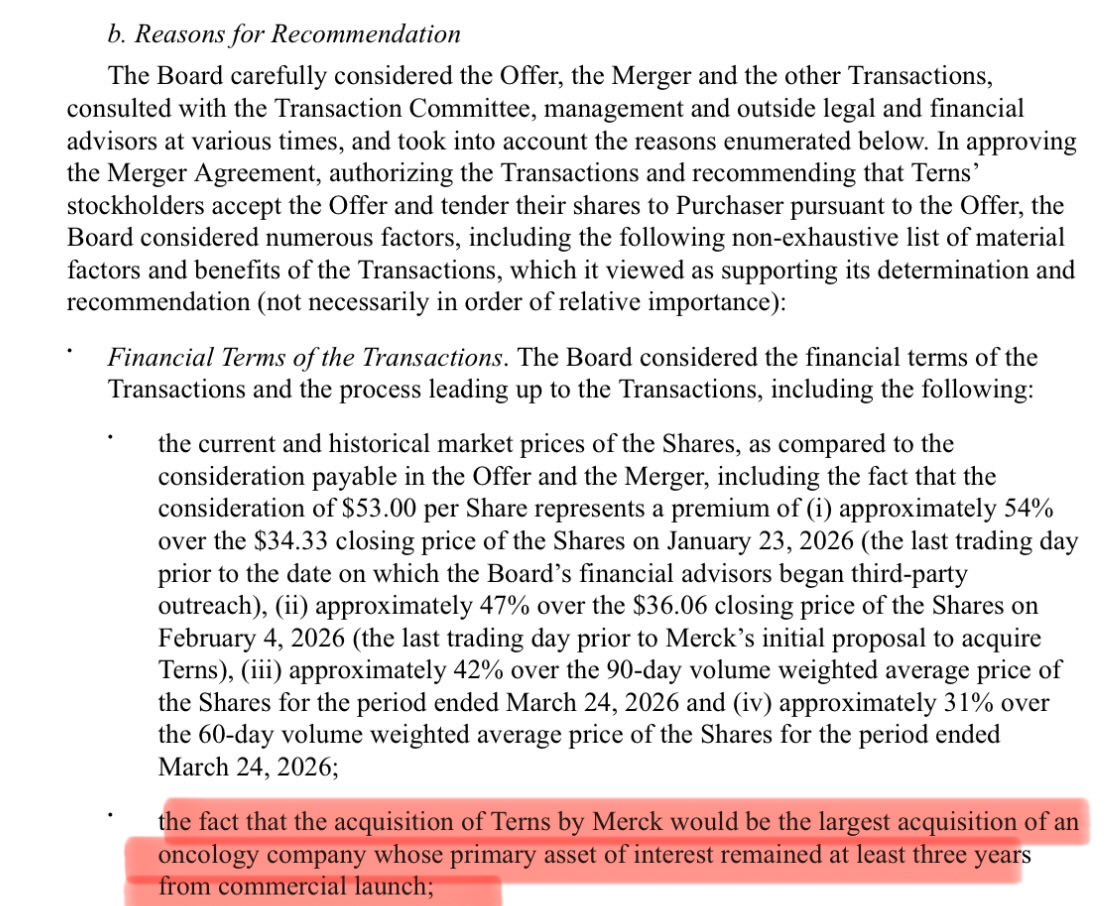

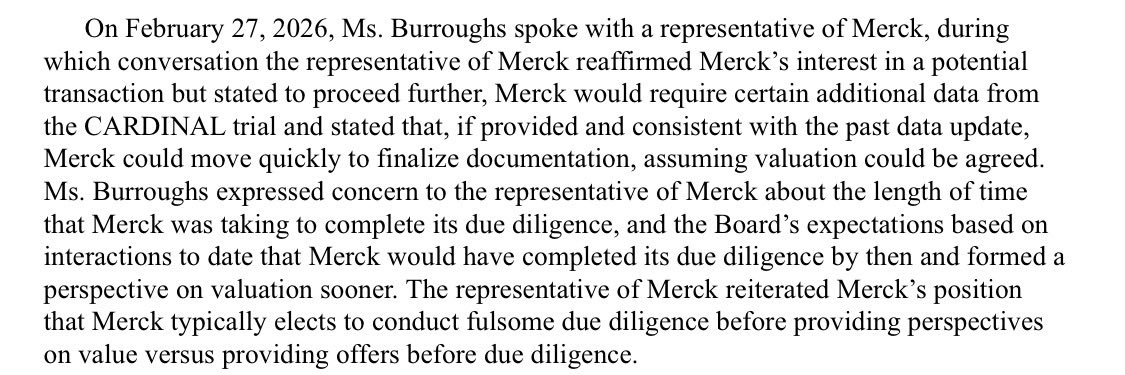

Some nuggets on the Terns-$MRK deal from SEC fillings

Merck/Terns had confidentially agreement in place since Sept 23. TO took place in March 26

Shows how long the “dating” stage can take. Expect #AVCT has been party to CA’s for a while given multiple mentions of partnering.1/4

Lead asset is P1/2 stage oral inhibitor with Fast Track designation. N=63 in Sept but Best in Class claims for leukaemia, so big TAM = blockbuster potential

Not a platform. 1 core lead drug. $6bn

Terns also sitting on ~£1bn cash. So negotiating strength & SP 1400% in 12 months

2

3

42

9,651

Recognised this was an unprecedented offer for a co ~3 years from revenue.

$5.7bn valuation (ex cash) for worldwide peak sales of $6.7bn p/a for a single Leukemia drug.

All eggs in one basket - so how much for the goose that lays them? ie much desired platform tech. 3/4 #AVCT

1

1

35

1,993

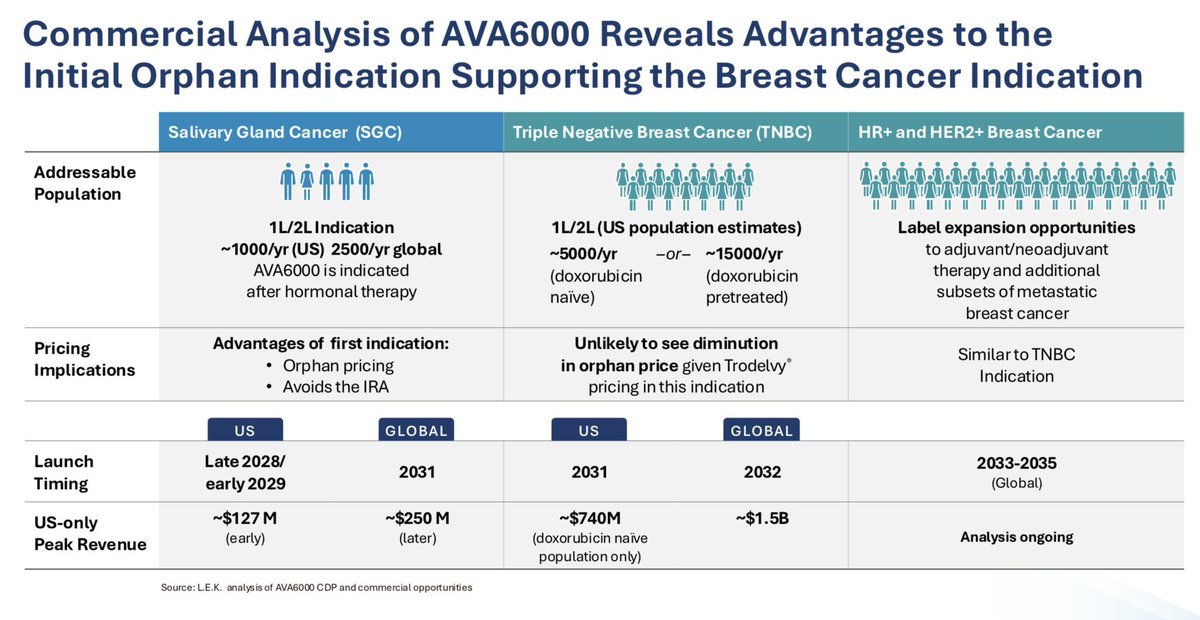

Ignoring preCISION, asset-wise, A6K offers nearer term sales. Column on the right pushing sales into Terns range.

Then there is AVA6103, which is a different stratosphere. #AVCT seems to show more confidence in The Beast every day. Plus dual warhead, Gen 3, oral delivery(?).4/4

1

5

45

2,159