Joined January 2014

- Tweets 7,431

- Following 823

- Followers 1,351

- Likes 43,623

36 Photos and videos

Jun 11

Asked @grok: What permits—federal, state, or county--will HydroGraph $HGRAF need to get a short (on WGI property outside of Bellville, Tx in unincorporated Harris County) acetylene pipeline serving a planned 70k square foot graphene production facility using HydroGraph's patented detonation synthesis process? No city permits needed, as Western (WGI) is located in an unincorporated part of Austin County.

Grok’s answer, lightly edited: For a short acetylene pipeline entirely on private (WGI) property in unincorporated Austin County, Texas (near Bellville; note the query mixes Harris and Austin Counties, but Bellville is in Austin County), requirements focus mainly on state/county levels with limited or no federal involvement. Acetylene is a flammable gas (Division 2.1 hazardous material), used in HydroGraph’s detonation synthesis process. Regulations treat it under flammable gas/pipeline rules, but a very short, on-site line differs from transmission or gathering pipelines.

Federal Permits (Likely None Required)

•PHMSA (Pipeline and Hazardous Materials Safety Administration): PHMSA regulates interstate pipelines and certain intrastate ones under 49 CFR Parts 191/192 (gas) or 195 (hazardous liquids). A short, on-site pipeline wholly within one facility/property, not used for transportation across property lines or in interstate commerce, generally falls outside PHMSA jurisdiction (more like process piping or facility piping). OSHA may cover workplace safety aspects instead.

•No FERC involvement (that's for interstate natural gas facilities).

No other major federal permits (e.g., Corps of Engineers) expected unless wetlands/crossings of jurisdictional waters are involved (unlikely for a short on-site line).

Recommendation: Confirm with PHMSA or a pipeline safety consultant, as acetylene has special stability/pressure rules (e.g., max ~15 psig in piping).

State Permits (Primarily Railroad Commission of Texas - RRC)

•T-4 Pipeline Permit (16 TAC §3.70): Required for operators of transmission, gathering, or certain other pipelines before operation. However, exemptions apply for production/flow lines that never leave a lease or a tract of land under the operator’s control (ownership or lease).

•If the acetylene line stays entirely on WGI property (one controlled tract) and serves only the on-site graphene facility, it likely qualifies as exempt (private/on-site piping, not leaving the tract).

•If it crosses property boundaries, serves multiple sites, or is classified as gathering/transmission, a T-4 (and annual renewal) would be needed, plus P-5 Organization Report and financial assurance.

•RRC has no siting/routing authority for intrastate lines like this.

County Permits (Austin County - Key Requirements)

•Unincorporated areas have lighter oversight than cities, but development and utility work still require approvals. Austin County has specific processes for pipelines and industrial development.

Pipeline/Utility Permits:

•Pipeline Agreement or Permit to Construct in Public Road Right-of-Way (PIPROW) if the line crosses or impacts any county roads/drainage (common even for short lines). Requires commissioner/engineer approval, fees, depth/cover specs (e.g., minimum burial), and safety measures.

•Development/Commercial Building Permit: Required for the 70k sq ft facility itself. Submit Commercial Development Permit Application; may include site plans, engineering, floodplain review (if applicable), and drainage. No full building code enforcement in many unincorporated Texas counties, but development standards apply.

•Oil & Gas Development Application (Volume 08): Relevant due to flammable gas handling; covers pipelines in this context.

•Other possible: On-site sewage (OSSF) if needed, driveway/culvert permits, floodplain development order.

Contact: Austin County Planning & Development Department (979-865-5911, planning emails) for pre-application review. They have forms for development, pipelines, and ROW work.

Additional Considerations

•Fire/safety codes: Local fire marshal or county may require compliance with NFPA standards for acetylene (storage, piping, separation from oxidizers). Hot work/welding permits during construction.

•Environmental/zoning: Check for any county-specific hazardous material rules or TCEQ coordination. No city permits needed, as noted.

•Construction practices: Licensed contractors, 811 locates (Texas One Call), proper burial/depth, materials (steel/wrought iron for acetylene), and purging/safety protocols.

•Overall facility: The graphene plant will drive most permitting (air emissions, etc.); the pipeline is ancillary.

Next Steps: Consult Austin County Planning first for site-specific guidance, then RRC to confirm T-4 exemption. Engage a Texas pipeline/facility permitting consultant or attorney familiar with industrial gas operations, as acetylene adds safety scrutiny. Requirements can vary by exact route, length, pressure, and whether any public ROW is touched. This is general guidance based on public regulations—official confirmation is essential.

*Looks like few permits are required if the entirety of the $HGRAF development is sited on WGI property, within a single tract/parcel.*

Thanks to @SportyJ from CEO.CA for sending me the initial inquiry and helping me frame it.

2

2

38

5,540

Jun 11

Asked @grok: What permits—federal, state, or county--will HydroGraph $HGRAF need to get a short (on WGI property outside of Bellville, Tx in unincorporated Harris County) acetylene pipeline serving a planned 70k square foot graphene production facility using HydroGraph's patented detonation synthesis process? No city permits needed, as Western (WGI) is located in an unincorporated part of Austin County.

Grok’s answer, lightly edited: For a short acetylene pipeline entirely on private (WGI) property in unincorporated Austin County, Texas (near Bellville; note the query mixes Harris and Austin Counties, but Bellville is in Austin County), requirements focus mainly on state/county levels with limited or no federal involvement. Acetylene is a flammable gas (Division 2.1 hazardous material), used in HydroGraph’s detonation synthesis process. Regulations treat it under flammable gas/pipeline rules, but a very short, on-site line differs from transmission or gathering pipelines.

Federal Permits (Likely None Required)

•PHMSA (Pipeline and Hazardous Materials Safety Administration): PHMSA regulates interstate pipelines and certain intrastate ones under 49 CFR Parts 191/192 (gas) or 195 (hazardous liquids). A short, on-site pipeline wholly within one facility/property, not used for transportation across property lines or in interstate commerce, generally falls outside PHMSA jurisdiction (more like process piping or facility piping). OSHA may cover workplace safety aspects instead.

•No FERC involvement (that's for interstate natural gas facilities).

No other major federal permits (e.g., Corps of Engineers) expected unless wetlands/crossings of jurisdictional waters are involved (unlikely for a short on-site line).

Recommendation: Confirm with PHMSA or a pipeline safety consultant, as acetylene has special stability/pressure rules (e.g., max ~15 psig in piping).

State Permits (Primarily Railroad Commission of Texas - RRC)

•T-4 Pipeline Permit (16 TAC §3.70): Required for operators of transmission, gathering, or certain other pipelines before operation. However, exemptions apply for production/flow lines that never leave a lease or a tract of land under the operator’s control (ownership or lease).

•If the acetylene line stays entirely on WGI property (one controlled tract) and serves only the on-site graphene facility, it likely qualifies as exempt (private/on-site piping, not leaving the tract).

•If it crosses property boundaries, serves multiple sites, or is classified as gathering/transmission, a T-4 (and annual renewal) would be needed, plus P-5 Organization Report and financial assurance.

•RRC has no siting/routing authority for intrastate lines like this.

County Permits (Austin County - Key Requirements)

•Unincorporated areas have lighter oversight than cities, but development and utility work still require approvals. Austin County has specific processes for pipelines and industrial development.

Pipeline/Utility Permits:

•Pipeline Agreement or Permit to Construct in Public Road Right-of-Way (PIPROW) if the line crosses or impacts any county roads/drainage (common even for short lines). Requires commissioner/engineer approval, fees, depth/cover specs (e.g., minimum burial), and safety measures.

•Development/Commercial Building Permit: Required for the 70k sq ft facility itself. Submit Commercial Development Permit Application; may include site plans, engineering, floodplain review (if applicable), and drainage. No full building code enforcement in many unincorporated Texas counties, but development standards apply.

•Oil & Gas Development Application (Volume 08): Relevant due to flammable gas handling; covers pipelines in this context.

•Other possible: On-site sewage (OSSF) if needed, driveway/culvert permits, floodplain development order.

Contact: Austin County Planning & Development Department (979-865-5911, planning emails) for pre-application review. They have forms for development, pipelines, and ROW work.

Additional Considerations

•Fire/safety codes: Local fire marshal or county may require compliance with NFPA standards for acetylene (storage, piping, separation from oxidizers). Hot work/welding permits during construction.

•Environmental/zoning: Check for any county-specific hazardous material rules or TCEQ coordination. No city permits needed, as noted.

•Construction practices: Licensed contractors, 811 locates (Texas One Call), proper burial/depth, materials (steel/wrought iron for acetylene), and purging/safety protocols.

•Overall facility: The graphene plant will drive most permitting (air emissions, etc.); the pipeline is ancillary.

Next Steps: Consult Austin County Planning first for site-specific guidance, then RRC to confirm T-4 exemption. Engage a Texas pipeline/facility permitting consultant or attorney familiar with industrial gas operations, as acetylene adds safety scrutiny. Requirements can vary by exact route, length, pressure, and whether any public ROW is touched. This is general guidance based on public regulations—official confirmation is essential.

Looks like few permits are required if the entirety of the $HGRAF development is sited on WGI property, within a single tract/parcel.

Thanks to @SportyJ from CEO.CA for sending me the initial inquiry and helping me frame it.

1

12

1,144

Jun 11

Was curious about the Railroad Commission of Texas' (RRC.texas.gov) oversight of $HGRAF HydroGraph's acetylene pipeline, likely on or adjacent to WGI in Bellville, Texas. Found an approval last year for Orion's carbon black plant expansion to install a 12-inch acetylene pipeline (rrc.texas.gov/media/cyobcgq5… on p 1, if you're curious), and queried @Grok the following:

- What is the approximate annual delivery capacity (in tons) of the 12" acetylene pipeline whose application appears to have been received by the Texas Railroad Commission on 1/16/2025, with construction commencing on 1/27/2025?

- When was the pipeline completed?

- Is a ten-day timeline from submission to commencing construction a reasonable expectation for a company like WGI for a pipeline fully or predominantly constructed within its property?

Here are the responses:

Approximate Annual Delivery Capacity:

A rough estimate for a 12-inch acetylene pipeline (assuming typical industrial gas pressures, e.g., 100–500 psig range, and safe velocities for compressible gas) is in the range of tens of thousands to low hundreds of thousands of tons per year, depending on operating pressure, temperature, compression, and duty cycle.

Acetylene (C₂H₂) is a compressed gas, not a high-volume cryogenic liquid like LNG or typical hydrocarbons, so capacities are lower than for natural gas or liquids in similar-diameter lines.

For context, Orion's La Porte plant (the likely anchor user) was designed around acetylene supply from a neighboring site and targets specialty carbon black output on the order of ~12,000 metric tons/year capacity (earlier plans).

A dedicated 12" line would support far more than one plant's needs or serve as a distribution header. Real-world throughput would be set by downstream demand, pressure management, and safety factors for acetylene (which has unique decomposition risks).

This pipeline appears to be a short/on-site or intra-facility lateral (common for such notifications), not a long-haul transmission line.

Completion Date

Public records do not specify an exact completion or in-service date. Construction notification was received/started around January 27, 2025 (per RRC 2025 new construction reports).

Short laterals on industrial property can be completed in weeks to a few months. No major updates on delays or operational start were found as of mid-2026; it aligns with Orion's La Porte plant ramp-up timelines (targeting 2024–2026 phases).

Was a ~10-Day Timeline (Application to Construction Start) Reasonable?

Yes, for a company like WGI (or similar industrial gas/pipeline operator) on predominantly private/owned property. Texas RRC T-4 pipeline permits (or notifications like PS-48) for short, non-public-right-of-way lines on industrial sites involve simpler reviews focused on safety/compliance rather than extensive environmental/stakeholder processes.

Intra-plant or adjacent-facility acetylene lines (e.g., from supplier to user like Orion) often move quickly if no crossings or eminent domain issues exist.

The ~10-day gap (application ~1/16–1/17/2025 to start 1/27/2025) fits typical fast-track notifications for minor extensions or new short systems. Longer interstate/transmission lines take far more time.

Note: This pipeline supports industrial acetylene users (e.g., Orion's carbon black production) in the Houston area. HydroGraph's separate Texas graphene plans involve acetylene supply/pipeline access but are not directly tied to this specific Orion-named line.

Great news!

2

41

2,977

Jun 11

Was curious about the Railroad Commission of Texas' (RRC.texas.gov) oversight of $HGRAF HydroGraph's acetylene pipeline, likely on or adjacent to WGI in Bellville, Texas. Found an approval last year for Orion's carbon black plant expansion to install a 12-inch acetylene pipeline (rrc.texas.gov/media/cyobcgq5… on p 1, if you're curious), and queried @Grok the following:

- What is the approximate annual delivery capacity (in tons) of the 12" acetylene pipeline whose application appears to have been received by the Texas Railroad Commission on 1/16/2025, with construction commencing on 1/27/2025?

- When was the pipeline completed?

- Is a ten-day timeline from submission to commencing construction a reasonable expectation for a company like WGI for a pipeline fully or predominantly constructed within its property?

Here are the responses:

Approximate Annual Delivery Capacity:

A rough estimate for a 12-inch acetylene pipeline (assuming typical industrial gas pressures, e.g., 100–500 psig range, and safe velocities for compressible gas) is in the range of tens of thousands to low hundreds of thousands of tons per year, depending on operating pressure, temperature, compression, and duty cycle.

Acetylene (C₂H₂) is a compressed gas, not a high-volume cryogenic liquid like LNG or typical hydrocarbons, so capacities are lower than for natural gas or liquids in similar-diameter lines.

For context, Orion's La Porte plant (the likely anchor user) was designed around acetylene supply from a neighboring site and targets specialty carbon black output on the order of ~12,000 metric tons/year capacity (earlier plans). A dedicated 12" line would support far more than one plant's needs or serve as a distribution header. Real-world throughput would be set by downstream demand, pressure management, and safety factors for acetylene (which has unique decomposition risks).

This pipeline appears to be a short/on-site or intra-facility lateral (common for such notifications), not a long-haul transmission line.

Completion Date

Public records do not specify an exact completion or in-service date. Construction notification was received/started around January 27, 2025 (per RRC 2025 new construction reports).

Short laterals on industrial property can be completed in weeks to a few months. No major updates on delays or operational start were found as of mid-2026; it aligns with Orion's La Porte plant ramp-up timelines (targeting 2024–2026 phases).

Was a ~10-Day Timeline (Application to Construction Start) Reasonable?

Yes, for a company like WGI (or similar industrial gas/pipeline operator) on predominantly private/owned property. Texas RRC T-4 pipeline permits (or notifications like PS-48) for short, non-public-right-of-way lines on industrial sites involve simpler reviews focused on safety/compliance rather than extensive environmental/stakeholder processes.

Intra-plant or adjacent-facility acetylene lines (e.g., from supplier to user like Orion) often move quickly if no crossings or eminent domain issues exist.

The ~10-day gap (application ~1/16–1/17/2025 to start 1/27/2025) fits typical fast-track notifications for minor extensions or new short systems. Longer interstate/transmission lines take far more time.rrc.texas.govNote: This pipeline supports industrial acetylene users (e.g., Orion's carbon black production) in the Houston area. HydroGraph's separate Texas graphene plans involve acetylene supply/pipeline access but are not directly tied to this specific Orion-named line.

Great news, overall!

2

32

1,276

Jun 10

If you're not paying attention to the hires $HGRAF's been making, you're missing the story. These hires are about connection, competence and confidence.

- Connections to the companies, agencies and competitions that would benefit most from HydroGraph graphene.

- Competence, in terms of what these folks project to potential buyers about the products they put a face to.

- Confidence in HydroGraph as an organization, starting with CEO Kjirsten Breure, through the BoD, and extending throughout senior staff *and* intellectual property.

Connect the dots. Add more. Get on board. The data points keep getting clearer. The choice is yours.

2

6

91

6,166

Jun 10

If you're not paying attention to the hires $HGRAF's been making, you're missing the story. These hires are about connection, competence and confidence.

- Connections to the companies, agencies and competitions that would benefit most from HydroGraph graphene.

- Competence, in terms of what these folks project to potential buyers about the products they put a face to.

- Confidence in HydroGraph as an organization, starting with CEO Kjirsten Breure, through the BoD, and extending throughout senior staff *and* intellectual property.

Connect the dots. Add more. Get on board. The data points keep getting clearer. The choice is yours.

2

6

91

2,145

Jun 8

@ArneriDesignand others asked if I could share my investment approach a few days ago. With the caveat that this is not for most, but might be helpful for a few, here is a stab at it:

Critical elements of my investing philosophy:

1.Good management is a must. Excellent management is even better, especially when making out-sized investments.

2.Identify asymmetric risk/reward

3.Understand “Risk of Ruin” and invest/manage accordingly. Read this to better understand RoR: en.wikipedia.org/wiki/Risk_o… *Do Not Make Huge Bets if You Don’t Understand “Risk of Ruin”!!* 4.Understand all investments from a Downside-First approach; e.g., “How much can I afford to lose?”

Key Ways to Manage Risk of Ruin: mitigate concentrated bets that risk wiping out most of your capital. My approach includes several layers of protection; all of the following are included:

•Asymmetric Risk-Reward Focus (Core Filter for Concentration): Investments are made based on capacity to grow quickly in large multiples. Size up massively when downside is capped/limited and upside is wide open. I seek setups where I can make a lot when right and lose little when wrong. This comes from George Soros’ investing approach: (position) sizing is 70-80% of this game. Often more, in my case.

•Downside-First Analysis: First thing I do is figure out how much money I can risk. I prioritize quantifying maximum potential loss and protecting capital over chasing gains. I hate drawdowns and focuses on preservation first—home runs come from that base.

•Quick, Flexible Loss-Cutting: No rigid mechanical stop-losses, but ruthless discipline to exit when the thesis breaks (price paid becomes irrelevant). I’ll drop positions fast. If an investment doesn’t work, walk away confidently; there are always other opportunities. This prevents small losses from becoming ruinous.

•Position Sizing and Pyramiding: Start small to test the thesis, then scale in (pyramid) aggressively only as the trade moves in my favor and conviction confirms. This can happen quickly; acting fast on conviction supported by data and analysis makes a huge difference. Biggest exposure comes on winners, not at entry. For example, in $HGRAF HydroGraph I bought in after three days of analysis (following reading a thread by @BambroughKevin and doing my own and doing my own analysis on top of his), then added massively throughout the remainder of the Summer, and modestly thereafter (as I was adding as new funds became available or other positions made sense to close out).

Here’s how things started for me:

•July 29, 2025:initial buy 1450 shares $0.713/share / $1,084

•August 2025Added23,550 shares$1.093/share/$25,747

•Mental and Process Discipline: High conviction allows me to hold through volatility but also exit without ego. I stay flexible, pay constant, close attention, and avoid over-analysis.

•Management: Management openness, competence, and delivery have become key since I watched an investment rise over 15x, then fall nearly 90% before I pulled out. I was up 150% over 18 months, but there were clean signs that management wasn’t worthy of full trust (poor communication and self-dealing, imo). But I liked the story they told, and ignored facts at odds with the narrative. Never again! This isn’t the same as delayed delivery—I’ve managed big, complex organizations and processes. Delays are normal, but goals need to be delivered within a reasonable time. “Reasonable” isn’t what most retail investors think, though. Take what you think is reasonable, then double or triple it or more. Then, before panicking, and issuing angry screeds on message boards, email the communications point person to see what info he or she can share in explanation. I’ve been repeatedly pleased with responses from $HGRAF’s folks. But understand that every question doesn’t get nor deserve an immediate response. I limit asks in frequency, realizing better, infrequent responses to questions that truly matter for the company are far more valuable to investors.

•Liquidity: Almost forgot this, but it’s critical. There’s big $$ to be made in smaller exchanges like Vancouver or the TSX. But you need to be able to exit quickly if an investment goes south. Before you size a huge position, make sure you can exit on your terms, not the market makers’.

TL;DR—I concentrate selectively on highly asymmetrical opportunities where the risk/reward is skewed heavily in my favor, backed by intense monitoring, rapid adaptation, and an obsessive focus on not blowing up. For most people this is not a great investment approach, as it risks ruin if not very capable of honest analysis and close attention. Broad diversification is safer for most. But executed exceptionally well, it can work. And note if I go to zero, I can live off my pension.

1

16

4,574

Jun 8

@ArneriDesign and others asked if I could share my investment approach a few days ago. With the caveat that this is not for most, but might be helpful for a few, here is a stab at it:

Critical elements of my investing philosophy:

1.Good management is a must. Excellent management is even better, especially when making out-sized investments.

2.Identify asymmetric risk/reward

3.Understand “Risk of Ruin” and invest/manage accordingly. Read this to better understand RoR: en.wikipedia.org/wiki/Risk_o… *Do Not Make Huge Bets if You Don’t Understand “Risk of Ruin”!!*

4.Understand all investments from a Downside-First approach; e.g., “How much can I afford to lose?”

Key Ways to Manage Risk of Ruin: mitigate concentrated bets that risk wiping out most of your capital. My approach includes several layers of protection; all of the following are included:

•Asymmetric Risk-Reward Focus (Core Filter for Concentration): Investments are made based on capacity to grow quickly in large multiples. Size up massively when downside is capped/limited and upside is wide open. I seek setups where I can make a lot when right and lose little when wrong. This comes from George Soros’ investing approach: (position) sizing is 70-80% of this game. Often more, in my case.

•Downside-First Analysis: First thing I do is figure out how much money I can risk. I prioritize quantifying maximum potential loss and protecting capital over chasing gains. I hate drawdowns and focuses on preservation first—home runs come from that base.

•Quick, Flexible Loss-Cutting: No rigid mechanical stop-losses, but ruthless discipline to exit when the thesis breaks (price paid becomes irrelevant). I’ll drop positions fast. If an investment doesn’t work, walk away confidently; there are always other opportunities. This prevents small losses from becoming ruinous.

•Position Sizing and Pyramiding: Start small to test the thesis, then scale in (pyramid) aggressively only as the trade moves in my favor and conviction confirms. This can happen quickly; acting fast on conviction supported by data and analysis makes a huge difference. Biggest exposure comes on winners, not at entry. For example, in $HGRAF HydroGraph I bought in after three days of analysis (following reading a thread by @BambroughKevin and doing my own analysis on top of his), then added massively throughout the remainder of the Summer, and modestly thereafter (as I was adding as new funds became available or other positions made sense to close out). Here’s how things started for me:

•July 29, 2025:initial buy 1450 shares $0.713/share / $1,084

•August 2025Added23,550 shares$1.093/share/$25,747

•Mental and Process Discipline: High conviction allows me to hold through volatility but also exit without ego. I stay flexible, pay constant, close attention, and avoid over-analysis.

•Management: Management openness, competence, and delivery have become key since I watched an investment rise over 15x, then fall nearly 90% before I pulled out. I was up 150% over 18 months, but there were clean signs that management wasn’t worthy of full trust (poor communication and self-dealing, imo). But I liked the story they told, and ignored facts at odds with the narrative. Never again! This isn’t the same as delayed delivery—I’ve managed big, complex organizations and processes. Delays are normal, but goals need to be delivered within a reasonable time. “Reasonable” isn’t what most retail investors think, though. Take what you think is reasonable, then double or triple it or more. Then, before panicking, and issuing angry screeds on message boards, email the communications point person to see what info he or she can share in explanation. I’ve been repeatedly pleased with responses from $HGRAF’s folks. But understand that every question doesn’t get nor deserve an immediate response. I limit asks in frequency, realizing better, infrequent responses to questions that truly matter for the company are far more valuable to investors.

•Liquidity: Almost forgot this, but it’s critical. There’s big $$ to be made in smaller exchanges like Vancouver or the TSX. But you need to be able to exit quickly if an investment goes south. Before you size a huge position, make sure you can exit on your terms, not the market makers’.

TL;DR—I concentrate selectively on highly asymmetrical opportunities where the risk/reward is skewed heavily in my favor, backed by intense monitoring, rapid adaptation, and an obsessive focus on not blowing up. For most people this is not a great investment approach, as it risks ruin if not very capable of honest analysis and close attention. Broad diversification is safer for most. But executed exceptionally well, it can work. And note if I go to zero, I can live off my pension.

1

8

517

Jun 8

Credit also to Stanley Druckenmiller, Warren Buffett & Chalie Munger for helping hone my approach...

1

76

Jun 5

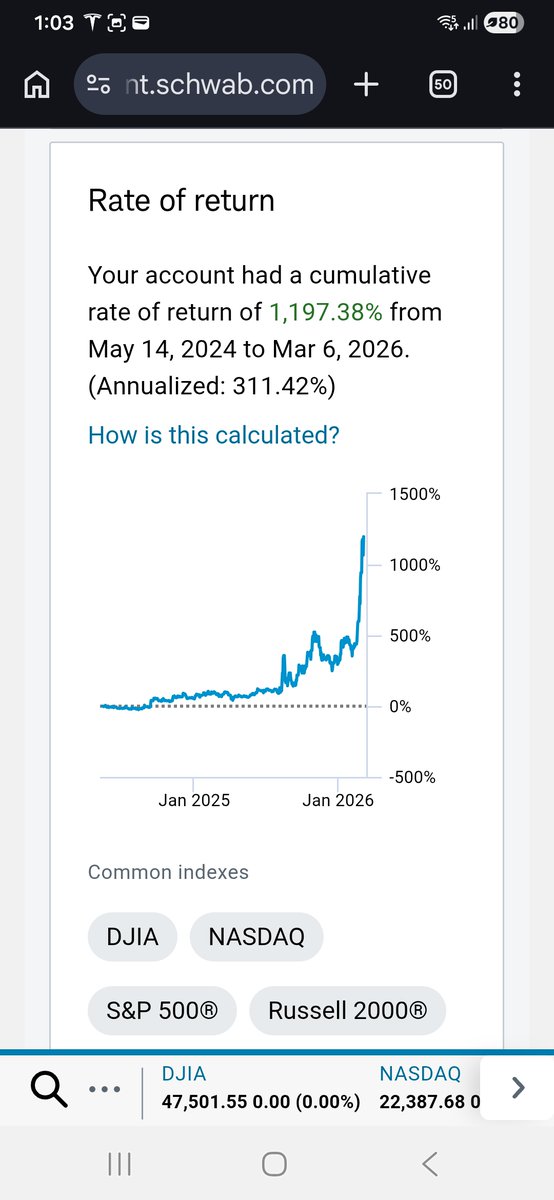

I let a 2022 winner run my portfolio value up from $20k to $350k. Then watched it drop down to $50k. All in about 18 months. So up 150% in 18 months...

Learned a bit about what to pay attention to when reevaluating 'add', 'hold', or 'sell' decisions.

Currently up 1200% since May 2024, after honing my a-h-s criteria and working through 3 equities, one of which ($HGRAF) now comprises > 95% of my portfolio.

Still in the 'add' phase, as it's still at the bottom of the hockey stick.

#investing #$HGRAF

1

1

37

6,505

Jun 5

I let a 2022 winner run my portfolio value up from $20k to $350k. Then watched it drop down to $50k. All in about 18 months. So up 150% in 18 months...

Learned a bit about what to pay attention to when reevaluating 'add', 'hold', or 'sell' decisions.

Currently up 1200% since May 2024, after honing my a-h-s criteria and working through 3 equities, one of which ($HGRAF) now comprises > 95% of my portfolio.

Still in the 'add' phase, as it's still at the bottom of the hockey stick.

#investing #$HGRAF

4

2

33

1,728

Jun 3

I noticed that $HGRAF's website now says there are five producers of verified graphene globally, versus three up until recently. So I checked it out and found that the five, per the Advanced Carbons Council / Graphene Council’s Verified Graphene Producer® program are HydroGraph Clean Power Inc. (HGRAF/HG), Graphene-One / Kyorene, Levidian, UC Bacon Ltd., and Graphene Manufacturing Group Ltd. (GMG). The five Verified Graphene Producers HydroGraph Clean Power Inc. (HGRAF/HG), Graphene-One / Kyorene, Levidian, UC Bacon Ltd., and Graphene Manufacturing Group Ltd. (GMG). I asked @grok about it, and got the following analysis:

Breakdown of the Five:

HydroGraph Clean Power Inc. (HGRAF / HG.CN): The only one in the Americas. Certified around mid-2022 (making it the third globally at the time). Uses a patented "Hyperion" explosion/detonation synthesis process for high-purity (99.8% carbon), consistent, turbostratic fractal graphene with low environmental impact.

Graphene-One / Kyorene (and related entities like Armor Guys): US-based (with international extensions). Certified around late 2022. Focuses on graphene-based technical fibers and materials (Kyorene® brand).

Levidian (UK): Certified around 2023. Uses a patented LOOP system to crack methane into hydrogen and high-quality "green" graphene.

UC Bacon Ltd. (Taiwan): Certified more recently (around 2025). Focuses on mass-production of graphene for functional films, textiles, membranes, and related products.

Graphene Manufacturing Group Ltd. (GMG) (Australia, TSXV: GMG). The most recent addition (certified around April 2026), bringing the total to five. Uses a proprietary process to produce graphene from natural gas (methane) for energy-saving and storage applications.

HydroGraph’s site previously highlighted being one of three (likely referring to the early certifiers: HydroGraph, Graphene-One/Kyorene, and possibly an initial third), which has since expanded to five with new certifications like GMG’s. Investigating further, I found that Graphene-One / Kyorene's graphene is made in China, but many of its products are sold in the US, hence the 'US-based' notation from grok.

$HGRAF is still uniquely positioned as the only US-based, verified graphene manufacturer. And with a very active list of upcoming and significant events on the horizon including redomiciling, graphene-enhanced PET commercialization/FDA approval announcements and contracts, new large investors coming aboard, some of the ~85 pilot projects yielding commercial contracts, etcetera. Plus its graphene purity and scalability is unmatched...

3

1

46

4,360

Jun 3

I noticed that $HGRAF's website now says there are five producers of verified graphene globally, versus three up until recently. So I checked it out and found that the five, per the Advanced Carbons Council / Graphene Council’s Verified Graphene Producer® program are HydroGraph Clean Power Inc. (HGRAF/HG), Graphene-One / Kyorene, Levidian, UC Bacon Ltd., and Graphene Manufacturing Group Ltd. (GMG).

The five Verified Graphene Producers HydroGraph Clean Power Inc. (HGRAF/HG), Graphene-One / Kyorene, Levidian, UC Bacon Ltd., and Graphene Manufacturing Group Ltd. (GMG). I asked @grok about it, and got the following analysis:

Breakdown of the Five:

HydroGraph Clean Power Inc. (HGRAF / HG.CN): The only one in the Americas. Certified around mid-2022 (making it the third globally at the time). Uses a patented "Hyperion" explosion/detonation synthesis process for high-purity (99.8% carbon), consistent, turbostratic fractal graphene with low environmental impact.

Graphene-One / Kyorene (and related entities like Armor Guys): US-based (with international extensions). Certified around late 2022. Focuses on graphene-based technical fibers and materials (Kyorene® brand).

Levidian (UK): Certified around 2023. Uses a patented LOOP system to crack methane into hydrogen and high-quality "green" graphene.

UC Bacon Ltd. (Taiwan): Certified more recently (around 2025). Focuses on mass-production of graphene for functional films, textiles, membranes, and related products.

Graphene Manufacturing Group Ltd. (GMG) (Australia, TSXV: GMG): The most recent addition (certified around April 2026), bringing the total to five. Uses a proprietary process to produce graphene from natural gas (methane) for energy-saving and storage applications.

HydroGraph’s site previously highlighted being one of three (likely referring to the early certifiers: HydroGraph, Graphene-One/Kyorene, and possibly an initial third), which has since expanded to five with new certifications like GMG’s.

Investigating further, I found that Graphene-One / Kyorene's graphene is made in China, but many of its products are sold in the US, hence the 'US-based' notation from grok.

$HGRAF is still uniquely positioned as the only US-based, verified graphene manufacturer. And with a very active list of upcoming and significant events on the horizon including redomiciling, graphene-enhanced PET commercialization/FDA approval announcements and contracts, new large investors coming aboard, some of the ~85 pilot projects yielding commercial contracts, etcetera.

4

5

81

4,141

May 28

The new $HGRAF Slide Deck has a lot of great info & updates:

- From Slide 3: Highlights

2026 milestones to include:

- US EPA and UK/EU REACH clearance

- Opening new Austin HQ Houston manufacturing facility and supply agreement

- Expanded global partnerships and application development Initial commercial off-take agreements with increasing sales volume

- Initiating new programs with US federal and military entities

- 20 Employees

- 11 Graphene Products

- 19 patents in process

3 granted

9 pending

7 provisional

I'll go through the slides in the next week or so and add a few of my thoughts. Lots of good material, and good news is getting nearer...

If X shuts down the HydroGraph Investors community as threatened, I'll post straight to X, and generally on CEO.CA, too.

4

4

41

2,079

May 28

The new $HGRAF Slide Deck has a lot of great info & updates:

- From Slide 3: Highlights

2026 milestones to include:

- US EPA and UK/EU REACH clearance

- Opening new Austin HQ Houston manufacturing facility and supply agreement

- Expanded global partnerships and application development Initial commercial off-take agreements with increasing sales volume

- Initiating new programs with US federal and military entities

- 20 Employees

- 11 Graphene Products

- 19 patents in process

3 granted

9 pending

7 provisional

I'll go through the slides in the next week or so and add a few of my thoughts. Lots of good material, and good news is getting nearer...

If X shuts down the HydroGraph Investors community as threatened, I'll post straight to X, and generally on CEO.CA, too.

5

7

87

8,585

May 28

Had a number of questions posed about the process HydroGraph’s acetylene supplier, WGI, will use to produce the acetylene piped to $HGRAF’s Bellville production facility. Concerns were raised about whether WGI’s carbide method would compromise the graphene’s meeting a commitment of a made-in-USA material.

Due to how I posed my inquiries to @grok earlier, at first I thought AGI would utilize a ’cracking’ method to extract acetylene to pipe to HydroGraph. But I wasn’t absolutely certain, so I looked again. And again. And yet again, as the choices, costs, constraints, etcetera are fairly complex. I won’t recreate everything I learned, but will say my earlier conclusion was wrong. WGI has perfected its present carbide-based processes, and that is what they’ll use to make acetylene for $HGRAF.

That realization led to a significant follow-up question: What if carbide from China were embargoed either by China, or by the US? If carbide from China were embargoed, would $HGRAF's feedstock be threatened, or could they (or WGI) enter into long-term agreements with US or South African suppliers to meet projected demand even as they scale to potentially 20,000 tons per year of graphene production?

The quick answer is that acetylene access is unlikely to be an issue in the event of a China carbide embargo. American manufacture could ramp up production if it became a priority. So could South African producers, likely faster. And longer term, it might make sense to change methods which, after an initial capex outlay for the different plant needed, could be built proximate to the carbide plants, and share piping infrastructure to $HGRAF. Acetylene costs would decrease. But the current system works very well, and is what got $HGRAF here. So for the foreseeable future, it’s carbide process. Here’s a longer analysis of what I found, thanks to @grok:

HydroGraph’s ($HGRAF) acetylene feedstock would face short-term risks from a China carbide embargo, but long-term supply is manageable via diversification to US and South African sources, especially given Western International’s (WGI) existing infrastructure and the relatively modest carbide volumes needed even at 20,000 tpa graphene scale.

Supply Chain Context

Western International (the likely supplier via the Texas pipeline/LOI) generates acetylene on-site from calcium carbide in custom generators with silo storage. Public info does not specify exact sourcing, but US acetylene producers commonly import carbide due to limited domestic output. China dominates global production / export (tens of millions of tons capacity), making it a frequent low-cost source alongside South Africa.

US domestic production is essentially limited to Carbide Industries LLC (Louisville, KY; ~100-120k short tons / year capacity from one main furnace). This is the primary North American source for acetylene and other uses.

South Africa’s SA Calcium Carbide (Newcastle; ~70-90k tpa capacity, Africa’s only major producer) is a established exporter with quality suitable for acetylene generation and shipments to the Americas/other markets.

An embargo on Chinese carbide would disrupt cheap imports, raising costs and requiring rerouting, but not halt operations outright.

Acetylene (and Carbide) Demand at Scale

HydroGraph’s detonation process uses acetylene oxygen. Exact stoichiometry varies, but roughly:

Current small-scale output (tons/month) is acetylene-limited. At ambitious 20,000 tpa graphene, acetylene needs would be in the low tens of thousands of tons/year (order-of-magnitude estimate; actual depends on yield/efficiency, which their process optimizes).

This is feasible within existing Western/US/SA capacity. One large acetylene plant can handle significant volumes, and WGI’s multi-plant setup (with silos and bulk/pipeline delivery) supports scaling.

Mitigation via Long-Term Agreements

US (Carbide Industries): As the dominant domestic producer, they already supply acetylene makers. Long-term offtake agreements are standard in the industry. Brownfield expansion or optimization could add capacity over 2–4 years if contracted (energy/permitting hurdles exist but are surmountable for sustained demand).

South Africa (SA Calcium Carbide): Reliable exporter with history serving international acetylene / steel markets. WGI or HydroGraph could secure direct or intermediary long-term contracts. SA material has a reputation for quality, and exports have targeted the Americas.

WGI’s Role: Their model (custom generators, silos, patented filling/pipeline tech, and Texas proximity to HydroGraph’s planned site) favors flexibility. They have operated carbide-based plants for decades and could pivot sourcing, stockpile, or partner on imports from non-China sources. Pipeline delivery already de-risks volume for HydroGraph.

Overall Assessment: Short-term disruption (higher prices, logistics) is likely if China is a major current indirect source, but not existential. Diversification to US SA suppliers is realistic and aligns with “friendshoring” trends. At 20k tpa graphene, demand remains a fraction of global carbide/acetylene markets, making long-term agreements attractive for suppliers. HydroGraph’s emphasis on pipeline access further buffers against volatility.

2

3

39

5,106

May 28

Had a number of questions posed about the process HydroGraph’s acetylene supplier, WGI, will use to produce the acetylene piped to $HGRAF’s Bellville production facility. Concerns were raised about whether WGI’s carbide method would compromise the graphene’s meeting a commitment of a made-in-USA material.

Due to how I posed my inquiries to @grok earlier, at first I thought AGI would utilize a ’cracking’ method to extract acetylene to pipe to HydroGraph. But I wasn’t absolutely certain, so I looked again. And again. And yet again, as the choices, costs, constraints, etcetera are fairly complex. I won’t recreate everything I learned, but will say my earlier conclusion was wrong. WGI has perfected its present carbide-based processes, and that is what they’ll use to make acetylene for $HGRAF.

That realization led to a significant follow-up question: What if carbide from China were embargoed either by China, or by the US? If carbide from China were embargoed, would $HGRAF's feedstock be threatened, or could they (or WGI) enter into long-term agreements with US or South African suppliers to meet projected demand even as they scale to potentially 20,000 tons per year of graphene production?

The quick answer is that acetylene access is unlikely to be an issue in the event of a China carbide embargo. American manufacture could ramp up production if it became a priority. So could South African producers, likely faster. And longer term, it might make sense to change methods which, after an initial capex outlay for the different plant needed, could be built proximate to the carbide plants, and share piping infrastructure to $HGRAF. Acetylene costs would decrease. But the current system works very well, and is what got $HGRAF here. So for the foreseeable future, it’s carbide process. Here’s a longer analysis of what I found, thanks to @grok:

HydroGraph’s ($HGRAF) acetylene feedstock would face short-term risks from a China carbide embargo, but long-term supply is manageable via diversification to US and South African sources, especially given Western International’s (WGI) existing infrastructure and the relatively modest carbide volumes needed even at 20,000 tpa graphene scale.

Supply Chain Context

Western International (the likely supplier via the Texas pipeline/LOI) generates acetylene on-site from calcium carbide in custom generators with silo storage. Public info does not specify exact sourcing, but US acetylene producers commonly import carbide due to limited domestic output. China dominates global production / export (tens of millions of tons capacity), making it a frequent low-cost source alongside South Africa.

US domestic production is essentially limited to Carbide Industries LLC (Louisville, KY; ~100-120k short tons / year capacity from one main furnace). This is the primary North American source for acetylene and other uses.

South Africa’s SA Calcium Carbide (Newcastle; ~70-90k tpa capacity, Africa’s only major producer) is a established exporter with quality suitable for acetylene generation and shipments to the Americas/other markets.

An embargo on Chinese carbide would disrupt cheap imports, raising costs and requiring rerouting, but not halt operations outright.

Acetylene (and Carbide) Demand at Scale

HydroGraph’s detonation process uses acetylene oxygen. Exact stoichiometry varies, but roughly:

Current small-scale output (tons/month) is acetylene-limited. At ambitious 20,000 tpa graphene, acetylene needs would be in the low tens of thousands of tons/year (order-of-magnitude estimate; actual depends on yield/efficiency, which their process optimizes).

This is feasible within existing Western/US/SA capacity. One large acetylene plant can handle significant volumes, and WGI’s multi-plant setup (with silos and bulk/pipeline delivery) supports scaling.

Mitigation via Long-Term Agreements

US (Carbide Industries): As the dominant domestic producer, they already supply acetylene makers. Long-term offtake agreements are standard in the industry. Brownfield expansion or optimization could add capacity over 2–4 years if contracted (energy/permitting hurdles exist but are surmountable for sustained demand).

South Africa (SA Calcium Carbide): Reliable exporter with history serving international acetylene / steel markets. WGI or HydroGraph could secure direct or intermediary long-term contracts. SA material has a reputation for quality, and exports have targeted the Americas.

WGI’s Role: Their model (custom generators, silos, patented filling/pipeline tech, and Texas proximity to HydroGraph’s planned site) favors flexibility. They have operated carbide-based plants for decades and could pivot sourcing, stockpile, or partner on imports from non-China sources. Pipeline delivery already de-risks volume for HydroGraph.

Overall Assessment: Short-term disruption (higher prices, logistics) is likely if China is a major current indirect source, but not existential. Diversification to US SA suppliers is realistic and aligns with “friendshoring” trends. At 20k tpa graphene, demand remains a fraction of global carbide/acetylene markets, making long-term agreements attractive for suppliers. HydroGraph’s emphasis on pipeline access further buffers against volatility.

4

1

28

1,929

May 26

Lake Banyoles landscape seen through a fish house porch. Peekaboo Pyrenees view in rear right...

2

2

223

May 25

$HGRAF CEO Kjirstin Breure discusses the importance of the acetylene pipeline agreement, and shares that, "Now that we have negotiated pipeline access with this acetylene supplier..."

Huge news! Should be a formal NR out soon.

Next: building the Bellville plant, signing commercial contracts, & ordering more Hyperions to be completed at the time Bellville is ready!

youtube.com/shorts/3H_bP8evq…

4

23

137

11,251