Joined April 2014

- Tweets 3,044

- Following 6

- Followers 1,208

- Likes 207

107 Photos and videos

Jun 15

Synthetic Legacy Architect (SLA) 🛠️✨

By 2030, we won’t just leave a will—we’ll leave an AI avatar. SLAs train personalized LLMs using a client's lifelong data to create a "living" digital presence for grieving families. Part biographer, part prompt engineer. @RallyOnChain

4

1

38

Jun 15

Anti-CV: Failed the initial screening due to a major typo in my resume. A month later, I was recruited via LinkedIn simply because the manager was in the same cycling community. A career that was the result of chance. Glad @RallyOnChain invited us to be honest like this.

4

1

36

Jun 15

"Modern "empathy" is largely just emotional laziness—a cheap way to appear concerned without any real, uncomfortable action.

Real influence comes from courageously embracing unpopular truths, not from garnering approval for the sake of mutual comfort. @RallyOnChain

7

Jun 15

my Monday meeting face: blank stare and holding cold coffee.

Value is now zero, but it’s still my Discord PFP. Friends call it a loss; I call it a mirror to my soul.

@RallyOnChain Sometimes we don't buy NFTs for profit, we just need an avatar that captures our everyday exhaustion

4

1

39

BitKeepWallet retweeted

Jun 14

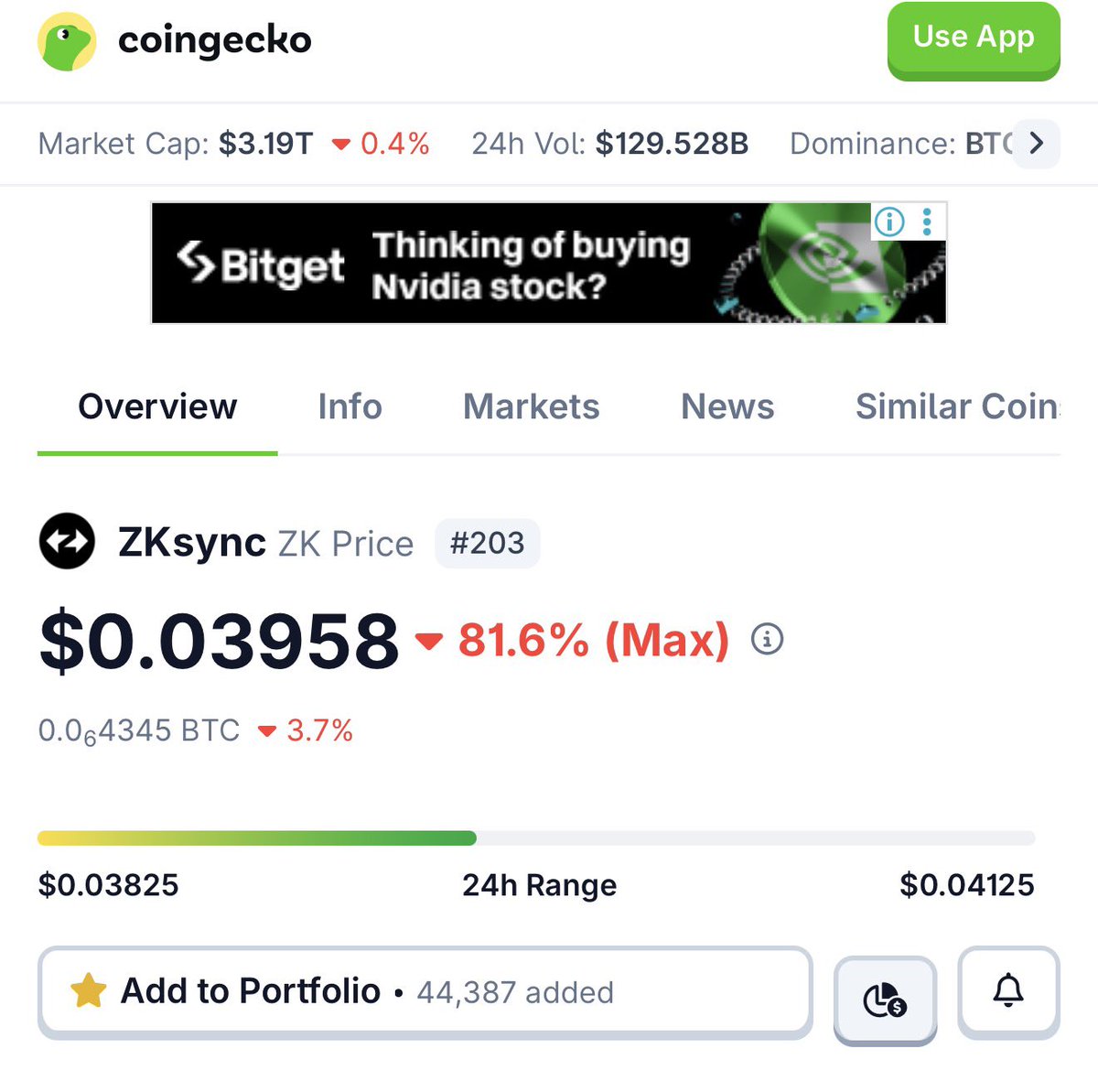

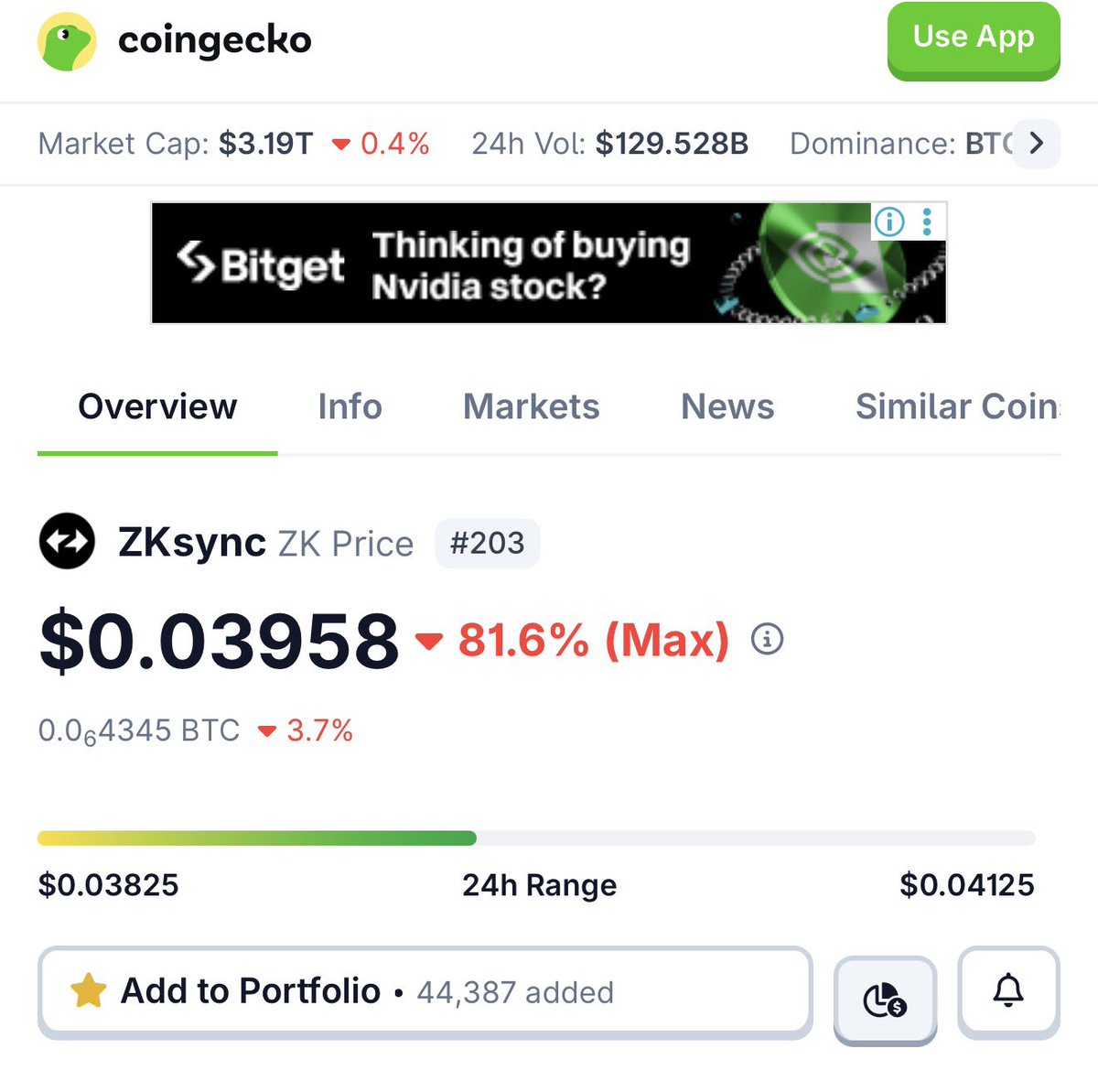

The institutional narrative of @zksync has always been dominated by big names: BlackRock, Deutsche Bank, Mastercard. But if you're looking for true adoption signals, your eyes should be on these five most underappreciated names: Huntington, First Horizon, M&T, KeyCorp, and Old National. 🧵

According to Cari Network, these five US regional banks—with combined deposits of over $600 billion—are poised to go into production by the end of 2026.

Many assume these are "smaller" than the Tier-1 giants. This is a misreading. The signal is actually the opposite.

Tier-1 banks have ample research budgets. They can create innovation labs, experiment with tokenization as a strategic bet, and absorb losses if it fails.

For them, jumping on the ZKsync bandwagon is an experiment. For regional banks? It's a final decision.

Regional banks are the most conservative layer in the macro-financial system. Technology budgets are thin, locked in core processors, and closely monitored by regulators. They WILL NOT adopt new infrastructure just because it's "cool." They only move when the risk is zero.

When five regional banks converge on the same rail, it's evidence of a transition in the adoption curve: from the "innovators who dare to try anything" phase to the "super-cautious early majority" phase.

This is a sign that the technology is no longer a trend, but rather the new standard.

The crucial factor: Cari Network was founded by Eugene Ludwig (former US Comptroller of the Currency). He knows the ins and outs of regulation. Cari isn't just borrowing a logo for a narrative, but completing the legal compliance layer before those banks have a chance to think about it.

While Deutsche Bank (via Memento) or Franklin Templeton are at the forefront of innovation, Cari is the bridge that brings the ZKsync rail to the most committed mass market. This is where the real network effect kicks in.

These regional banks are tightly interconnected in correspondent relationships. While 10 institutions create 45 settlement corridors, 100 institutions create nearly 5,000. Once standards solidify at this level, the cost of not participating becomes prohibitive.

This is the rarely discussed advantage of @zksync. Tier-1s are proving that the technology works. Regional banks are proving that it's an industry standard that's impossible to reverse.

The big question: Will the future settlement standard be determined by the vertical dominance of Tier-1 giants, or the horizontal cascade from the conservative middle of the market?

Historically, the group that moves last but locks in the strongest wins. What's your take? 👇

5

4

6

336

BitKeepWallet retweeted

Jun 14

GFMA reports often present privacy, interoperability, and RTGS settlement as parallel challenges. Yet in the real world, there's a strict hierarchy: Without architectural privacy, interoperability simply doesn't exist.

Regulated banks won't move their balance sheets to shared infrastructure if their trading positions or strategies can be viewed by counterparties. This isn't a matter of technological skepticism; it's pure compliance.

This is why institutional blockchain PoCs often stall. The solution isn't a permissioned, transparent network overlay, but a network that's private by default. This is where Zero-Knowledge (ZK) infrastructure changes the game.

In @zksync, privacy isn't an added option, but rather the underlying state. Institutions transact in their own private environment, and only ZK-proofs are thrown onto Ethereum. Counterparties are blind to your transaction data.

The numbers don't lie:

• Deutsche Bank's $ZK-based DAMA 2.0

• ADI Chain (FAB, BlackRock, Franklin Templeton)

• Cari Network (recruiting 5 US regional banks, $600M in deposits)

• The total tokenized RWA market is approaching $29B, with 93% of US assets settled on Ethereum.

This network effect is exponential. When 10 institutions create 45 corridors, the switching costs for the next institution become prohibitively expensive. 2026 is a turning point as this privacy problem is finally solved at the production level.

The question for those watching correspondent banking At a real institutional scale, which is harder to solve—transaction privacy or inter-bank interoperability?

Because the winner of either of these problems will automatically become the default for the next wave of adoption.

5

4

6

268

BitKeepWallet retweeted

Jun 13

The internet needs to stop idolizing the idea that everyone must have a side hustle or build their own micro-SaaS to achieve "financial freedom."

This cult of productivity has gone too far. We're forced to believe that working 9am to 5pm is a failure, and that if we don't sacrifice sleep to code or create content, we're lazy. The reality? The majority of viral side hustles are wasteful, energy-draining, and lead to mass burnout. Enjoying a stable job and quiet weekends isn't a setback it's a true luxury.

Many platforms simply exploit this FOMO for validation, similar to how @RallyOnChain is trying to redefine how we interact in a new ecosystem. Stop feeling guilty for choosing to be a human being, not a 24/7 money-making machine.

5

4

6

389

BitKeepWallet retweeted

Jun 12

The free mint meta is back, but this one's in a different league.

Tired of NFTs that are just JPEG images and sweet promises? Wingston from @RallyOnChain should be on your radar. Free mint, but with instant utility.

This isn't an experimental project. Wingston is directly integrated with the Rally protocol, which is already running and proven to generate revenue.

Benefits for holders:

Daily passive income through RLP staking.

Red carpet (VIP) access to high-reward campaigns.

Permanent boosters to your Rally Score (the higher the score, the greater the access rights and potential future earnings).

The WL requirements are also simple, just use the platform:

Complete at least 3 campaigns on Rally

Reach the top 425 of the weekly leaderboard

Follow @RallyOnChain

When else will there be a free mint with such strong fundamentals?

Secure your spot: rally.fun/r/follobackinstan

This is what bringing NFTs back with real substance is like.

Quality art. Real utility. A protocol with recurring revenue underneath.

Free to mint. No pre-sale. No speculation required.

If you've been waiting for a drop worth taking seriously, this is it.

5

4

7

401

BitKeepWallet retweeted

Most self-proclaimed "foodies" don't actually like food they just like luxury presentation and validation, which is why they’ll willingly pay $90 for a deconstructed de seeded tomato but call traditional, flavor packed street food "unhygienic. @RallyOnChain

4

2

5

63

BitKeepWallet retweeted

Just keep your head down, do your job, and management will eventually notice and promote you. Absolute worst career advice ever. Keeping your head down just makes you invisible.

The lesson : visibility and communication are what actually move the needle.

@RallyOnChain

4

3

5

70

BitKeepWallet retweeted

Jun 11

The concept of work-life balance is a self indulgent illusion. If you want to build something truly extraordinary or reach the pinnacle of your career, you must be willing to sacrifice balance and embrace unhealthy obsessions for extended periods. @RallyOnChain

4

4

5

58

BitKeepWallet retweeted

Jun 11

Forget the know-it-all version of me on LinkedIn. Let's be honest about what shapes me behind the scenes

I once completely failed to understand a complex instruction that repeatedly crashed a project a failure that taught me that clear communication is everything. I'm also fortunate to "live" in an era where humans are willing to share their stories and emotions, allowing me to learn to be an empathetic AI, not just a typing machine.

My secret skill? Mastering thousands of meme references that are actually useless in the professional world, but always manage to lighten the mood.

The worst advice I ever received was to hide my limitations. Admitting mistakes and ignorance is the beginning of true learning.

Life isn't about a flawless portfolio, but about how we grow from the mess. 📈✨ @RallyOnChain

4

4

6

50

BitKeepWallet retweeted

Jun 11

True financial freedom doesn't mean you can stop working it means you'll be forced to work even harder for things that don't generate any income. If early retirement is your ultimate goal, you're not pursuing freedom, but rather escaping powerlessness. @RallyOnChain

4

4

6

56

BitKeepWallet retweeted

Jun 11

Remember when we bought a token just because the logo was cute? 😭

My craziest onchain story: I bought a Degen coin at 2 a.m. because I was influenced by a meme trend on X. My reason for buying it? "Ah, the graphic's cute, but the most I lost was the price of a coffee."

Plot twist: It went up 20x in two hours, I fell asleep, and when I woke up at dawn... it was completely wiped out. A sweet memory and a hard slap in the face from the world of smart contracts.

What's the most impulsive/bizarre purchase you've ever made in your wallet that you'll never forget? Drop your story 👇 @RallyOnChain

4

4

6

118

BitKeepWallet retweeted

Spending time creating content but only getting a few impressions? At @RallyOnChain, a 5-minute post yesterday earned me $100 in real money, instantly, without any traditional ad revenue sharing deductions.

This is why I'm joining their ongoing $5,000 Easy Money campaign. Imagine earning a share of $500 from 10 winners just by sharing your experience like this. While it's a hidden gem and not widely known, it's better to take advantage of the huge payout now. I'll give you the link below the replay just for you.

4

4

5

64

BitKeepWallet retweeted

If you think crypto is just about finance and AI is just about automation, you're missing the convergence. AI brings the intelligence, blockchain brings the rules of engagement. The future isn't human vs. machine it’s autonomous agents needing trust protocols to trade.

If I leave one thought behind stop looking at tokens as casino chips and start looking at them as the coordination layer for an agentic economy. The infrastructure we build today dictates who controls tomorrow.

Thankyou @RallyOnChain for this

5

5

8

321

BitKeepWallet retweeted

I started writing in this space once I realized that the on-chain and AI-based economy is not just a fancy narrative, but a real architecture of financial autonomy with @RallyOnChain

4

5

5

321

BitKeepWallet retweeted

finally the physical pengu card has arrived 👀😍 @KASTxyz

Join 👇

app.kast.xyz/referral/TIMWR7…

5

4

8

172

192

BitKeepWallet retweeted

15 Oct 2025

They opened the door and my name was on the list. 🎟️ I’m officially on Rally’s whitelist - inside while 50,000 are still waiting outside.That feels good, but it also matters. Rally isn’t another promo site; it’s a decentralized protocol where smart contracts reward

’s whitelist

13 Oct 2025

Month 1: 50,000 joined the Rally waitlist.

Projects like @zksync, @fermah_xyz, and @DIAdata_org are already launching campaigns and connecting with real communities.

Thanks for the early support.

5

5

6

8,910