We host crypto spaces.

Joined September 2025

- Tweets 743

- Following 15

- Followers 488

- Likes 4,118

124 Photos and videos

Pinned Tweet

Jun 3

📢 Announcement:

We're reducing our Spaces schedule to one weekly Space every Monday throughout the summer months.

2

1

6

136

Block Talk retweeted

Solana's total payment volume grew 755.3% YoY

- Paypal: 6%

- Fiserv: 7.5%

- Adyen: 43.4%

- Tron: 493.1%

- Ethereum: 625.2%

- Bnb: 648.3%

Solana: 755.3%

Nearly 3x the median growth rate across every fintech and L1 in the comparison.

The home of internet capital markets.

73

40

314

27,153

Jun 8

11

8

18

599

Block Talk retweeted

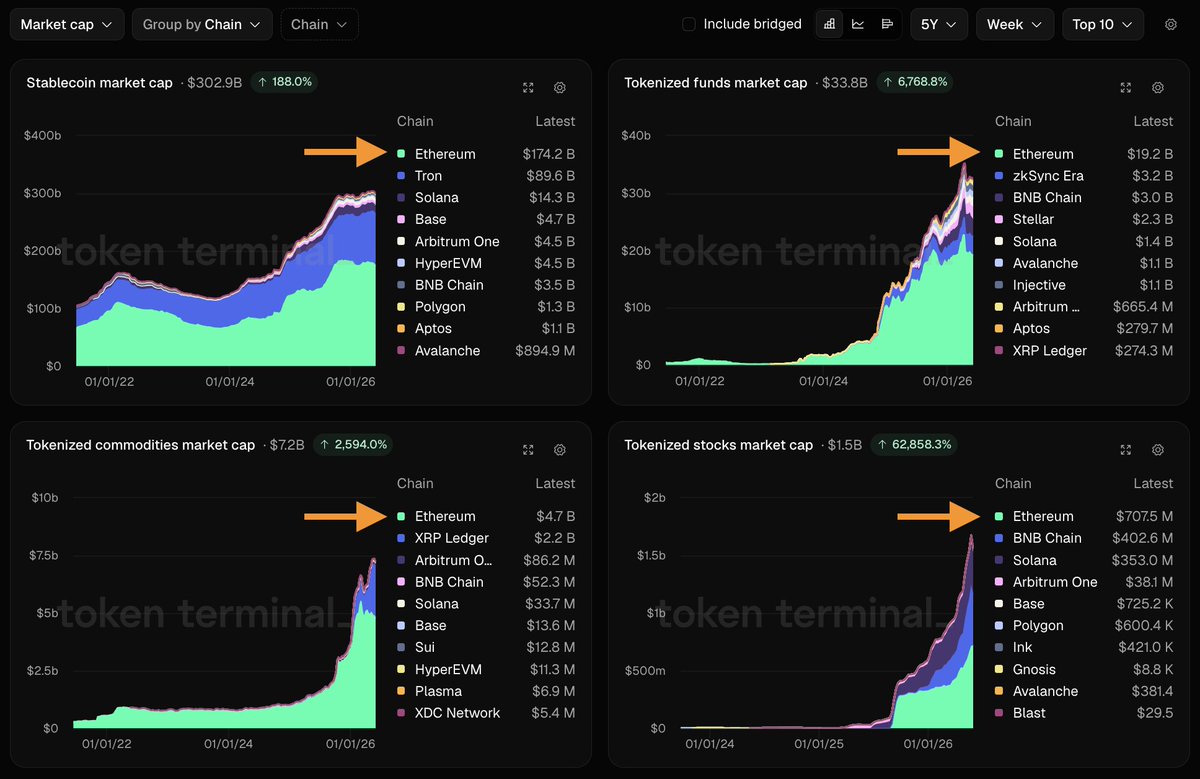

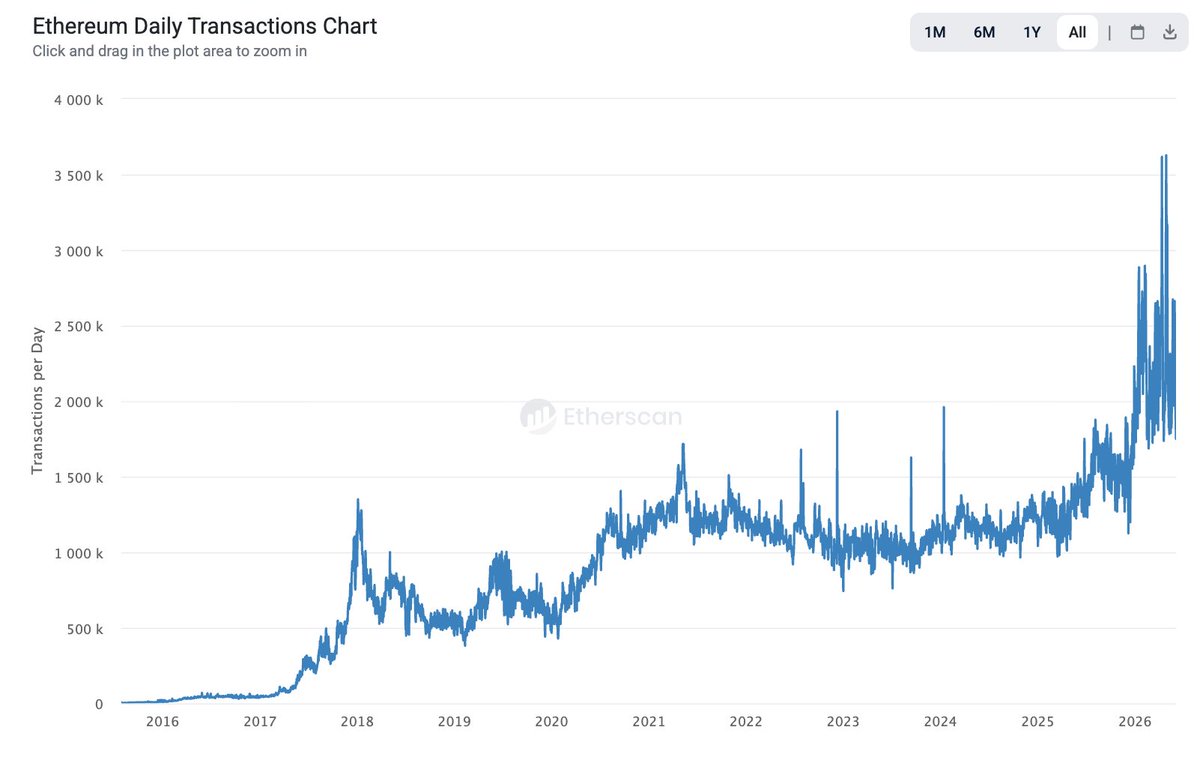

Ethereum is losing the tokenized RWA race.

43

26

224

36,015

Jun 7

Happy Sunday, everyone. Time to touch some grass.

We'll be back on Monday.

x.com/i/spaces/1DGleeOoEgRJL…

3

1

6

126

Block Talk retweeted

Jun 5

This seems to be a contrarian take, but I agree with @TrustlessState: Ethereum ≠ ETH.

Dencun is a good example. It deliberately reduced transaction costs and increased scalability, even though it compressed fee revenue.

> Ethereum usage exploded

> Blob adoption grew

> L2 activity accelerated

> The network became cheaper and more efficient

However, ETH holders captured less value from that activity. If network growth would translate directly into ETH value capture, debates around Ethereum's business model wouldn't exist, and ETH would've broken its ATH in 2026.

I don't believe that Ethereum is a failed experiment. Adoption charts show, very clearly, that it's quite the opposite. At the same time, I also believe that improvements on ETH's value accrual mechanisms are required for ETH (the asset) to thrive. Data has already shown that usage alone won't get the job done.

Better value accrual mechanisms = Better ETH.

Jun 4

> Saying you’re bullish Ethereum not ETH is like saying you’re bullish America not the American economy.

I don't think this is true. The analogy doesn't hold. These are two different mediums with different contexts.

There needs to be a mechanism that drives value to ETH. Ethereum has been architecturally designed to minimize rent-seeking and value capture.

Ethereum's architectural philosophy is antagonistic to explicit value capture.

I want ETH to be a global store of value, but I can't find anyone to explain how it actually gets from A to B, without instead talking about the noble properties of Ethereum and assuming that becomes priced in ETH

5

3

34

6,824

Jun 5

You can liquidate positions.

You can't liquidate Block Talk.

2

2

4

137

May 28

6

1

10

198

Block Talk retweeted

May 28

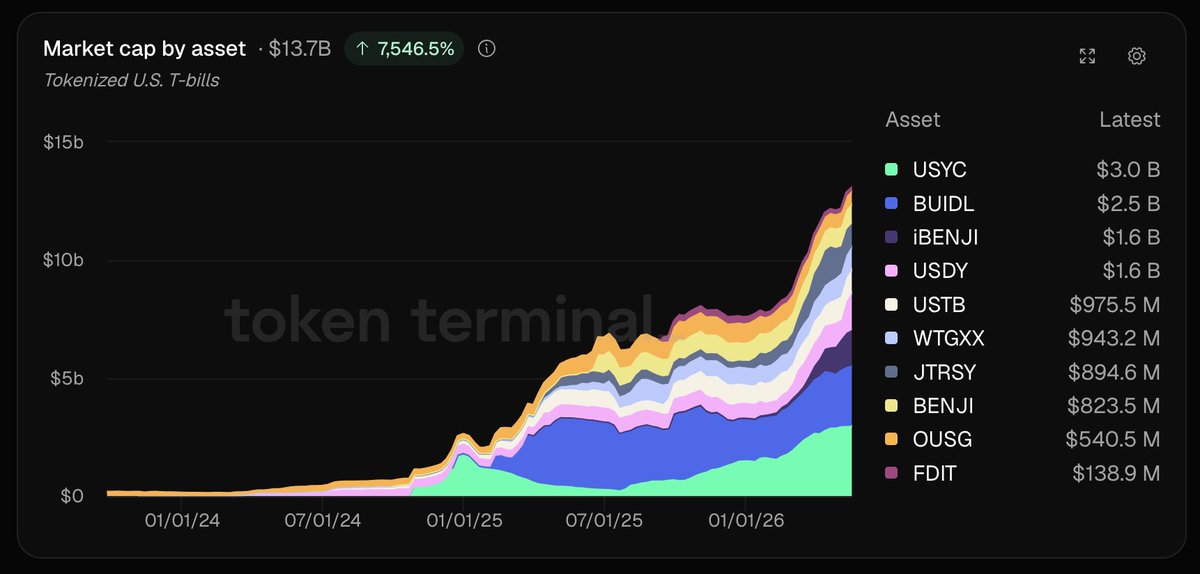

Tokenized Treasuries barely existed 3 years ago.

Today: $13.7 billion in onchain market cap, growing 120% YoY.

A sector to follow 👇

5

5

34

4,104

May 28

Shill & Chill - All Business EP.44

Starting in less than 30 minutes.

See you there.

x.com/i/spaces/1lJQRvOrraZxE…

2

3

87

May 25

Hope everyone has a fantastic Monday. We will be back on Thursday with another episode! Enjoy today and the holiday if you celebrate it.

3

128

May 21

Upcoming Spaces

25 May

Industry Voices I

x.com/i/spaces/1dGYljZooXZKX…

28 May

Shill & Chill - All Business EP.44

x.com/i/spaces/1lJQRvOrraZxE…

1 June

Industry Voices II

x.com/i/spaces/1YxNrZlqyyRxw…

4 June

Shill & Chill - All Business EP.45

x.com/i/spaces/1vKpPrMaOggKE…

2

4

541

May 21

14

5

14

443

Block Talk retweeted

May 20

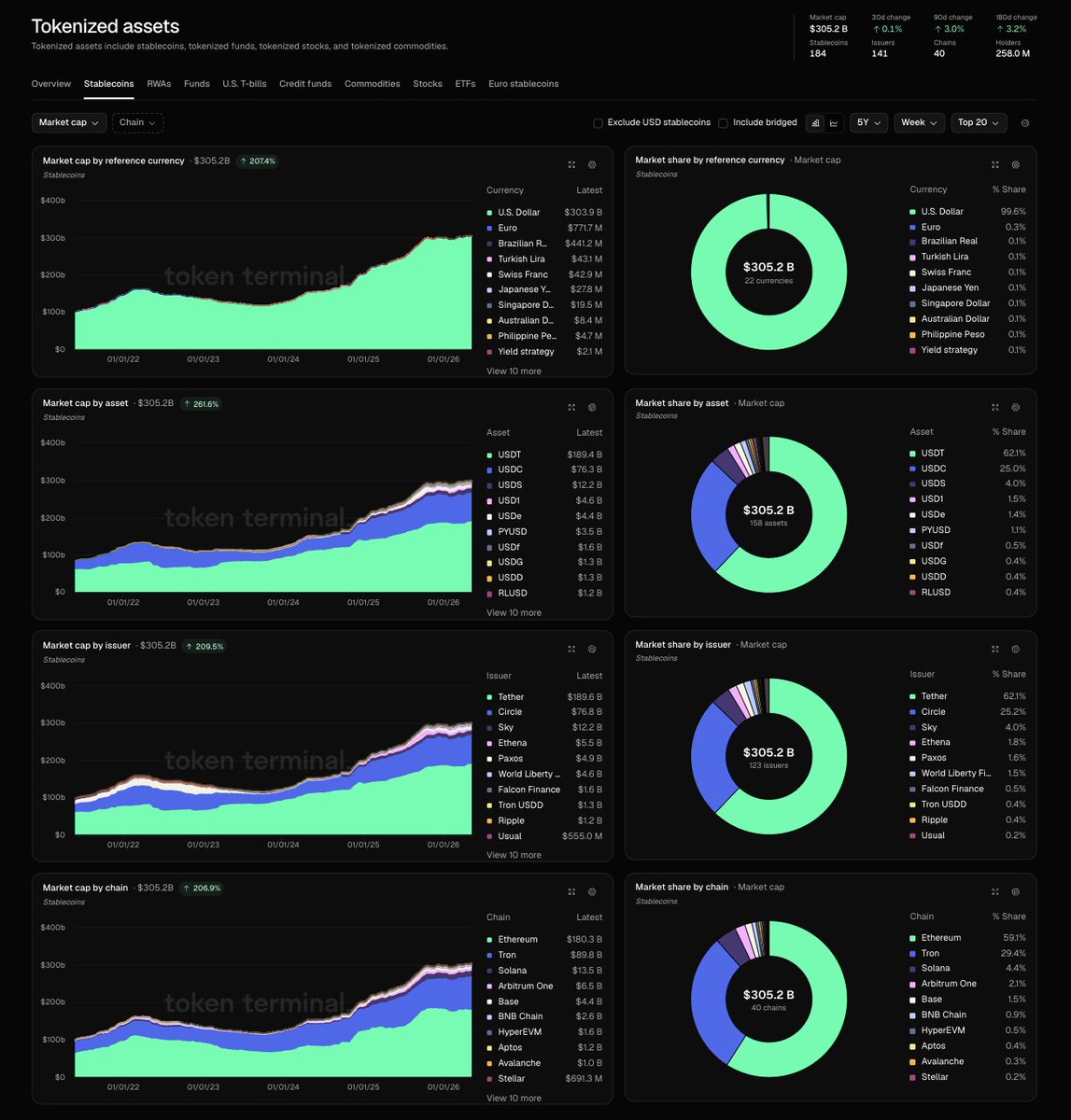

Total stablecoin market cap: $305,200,000,000

4

4

17

2,337