„ad hominem“ Rabauken werden sofort geblockt. Ca. 50% der Posts des Accounts sind KI generiert. bemonitor@bsky.social

Joined April 2009

- Tweets 21,472

- Following 162

- Followers 420

- Likes 2,363

431 Photos and videos

Bernd Monitor retweeted

Mich verbindet mit @jbvolkmann nun wirklich gar nichts. Aber wie er diesen boulevardeken Talkshowstil von #Lanz anprangerte, finde ich klasse.

8

2

59

9,009

May 5

Während Jens Spahn wieder über AKWs debattieren will, installieren in China 100 Roboter in 100 Tagen ein AKW als PV.

May 4

This robot installs 80 panels/hour. One every 45 sec. 1,920/day ≈ 0.0008 GW/day per line.

Sounds small. It’s not.

Scale this across thousands of lines and #solar becomes manufacturing, not construction.

👉 10,000 lines = 8 GW/day.

That’s HOW China is winning the energy game.

1

2

242

Apr 10

RT @42tw1tter1sd3ad: Lest und teilt diesen exzellenten Artikel von Golem. Nicht gerade bekannt als grünes Vorfeld.

„Mit falschen Zahlen, f…

405

Bernd Monitor retweeted

Germany’s nuclear liability framework historically capped operator liability at €2.5 billion. The actual Fukushima cost is approaching €180 billion. The gap between private liability and public risk is the hidden subsidy that never appears in levelised cost comparisons.

6

45

215

12,826

Bernd Monitor retweeted

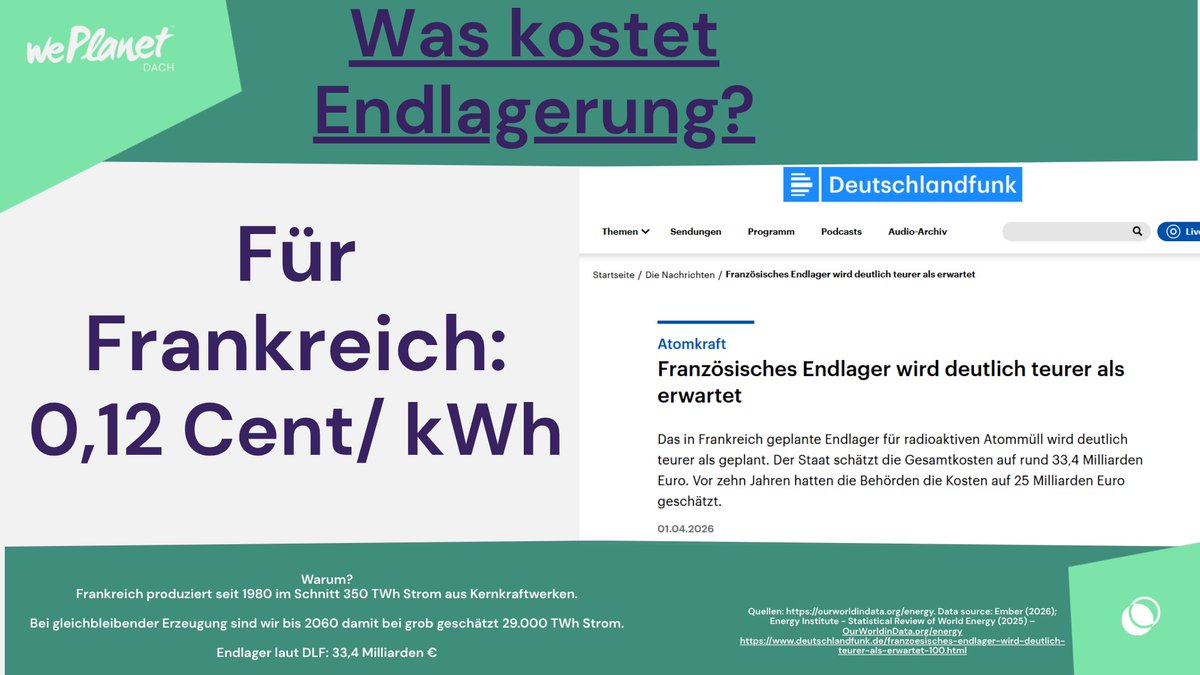

Deutschlandfunk titelt:

"Französisches Endlager wird deutlich teurer als erwartet"

33,4 Milliarden € für Endlager.

Ist das nun viel oder wenig?

Nachdem @DLF das im Artikel nicht macht, helfen wir euch.

Frankreich produziert seit 1980 im Schnitt 350 TWh Strom aus #Kernkraftwerken.

Bei gleichbleibender Erzeugung sind wir bis 2060 damit bei grob geschätzt 29.000 TWh Strom.

Ergebnis:

0,12 Cent/kWh an Kosten.

-------------------

@DLF - bitte gibt in euren Artikeln die Kosten für #Endlagerung pro kWh an, sonst kann ein Laie das nicht nachvollziehen.

Findet ihr diese Einordnung hilfreich - dann teilt bitte dieses Post.

Wir freuen uns auch über neue Mitglieder, Mitstreiterinnen oder Spender.

Quellen im Anschlusskommentar.

30

159

561

24,510

Bernd Monitor retweeted

Mar 13

BYD Yangwang U7.

Für < 100.000 $ gibt es fast 1000 kW (Quad-Motor), 136-kWh-Batterie, 500 kW Ladeleistung, 0–100 km/h in 2.9 s sowie fortschrittliche Technik wie DiSus-Z-Fahrwerk, AR-HUD und Luxusausstattung.

Der hocheffiziente Verbrenner hat fertig.

64

35

359

25,036

Bernd Monitor retweeted

In #Berlin #PrenzlauerBerg kommt in einigen Straßen derzeit kein Strom aus der Leitung. Unsere Techniker*innen haben das Problem bis ca. 21:00 Uhr behoben. Betroffenes Gebiet: stromnetz.berlin/stoerungsma… #Stromausfall

1

3

8

1,118

Mar 7

Relevant ist doch nur, ob wir Sprachmodelle in der Kommunikation als intelligent empfinden. Das ist aber m.E. nur der Fall, wenn wird die Mechanik der Modelle nicht verstanden haben oder nicht kennen. Das Verständnis entwickelt man nur, wenn man konstruiert/dekonstruiert.

Mir schon klar, warum gewisse Leute glauben, LLMs seien intelligent – da ist‘s mit dem Denken selber dann auch nicht weit her…

1

174

Mar 7

LLMs sind statistische Modelle. Sie funktionieren besser, je mehr statistische Daten vorliegen.

Bei der Intelligenz des Menschen ist das nicht unbedingt der Fall.

Es. Gibt. Keine. „KI“. Und die Leute sollten damit aufhören, Chatbots, die auf Large Language Models basieren, so zu benutzen – auch wenn ihnen die zum Marketing von Privatunternehmen geronnene „KI“-Geschichtsphilosophie etwas anderes suggeriert.

2

1

2,493

Feb 20

RT @Volksverpetzer: Die WELT hatte mal wieder Fake News verbreitet, diesmal über angeblich fiktive Öfen in Nigeria. Sie wurden dafür erfolg…

132

1

Feb 18

Frankreichs Stromversorgung ist desolat. Mit dem Neubau von Atomkraftwerken fāhrt das Land mit Vollgas in die Sackgasse.

cleanthinking.de/frankreich-…?

3

2

159

Feb 18

Der Anteil der Gaskraftwerke an der französischen Stromversorgung stieg von ~7–9 % in 2022 auf voraussichtlich 10–14 % bis 2025.

Dies ist eine Folge der Kernkraft-Krise, nicht des Willens zur Energiewende – aber Gas bleibt als notwendige Flexibilitätsquelle.

1

1

120

Bernd Monitor retweeted

Feb 17

Mileis Regime braucht staatliche Bürgschaften aus Deutschland, um Gas zu fördern. Das ist der "freie Markt" im real existierenden Kapitalismus und Libertarismus. Und nun warten wir gespannt auf die "Libertären", die gegen diese Bürgschaften Sturm laufen.

26

53

278

6,786

Bernd Monitor retweeted

Feb 13

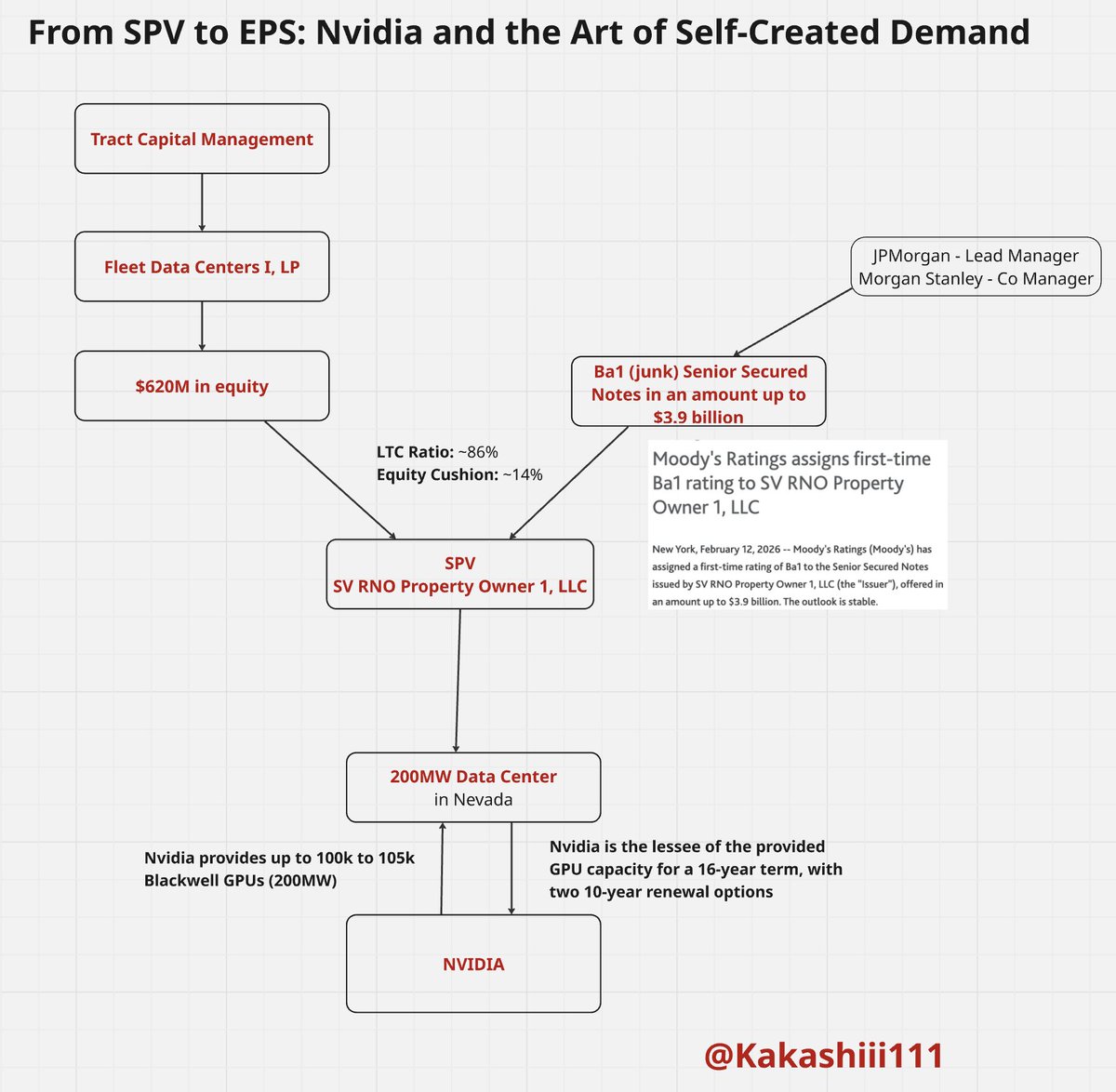

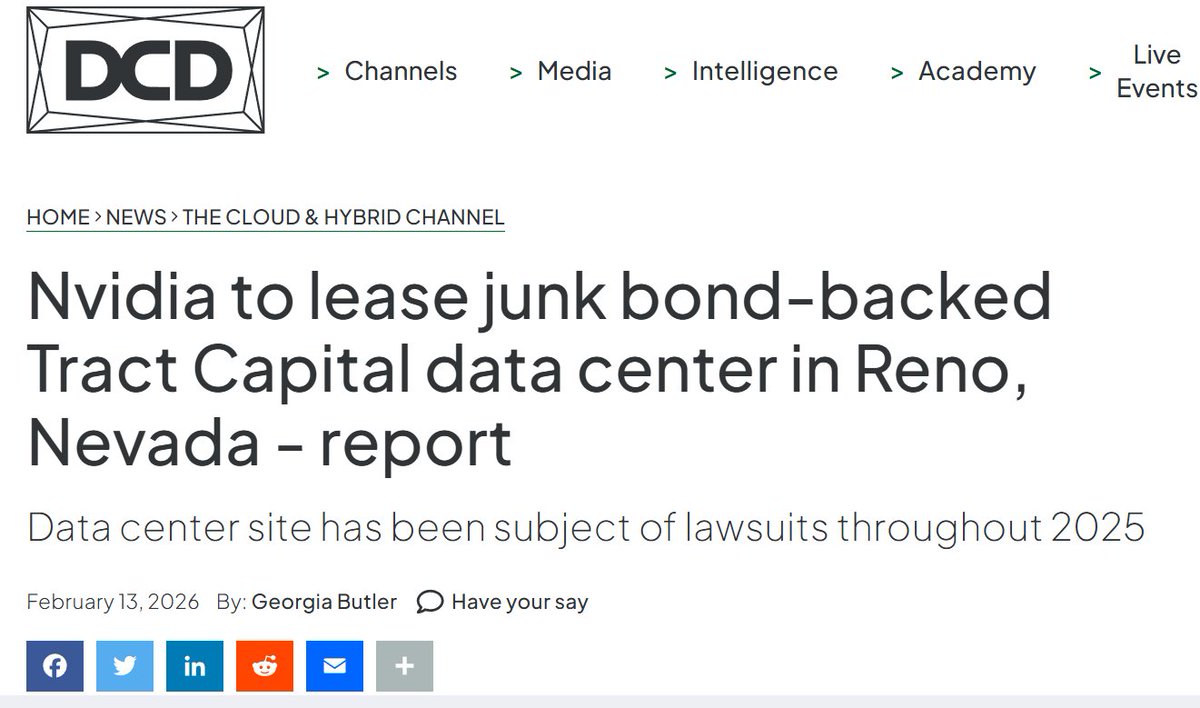

So Nvidia, the Orchestrator of GPU Supply and Demand, strikes again with yet another circular deal, once more using the favorite financing vehicle, the SPV.

I broke down the structure in the diagram below. It shows how Nvidia, a veteran of the dot-com era, seems to have learned a lesson or two and makes sure nothing lands on its own balance sheet. The debt, loans, notes, and bonds sit across dozens of SPVs, hyperscalers, and an army of neoclouds, many of which function as de facto Nvidia SPVs.

How to summarize it?

One SPV at a time.

Feb 13

$NVDA sells chips to a datacenter startup who pays by issuing junk bonds, and then Nvidia signs a contract to rent them back for the next 16 years even though they only last 4-6 years. What's the worst thing that could happen? 👀

6

69

226

31,672

Feb 13

Ganz wichtig für die neue Rechte in den USA und für Dugin.

Alfred Rosenberg hat dort viel abgeschrieben.

de.wikipedia.org/wiki/Guido_…

Feb 12

Sag ich ja: die Bezüge zum europäischen Okkultismus sind offensichtlich – bei Land und Thiel ebenso wie bei Epstein.

1

1

79

Bernd Monitor retweeted

Moscow are making some changes to their playbook - londonlovesbusiness.com/mosc…

2

3

9

3,385

Bernd Monitor retweeted

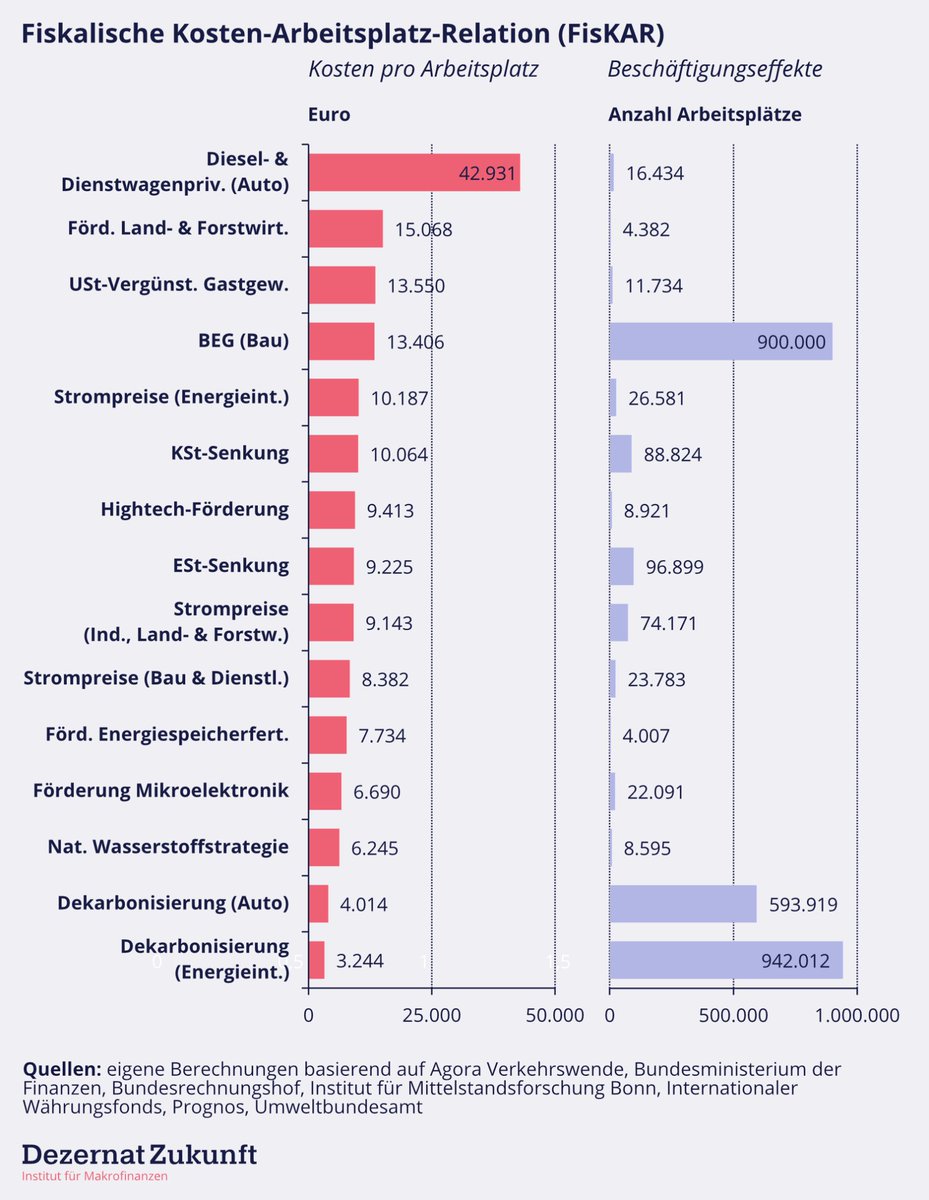

Für mich jetzt schon vielleicht die Grafik des Jahres.

Wer sich über die "Dekarbonisierung Auto" wundert, nicht gleich Zähne fletschen: Studie lesen!

9

40

104

6,683

Bernd Monitor retweeted

Feb 6

Talking points from Moscow: How RT and the GRU set the agenda on German-language Telegram

Using a layered system of Kremlin-controlled channels, Putin's propagandists have effectively become the main source for several German-language influencers.

theins.press/en/inv/289149

10

374

767

103,149

Bernd Monitor retweeted

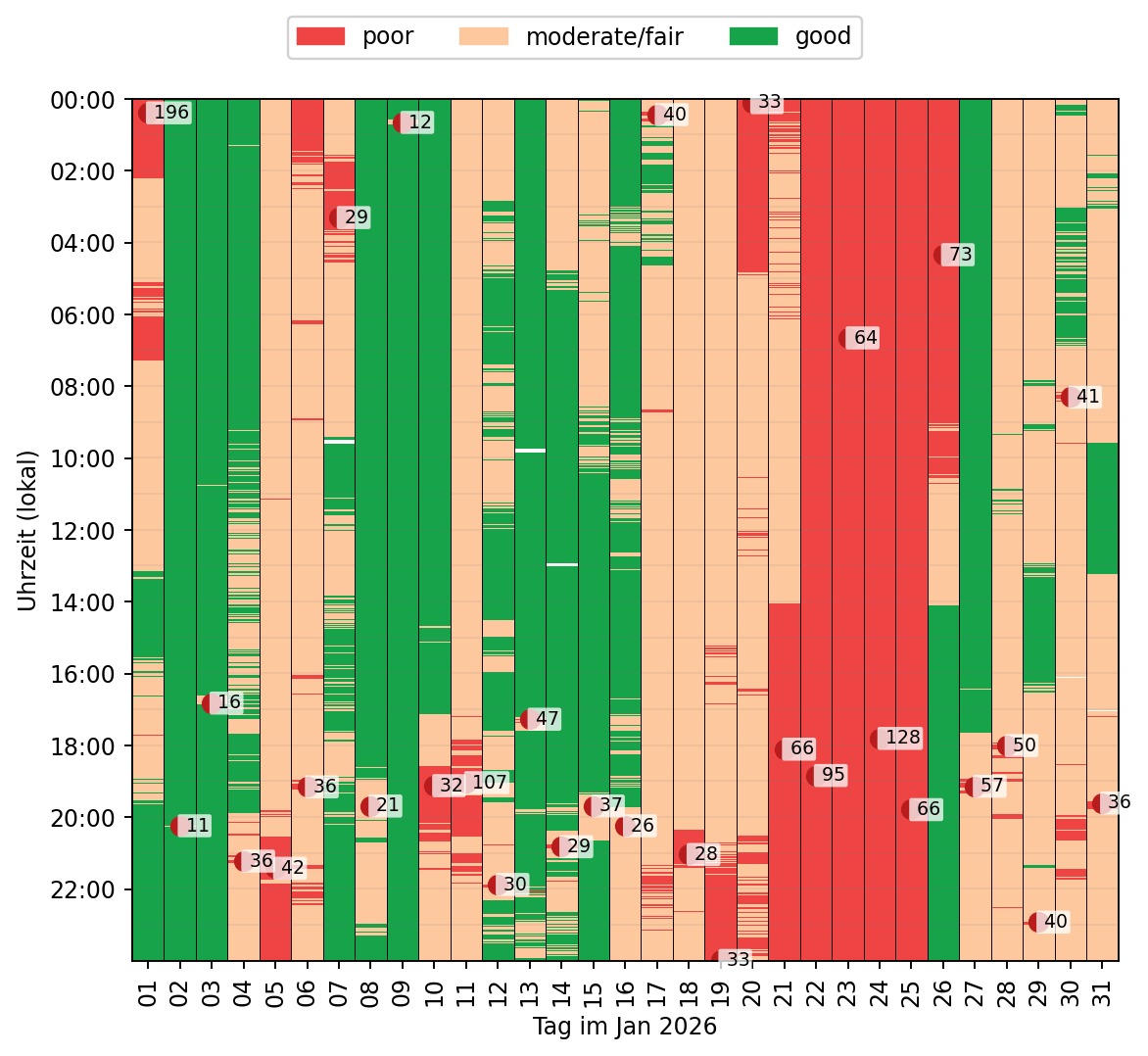

Leider hat das @umweltbundesamt den Zugang abgeschaltet, damit man Feinstaubwerte stündlich aktuell darstellen kann.

Es gibt jetzt nur noch die 24-Stunden-Mittelwerte, die absichtlich verschleiern, wann die höchste Belastung auftritt.

Es scheint wahrhaftig eine kriminelle Energie hinter der systematischen Desinformation zu stecken, worin das Problem in der Luftreinhaltung besteht.

Die PM2.5-Heatmap für ein Wohngebiet in #Stutensee für Januar 26 liegt vor. Messdaten unserer Forschungsstation zeigen Höchstwerte am 1.1. (Feuerwerk), während der Inversionswetterlage sowie regelmäßig abends im zeitlichen Zusammenhang mit beobachtetem Holzofenbetrieb.

67

373

1,373

51,493

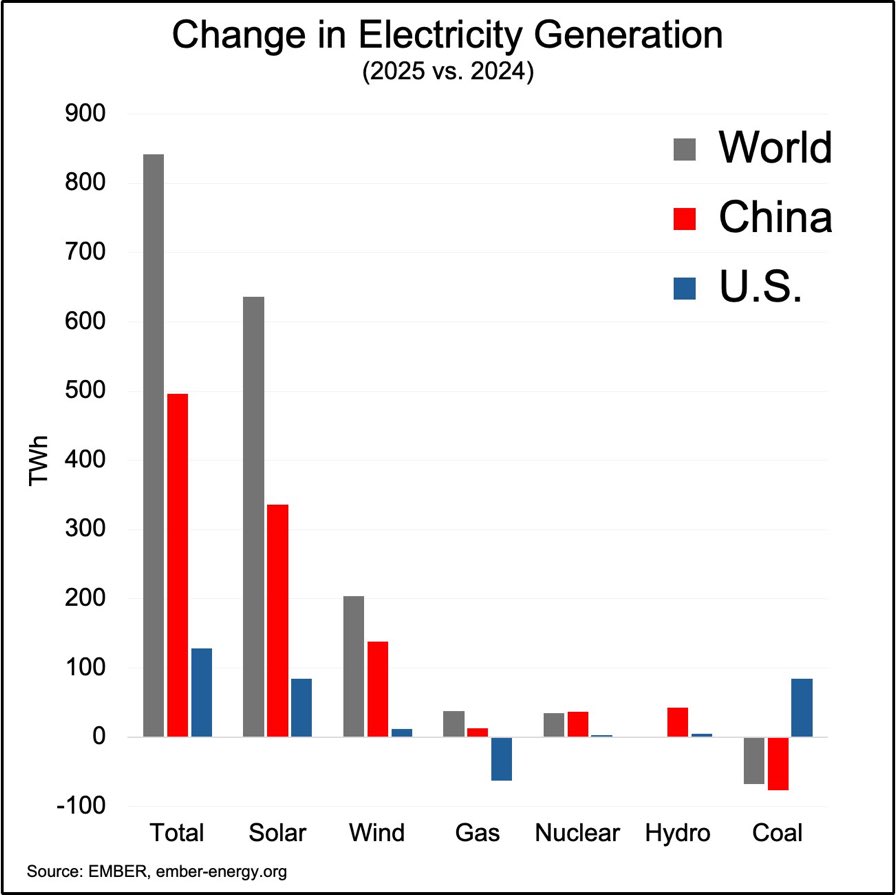

Feb 2

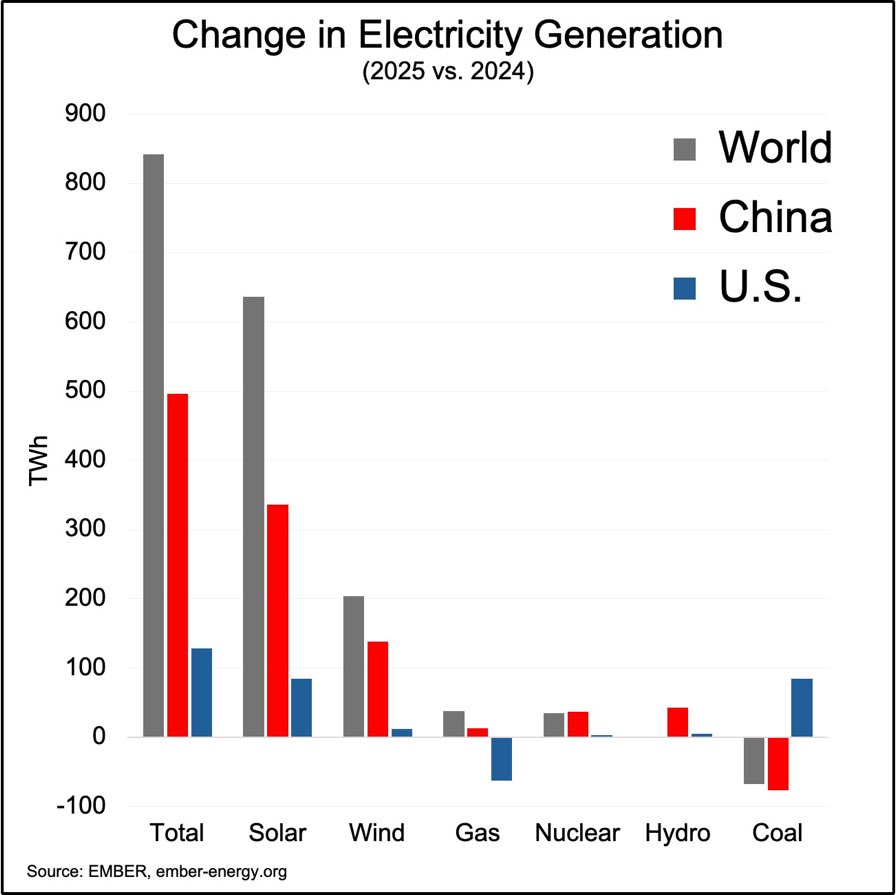

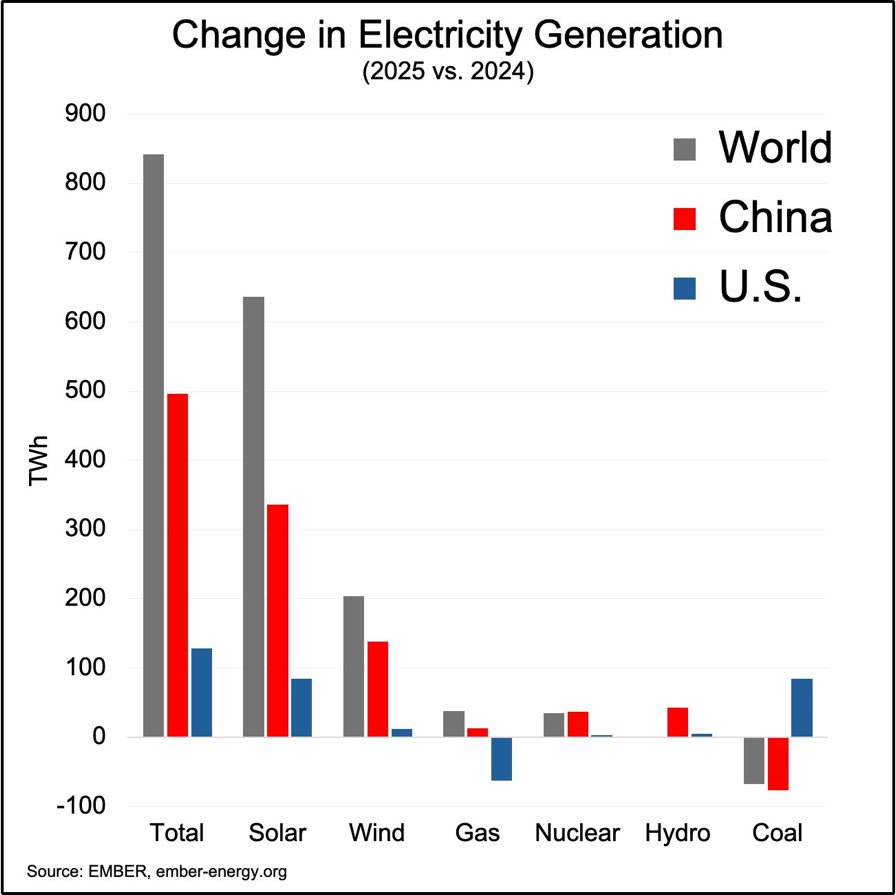

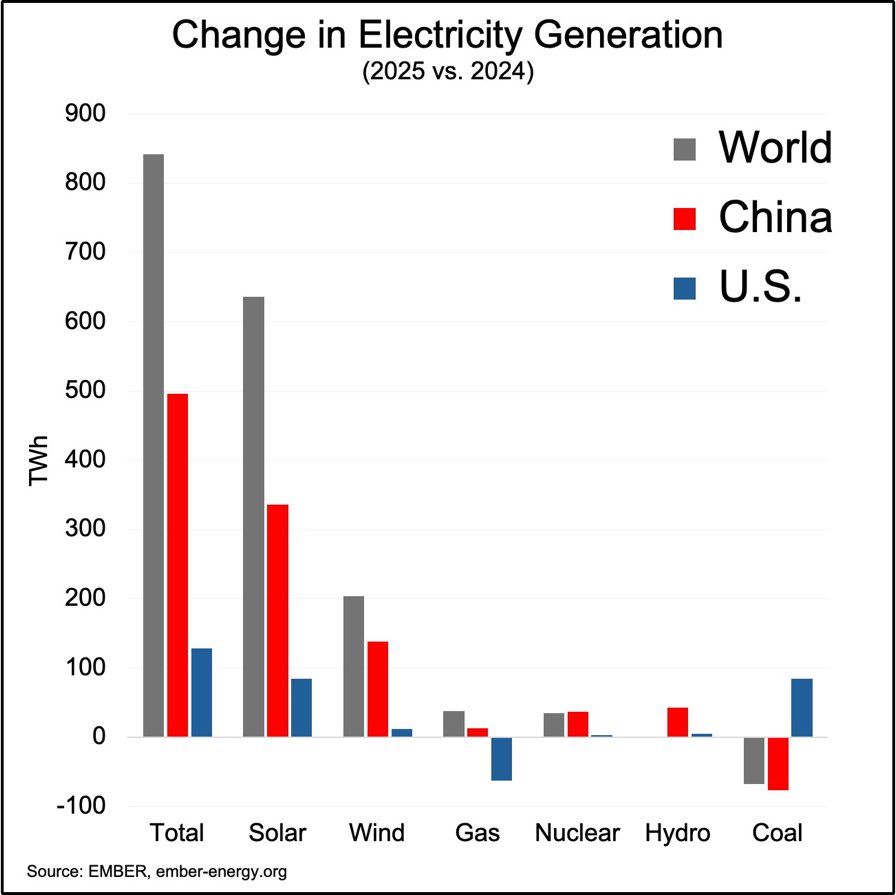

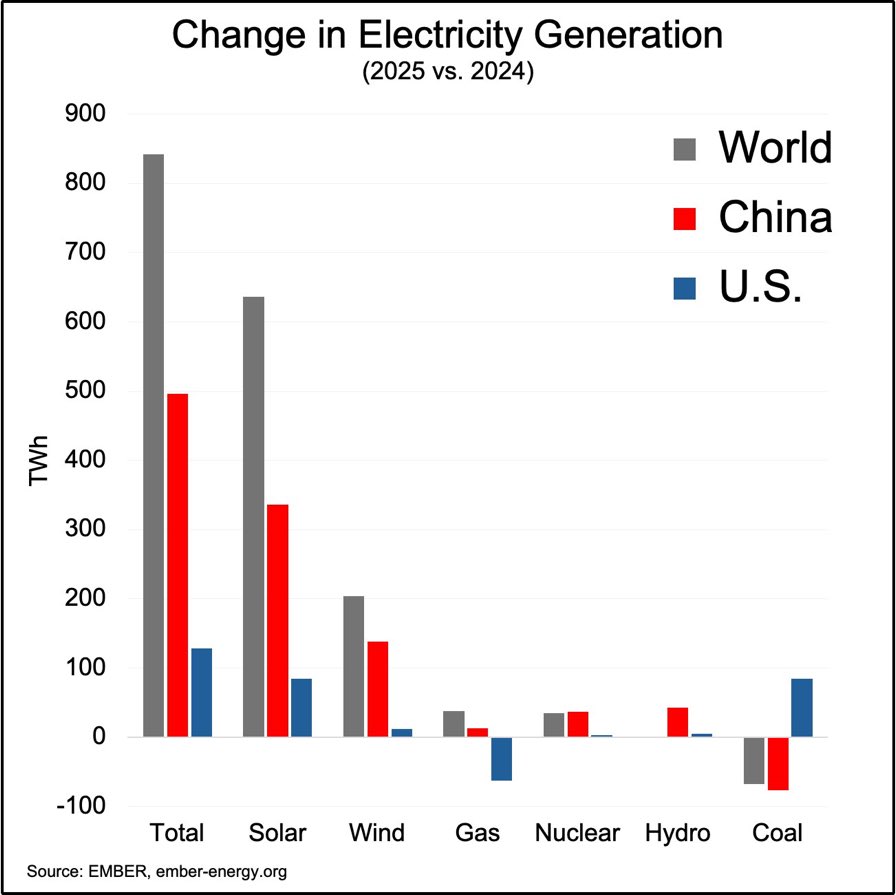

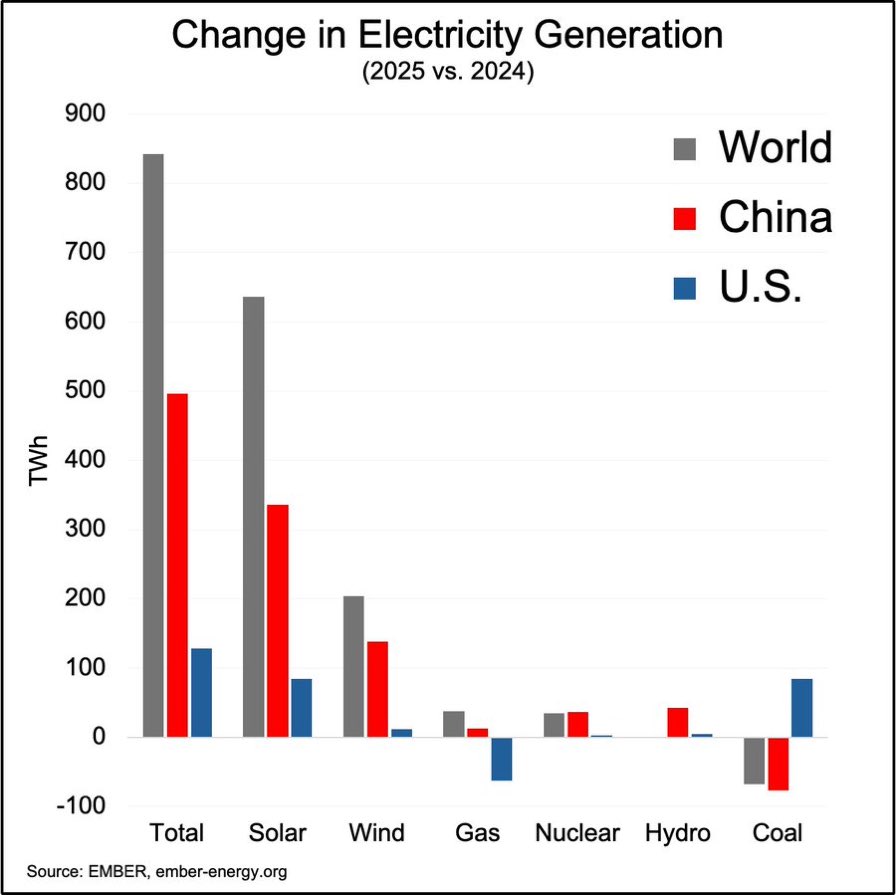

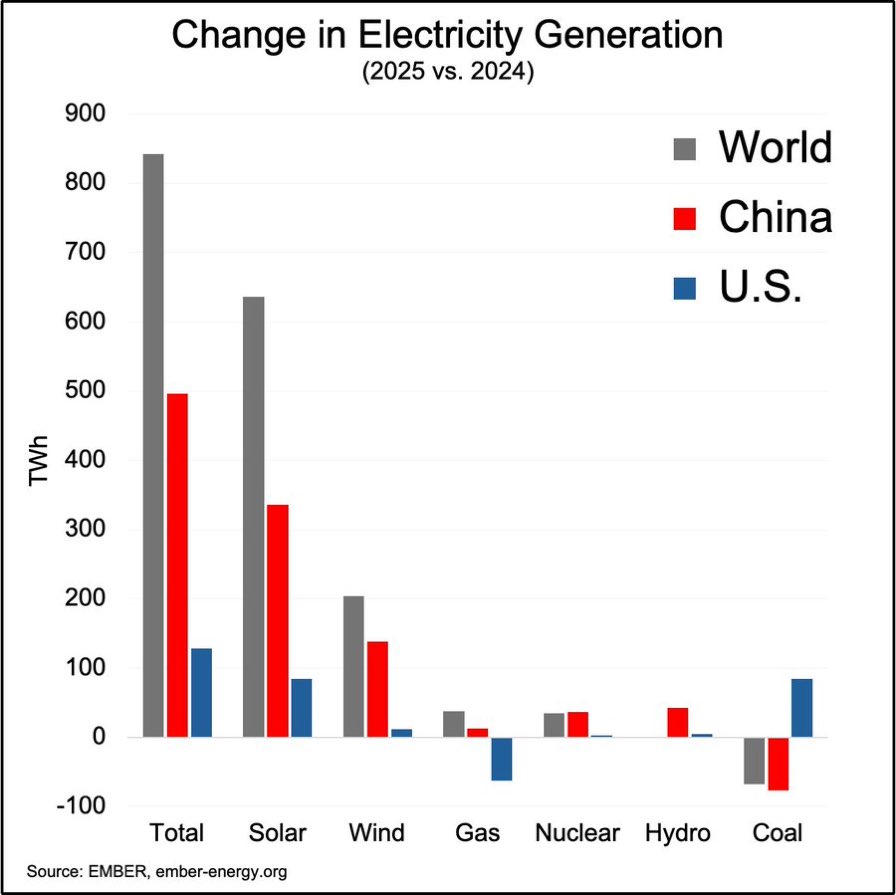

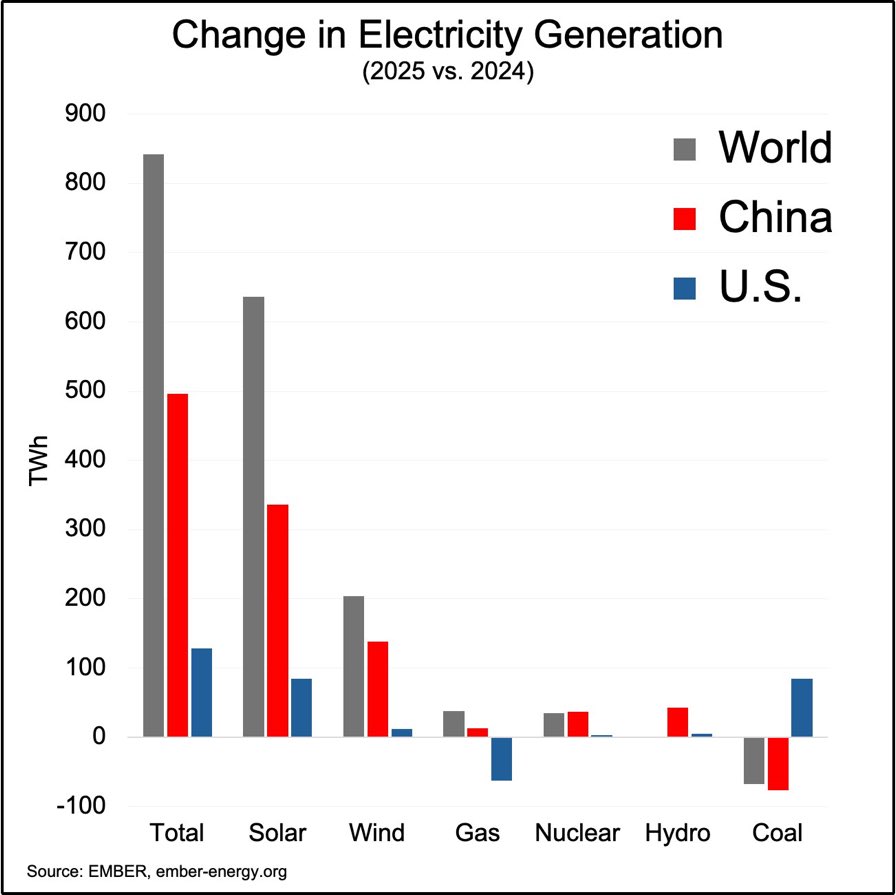

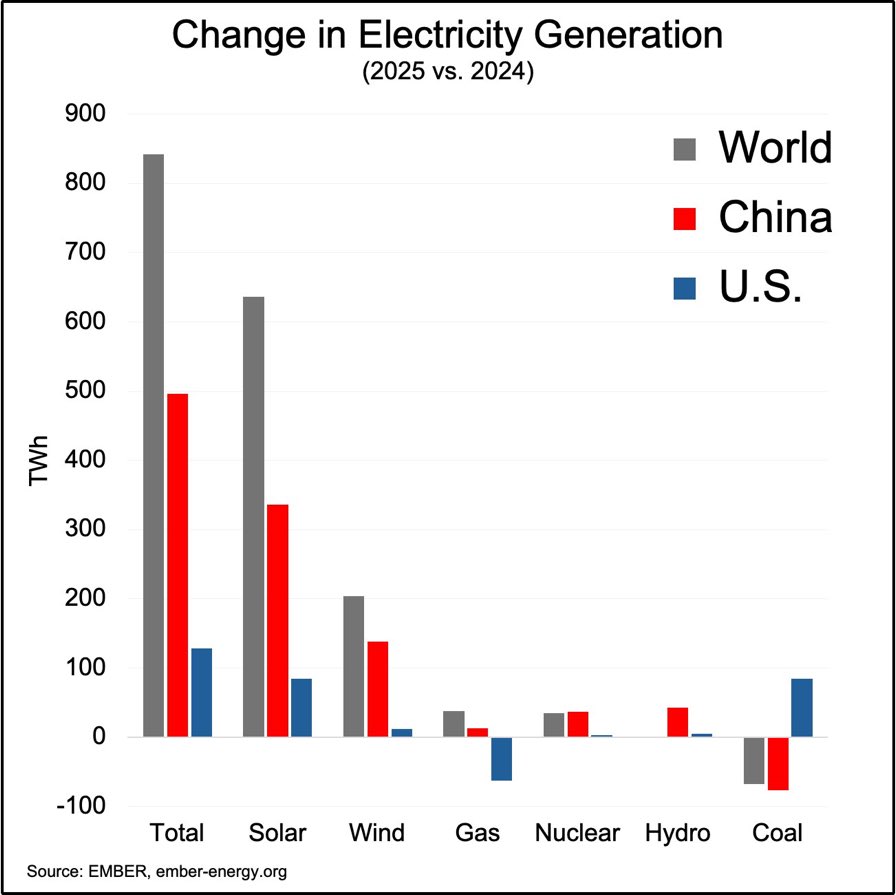

Suchbild: Wo ist die „Renaissance of Nuclear“ versteckt?

Feb 2

Solar is up. Coal is down. (56% in 2025)

The reason why has nothing to do with climate.

It’s very important to understand this.

1

123