Former analyst and portfolio manager. Fundamental buy-and-hold investor. Talking stocks and markets. Politics and golf occasionally. This is not advice.

Joined April 2025

- Tweets 1,842

- Following 232

- Followers 2,932

- Likes 3,847

337 Photos and videos

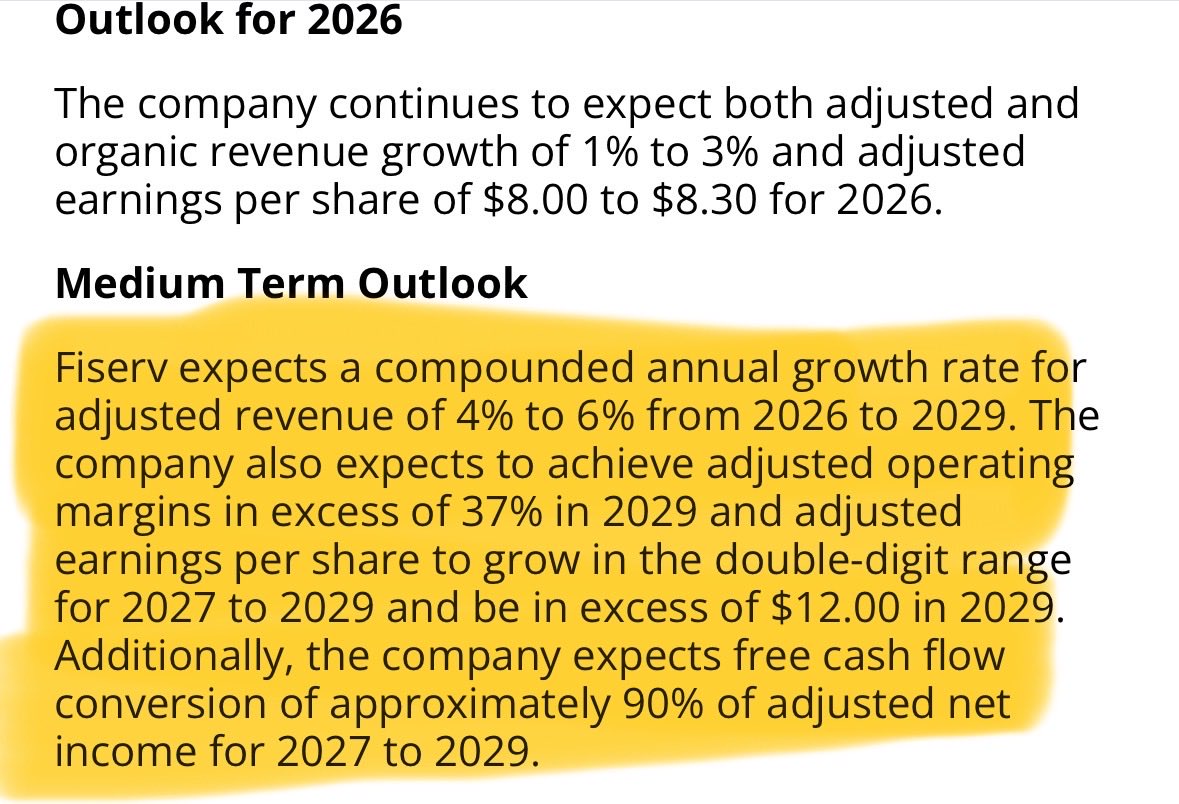

$FISV heading toward that magical place of 5x EPS where legacy payments stocks go to bottom (from 23x to 6x in 15 months). Yes, the CEO leaving is an awful look, but I got the sense earnings power had been reset to a 'bare bones' minimum where attractive growth is imminently achievable moving forward. I hate to ask it, but how much worse can it really get for $FISV?

4

22

2,291

$ADYEN announced their second acquisition in <2 months last night. They are buying Orb, a usage-based pricing/billing platform for $335M, or ~€290M. In a world of AI-based services, software companies are moving away from static subscriptions and toward dynamically pricing their services based on consumption. In this regard, $ADYEN fills a need that existing and prospective customers were asking for, and closes a perceived gap with Stripe, who had made a deal themselves back in January to bulk up in this area.

Combined w/TalonOne, $ADYEN has spent €1.04B on these two acquisitions. Both are expected to close on July 1. They will add 1-point to 2026 net revenue growth, or €25-35M, implying a full-year revenue run-rate of €50-70Mish. With TalonOne expected to reach an ARR of €60M by the end of 2026, the initial revenue contribution from Orb appears to be very modest. Margin dilution will be 1-point in 2026, but this will be inclusive of 1x acquisition-based costs.

In a video accompanying the acquisition, $ADYEN stressed they remain committed to building their own technology where possible, and their acquisition approach remains highly selective (so, a deal every other month should not become a trend). While some could view this acquisition as 'defensive', I see it as a low cost way to address an important need quickly, which $ADYEN has the luxury of doing based on their significant cash position.

4

2

34

4,019

Oh man, Lefty’s a $FOUR bull. Might have to load the boat now. Definitely not financial advice and I’m (mostly) kidding.

2

2

23

4,257

$FOUR: Midpoint of 2026 non-GAAP EPS guide is $5.60. SBC and acquisition-related costs have each been running $20M/Q for the last 5 quarters. Burden the $5.60 for these costs (about $1.40/share after tax) and you get a normalized 2026 EPS number of around $4.20, which implies 8.7x. Now, $FISV, $GPN and $PYPL all trade below that, so I guess things can always get worse. Feels like we're in a 'max pain' situation right now. I'm not sure if it's relentless shorting, overall apathy towards payments, or a genuine belief by the market that we're going to see a Fiserv-type reset for $FOUR in the not too distant future (I don't believe so)--or all of the above. We're clearly past the point of bitching about the Global Blue acquisition (will they or will they not achieve the targeted revenue synergies), having moved on to some real existential threats to the business being priced in. At another time, there would've been support under this stock given consolidation potential. But the most likely strategic buyer $GPN is out of the market and $FISV (which is rumored to have made a bid a few years back) also does not appear eager for any large scale M&A given all of its problems. So, here we are. Having acquired the majority of my shares in the 2022/2023 time period, I've more than round-tripped this sucker. No interest in selling at these levels but not looking to run out and buy more given the abundance of higher-quality options in payments right now.

10

35

6,186

Bob's Payment Stock Substack retweeted

A good review of the most recent developments in settlement talks b/w merchants and $V and $MA. A reminder that when these interchange reductions/changes do eventually occur, they will likely be beneficial (at least temporarily) for PSPs and acquirers, especially those serving unsophisticated SMBs. Example: $XYZ Square charges a flat rate to many of its merchants and takes risk on the composition of spend. With interchange rates moving lower, Square will have a lower COGS, which will allow them to ‘lower’ the rate for their customers. In reality, it will yield a higher net take rate because they will lower their rate by a smaller amount than the decline in interchange. Eventually, it will be competed away, but historically it provides a near-term boost. Something to consider.

$V $MA. Positive on Merchant Litigation Settlement. Judge Brian Cogan granted prelim approaval of new settlement (addresses court's prior 2024 rejection).

New terms, V/MA would lower US credit interchange by ~10bps over 5 yrs and cap, as well as loosen Honor All Cards/surcharging rules. "The Amended Settlement offers further relief: it would cap posted interchange rates on standard consumer credit cards at 125 basis points for at least eight years, marking a 62-basispoint reduction from the current average posted rate on standard cards"

Significant update in wallets. "The Settlements would require the Networks to modify the Honor All Wallets rules to allow merchants to accept some digital wallets (e.g., Apple Wallet) and decline others (e.g., Google Wallet), subject to several restrictions"

Settlements would allow all merchants to surcharge at the brand or product level up to 3% of transaction.

Opinion storage.courtlistener.com/re…

1

2

11

4,859

Bob's Payment Stock Substack retweeted

$V and $MA have been under 'attack' for decades. Nothing about their businesses, including actual results, has changed all that much. Of course, from time to time, concerns emerge that hit the stocks. It's a natural reaction b/c multiples are (typically) high (rightfully so) and concerns represent 'unknowns' even though they've successfully managed through all of these 'unknowns' so far. A couple of examples. In 2010, when the Durbin Amendment passed and debit interchange was slashed in the U.S., the market believed $V and $MA would be hurt (badly) b/c issuers would demand steep reductions in the fees they paid to the networks b/c of their lost interchange revenue. While $V and $MA did offer issuers relief, they balanced it by adding fees to merchants (who benefited greatly from lower debit interchange), reflecting the value networks bring to both merchants and issuers. Similarly, with BNPL. Post-pandemic, the market sensed a threat as BNPL providers were set to move credit outside traditional network rails. Fast forward to today, and the fastest growing product for BNPL providers is a network-branded card. Why? Because they realized the quickest way to gain broad acceptance was to partner with the networks and not establish a direct integration merchant-by-merchant. $V and $MA have endured b/c they've built a system with trust, broad acceptance, and habituation. I think it's going to serve them well whether agents or humans are paying, or if fiat currency is being used to pay or another digital asset (like stablecoins).

8

5

58

4,136

A couple concluding thoughts on payments from another tough week:

Right now, multiple companies are being priced for permanent disruption in payments i.e., $GPN $FISV $PYPL $FOUR but there is diminishing value being allocated to the disruptors, at least the publicly traded ones. An example: $GPN trades at 4.5x. This is due in (large) part to concerns about its integrated channel, where it provides processing for vertical-specific ISVs. Who’s encroaching on this space? Stripe yes, but also $ADYEN, whose Platforms segment is its fastest growing. If $GPN trades at 4.5x then $ADYEN can’t trade at less than a market multiple. Either $GPN or $ADYEN should trade at a higher multiple. The market is pricing a large chunk of this business going away from $GPN, but who is it going to? All of it can’t go to Stripe, can it?

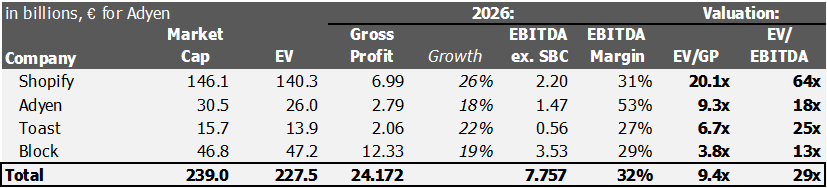

The other point, which reinforces the first point: There is a shocking disconnect between private and public market valuations for payments companies. Last fall, Checkout was assigned a $12B valuation in an employee sale. Checkout did $300B of volume in 2025. Assuming a 15bps take rate implies $450M of revenue. Adjusted EBITDA was 10% so around $50M of adjusted EBITDA. $12B market cap for $50M of ‘adjusted’ EBITDA. Meanwhile, $ADYEN will do ~$1.68B of GAAP EBITDA in 2026 and currently has a market cap of ~$30B and <$25B EV.

My conclusion: no winners in payments, only losers. I don’t think that’s sustainable, but certainly been wrong so far.

13

2

66

25,289

$META walking the plank. Honestly thought Zuck would be first to blink (on the capex super cycle) but does not appear to be happening anytime soon!

Meta weighs big equity raising after blockbuster Google deal - FT ft.com/content/e6df645d-1709…

2

4

2,273

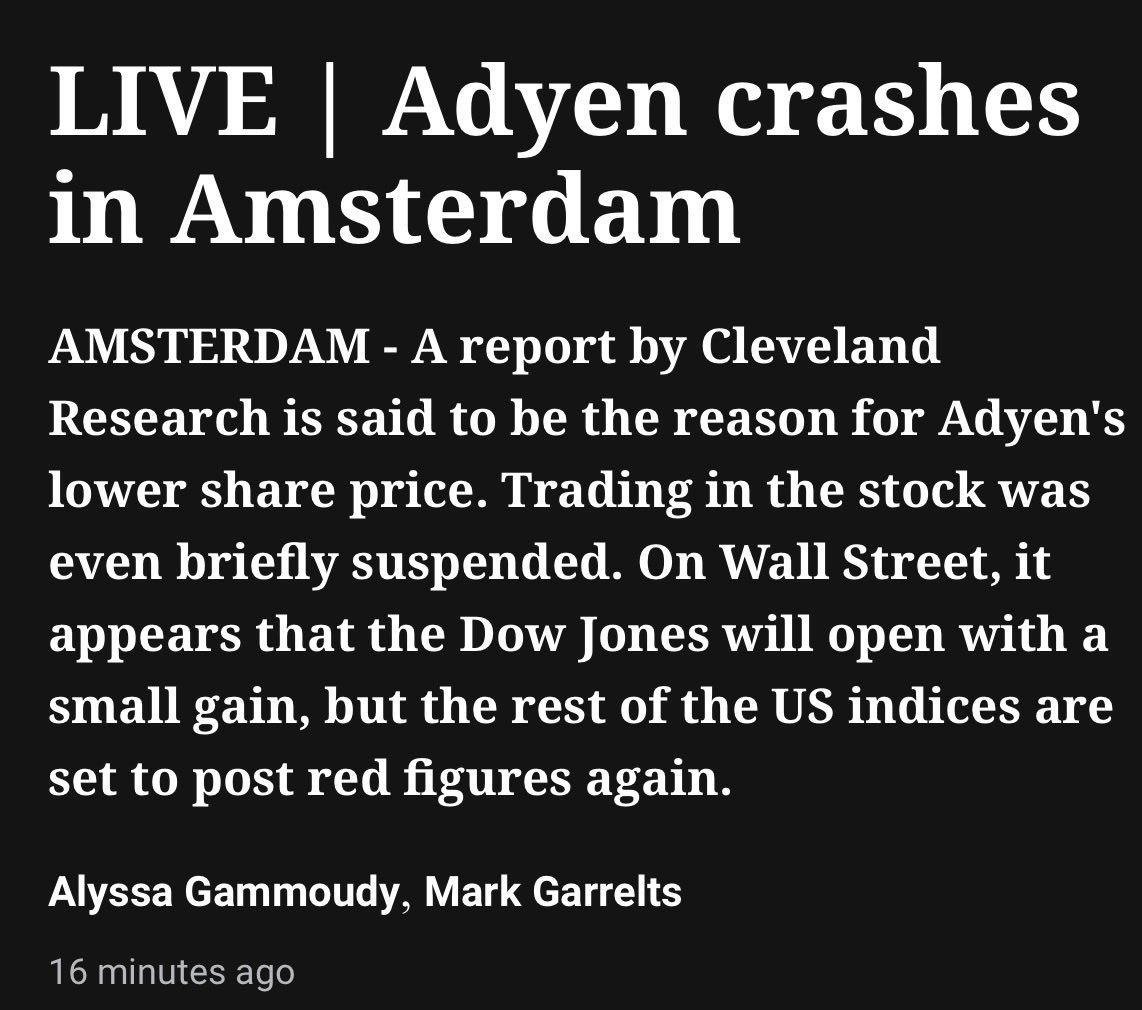

Negative report from Cleveland Research is behind drop in $ADYEN. Concerns over market share and pricing (apparently, I have not read report). Again, market share commentary is a bit surprising given mid-20s FXN volume growth in Q1, which ran a bit better than 2024 (by my estimate). I can’t speak to pricing, but perhaps they are picking up rumblings of increased pressure in their channel checks?

7

3

34

7,416

I'm not sure why payment and fintech stocks gap down from day-to-day (b/c it happens so frequently) but I'm guessing this *may* be a reason for today's decline. @stripe $v and $ma are close to launching a stablecoin infrastructure platform for 'mainstream' payments in potential collaboration with $coin. While the success of stablecoin payments are going to depend on the willingness of consumers to adopt (which I don't think there's a strong case for as of yet), the major players are certainly planning for that eventuality. Also, dovetails with the theme of most of the 'value' in payments being accrued to @stripe and away from the public players like $adyen $gpn and $fisv.

Payment giants Stripe, Visa, Mastercard said to be among backers of soon-to-debut stablecoin platform coindesk.com/business/2026/0… via @coindesk

6

1

26

8,651

May sucked, but I did manage to get 10k steps every single day. On to better things in June!

2

11

981