The future is now. AI, business, robots, investing, or whatever else I find interesting…and a bit of F1 & TDF

Joined September 2010

- Tweets 6,979

- Following 798

- Followers 1,187

- Likes 618

380 Photos and videos

Trump coming out to cut the legs out from Warsh's completely neutral first FOMC speech.

52

FOMC Chair seems like he's having a fairly calming effect on the markets...so far. Sounds like they want to bring the fed's data reporting into the modern age (AI) which may bring more volatility as they make more "real time" decisions.

86

New FOMC chair already coming out soft by leaving rates unchanged. They need to start hiking rates 25 basis points every FOMC meeting for the rest of the year. Sadly, they won't. Instead, we're going to continue with higher inflation.

1

120

Bryan Waldo retweeted

Jun 15

Architecture interior design. Wait for the result.

28

154

2,466

573,623

Jun 15

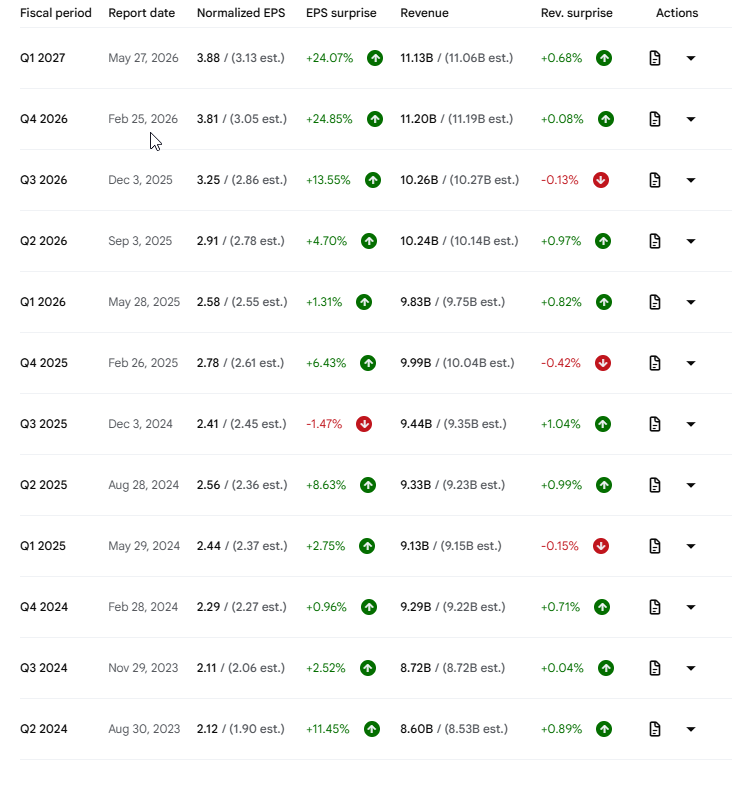

$CRM is starting to look pretty interesting. They are accelerating earnings while having the share price beaten down heavily. Will AI destroy the company? Or be the catalyst to strengthen their relationships?

1

131

Jun 14

Sounds like a case for regulatory capture? Preventing the hollowing out of dying industries is not the path to an open free society.

60

Jun 13

"Relying on willpower or discipline is not noble...it's stupid"

Simon Russo

Market Wizards ~The Next Generation

1

93

Jun 13

"Systems over willpower. Mechanical over manual and hard stops over hope!"

34

Jun 12

$spcx next earnings is somewhere around 8/11. Insiders can sell 20% after earnings. If the stock trades at 170.51 or greater for 5 of the 10 days immediately prior that earnings date it unlocks an additional 10% (30% total) eligible to sell. This is critical to understand

78

Jun 12

These massive sell orders dumping $spcx down to $150 and getting insta bought are quite interesting to watch. This stock is going to be an amazing stock to range trade over the next few years.

1

105

Jun 12

Excited to check out @jackschwager latest Market Wizards book. This series might be the best 'series' about trading to ever be written. Can't hardly wait to start it.

51

Jun 12

Looks like Elon becoming the first trillionaire is going to happen much faster than I thought. I think he was around 300 billion at the time I wrote this invisible X post. He's currently estimated at 971 billion.

1

1

29

Jun 11

Still in 2nd or 3rd inning of AI. So many ways for the little guy to make money off this AI spending. All a guy has to do is pick one

Jun 11

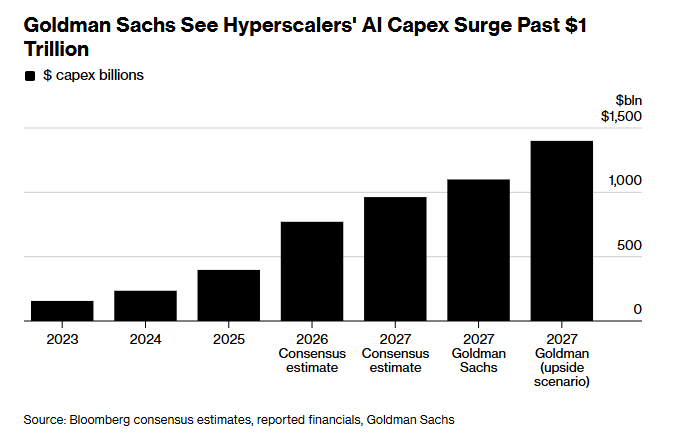

going to need a lot of energy and metals for that >>

Goldman Sachs See Hyperscalers' AI Capex Surge Past $1 Trillion

18

Jun 7

Why does apple insist on making the iPhone so slippery? I would love to eliminate my case, but after q weekend running naked I've dropped my phone more than last 5 years.

1

48

Jun 7

Everyone's saying how AI is in bubble, but with the tremendous energy requirements over the next decade it seems like we're still super early. The playing field is shifting, but we're only in 2nd maybe 3rd inning. Large fortunes are still to be made.

1

2

1,207

HOW TO ABANDON THE PRESENT VALUE FORMULA IN POLITE COMPANY

While retail investors are free to completely abandon the present value formula whenever they so desire, professional sell-side research analysts do not have such freedom. The professional standards force those analysts to follow a set of complex rules and social conventions resembling a tea ceremony to do so.

The research analyst has a target price that has to be about 15% above the current price. Then he must construct a set of cash flow forecasts, long-term growth forecasts, and discount rates that mechanically justify that target price.

In a bubble, the price is unjustifiable, which means that those forecasts must also be unjustifiable, but they must appear on the surface to be as justifiable as possible. Furthermore, the near-term cash flow forecasts must actually be relatively accurate because the reality of those near-term cash flows will, by definition, be revealed in the near term.

The two main ways analysts can tune their present value formula to justify the unjustifiable target prices are (1) pushing out the earnings in the multiple and (2) increasing the long-term growth rate. The first method simply says that the front page of the report will not compute multiples based on year 2026 or 2027 earnings, but year 2030 or even year 2040 earnings. This is relatively safe, as both the analyst and the institutional investor listening to the analyst are likely pursuing other career paths by 2040, when those 2040 earnings fall short of the forecasts.

The second method is just to increase the terminal value and terminal multiple after the explicit forecast horizon by increasing the long-term growth rate forecast. Owen Lamont has recently written about this, but the observation that the analyst long-term forecasts become unrealistic in a bubble is almost as old as the field of security analysis itself as each analyst covering each stock has to stretch the long-term growth forecast higher and higher.

Although some stocks may meet these high long-term growth forecasts, at some point of the bubble they will aggregate for the whole market to a level that is almost certainly impossible for even the godliest Machine God to produce. This observation is also not original but has been made, among other people, by Cliff Asness in his “Bubble Logic” piece.

A good proxy for Step 4 of the bubble is to compute the difference between aggregated individual stock analyst long-term growth forecasts and macroeconomic analysts’ long-term GDP growth forecasts. (This may be the sole case in which macroeconomic analysts’ forecasts of anything have any utility.) When the bottom-up LTG aggregated across stocks is unusually high compared to the long-term GDP growth forecast, that is evidence of the professional investors taking the fourth step and abandoning the discipline of the present value formula in a polite way.

THE LIFE CYCLE OF A BUBBLE

1. A genuine advancement creates real productivity gains. A real technological or economic improvement increases productivity and leads to genuine revenue and earnings growth.

2. Stock prices leak into reported profitability. Rising stock prices improve reported earnings, financing conditions, collateral values, and perceived business performance.

3. Reported profitability drives real investment. Companies increase hiring, capital spending, construction, expansion, and speculative investment because of their own or their customers’ reported profitability.

4. Bubble beliefs and abandonment of present-value discipline. Investors stop focusing on discounted cash flows and begin relying on continuing gains from the greater fool theory, believing they can sell later at a higher price.

5. Inflows from sideline investors. Previously cautious investors enter the market in large numbers. New money from existing and new investors participation drive prices higher.

6. Extreme overvaluation. Prices rise far above historical normal multiples of reported fundamentals, even ignoring the fact that reported fundamentals have been driven by rising stock prices.

7. Issuance. Companies take advantage of high valuations through IPOs, secondary offerings, stock-based acquisitions, SPACs, and insider selling.

8. Exhaustion of inflows. The flow of new investors starts shrinking while existing investors approach their risk and leverage limits. Volatility and dispersion grow and gains become less uniform across stocks.

9. Earnings disappointments from slowing price appreciation. As stock prices stop rising rapidly, the earlier boost from higher valuations into earnings weakens or reverses. Companies begin missing expectations.

10. Stock-price collapse with high volatility. Confidence in both the fundamental growth and in the greater fool theory break down and prices fall sharply. Volatility rises further as leverage unwinds.

11. Bear-market rallies and progressively greater exhaustion. Bargain hunters and frustrated latecomers repeatedly buy the dips, creating violent temporary rallies that fail. Markets make lower highs and lower lows.

12. Capitulation, abandonment, and normalization. Bubble participants eventually give up in disgust or exhaustion. Volatility falls, valuations normalize, and the market returns to more ordinary behavior.

13

22

252

183,355

Jun 6

After the initial AI goldrush is over (10 to 20 years) it will become near impossible for 1 man to become a billionaire. There's a certain level of 'grey area ' business needs to operate in which will become very difficult to operate in.

92

Jun 4

Companies like Walmart $wmt seem like a nice safe haven as these tech plays getup in the nosebleeds. These retailers will benefit from reduced tariffs and strong sales on next earnings (pre-war)

1

155