Build Alpha Trading Software creates, tests and codes trading strategies with the click of a button. Demos: buildalpha.com/demo

Joined January 2017

- Tweets 2,868

- Following 0

- Followers 6,765

- Likes 638

105 Photos and videos

Jun 12

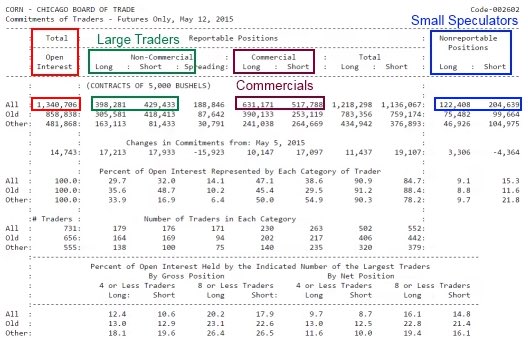

Trader positioning is one of the most powerful alternative data sets available buildalpha.com/commitment-of…

3

326

Jun 11

AI operates Build Alpha and also makes pretty cool thumbnail images 😂

6

365

Jun 10

It's so great to see so many retail traders talking about overfitting and robustness testing now. It really feels like Build Alpha changed the conversation over the last decade 🤝

1

12

644

Jun 10

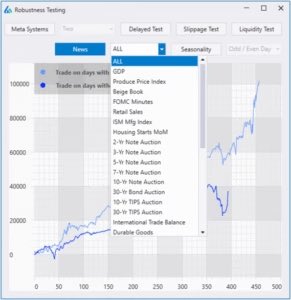

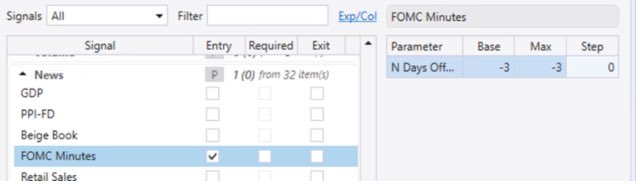

For the full robustness overview with pass/fail examples: buildalpha.com/robustness-te…

5

501

Jun 10

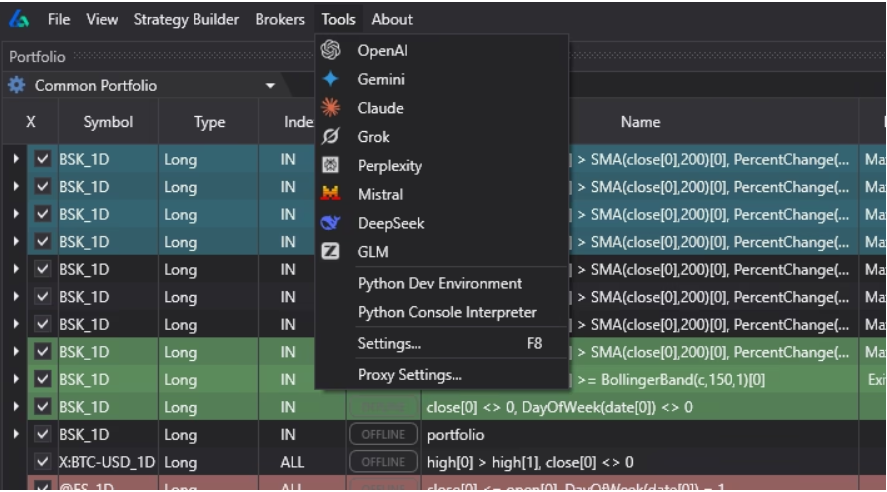

Which LLMs should be added to Build Alpha for the upcoming release?

Am I missing any? Open Router for free/marketplace?

5

1

19

1,156

Jun 5

Build Alpha 🤝 Claude

Automated strategy generation and validation in one platform. More to share next week..

2

1

18

744

Jun 4

Connected AI to drive Build Alpha and it's insane! Claude, Grok, ChatGPT, Gemini, you name it.

Video will drop next week. Beta will open soon. Fun times ahead!

14

455

Jun 3

hard to believe this was almost ten years ago. Approach remains the same 💪chatwithtraders.com/103

Escaping Randomness and turning to data for an edge

1

2

8

1,432

Jun 1

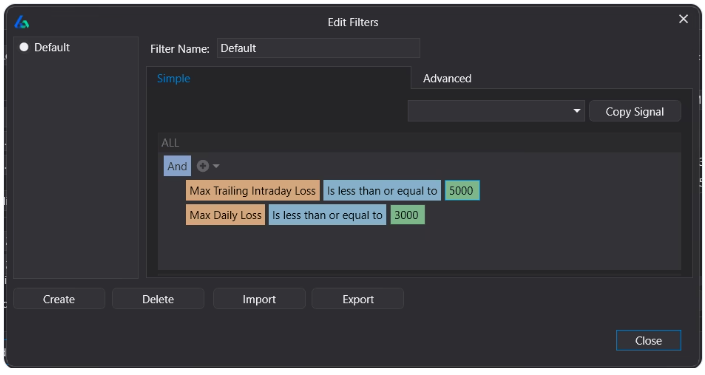

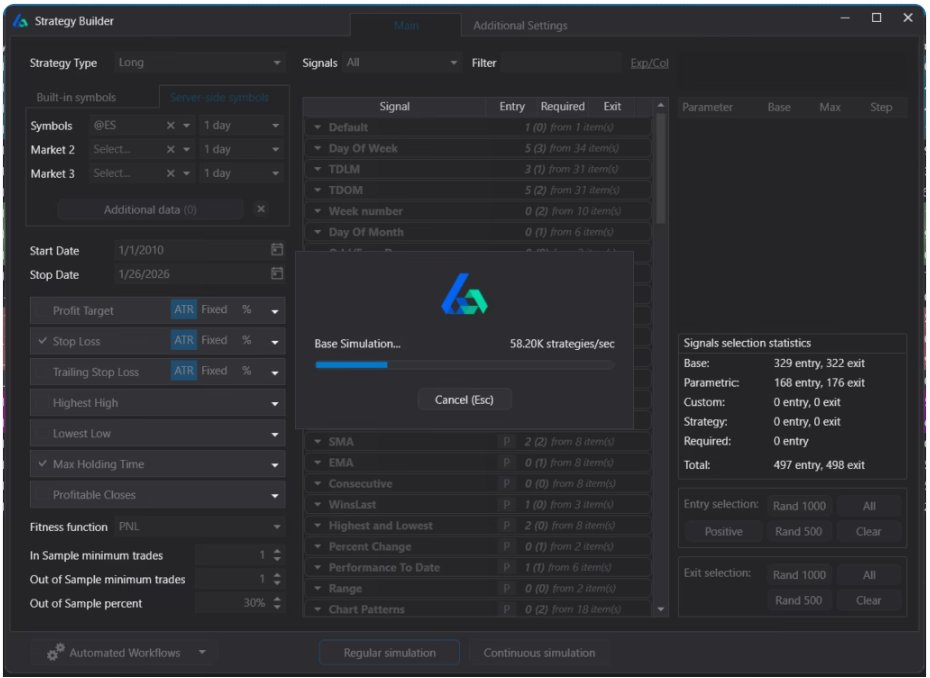

How Build Alpha works in 3 steps

1. Set Constraints

2. Set Filters/Robustness gates

3. Automatically generates strategies and exports code

Here's how 👇

1

1

8

1,022

Jun 1

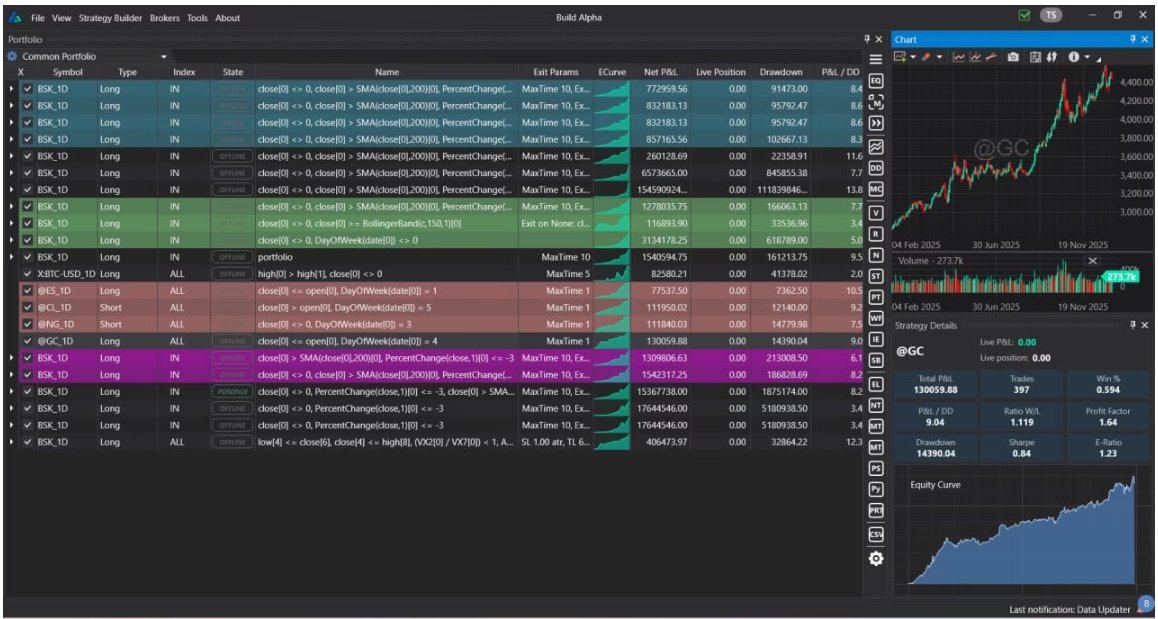

3. Generates Strategies and Code - results window shows strategy candidates that pass your metrics using only your constraints/inputs.

Export fully automate-able code for

· TradeStation

· MultiCharts

· Ninjatrader8

· TradingView

· Metatrader4/5

· Python

· ProRealTime

1

2

362

Jun 1

All of this with NO coding.

Automated strategy discovery and validation have been and still are the future of trading. Much more to come soon...

3

303

May 29

Genichi Taguchi was a famous quality control engineer whose methods were adopted by Toyota, Ford, and NASA.

He focused on processes that survived noise and uncertainty, not ones that performed best in optimal conditions.

Quant traders should build strategies like this.

Build Alpha's Noise Test and automated strategy filtering are largely inspired by Taguchi's work.

6

25

4,359

May 26

Citadel pays atmospheric scientists $1M a year.

Why: weather moves natural gas, heating oil, and electricity demand before charts ever react.

30 years of the same US weather data ships with Build Alpha. The big desks model on it. Now so can you.

3

13

3,456

May 21

Timothy Masters runs one test before approving any backtest:

Monte Carlo Permutation Test

Your edge has to hold across 1,000 alternate paths. Same statistics, different sequence.

Most retail quants skip it. Build Alpha automates it.

5

38

9,054

May 19

Jaffray Woodriff runs every trading signal at his $1B Hedge Fund QIM through one test before it ever sees live capital:

Vs Random Benchmarking

It answers could a coin flip have done this?

Most traders have never run this test once. Build Alpha can run it automatically on every strategy it generates.

6

81

12,291

May 15

Most systematic traders are training on a coincidence.

The historical price chart is one path the market took. It is not the path. The future could land on any of a thousand others and if your strategy only survives the one timeline you trained on, you do not have an edge.

You have memory.

Backtesting on the historical OHLC is an already known limit. The fix the industry settled on: Monte Carlo, walk-forward, noise testing - all happen AFTER the strategy is built.

By the time you run them, your search algorithm has already memorized the noise. You're mostly checking how badly.

"Do not optimize for the known past. Optimize for the unknown futures."

Robustness is the only thing that compounds in this game. Everything else is one regime away from going to zero.

The fix: train your models and build your strategies on synthetic data not just the historical data. Link below 👇

1

1

21

2,471

May 15

Pre-simulation synthetic data, not just post-validation. Write-up with the "how" and visuals here: buildalpha.com/synthetic-dat…

1

565

May 13

ICYMI:

Pooling trading signals together: buildalpha.com/trading-signa…

Monte Carlo Permutation Testing: buildalpha.com/monte-carlo-p…

Portfolio Testing: buildalpha.com/portfolio-bac…

2

764