Joined December 2020

- Tweets 1,942

- Following 669

- Followers 741

- Likes 531

303 Photos and videos

Pinned Tweet

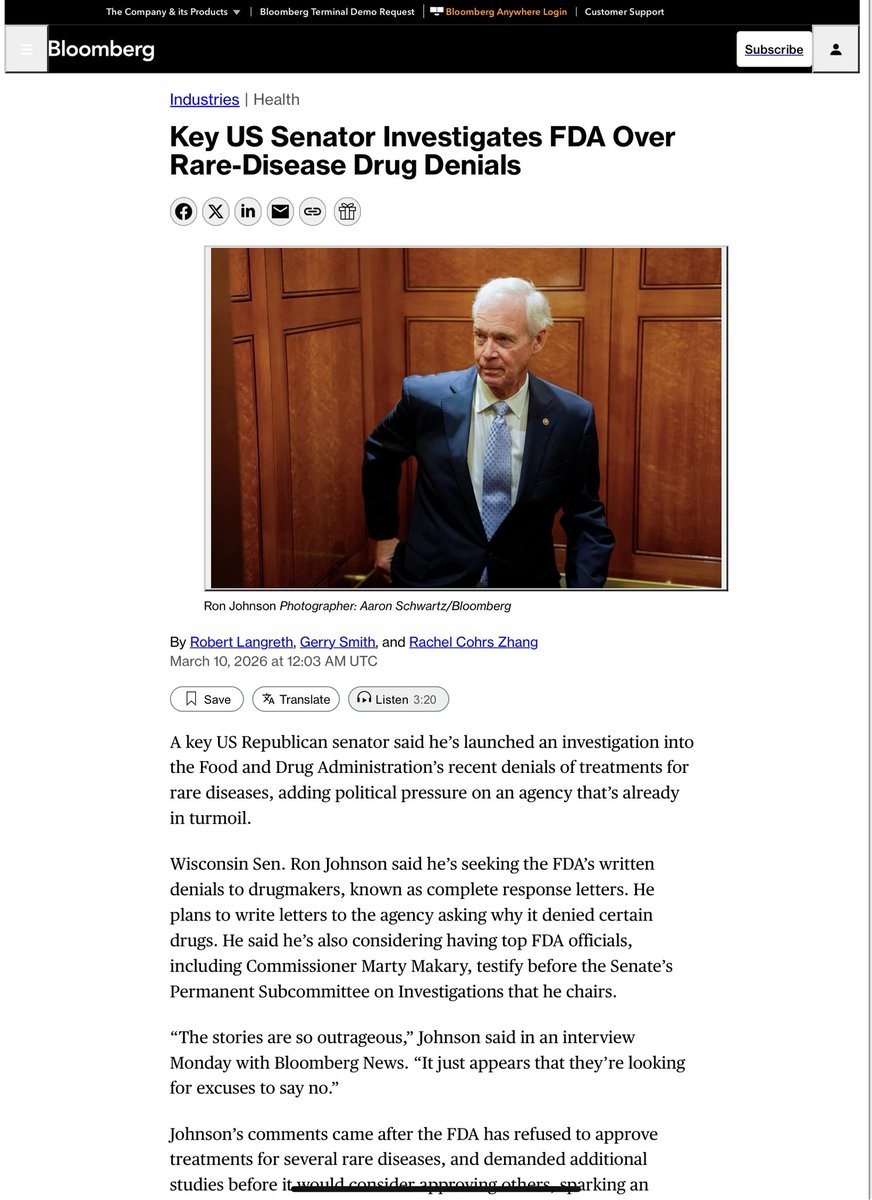

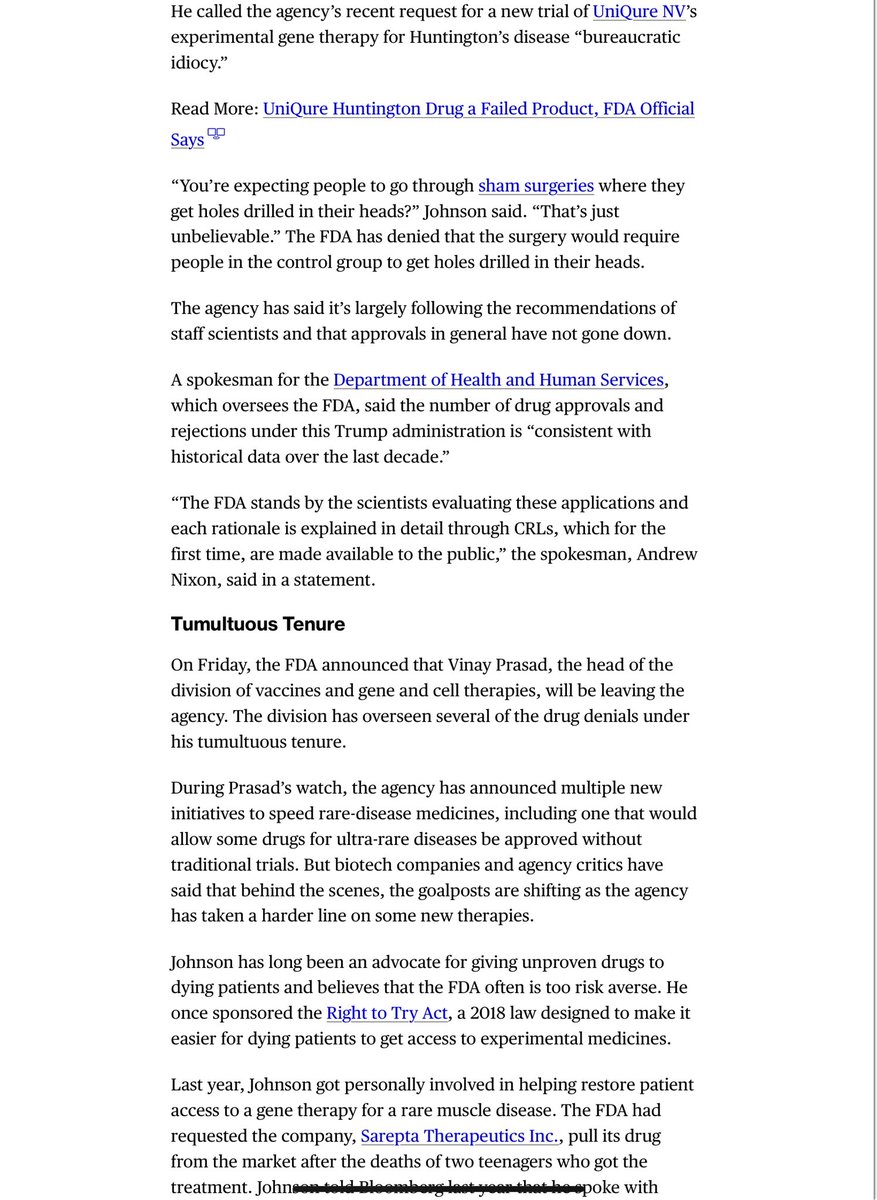

Mar 10

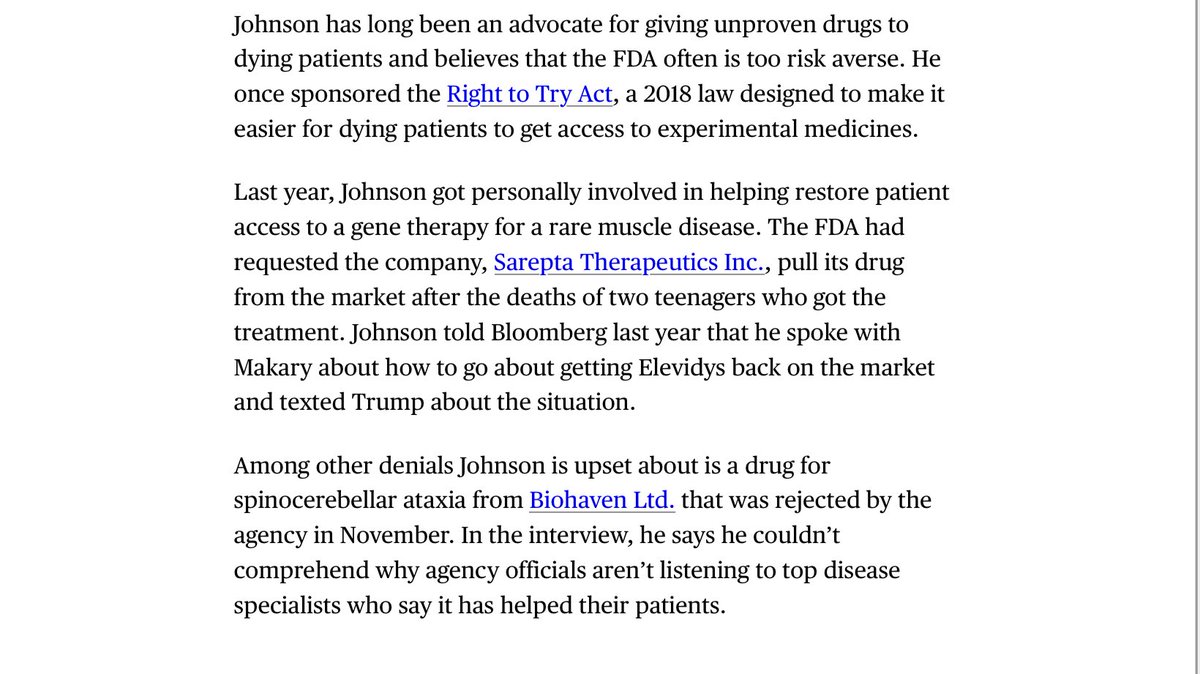

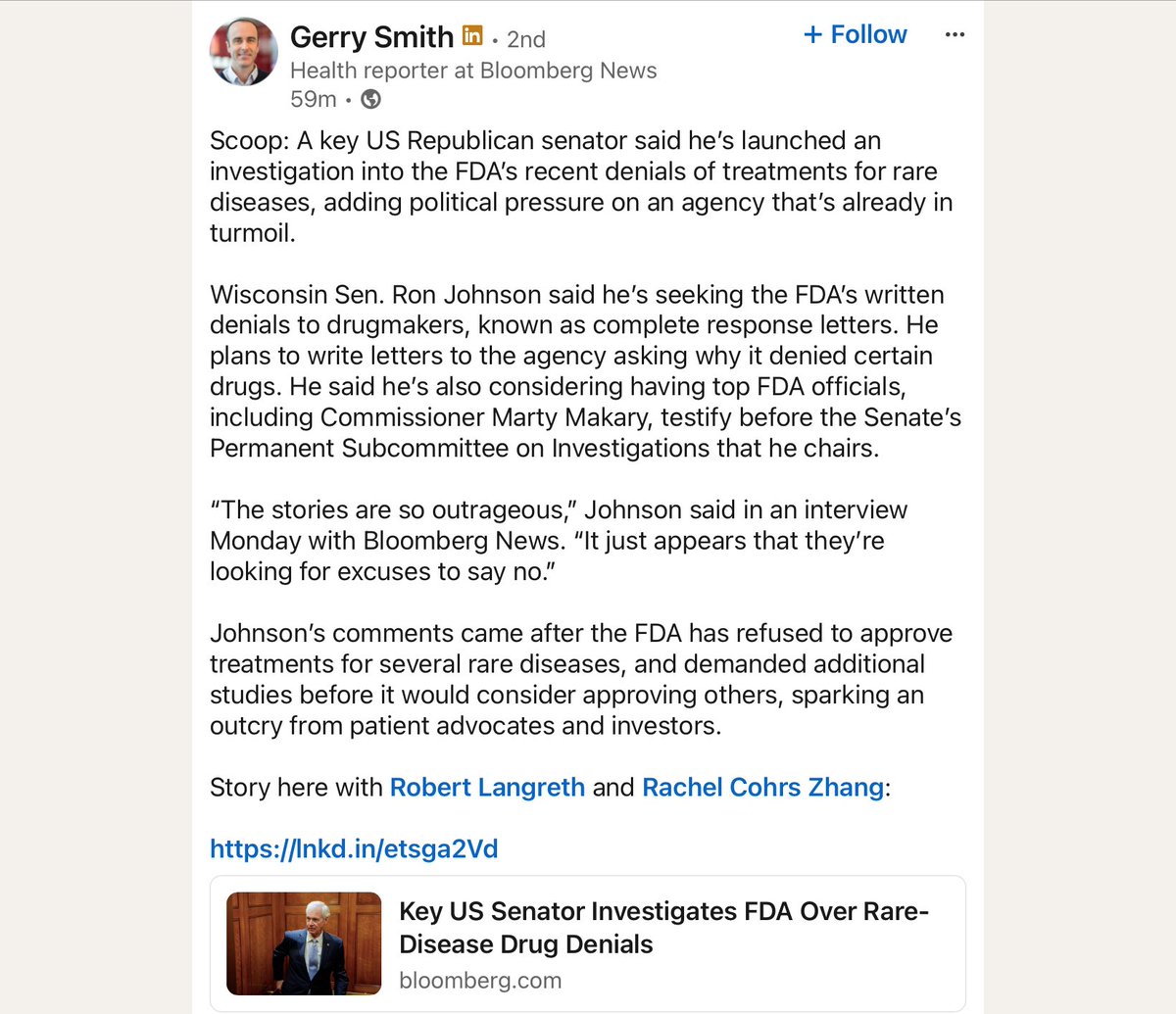

$qure, this is huge. Senator Ron Johnson launched investigations into FDA per Bloomberg. MM could be questioned at senator hearing. MM must go.

2

16

100

16,060

Jun 14

$abvx I am bearish on both efficacy and safety.

Jun 14

Lots of misinformation out there (go figure).

I am not short/bearish $ABVX at all.

Article 1 (July 2025) BUY @ $68/share (immediately after P3 UC induction data)

Article 2 (January 2026) BUY @ $118/share (amid M&A rumors)

"Whether the company is acquired or not, investors have a lot of catalysts to look forward to this year. Bear in mind that its stock is likely already priced for some M&A premium. So I would be wary of investing in the stock with the sole expectation that it will be acquired. Rather, I would keep the focus on obefazimod and the multi-billion dollar opportunity in UC and Crohn's disease."

Article 3 (March 2026) downgrade to HOLD @ $110.70

"Still, I remain very optimistic about the long-term prospects of obefazimod in UC and CD. But I’m in favor of trimming the position ahead of Phase 2 CD and Phase 3 UC data later this year, as expectations are clearly very high."

Article 4 (June 2026) maintain HOLD @ $85/share

"Notice that I did not, in any way, penalize obefazimod for malignancy concerns. As of right now, I don't think this is something that merits a model adjustment (e.g., in peak share assumption).

Abivax’s price drop following maintenance data likely reflects a faded M&A "perfection" premium. Obefazimod is no longer viewed as a flawless drug with placebo-like safety. The "malignancy conundrum" is an overhang that could continue to rear its ugly head in Phase 2b Crohn’s data next year and/or during the ulcerative colitis regulatory review later this year.

The biggest issue, in my view, was leading into maintenance data: ABVX's price. Before the results came out, Abivax's shares were trading over $120. But if you looked at my analysis from March, my fair value per share of Abivax was in the low 90s (with generous assumptions). That's the problem if you go into these data events without any context on what the valuation implies about market expectations."

3

3,048

Jun 13

One by one ALMOST all reversed by the current FDA. Way to go to restore trust

Jun 13

NEW: The FDA approved Sanofi's type 1 diabetes drug that was selected for the Commissioner's National Priority Review program. Staff and former CDER director Tracy Beth Høeg had previously disagreed on the approval.

statnews.com/2026/06/13/tepl…

4

5

24

8,153

Jun 12

$abvx don’t want to scare bulls because it makes my puts expensive. But FDA does not approve drugs based on pooled primary endpoints. Hope you can pump it back to $120. My puts will worth more than x5,000%.

2

1

1,161

Jun 11

Exclusive | OpenAI Considers Drastic Price Cuts, Anticipating War for Users With Anthropic - WSJ Token price war. wsj.com/tech/ai/openai-consi…

222

Jun 10

The FDA rejected bitopertin in February amid reports of skepticism from former CBER director Vinay Prasad, who has since departed the agency.

hubs.li/Q04kQvWZ0

2

18

4,937

Jun 10

I do, but won’t recommend chasing. Co’s competency is questionable.

245

Booked most profits from my bio put options but look for another entry point targeting the ones I have already highlighted with $xbi down to $100-110 level later this year.

1

435

Another way to interpret Trump’s AI investment: open AI weakness!

Jun 5

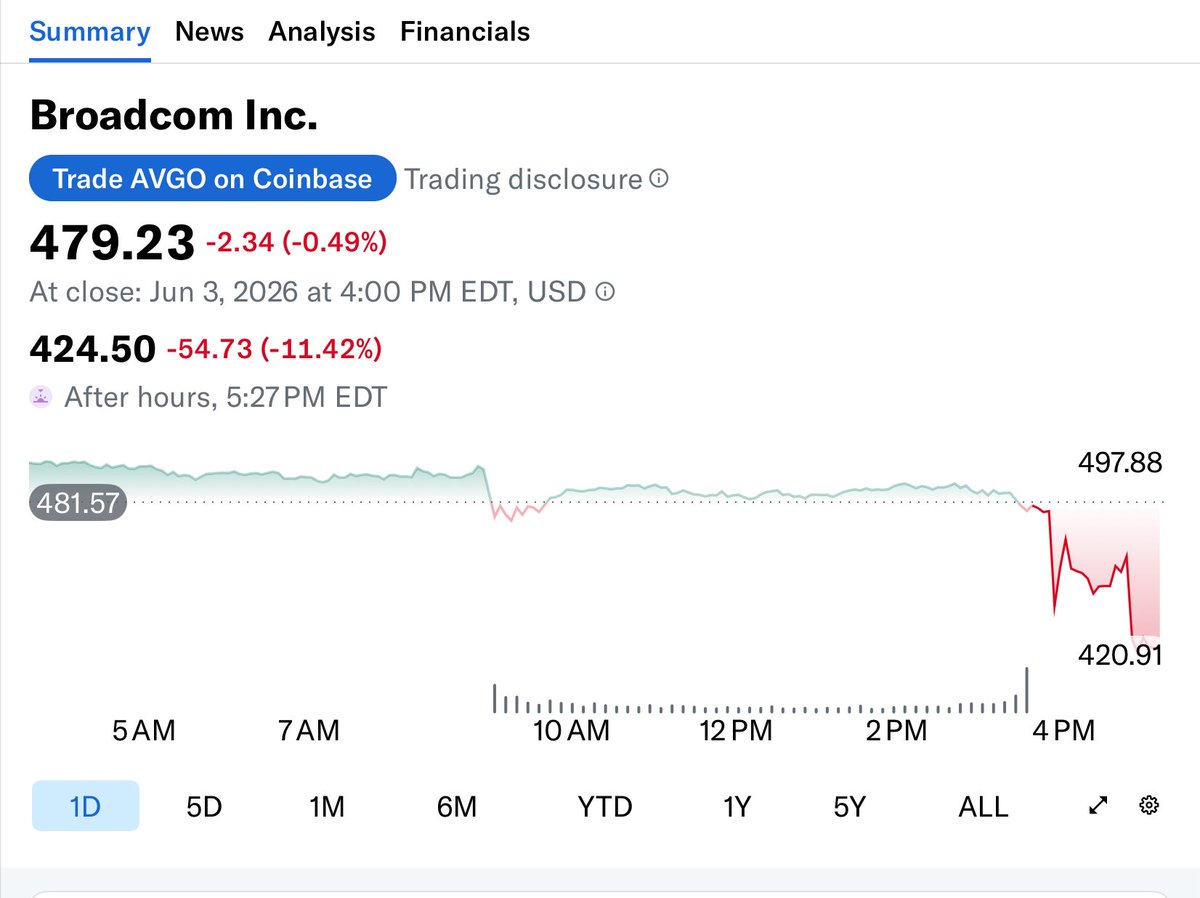

Absolutely brutal day for AI fantasies:

Nvidia $NVDA: down 6.2%

Broadcom $AVGO: down 7.92%

Coreweave $CRWV: down 7.07%

Nebius $NBIS: down 12.27%

Oracle $ORCL: down 9.59%

Worst of all?

OpenAI is rumored to be looking for government to invest, a huge sign of weakness.

Less than 24 hours after the S&P said no to fast-tracking, things are looking very different.

532

Could Americans Build Wealth Through AI? Why Trump May Be Considering Equity-Sharing Scheme

go.forbes.com/nj_fty

32

24

135

25,214

heavy recruitment toward Eastern European centers artificially depresses the background rate for malignancies. it sometimes creates a variance when the drug is later rolled out into US, W EU where patients are older, have longer-standing disease, and possess heavier pre-treatment

1

376

Deserves a read.

The FDA must provide consistent and predictable regulatory frameworks if the U.S. is to maintain its leadership in gene therapy, one of the most consequential therapeutic fields of our generation.

hubs.li/Q04kgFSv0

1

547