Powering The Future With Hyperlocal DePIN

Joined April 2024

- Tweets 100

- Following 11

- Followers 34

- Likes 196

48 Photos and videos

Pinned Tweet

10 Mar 2025

GM world 👋

Meet CipherNode.

We’re a next-gen Hyperlocal DePIN Network designed to revolutionize decentralized infrastructure.

Our vision is to build a new economy where individuals can earn by hosting DePIN nodes, powering a decentralized digital world.

4

2

9

734

CipherNode retweeted

11 Aug 2025

🚀 New Milestone for Blockchain & Cybersecurity Education

We’ve deployed a #Bitcoin Private Network on @cipher_node DePIN at SSIT, Tumkur - part of the Cybersecurity & Forensic Training Lab by @skillsda

1

1

4

78

10 Jul 2025

We had the privilege of hosting a hands-on Blockchain Bootcamp of @MOI_Tech at Mahatma Gandhi University, Nalgonda - empowering students to dive deep into the world of #decentralized infrastructure.

1

5

122

25 Jun 2025

Be the Enabler, not the Controller

Here's the link to the full fireside chat with the Founder and CEO of @MOI_Tech, Mr. @Arshasays :

youtu.be/8BR23_UKgm8?si=sUC1…

2

3

102

4 Jun 2025

The system needs to behave the same way for all the applications.

3

7

199

28 May 2025

🚨 Fireside Chat Speaker Unveiled!

We're excited to host Kamlesh Nagware, Co-Founder of FSV Capital and a TEDx speaker, for an exclusive session on the future of DePIN and blockchain innovation.

Kamlesh brings:

• 15 years of experience in tech & blockchain

• Founding member, India Blockchain Forum

• Co-chair, IEEE Blockchain Global

• Ex–TSC member, Hyperledger Foundation

📅 May 31 | 6 PM IST

📍 Twitter/X Spaces Google Meet

🎙️ 30-min Fireside Chat – compact, casual, and loaded with insights.

Don't miss this rare opportunity to hear from one of India’s leading blockchain minds.

1

30

23 May 2025

We’re kicking off our community engagement series with a special session featuring a leading voice in blockchain!

📅 May 31

🕕 6 PM IST

📍 Twitter/X Spaces Google Meet

🎙️ Format: 30-min casual yet insightful chat

Join us as we explore the evolving DePIN landscape and what it means for builders, devs, and the Web3 curious.

Stay tuned, speaker reveal coming soon 👀

2

48

22 May 2025

Hosted a Blockchain & DePIN bootcamp at @Bitsathyindia Coimbatore last Saturday, the energy was 🔥

From DePIN to hands-on @MOI_Tech sessions, the curiosity from students was next level.

Grateful for the warm welcome

2

9

183

20 Apr 2025

This isn’t just a webinar -it’s your chance to score an invite to MOI’s private dinner at #TOKEN2049 Dubai 🥂

Join us on Apr 24 to explore: 🧠 Context-driven crypto

🌐 What’s missing in Web3

🎟️ Win a seat at the table with @MOI_Tech's core team, VCs & builders

📍 Register now → lu.ma/ffmf0efb

🛫 Travel/accom not included – but the dinner’s on us

#Web3WithContext #TOKEN2049 #CryptoEvents #MOI

2

8

555

17 Apr 2025

Not another L2, bridge, or ZK talk.

This is a fireside chat with the OG @MOI_Tech's CEO on what’s missing in Web3: Context.

🗓️ Apr 24 | ⏰ 7 PM IST

🧠 Real talk on infra, identity, DAOs & the MOI token.

🎙️ Q&A open.

👉 Register here: lu.ma/ffmf0efb

3

6

141

President Trump just signed the first-ever crypto bill into law.

But what does it actually mean for DeFi, self-custody, and the future of crypto?

President Trump just signed the first-ever crypto bill into U.S. law — and it’s a major turning point. The bill officially repeals the IRS’s “DeFi broker rule,” a last-minute Biden-era regulation that would’ve forced decentralized platforms, protocols, and even smart contracts to collect and report user data like names, addresses, and gross proceeds to the IRS. That rule treated code like corporations — and devs like financial institutions — making privacy-preserving DeFi nearly impossible in the U.S. Under the new law, DeFi platforms aren’t classified as brokers just because they enable peer-to-peer transactions. There’s no mandatory KYC for protocols, no criminal liability for developers writing open-source code, and no surveillance built into self-custody tools. This isn’t just a regulatory rollback — it’s a clear declaration that the U.S. won’t crush innovation in digital assets. Combine that with this week’s DOJ memo clarifying that devs aren’t responsible for third-party actions on their code, and the signal is undeniable: crypto builders are safer, freer, and finally being heard. Huge win for innovation, privacy, and U.S. leadership in Web3.

3

7

431

8 Apr 2025

Another day

Another partnership &

This one's big. 🚀

We’re officially teaming up with @Central_DAO as our community partners.

Together, we're on a mission to build a community that beats with the rhythm of DePIN.

Here’s what’s coming your way:

- Bootcamps

- Hackathons

- Webinars

And more hands-on experiences in the world of decentralized infrastructure.

This is just the beginning and we’re building it with the community, not just for it.

If you're part of CentralDAO, drop a 🤝 in the replies so we can give you a proper welcome.

And for lightning-fast updates, hop into our telegram:

t.me/ciphernodeai

2

2

13

225

CipherNode retweeted

5 Apr 2025

Context Aware Blockchain- Interesting!! I want to check this out!!

lu.ma/62gvs9cf

#Blockchain #nodevalidators #Mining #Crypto #CryptoNews #tokenization #Tokenomics

1

2

46

2 Apr 2025

GM fam

We’ve officially joined hands with @pune_dao as our first community partners.

This is a major step toward building a community that beats.

Together, we’ll be rolling out:

- Bootcamps

- Hackathons

- Webinars

and more — all focused on the ever-evolving world of DePIN.

1

3

9

256

2 Apr 2025

Big things coming your way!!

If you’re part of the PuneDAO, drop a 🤝 in the comments, so that we can say 'hi'.

And don't forget to join our Telegram Channel for the fastest updates: t.me/ciphernodeai

1

3

115

CipherNode retweeted

1 Apr 2025

Exciting discussions with @skillsda on synergies with @ciphernodex !

We are exploring how we can scale decentralized infrastructure with real-world applications that solve critical challenges at scale.

Looking forward to building while driving meaningful innovation. Stay tuned!

1

2

4

85

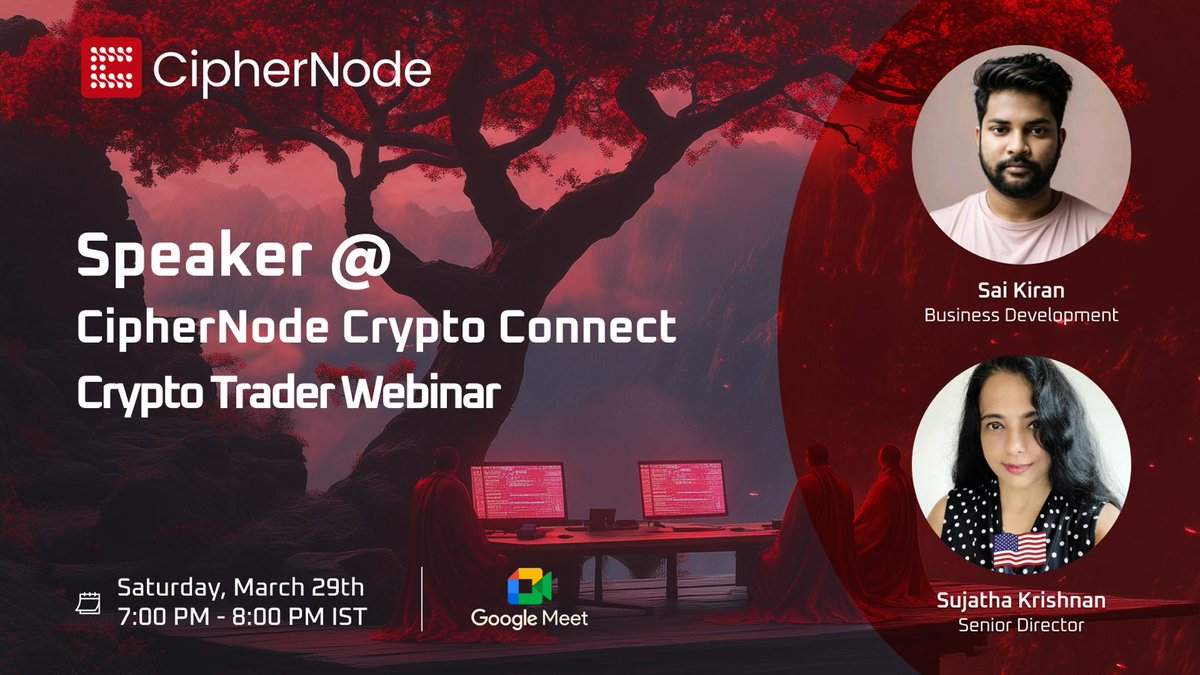

29 Mar 2025

Final Call (Few Hours Left)

LAST CHANCE: Your Passive Crypto Journey Starts Tomorrow

Today at [7 pm], you’ll discover:

• How to turn idle hardware into a token-earning machine

• The exact nodes paying right now (no guesswork)

1

1

32

29 Mar 2025

• Our step-by-step setup guide (even if you’re not techy)

Miss this = Miss your easiest crypto opportunity this year.

🔗 Register NOW → lu.ma/wk7pxwp8

(Doors close soon!)

19

28 Mar 2025

Node Hosting is Only for Tech Geeks With Expensive Gear

(Spoiler: That’s 100% false.)

You don’t need:

❌ A $10,000 server

❌ A coding degree

❌ 24/7 maintenance

1

1

2

77

28 Mar 2025

What you do need:

• Basic hardware (yes, even your old laptop might work)

• 1 hour to set it up (we’ll show you how)

• A webinar invite for Saturday where we break it all down!

🔗 Claim Your Spot → lu.ma/wk7pxwp8

1

1

16

28 Mar 2025

P.S. The biggest myth? That you’re "too late" to start. (You’re not.)

11