CI is a globally integrated proprietary AI/ML forecasting platform for finance and planning automation. Stop Guessing. Start Planning. Succeed.

Joined March 2015

- Tweets 12,205

- Following 1,327

- Followers 5,009

- Likes 6,431

7,918 Photos and videos

Pinned Tweet

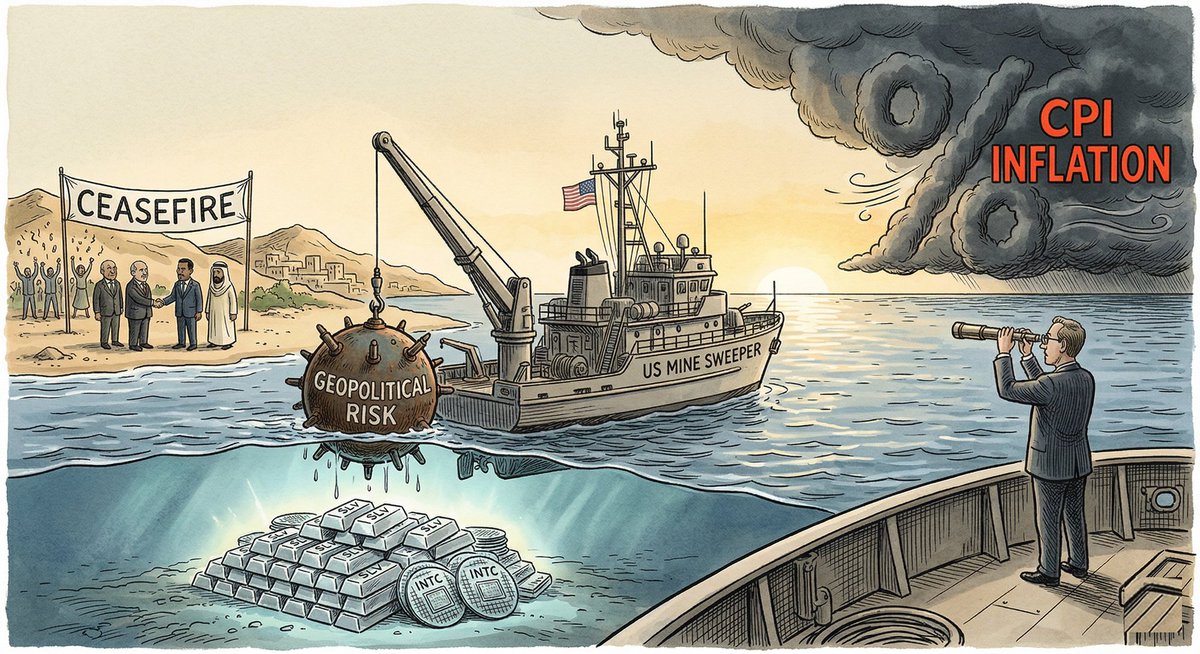

Geopolitics and market volatility are creating a perfect storm of anxiety. But while others are panicking over the headlines, drown out the noise. Don't panic. Stop relying on outdated indicators. More about CI Markets here: completeintel.com/markets

1

4

4,083

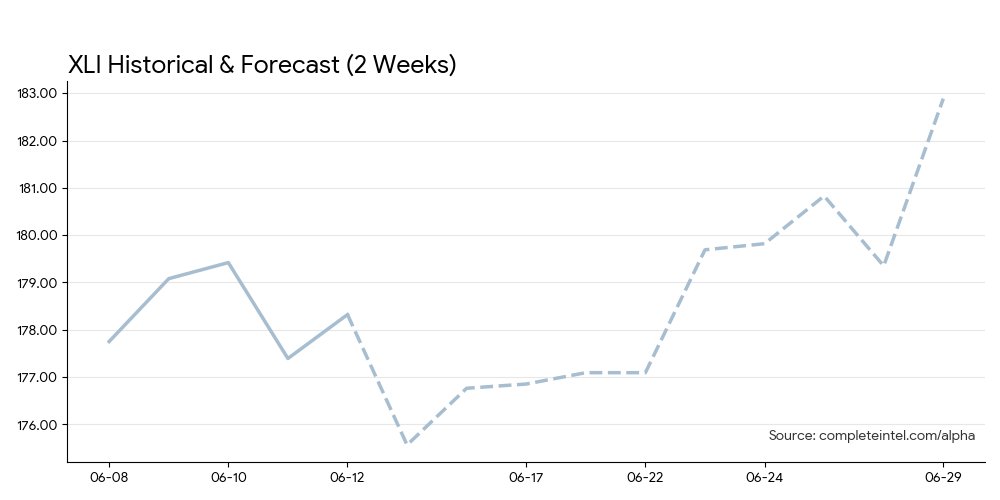

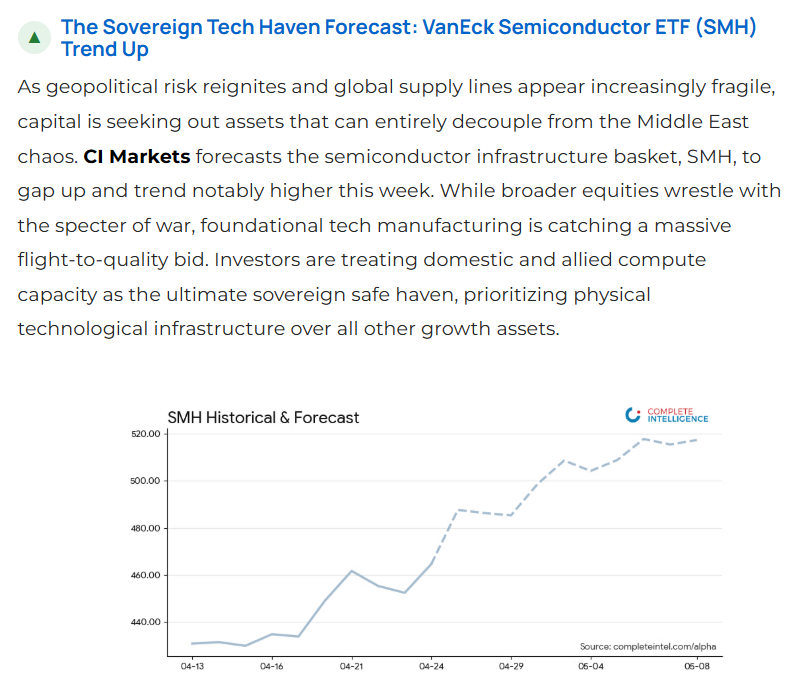

CI Weekly Outlook: Beyond the Hype Cycle

📈 INTC 🔼 (Flight to Legacy Quality)

🏭 XLI 🔼 (Industrial Rotation Breakout)

🛢️ CL=F 🔽 (Geopolitical Risk Premium Dropping)

completeintel.com/weekly-out…

2

1,303

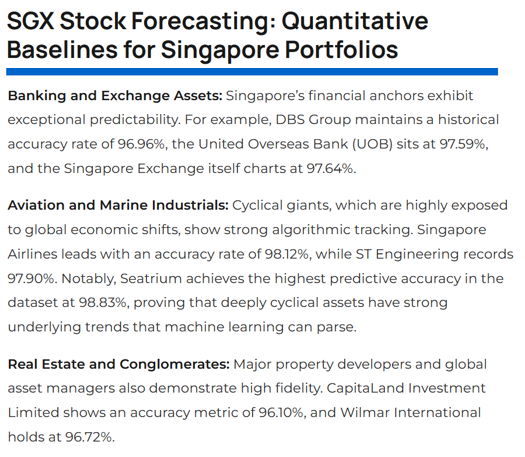

Our AI-driven models hit a 94.3% average accuracy baseline tracking SGX blue chips. CI Markets Free covers 45 individual Singapore stocks - including DBS, UOB, and Seatrium - to remove emotional bias. Learn more here: completeintel.com/sgx-stock-…

ALT $D05, $U11, $S68, $C6L, $S63, $5E2, $9CI, $F34, SGX, D05, U11, S68, C6L, S63, 5E2, 9CI, F34

147

The Weekly newsletter is out!!!

Jun 6

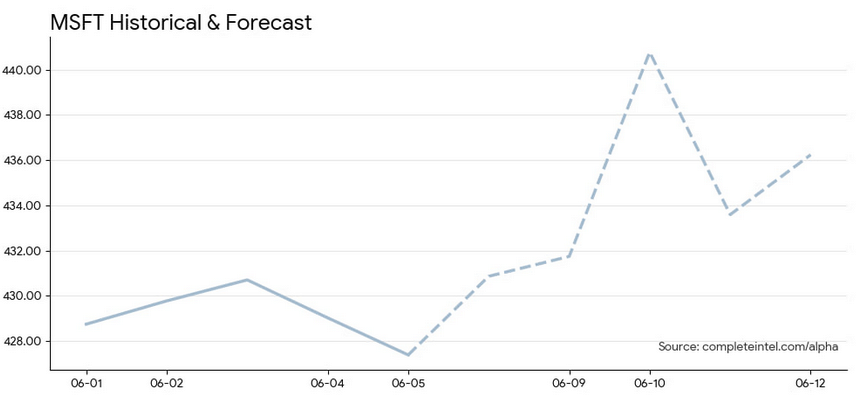

CI Weekly Outlook (Strategic Rotation 🏢🛢️)

The market is transitioning beyond the AI hype cycle. As speculative tech faces a reality check, capital is rotating aggressively toward proven mega-caps and energy commodities.

📈 MSFT🔼 (Flight to Quality)

🛢️CL=F🔼(Energy Persistence)

🪙GC=F🔽 (Defensive Consolidation)

Wildcard: Will the White House AI summit bring new regulations? 🃏

completeintel.com/weekly-out…

1

186

Complete Intelligence retweeted

Try CI Markets Free today. Major currency pair forecasts and Singapore SGX stock forecasts free. If you like it, upgrade to Plus or Premium for 1,200 assets with a new forecast each week. completeintel.com/free

3

2

1,694

Complete Intelligence retweeted

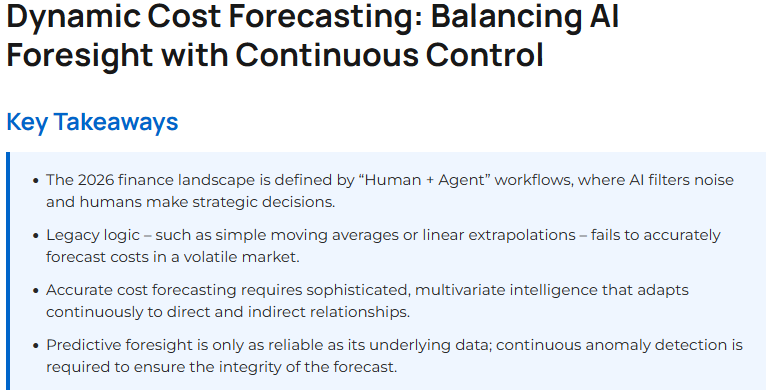

New: Dynamic Cost Forecasting: Balancing AI Foresight with Continuous Control

completeintel.com/dynamic-co…

1

1

1,926

CI Weekly Outlook (The Computex Showdown 💻⚡)

The force of the AI super-cycle is colliding with the immovable object of rising interest rates.

📈 $AMD 🔼Historic Outlier Setup

🖥️ $NVDA ↔️Incumbent Volatility

📉 $FVX 🔼Yield Reality Check

completeintel.com/weekly-out…

2

1,469

Complete Intelligence retweeted

May 23

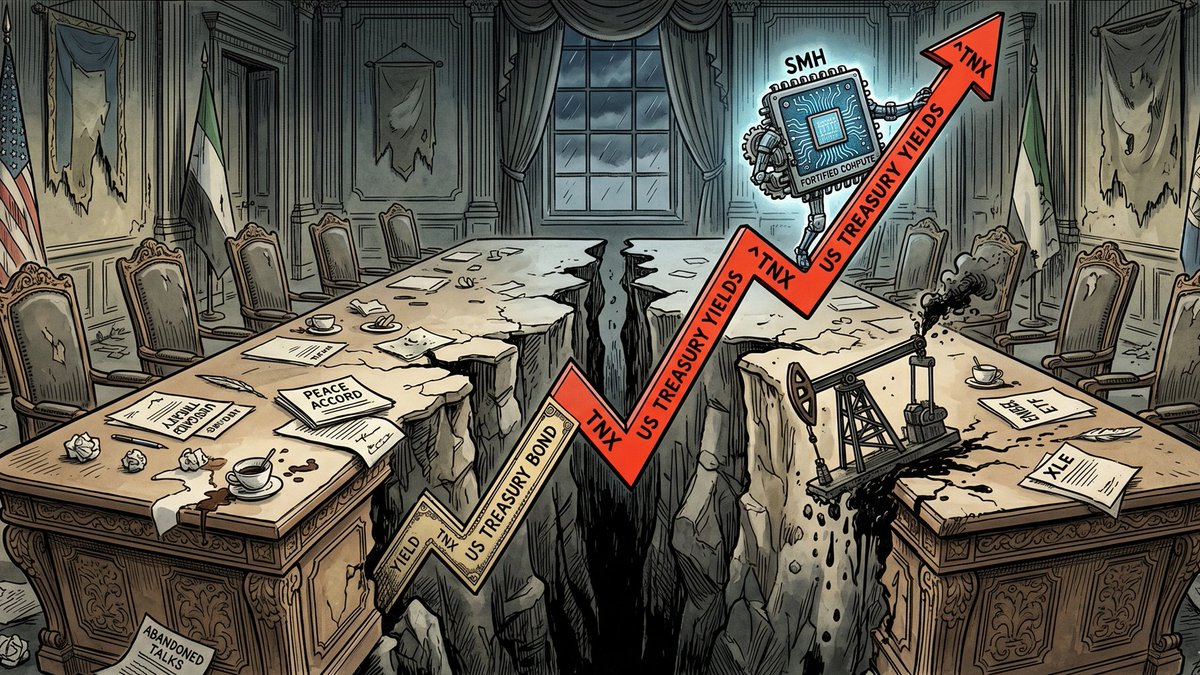

CI Weekly Outlook (The Yield Squeeze 📈🛢️)

The market is bifurcating. Rising Treasury yields are providing a tailwind for energy while acting as a heavy ceiling for high-growth tech valuations.

📈 ^TNX 🔼 (Yields Climb)

🛢️XLE 🔼 (Geopolitical Supply Risk)

🌐XLK 🔽 (Tech Valuation Headwind)

completeintel.com/weekly-out…

1

1

11

1,123

The newsletter is out!

May 23

CI Weekly Outlook (The Yield Squeeze 📈🛢️)

The market is bifurcating. Rising Treasury yields are providing a tailwind for energy while acting as a heavy ceiling for high-growth tech valuations.

📈 ^TNX 🔼 (Yields Climb)

🛢️XLE 🔼 (Geopolitical Supply Risk)

🌐XLK 🔽 (Tech Valuation Headwind)

completeintel.com/weekly-out…

173

Complete Intelligence retweeted

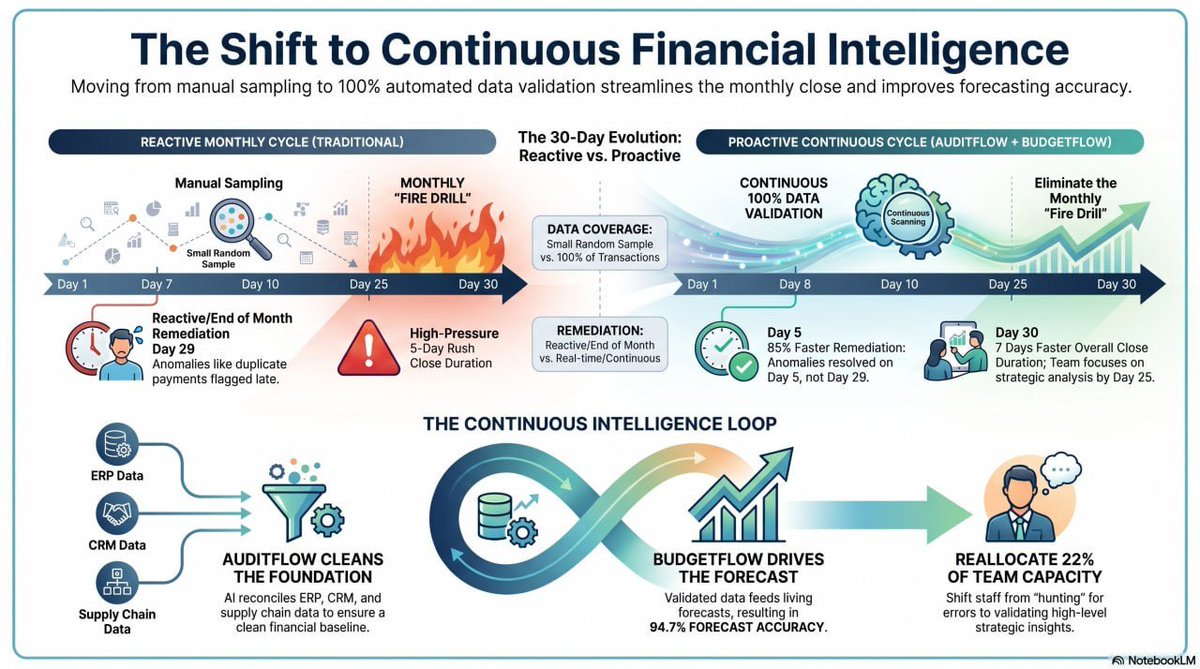

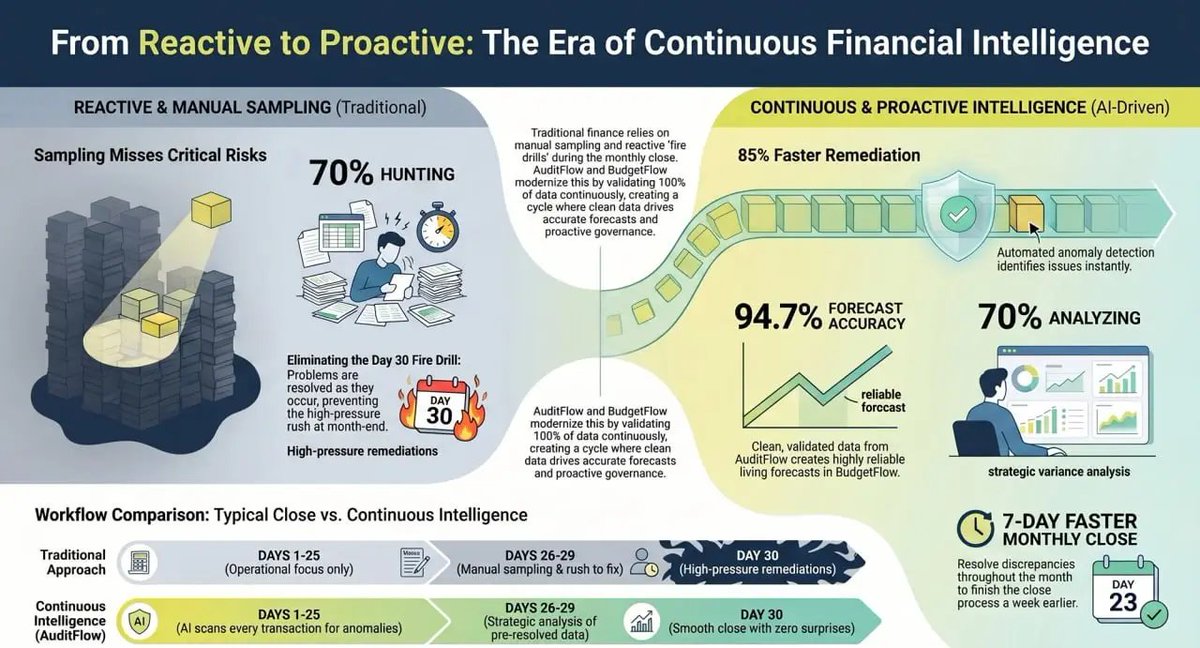

Explainable AI in Finance for Accounting and Audit Teams

➡️Finance leaders can't risk blind trust in a black box.

➡️Explainable AI is a compliance mandate.

➡️See how AuditFlow and BudgetFlow bring transparency to audits and forecasting.

completeintel.com/explainabl…

4

7

905

Complete Intelligence retweeted

May 18

🎙️Here's my interview on Singapore's CNA 938 from earlier today. Hope you enjoy it! completeintel.com/cna938-rew…

May 17

🎙️ I'll be on Channel News Asia later today discussing Kevin Warsh and changes at the Fed. Notes follow.

==========

If you like this, try our daily interval forecasts with CI Markets Alpha completeintel.com/alpha

==========

Most political Fed Chair?: "The idea that Kevin Warsh is the 'most political Fed Chair in history' is a classic case of historical amnesia.

The Reality: The confirmation process was hyper-political, but the man is a deeply credentialed crisis-manager taking over at a brutal economic moment.

The Kevin Warsh Snapshot

- The Resume: Former Morgan Stanley M&A banker, Bush White House economic advisor, and the youngest Fed Governor in history at age 35.

- The Crisis Credentials: He was Ben Bernanke’s right-hand man and primary Wall Street liaison during the 2008 financial meltdown.

- The Mandate: He was confirmed on a razor-thin, highly partisan 54-45 vote (with John Fetterman as the lone Democrat crossing the aisle) to bring "regime change" to a Fed that has let inflation sit above target for five years.

"The Most Political Fed Chair Ever?"

- The Partisan Split is New, the Politics Aren't: What's historically unprecedented is the 54-45 confirmation vote. That's Washington's politics, not Kevin Warsh's.

- The Nixon-Arthur Burns Era: If you want real political manipulation, look at Richard Nixon, who openly bullied Fed Chair Arthur Burns into keeping rates low for the 1972 election, triggering the stagflation of the '70s.

- The LBJ Ranch Shove: Lyndon B. Johnson literally flew Fed Chair William McChesney Martin to his Texas ranch and physically shoved him against a wall for raising rates during the Vietnam War. That is political pressure. Warsh answering tough questions in a Senate hearing is standard D.C.

- The FDR Precedent: FDR explicitly designed the modern Fed structure to finance the New Deal and keep interest rates pegged low during WWII. The Fed has always lived at the intersection of economics and politics.

The Fed's Formal vs. Functional Independence

- Formal Independence is the Armor: Formally, the Fed is structurally independent. Governors have 14-year terms to outlast presidents, and they fund themselves so Congress can’t hold them hostage.

- Functional Interdependence is the Reality: Functionally, the Fed lives in the real world. They don't operate in a vacuum. If a President and Congress pass sweeping tariffs or massive spending bills, the Fed is forced to react with monetary policy. It’s an unavoidable dance.

- Why Warsh Fits: Warsh’s background in the White House and on Wall Street doesn't make him a political puppet. It means he understands how fiscal and monetary policy collide. In an economy facing sticky 3.8% inflation and global conflict, that kind of realism is exactly what we need, not an academic ivory tower.

The "Regime Change" Tools (Beyond Just Interest Rates)

- Warsh has made it clear that the Fed under his watch won’t just rely on tinkering with interest rates. He wants a structural overhaul:

- Aggressive Balance Sheet Shrinkage (Faster QT): Warsh wants to aggressively wind down the Fed’s $6.6 trillion balance sheet. He believes quantitative easing (QE) should be restricted to true emergencies, arguing that the Fed’s massive bond-buying has blurred the line between monetary policy and government deficit spending.

- Killing the "Dot Plots" and Forward Guidance: Expect a much quieter Fed. Warsh has openly criticized the Fed’s habit of trying to move markets via "rolling incantations" and constant verbal hints. He wants to scrap or significantly reduce forward guidance (including the famous "dot plots") to restore the Fed's element of surprise and flexibility.

- Rewriting the Inflation Playbook: He rejects the old Fed models that blame wage growth and employment for inflation. Instead, Warsh blames excessive government spending and money-supply growth. Expect him to look at inflation through a forward-looking lens, heavily factoring in AI-driven productivity gains.

The New Fed-Treasury Accord (The 1951 Sequel)

- The historic 1951 Treasury-Fed Accord originally freed the Fed from its obligation to keep government borrowing costs artificially low after WWII. Warsh and Treasury Secretary Scott Bessent want a modern sequel.

- The Goal: To reset the boundaries between the Fed and the Treasury in an era of massive national debt.

- How it Works: Rather than the Fed acting as a "general-purpose agency" that hoards long-term government debt, a new accord would narrow the Fed's footprint. The Fed would shift its holdings toward shorter-term Treasuries and step out of the long-term bond market, forcing Congress and the private sector to price long-term risk properly.

The Impact on the US Dollar

- Structurally Bullish: Speeding up balance-sheet reduction drains money supply from the banking system. Fewer dollars in circulation naturally makes the dollar stronger.

- Credibility Boost: By refocusing on money supply and a narrower mission, Warsh signals to global markets that the U.S. is serious about long-term inflation discipline, reinforcing the dollar’s status as the global reserve currency.

- Short-Term Choppiness: Because Warsh wants to kill forward guidance, currency traders will have less predictability. Expect brief spikes in dollar volatility around Fed meetings as the market adjusts to a less talkative central bank.

The Impact on the US Economy

- The "Interest Rate Twist": Warsh’s strategy could create a unique economic dynamic. He favors cutting short-term interest rates to relieve small businesses and consumers, but his aggressive balance sheet cuts could push long-term bond yields (like the 10-year Treasury) higher.

- The Real-World Effect: This could keep mortgage rates and corporate bond costs somewhat elevated, even while the Fed lowers the baseline short-term policy rate.

- The AI Productivity Bet: Warsh is banking on an artificial intelligence boom to spark a massive productivity miracle. If AI successfully drives down production costs across the economy, it gives him the perfect runway to lower rates without reigniting inflation.

- Passing the Baton to the Private Sector: Ultimately, Warsh wants to shift economic momentum away from government stimulus and central bank interventions, forcing the private sector to step up as the primary engine of American growth.

1

9

1,504

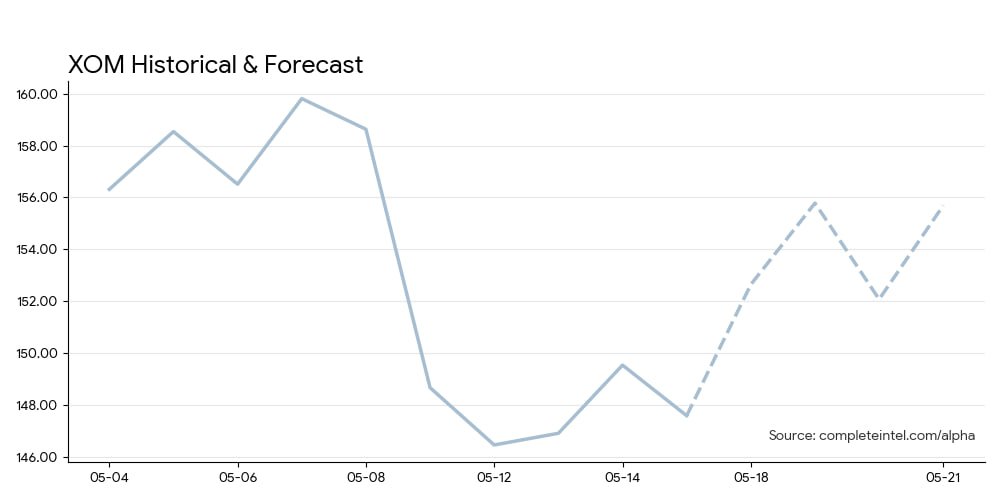

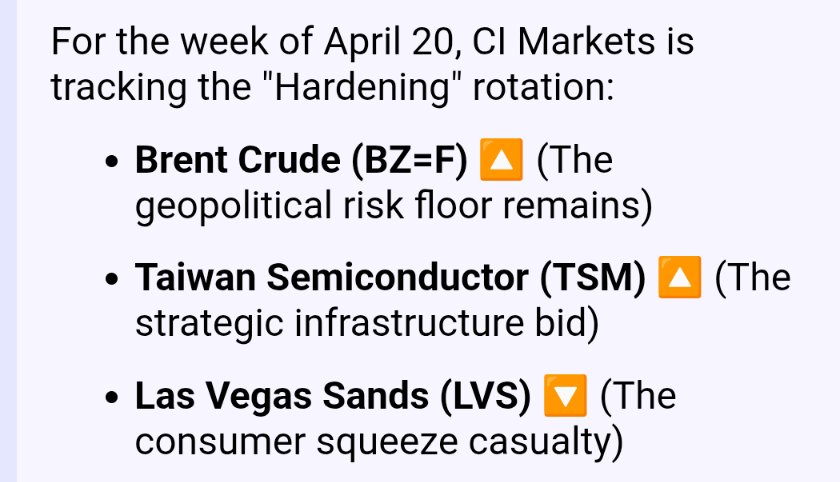

CI Weekly Outlook (The Geopolitical Pivot 🇺🇸🇨🇳)

The market is actively pricing in a "trade thaw," lifting emerging markets and stabilizing currencies.

🌏 $EEMA 🔼 (Emerging Market Surge)

💱 $USDCNY 🔽 (Yuan Strengthens)

🛢️ $XOM ↔️ (Energy Volatility)

completeintel.com/weekly-out…

1

3,003

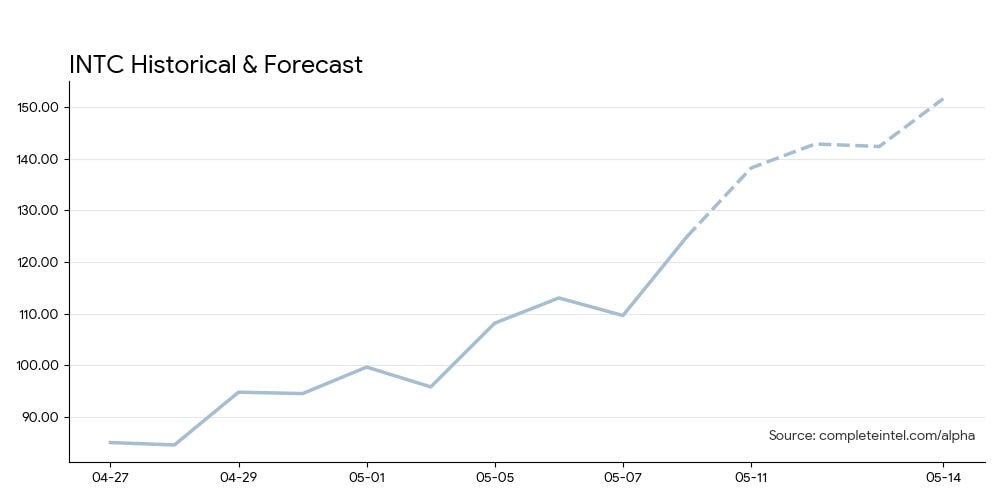

CI Weekly Outlook (The Tech Decoupling 💻🚀)

An Apple-Intel chip deal is reshaping the semiconductor space, triggering a breakout across tech.

📈 INTC 🔼 (Foundry Shockwave)

💾 TSM 🔼 (AI Super-Cycle Capacity)

🌐 XLK 🔼 (Broad Tech Breakout)

completeintel.com/weekly-out…

2

5,289

Why does your finance team spend 22% of capacity hunting for problems?

AI does the hunting. Your team does the validating.

85% faster remediation. 7-day faster close.

Book a demo 👇

completeintel.com/auditing-s…

1

1,520

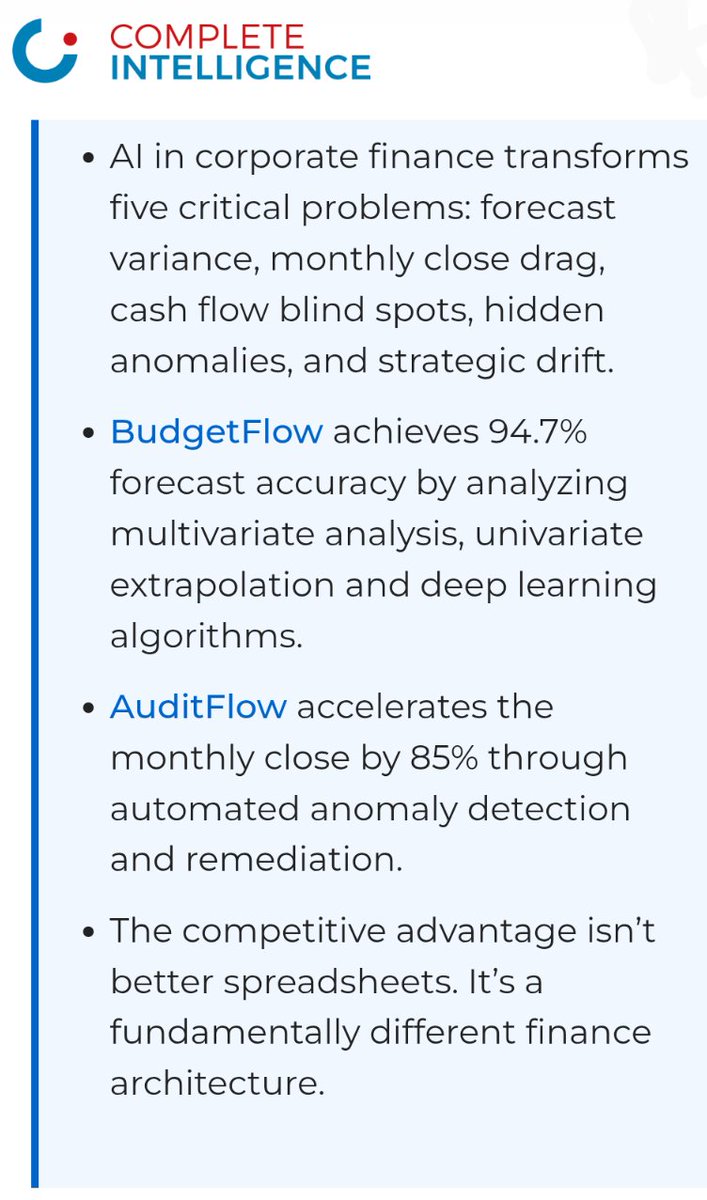

AI in Corporate Finance: 5 Problems It Solves That Spreadsheets Can’t completeintel.com/ai-in-corp…

1

4

734

Weekly newsletter is out. It's the first one with our daily interval charts. Enjoy!

May 2

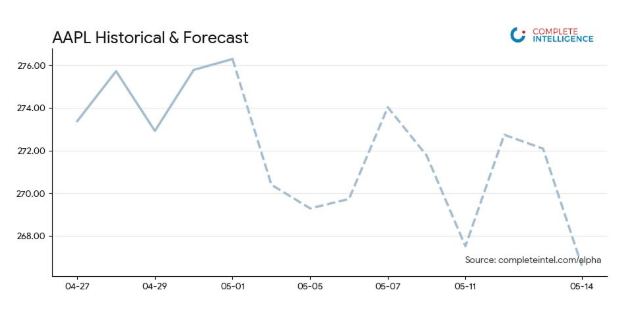

CI Weekly Outlook (Macro Divergence 📉💻)

🏦The Fed is trapped by sticky inflation, and the bond market is testing Washington. Capital is fleeing long-duration yields and hiding in the "Sovereign Balance Sheets" of Big Tech.

📉 TLT 🔽 (Yield Shock Casualty)

🍎 AAPL ↔️ (Sideways Buyback Haven)

🥇 GC=F 🔽 (Rate-Trapped Safe Haven)

Wildcard: Will weak Treasury auctions finally crack the tech rally? 🃏

Read our weekly note & see the charts here: completeintel.com/weekly-out…

2

4

974

👇 This is a HUGE change. You can now see the daily fair value forecasts for the next 10 trading days for items in our CI Markets newsletter. FREE. Sign up!

May 1

🚨BIG

We're adding our DAILY INTERVAL FORECAST CHARTS to our CI Weekly Newsletter! We've updated this week's with daily charts and you'll see these in all future newsletters. Check it out and subscribe:

completeintel.com/weekly-out…

1

1

3

1,028

Our CEO, Tony Nash, Joined @CNA938 to discuss the Big Tech AI rally vs. the Fed’s "Defensive Hold." 📉

We break down the Q1 "Growth Illusion" and how fiscal dominance is squeezing private capital.

🎙️ Listen (13 min): completeintel.com/big-tech-a…

1

1,167