AI-powered analytics platform for equity research. Sign up to start using AI for stock market analysis.

Joined August 2024

- Tweets 3,298

- Following 211

- Followers 5,099

- Likes 695

1,074 Photos and videos

Pinned Tweet

Jun 9

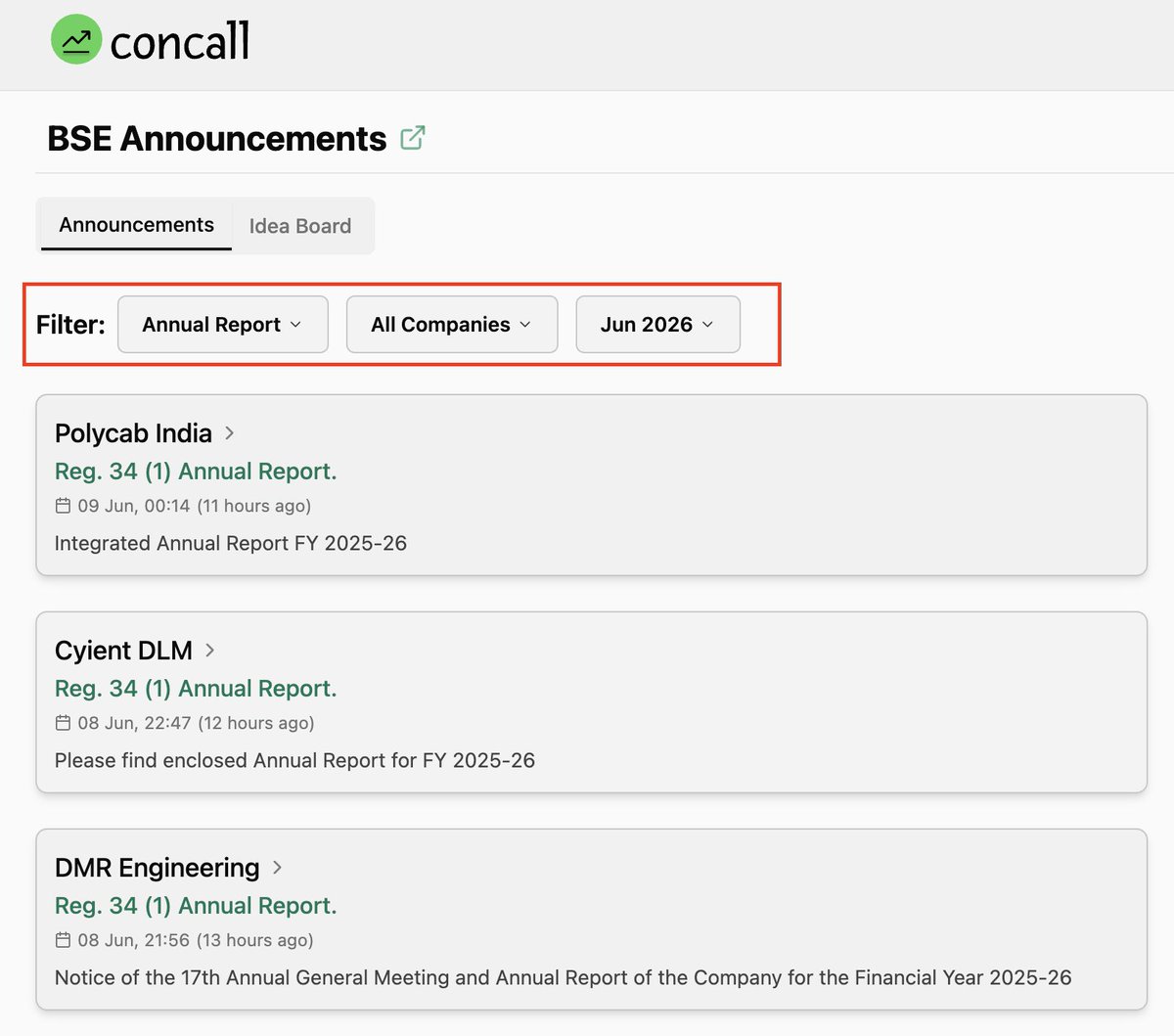

FY25-26 Annual Reports are starting to come in.

We've made it easier to track and analyse them:

• Use the Annual Reports filter to find newly released reports in one feed

• Read concise summaries to get the key highlights before diving into the full report

• Track companies publishing their first annual report post-listing

Links in the thread 👇

4

6

31

4,255

Sudeep Pharma closed FY26 on a solid note and is now expanding both its existing businesses and a new battery materials vertical.

Let's deep dive into the latest concall to understand the opportunity ahead 👇

Sudeep Pharma today operates across two businesses:

• Pharma, Food & Nutrition Ingredients (56% of FY26 revenue)

• Specialty Ingredients (44% of FY26 revenue)

And it's building a third segment, which is Battery Materials.

FY26 revenue grew 28% to ₹642 crore, while net profit grew 25% to ₹174 crore.

The core business is entering a new phase.

Management said the newly commissioned Greenfield facility removes a key capacity bottleneck and can support ₹1,000-1,200 crore of revenue from the existing Pharma, Food, Nutrition and Specialty Ingredients businesses without any major additional capex.

That's nearly 2x the current revenue base.

The fastest growing segment continues to be Specialty Ingredients.

This segment grew 62% in FY26 and now contributes 44% of revenue versus 34% a year ago.

The company is also expanding into higher-value products such as bisglycinates, which are gaining approvals in North America and Europe. Management estimates the global market opportunity for this category alone at roughly $1 billion.

These products carry significantly higher realizations than the traditional portfolio and could gradually improve both growth and profitability.

Management also expects the Pharma, Food & Nutrition segment to grow faster in FY27 as customer approvals for the new facility come through and recent price increases start flowing into revenues.

One area investors should watch is margins.

Despite strong revenue growth, EBITDA margins declined from 37.8% to 34.6% during FY26 as the company invested in new facilities, overseas teams, inventory and future growth initiatives. Management expects these investments to start contributing more meaningfully going forward and margins return to the 37-38% level in FY27.

Then comes the newest vertical: Battery Materials.

The first 25,000 MT battery-grade iron phosphate plant remains on track for commissioning in April 2027.

What's notable is that customer traction is already building before the plant goes live.

• 42 customers engaged globally

• 22 in lab validation

• 14 in pilot-scale evaluation

• 6 in active offtake discussions

• Initial orders of ~700 MT already received

Management's long-term ambition is even bigger.

The company plans to build 100,000 MT of battery-grade iron phosphate capacity with total capex of around ₹600 crore.

At full utilization, management estimates revenue potential of roughly ₹1,600-1,800 crore from the battery business alone.

Put differently:

- Current revenue base: ₹642 crore

- Potential from existing businesses: ₹1,000-1,200 crore

- Potential from battery materials: ₹1,600-1,800 crore

The interesting part is that the battery opportunity alone could eventually become larger than Sudeep Pharma's entire business today in terms of revenue. However, it is expected to operate at lower margins than the company's existing business.

The key monitorables now are execution and margins, especially in the battery materials business.

Disclaimer: This post is for educational purposes only. Not a buy or sell recommendation.

#SUDEEPPHRM #Q4FY26 #Concall

1

62

Link to Sudeep Pharma Q4 FY26 concall & insights:

concall.in/company/239342/an…

Disc: Not a buy / sell recommendation. Only for informational purposes.

31

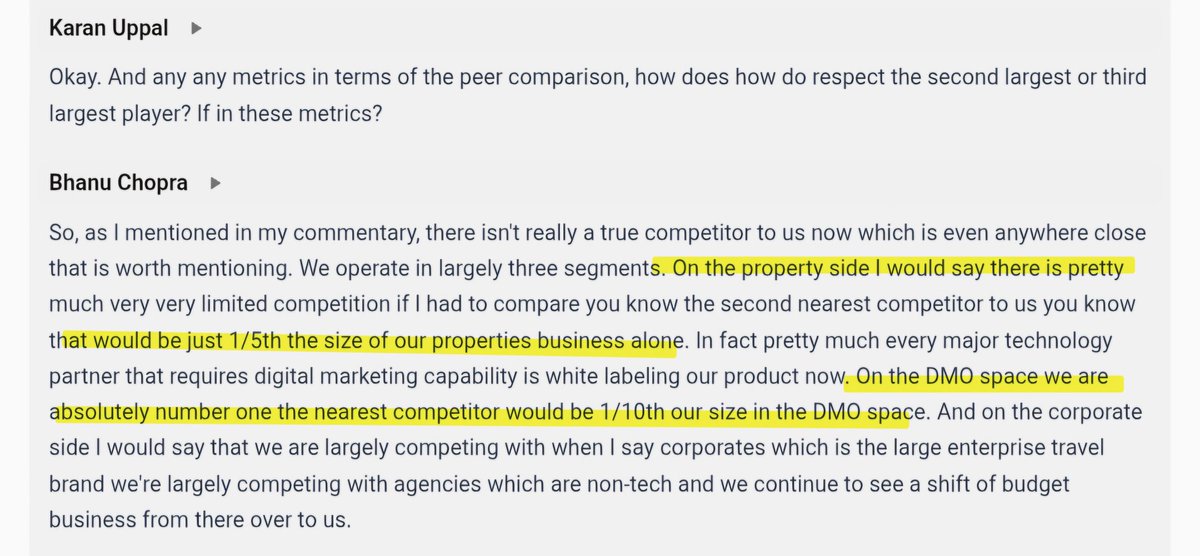

Avanti Feeds expects a potential refund of USD 15–20 million following the invalidation of U.S. tariffs.

Management said that, as the importer of record, the refund process has already been initiated.

1

7

733

Link to Avanti feeds Q4 FY26 concall:

concall.in/company/112573/an…

Disc: Not a buy / sell recommendation.

1

2

476

concall.in retweeted

14h

RateGain - From SaaS Player to AI-Powered Travel Giant 🔥

FY26 was the year RateGain changed its identity. Targeting $1 Bn revenues by FY31. 🚀

The company completed the Sojern acquisition, integrated Adara, and built what it claims is the world's largest travel intent data platform with 320 data partners, 1.5B travel graph IDs and 13,000 customers.

The goal is clear: become the operating system for travel revenue growth.

🔶️ Building the Moat

• The Sojern-Adara integration is complete, cost synergies have already reached $15M annually, and customer migration to a unified platform is on track by Q2 FY27

• Management believes no competitor matches its combination of:

>> Travel intent data

>> Distribution infrastructure

>> AI-powered commercial intelligence

🔶️ AI Is Becoming the Product

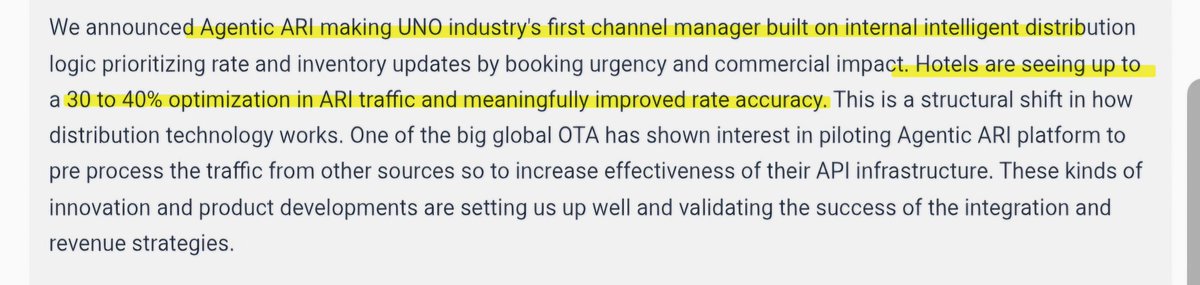

• RateGain is moving from software tools to AI agents

• Early outcomes:

>> UNO VIVA: Up to 40% higher hotel revenues

>> AI Concierge: 300% increase in ancillary revenue and 75% higher NPS

>> Agentic ARI: 30-40% reduction in distribution traffic

>> AI agents being built for marketing, revenue management and distribution workflows

🔶️ Growth Engines Firing

• Martech remains the biggest opportunity, driven by Sojern and Adara

• Distribution is evolving beyond connectivity with launches like Rate IQ, Agentic ARI and RG Pay

• DaaS continues winning marquee airline customers including Singapore Airlines, Vietnam Airlines, Philippine Airlines, Air Serbia and others

🔶️ Stronger Balance Sheet

• Repaid $31.5M (25.2%) of acquisition debt

• Net debt reduced to ₹722 Cr

• Cash balance at ₹199 Cr

• Debt-free target by FY28

🔶️ FY27 - Monetization Begins

Guidance suggests the next phase is execution:

• Revenue: ₹3,000-3,100 Cr

• Growth: 65-70%

• Organic Growth: 12-15%

• EBITDA: ₹650-700 Cr (21.5-22.5% margin)

• DaaS growth: 10-14%

• Martech growth: 12-15%

• Sojern expected to grow 30%

🔶️ Key Takeaway

FY26 was about assembling the pieces - data, AI, customers and global scale. FY27 is about monetizing them.

With a massive travel-data moat, accelerating AI adoption, 13,000 customers and improving cash flows, RateGain is positioning itself for its stated ambition of becoming a $1B revenue company by FY31. 🔥

Src - @concall_in

👉 Follow @vishan_29 for more updates.

🔴 Disclaimer: No recommendation. For educational purposes only.

3

33

2,018

Jun 13

Afcom Holdings grew revenue 2.4x and net profit 3.3x in FY26. Management says FY27 revenue could be "much more than double" as long-awaited fleet expansion finally begins to take shape.

Let's deep dive into Afcom's Q4 FY26 earnings call to understand the company's expansion plans.

The company delivered ₹587.7 crore in revenue and ₹121.9 crore in net profit during FY26, with operating cash flow turning positive at ₹36 crore.

Q4 was particularly strong, with revenue up 88% and profit up 73%, making it one of the best quarters in the company's history.

Part of that strength came from disruptions in Middle East cargo routes, which triggered a surge in charter demand. Afcom operated 602 flights in Q4, including 415 charter flights, helping move cargo stranded by reduced airline capacity.

Interestingly, these results were achieved despite capacity constraints.

For most of FY26, Afcom operated with only two aircraft while waiting for fleet additions. Earlier growth targets had to be revised because aircraft induction timelines slipped. Yet the company still delivered record revenue, record profits and over 81% aircraft utilization.

That explains why almost every investor question focused on fleet expansion.

The third aircraft is now operational. The fourth and fifth aircraft are expected before next quarter.

Management indicated that even on conservative assumptions, simply adding planned capacity should support revenue well beyond current levels because demand continues to exceed available aircraft supply.

Afcom has already raised capital through a preferential issue and QIP to fund four Boeing 777 freighters.

Management stated that financing for the entire expansion plan is in place and no additional fund raise is currently required. The first wide-body aircraft is expected around the end of calendar 2026, with the full planned fleet targeted over the following period.

Importantly, each Boeing 777 can generate roughly 3x the revenue of the current Boeing 737 freighters, even using conservative load assumptions.

Investors also pressed management on rising fuel prices and geopolitical uncertainty. The response was that fuel costs are largely passed through via fuel surcharges, while the newly acquired designated carrier status provides fuel tax benefits that partially offset cost inflation.

The bigger question for FY27 is now execution: can Afcom bring aircraft into service on schedule and convert its funded expansion plan into revenue growth?

The key metric to watch is It's fleet expansion and utilisation to achieve projected growth.

Disclaimer: This post is for educational purposes only. Not a buy or sell recommendation. Do your own research.

#Afcom #Q4FY26 #Concall

2

1

14

4,501

Jun 13

Link to Afcom Holdings' Q4 FY26 concall recording, transcript & insights:

concall.in/company/314657/an…

Disc: Not a buy / sell recommendation. Only for informational purposes.

1

563

Jun 13

JSW Energy to acquire 100% stake in Maruti Clean Coal and Power Ltd. for an enterprise value of ₹1,410 Cr.

MCCPL operates a 300 MW thermal power plant and reported FY26 revenue of ₹787 Cr.

The acquisition supports JSW Energy's journey towards its 30 GW capacity target by 2030.

1

15

1,357

Jun 13

Link to track acquisition updates:

concall.in/announcements/ide…

Disc: No buy / sell recommendations.

3

368

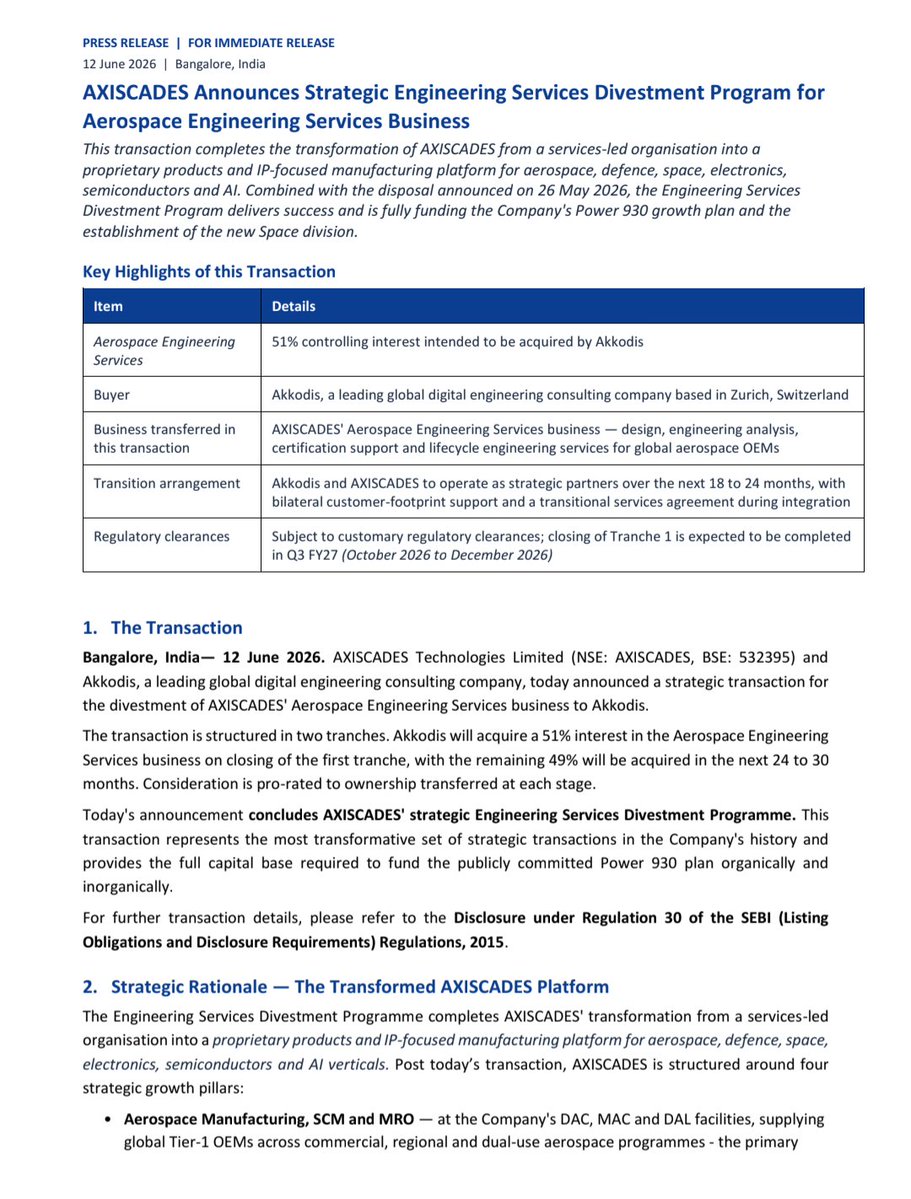

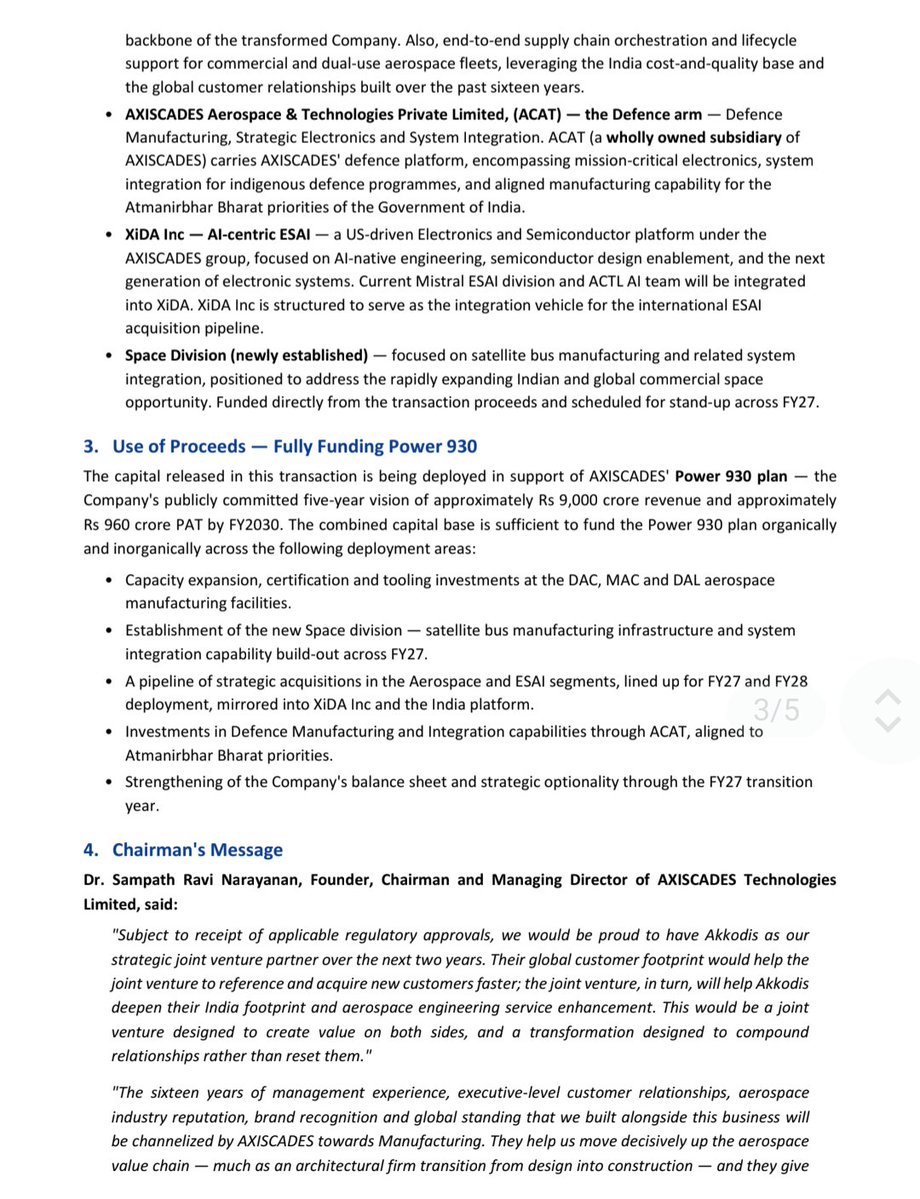

Jun 12

AXISCADES to divest a 51% controlling stake in its Aerospace Engineering Services business to Akkodis, unlocking capital to fund its Power 930 plan and newly launched Space division.

Management is reiterating its vision to achieve ₹9,000 Cr revenue and ₹960 Cr PAT by FY30.

The transaction will be completed in two tranches, with closing expected in Q3 FY27.

1

4

31

2,904

Jun 12

Link to track divestment announcements:

concall.in/announcements/ide…

Disc: No buy / sell recommendations.

521

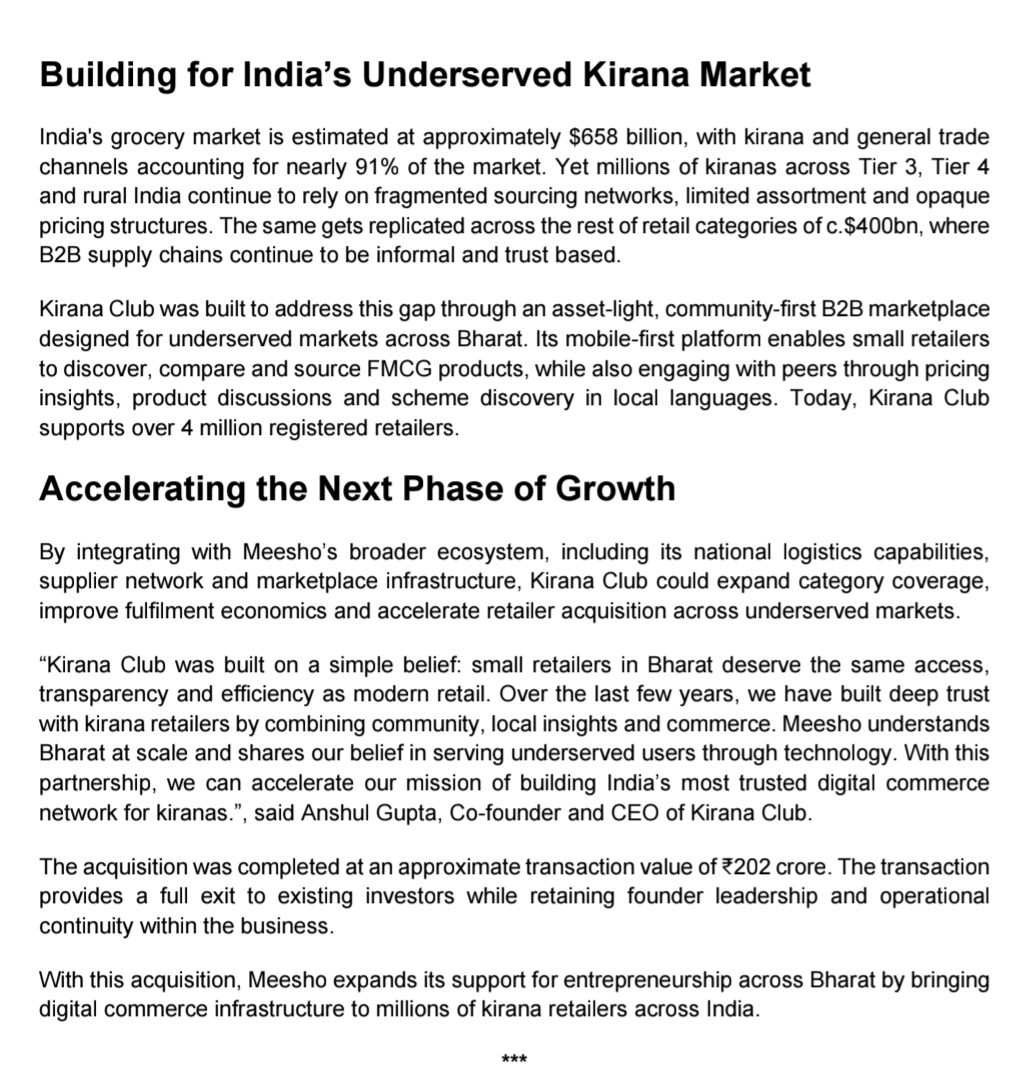

Jun 12

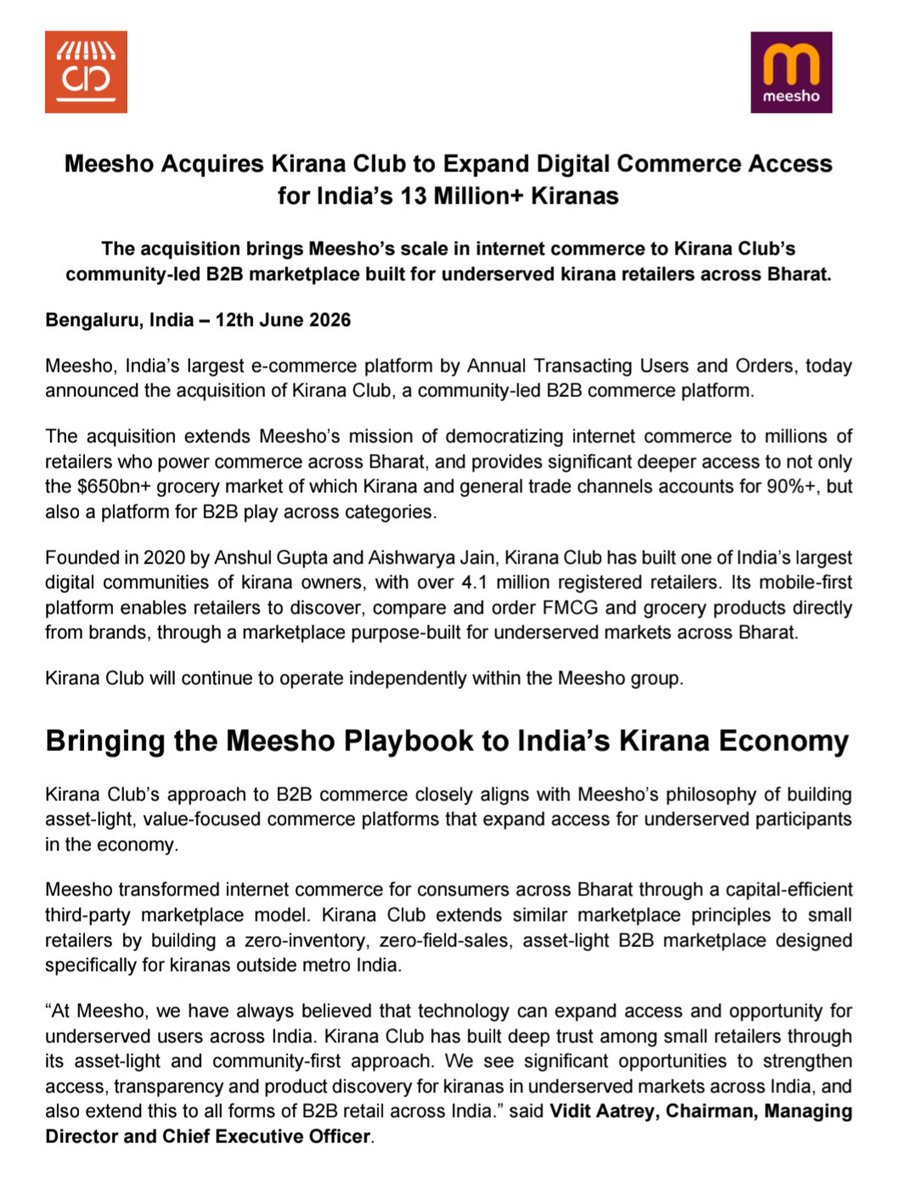

Meesho acquires Kirana Club for approximately ₹202 crore to expand digital commerce access for India's 13 million kiranas.

1

11

995

Jun 12

Link to track acquisition updates:

concall.in/announcements/ide…

Disc: No buy / sell recommendations.

451

Jun 12

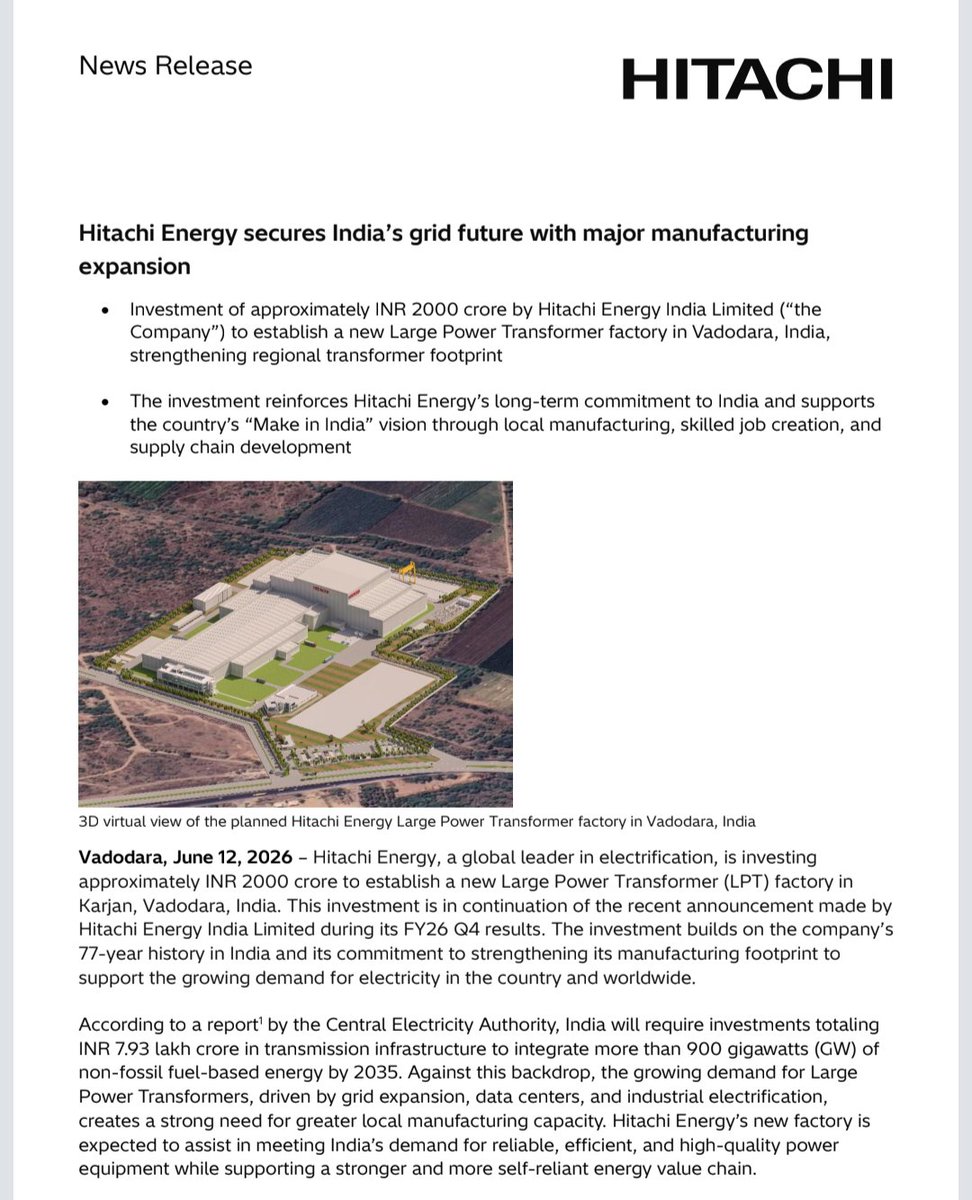

Hitachi Energy India will invest approximately INR 2000 crore to establish a new Large Power Transformer factory in Vadodara, Gujarat, aiming for completion by FY28.

1

12

706

Jun 12

Link to track new capex / expansion announcements:

concall.in/announcements/ide…

Disc: No buy / sell recommendations.

1

452

Jun 11

Sai Life Sciences doubled profit in FY26. Now it's nearly doubling CapEx too.

FY26 was a strong year for the company. Revenue grew 29%, operating profit grew 56%, and net profit jumped 109%. Both the CRO (drug discovery) and CDMO (development and manufacturing) businesses contributed, with CDMO revenue growing 33%.

But the most important takeaway from the earnings call wasn't the growth. It was management's confidence in the long-term outsourcing opportunity from global pharma companies.

Revenue contribution from the top 19 global pharma customers has risen from 28% in FY22 to 49% in FY26.

Management says large pharma companies are increasingly looking for partners that can support a molecule from discovery all the way to commercial manufacturing, creating deeper and longer-term relationships.

The confidence is showing up in capital allocation.

Sai plans to spend ₹1,100–1,300 crore in FY27, nearly double FY26's ₹633 crore.

Most of this will go toward capacity expansion, while the rest will be invested in new capabilities, automation, AI, biology platforms, formulation development, and emerging technologies such as ADCs and peptides.

The expansion will be funded through a mix of internal cash generation and debt, though management said leverage is expected to remain at comfortable levels.

Analysts repeatedly questioned the sharp increase in CapEx. Management's response was simple: customer conversations are giving them better visibility into future pipelines and demand than ever before. Rather than waiting for project requests, they are increasingly working alongside customers on long-term development plans, giving them confidence to invest ahead of growth.

The pipeline also continues to strengthen.

The company ended FY26 with 34 commercial molecules and 11 molecules in Phase III or pre-registration. Management indicated that at least three recently commercialized molecules should start contributing meaningful revenue during FY27.

On the outlook, Sai reiterated its ambition to deliver 15–20% annual revenue growth while maintaining operating profit margins of 28–30% over the medium term. Management also expects the second half of FY27 to be stronger than the first as new capacities gradually come online.

FY26 was strong, but management is already focused on building capacity for what it believes could be a multi-year outsourcing cycle for India's CRDMO industry.

Disclaimer: This post is for educational purposes only. Not a buy or sell recommendation. Do your own research.

#SAILIFE #Q4FY26 #Concall

1

8

47

4,002

Jun 11

Link to Sai Life Sciences Q4 FY26 concall recording, transcript & summarised insights:

concall.in/company/209147/an…

Disclaimer: Not a buy or sell recommendation.

588

Jun 11

DSM Fresh Foods entered into an MoU with Gohpur Fish Farmer Producer Company for development of the Assam Aqua Project, aiming for 300 tonnes annual fish production on 100 acres.

The project aims to strengthen backward integration & sourcing consistency.

Jun 8

DSM Fresh Foods ended FY26 with strong growth, expanding profits, and a business model that looks increasingly different from a year ago.

FY26 revenue rose 69% to ₹221 crore, while profit before tax nearly doubled to ₹23.2 crore. On the surface, it was a strong year. But the bigger story was what changed beneath the numbers.

The business has shifted heavily toward B2B and HoReCa, which now contribute 68% of revenue. That helped drive scale, especially in seafood, but also put pressure on margins as institutional sales are less profitable than direct consumer sales.

Seafood is becoming a key growth engine. Fish contribution increased from 21% in H1 to 27% in H2, while the company expanded partnerships with 300 farmers and is building a platform to improve sourcing and margins over time.

At the same time, DSM is betting on higher-value categories. Its newly launched frozen food brand, "meevaa", received 5,000 orders within 48 hours, and management expects it to contribute 15-20% of FY27 revenue. The attraction is simple: ready-to-eat products carry much higher margins than fresh protein.

The company is also scaling its partner-store model, growing from 100 stores today toward 300-400 stores, creating an offline distribution network alongside its online presence.

Investors spent considerable time discussing margins and cash flows. While profits are growing, operating cash flow remains negative due to working capital investments required to support expansion.

Management believes growth initiatives today should translate into stronger operating leverage over time.

Looking ahead, DSM is targeting 70-80% revenue growth in FY27, driven by seafood, meevaa, B2B expansion, and offline retail partnerships.

It is important to track whether margins and cash generation can grow as fast as revenue.

Disclaimer: This post is for educational purposes only. Not a buy or sell recommendation. Do your own research.

1

5

994

Jun 11

Link to track MoU updates:

concall.in/announcements/ide…

Disc: No buy / sell recommendations.

391

Jun 11

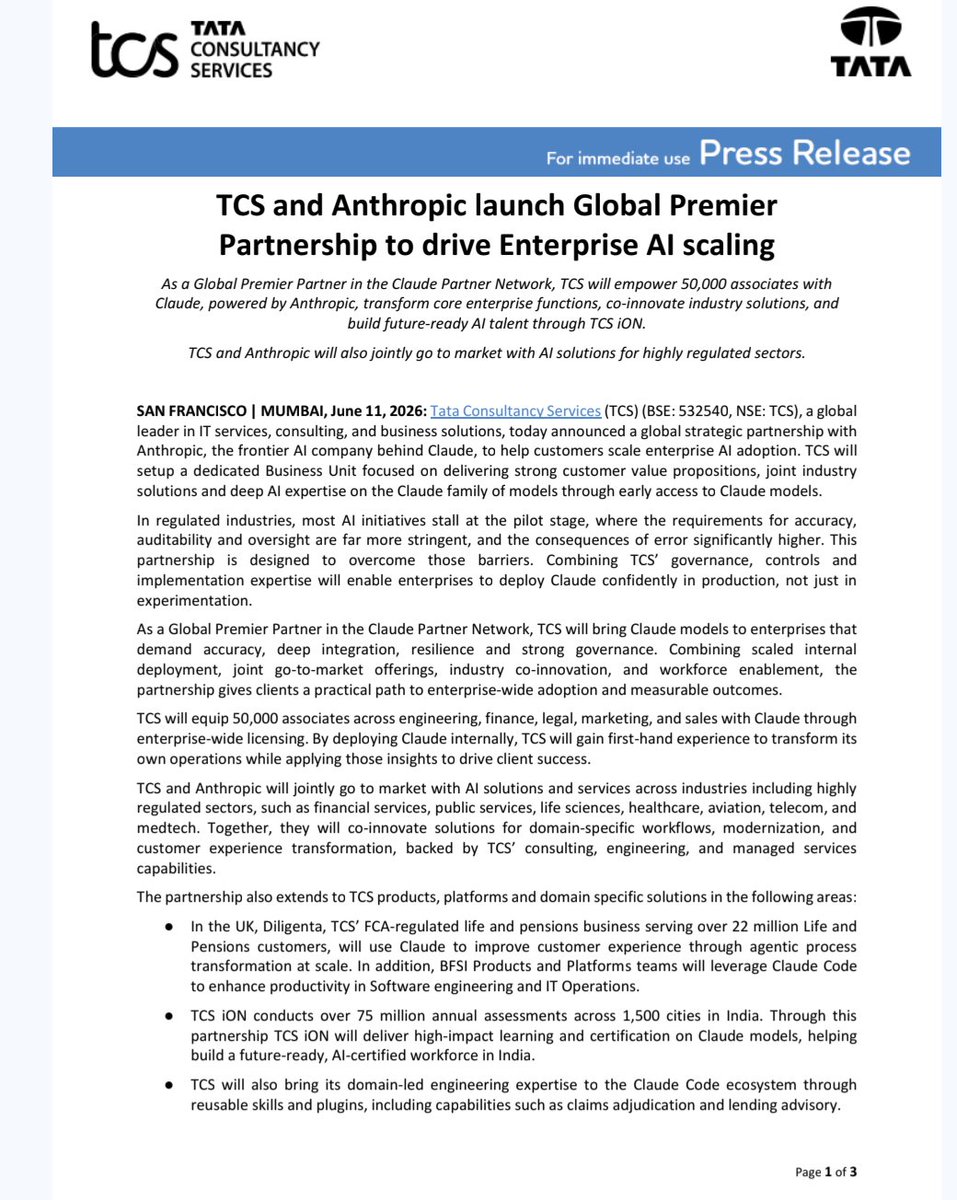

TCS and Anthropic launch a global premier partnership to scale enterprise AI adoption, equipping 50,000 associates with Claude and jointly marketing AI solutions.

2

10

702

Jun 11

Link to track partnership updates:

concall.in/announcements/ide…

Disc: No buy / sell recommendations.

1

457