Hedge fund CIO / Helping people understand the risks within the monetary system they live in. Not financial advice.

Joined December 2022

- Tweets 163

- Following 204

- Followers 84

- Likes 58

37 Photos and videos

Pinned Tweet

The Pentagon has reportedly estimated the cost of the war with Iran at approximately $1 billion per day. Such a figure might be manageable if the conflict were indeed expected to be short. However, I do not share that assumption.

In my view, the developments surrounding both Venezuela and Iran should be understood in the broader context of what represent the United States’ final strategic confrontation with China. Since 2021, I have pressed on that this conflict has already begun in stages. It started with rhetoric 2010, followed by trade disputes mid 2010s, then escalated into financial warfare between roughly 2019 and 2025. The next phase was always likely to be kinetic. We now appear to be entering that stage. The kinetic stage will happen simultaneously as the financial war enters turbo mode.

For that reason, it is difficult to view this as a short war, and Iran itself is without doubt not the primary strategic focus. Rather, it represent one theater within a much larger geopolitical contest.

The $1 billion per day estimate is concerning, and it may prove to be significantly understated. Realistically, the cost could rise to $2, or even $3 billion per day depending on the scale and duration of the operations. We simply do not have the budget to sustain a continuous expansion into new adventures. What is most striking is how closely this path mirrors the one taken by the Romans in the later stages of their empire.

In this broader framework, the actions of the United States and Israel can be interpreted as part of a strategic response to China’s rise. China’s growing economic and geopolitical influence represents the most significant challenge to American global dominance in its roughly 250-year history.

Over the past several years, China has appeared relatively restrained amid the turbulence in global politics. However, that posture will not persist indefinitely. We should now expect a more visible and perhaps, a more aggressive China. When China reveals gold reserves far larger than the roughly 2,500 tonnes officially reported, probably in the range of 30,000 to 40,000 tonnes, the implications for global currency and debt markets will be an event we will not forget.

There is little we can do to influence the course of events in this situation. I have been emphasizing these conflicts for a long time, and the picture is far larger than simply a small war here or there. Regardless of what unfolds, and regardless of who ultimately comes out on top, our approach should remain focused on one clear objective: hard assets.

Are we now beginning to see what smart money is pricing into gold, which began 2023, and initially back in 2018?

1

3

6

1,042

Jun 14

Central banks

40

Corporalis Commodis retweeted

50 Years of Propaganda

commodis.substack.com/p/50-y…

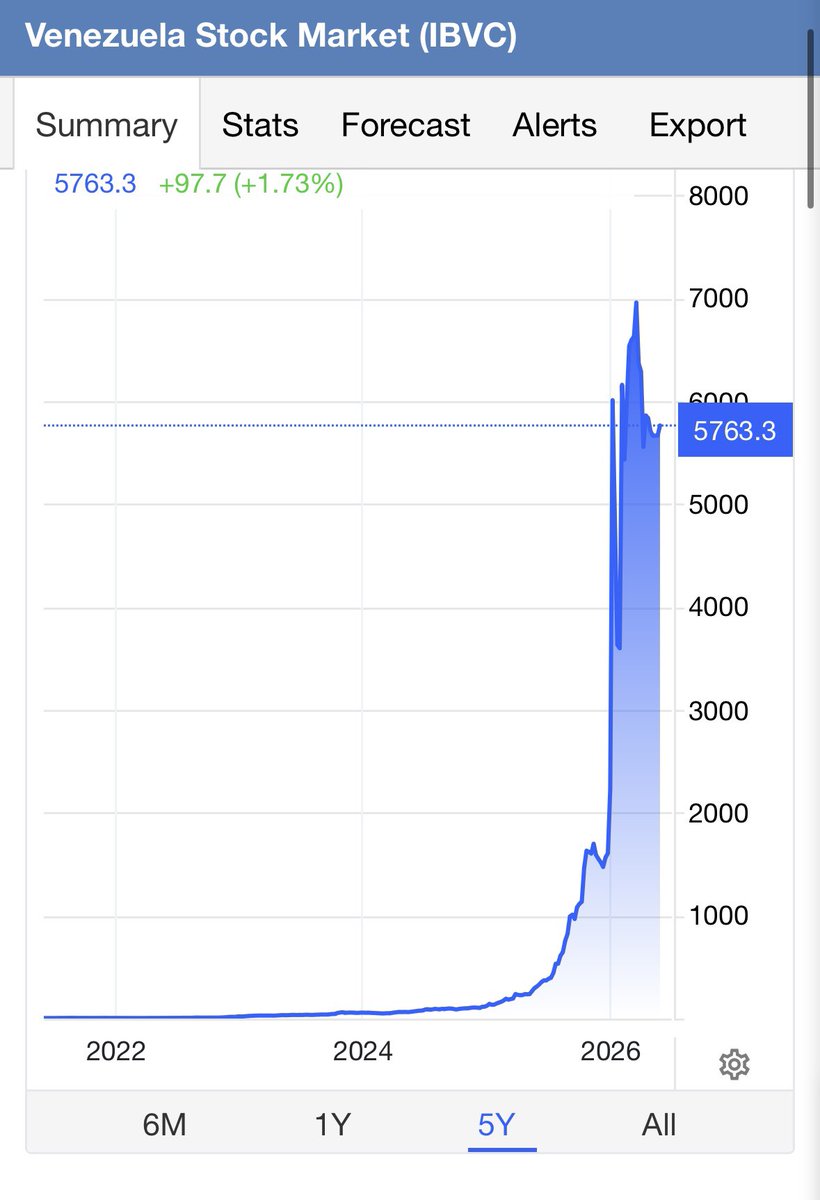

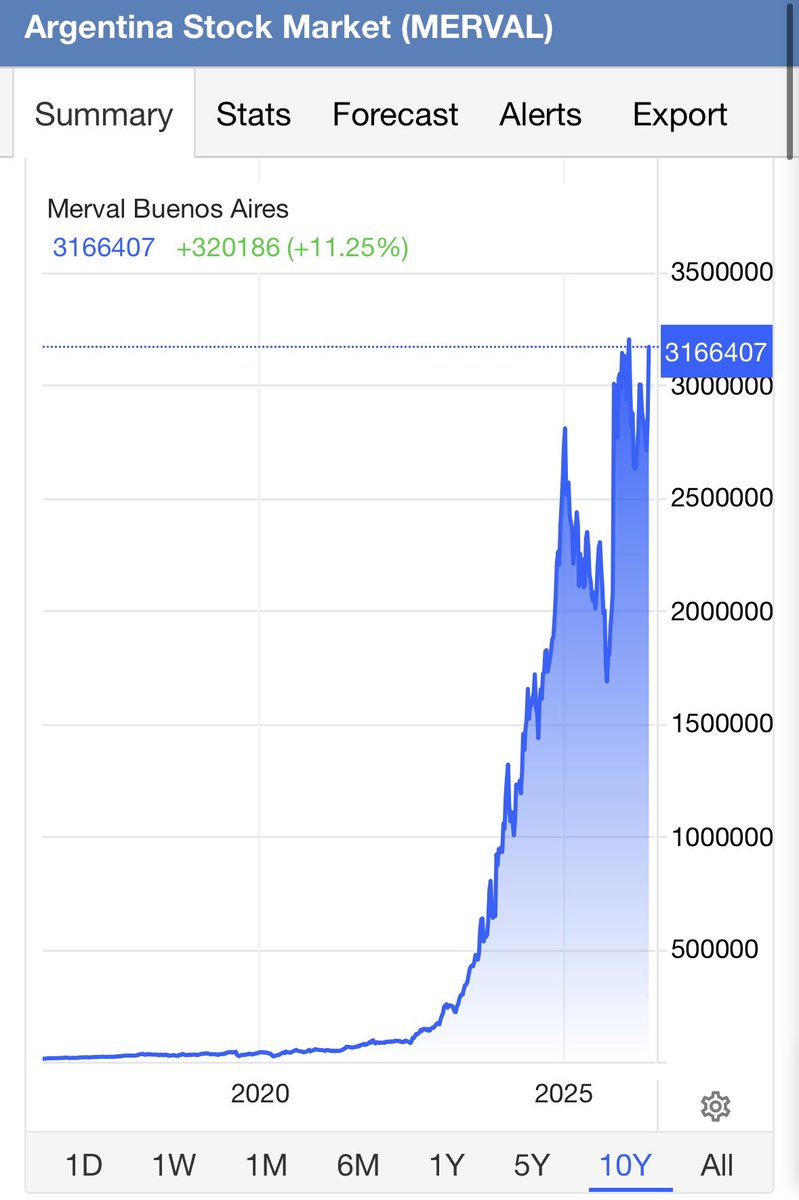

«Turkey offers a valuable lesson. For years, many citizens believed they were becoming wealthier because the stock market continued to rise. The mistake was not in observing rising asset prices. The mistake was measuring those gains exclusively in Turkish lira, a currency that was steadily losing purchasing power. A rising market does not necessarily indicate growing wealth. Sometimes it merely reflects a declining currency.

I suspect many people today are making the same mistake. They measure their success in dollars, kroner, euros, or pounds without stopping to ask whether the unit of measurement itself is preserving value. The question is not whether your assets are rising in price. The question is: rising relative to what?»

1

3

79

Generational wealth is on our doorstep.

What many people spend forty years building, we may have the opportunity to accomplish within the next ten.

commodis.substack.com/p/gene…

2

56

May 31

Please do not listen to this stuff. CC Family. Please.

May 31

🚨 JUST IN: President Trump just went ART OF THE DEAL MODE on Iran, reportedly sending a "TOUGHER" version of the peace framework to the regime, which could pressure them into accepting a deal quicker — NYT

Keep pushing, 47! 🇺🇸

Pure Art of the Deal. Make a bigger ask to make the current deal seem more enticing 🔥

He knows what he's doing. Nothing he accepts will not be America First!

Changes made were not clear, and the full extent of the framework is still not public.

This comes as the US is STILL enforcing the blockade, and Trump held a 2-hour situation room meeting at the end of this past week

1

101

May 31

Correct me if I am wrong, but why did the Republican Party push you to blame Biden for the problems, while you are perfectly aware, as my self, the problems are structural over decades. And no president what so ever can stop it?

Correct me if I am wrong, E.J. but please indulge me.:-)

1

75

May 31

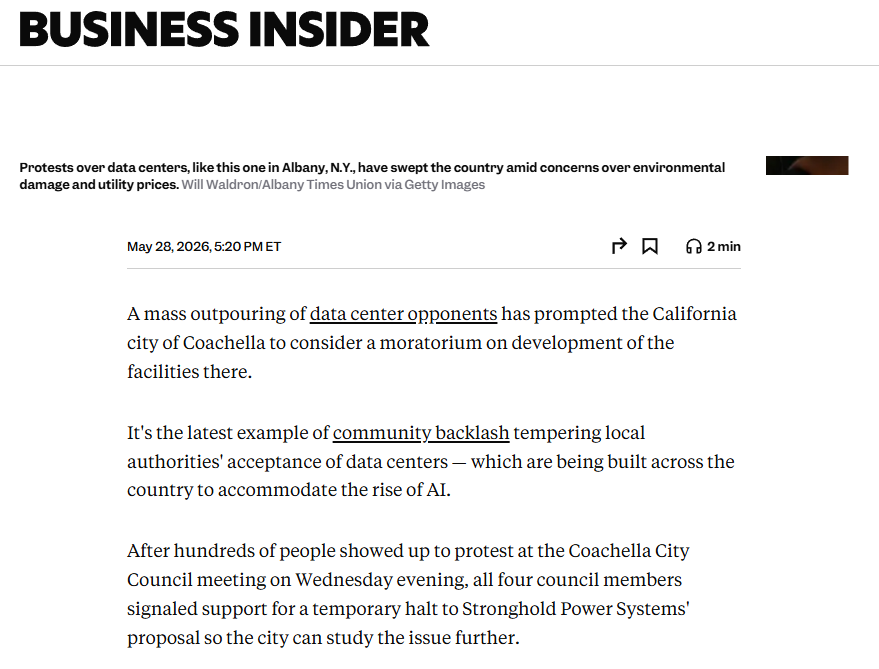

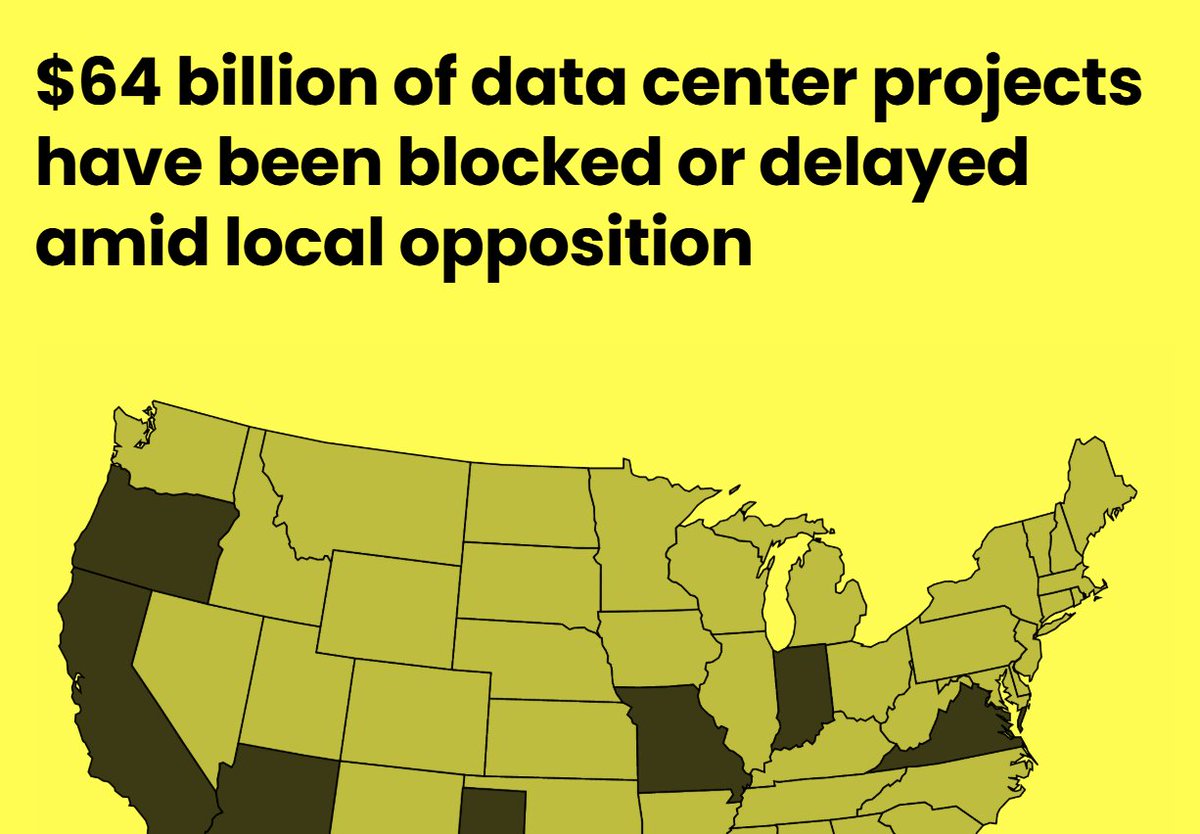

Burn the data centers

May 30

Data center protests are sweeping not just the United States but the globe

Across the political spectrum, humans have never been more united against anything than data centers

63

May 31

Did you see my «yadayada blabla»?

Yes. Trying to show you something. I stopped reading Bloomberg 2023/2024.

You are being played m8. Nothing can stop the already established debt trap.

No politician.

No president.

No bank.

No nothing.

Don’t waste your time buddy.

Godspeed!

1

50

May 31

Yadayadayada. Good luck with your purchasing power m8.

May 30

If you believed oil would go to $200 back in March, you missed out on a lot of stuff, including the S&P 500 rally. So much damage done by oil price alarmists and their apocalyptic forecasts, same as in 2022. One of the topics in this morning's live stream.

robinjbrooks.substack.com/p/…

1

80

May 31

Yadayadayada

May 31

Gold climbs on US‑Iran ceasefire progress as Fed rate hike bets fade-FX

1

59

May 31

Just shut the fuck up already eh?

May 31

NYT: Trump Proposed Tougher Terms to Iran, Including Uranium Limits, Hormuz Access Guarantees, and Long-Term Denuclearization

1

64

May 30

Bla bla and bla

May 30

This is like the 5th 24 hour deadline we’ve given them 😃

1

83

May 30

Yes, good sir. It is with intent.

May 30

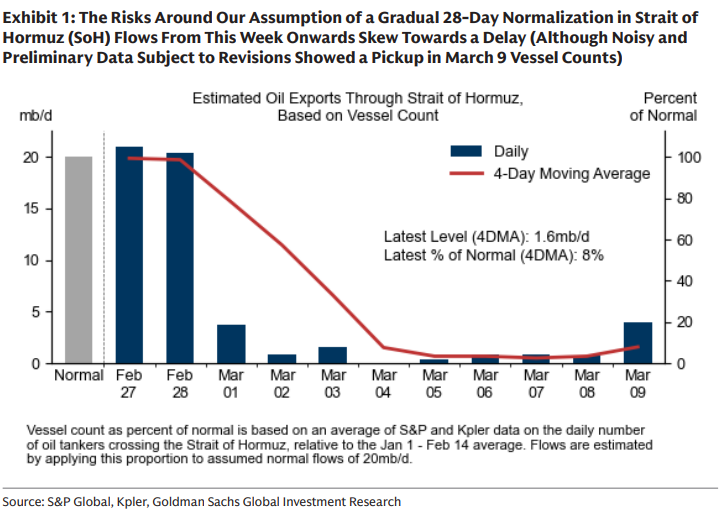

It’s Intentional. Which means it’s all going to get worse, not better.

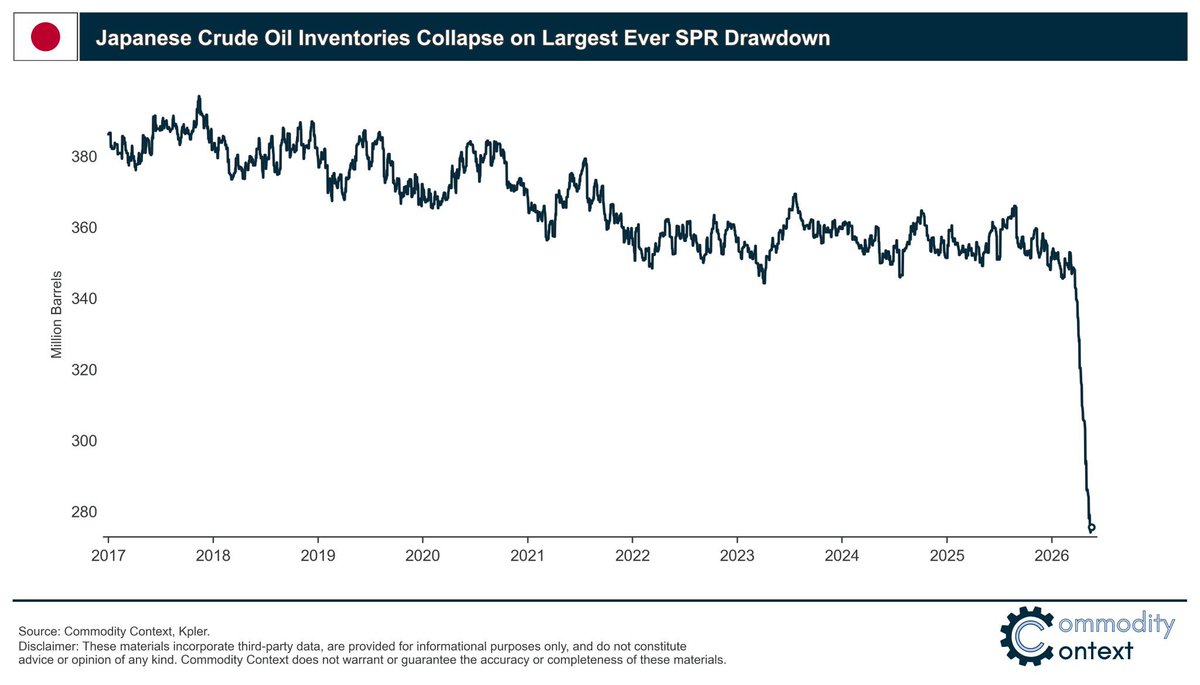

I’ve been connecting the dots on energy and the economy for 25 years. What’s unfolding with the Strait of Hormuz isn’t incompetence - it looks deliberate. The clock is ticking on oil inventories, and the economic damage coming will be severe.

If I’m right, we’re staring down a shock larger than the Great Depression. Get prepared, folks.

Click below to read my full Scouting Report.

peakprosperity.pulse.ly/boa2…

1

95

May 30

Ffs, TANGIBLES! Get out of the grid.

May 30

🇺🇸🇮🇷US is grabbing crypto wallets at will of adversaries.

Th grabbed more than $1 billion worth of Iranian crypto “outright took the wallet”

1

63

May 30

Blablabla

Meanwhile, our currencies are dying. What steps are you taking to protect you and your loved ones?

May 30

🇺🇸🇮🇷 Trump’s final terms for Iran:

1. No nuclear weapon

2. Destroy all nuclear materials

3. Open Hormuz. No tolls.

4. Remove all mines from the Strait of Hormuz

1

70

May 30

Wth are you even talking about, Mario? By that logic, Iran started to price in a deal already in 2025, or even 2020. Before the war, impressive!

The misinformation through your account to millions of X users will be a case-study in it self.

Same as these; @FirstSquawk @axios

May 30

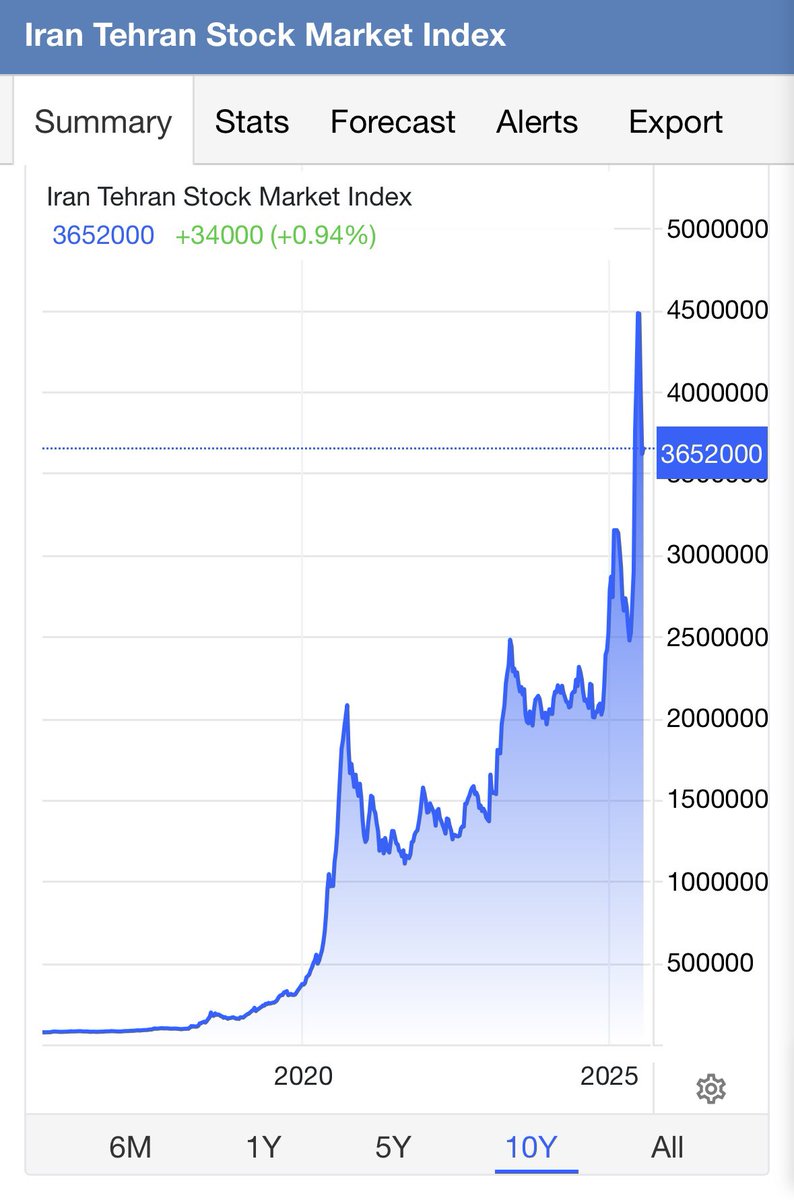

🇮🇷 Every single stock on the Tehran Stock Exchange closed green today. Not one in the red.

First time in the exchange's history.

Iran's market is pricing in the deal before the ink exists. When a population that's been cut off from the internet for 5 months sees every stock go green on the same day, they know something is coming.

The Supreme Leader hasn't signed. The terms are still disputed. The market already decided.

Source: Middle East Spectator

3

193

May 30

Yes

May 30

So basically admitting that us intelligence agencies made Bitcoin

1

62

May 30

Yes

May 29

Some of my friends are paying 100% of the bills for 25-30 year old kids. It’s astonishing.

2

85