Ancora imparo. Small cap investor.

Joined May 2019

- Tweets 2,399

- Following 342

- Followers 281

- Likes 11,384

412 Photos and videos

Correspondens retweeted

Turns out there's a faster way to board an aircraft!

Someone should tag literally every airline and show them this.

📹: bad_science_jokes

538

339

7,361

3,363,505

Jun 13

Indian lives are cheap. 3 sailors killed yesterday in a war we aren’t fighting. 5 IAF officers killed on routine domestic duty. Air India victims’ families hanging on pathetically for closure 1 year later.

And yet no large scale demands for accountability in the government - why are we such a subservient population?

Jun 13

Statement

Indian Air Force deeply regrets the loss of 5 personnel in the An-32 accident at Jorhat, Assam. Sqn Ldr Prashant Singh, Flt Lt Shubham Kumar, Sgt Jitendra Sharma, Agniveervayu Khemaram Kumawat & Agniveervayu Danish Alam made the supreme sacrifice in the line of duty

2

1

226

Jun 12

This is an appreciation post for @HDFCERGOGIC.

After awful experiences so far with another corporate health insurer, I filed my first reimbursement claim for annual checkup with HDFC Ergo under my personal policy, fully expecting follow ups and requests for more documents etc.

Barring a few glitches on their claim portal, the process was simple and most importantly, claim settled and paid in just two days. Surprised and impressed 👏🏻

1

117

Correspondens retweeted

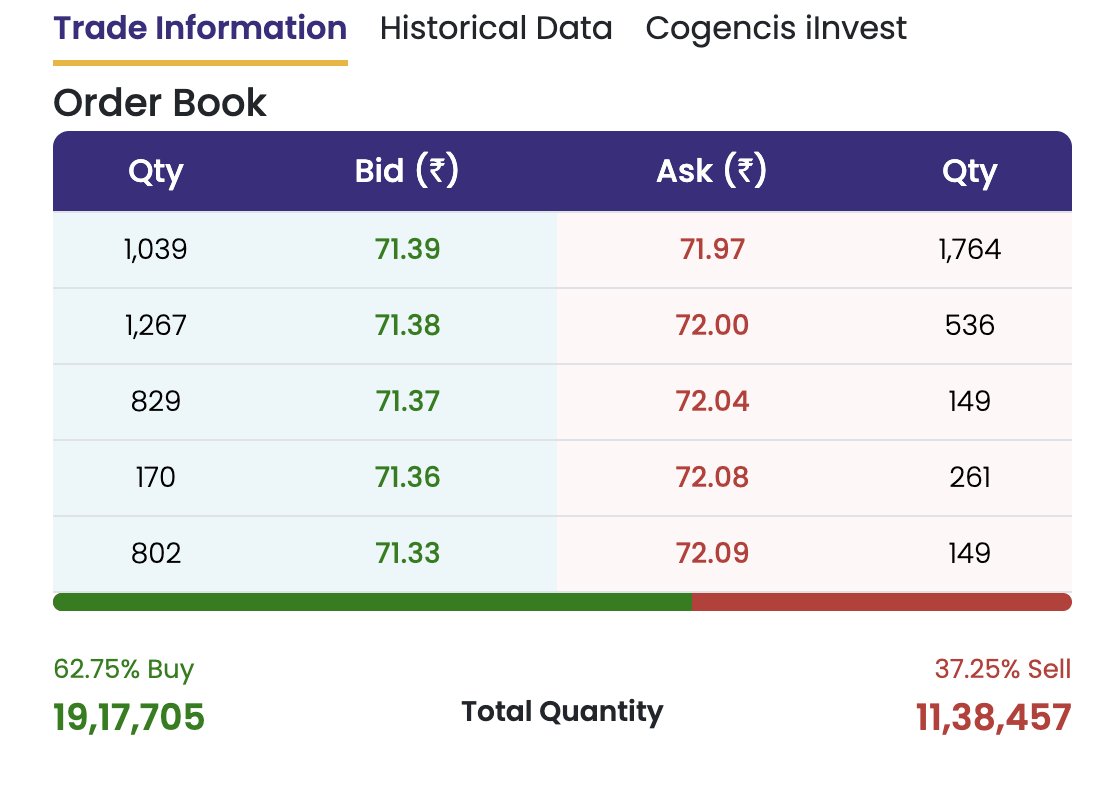

HFCL Ltd.

Maithan Alloys acquires 2,753,500 shares (0.18%) of HFCL for ₹50.04 Crore.

7

102

9,206

Correspondens retweeted

May 14

3B BlackBio up 10% over the last 2 days. Still available under 20 pe for a high quality global diagnostics play with excellent management.

Most undiscovered SME in my opinion, worth studying.

#3BBlackBio

1

1

3

480

Jun 10

Maybe I’ve been rug-pulled by Claude usage limits too many times, or maybe GPT-5.5 is just good enough, but is anyone else feeling zero urgency to try Claude Fable?

42

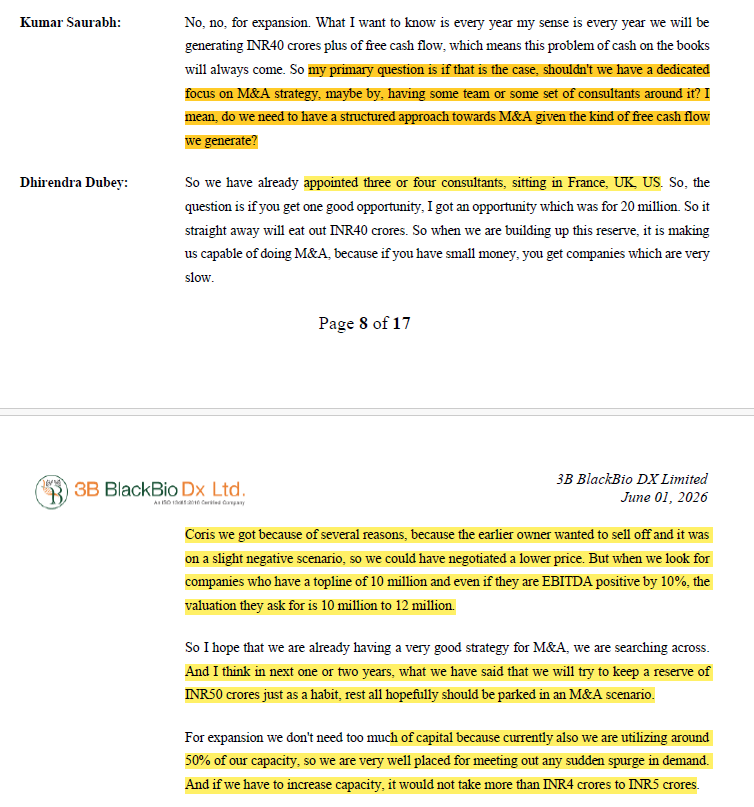

3B BlackBio is a cash flow machine. Very very good management in a niche business. Potential to explode this year with low valuation, low institutional ownership and war chest for M&A 👇🏼

Jun 8

Some businesses suffer from lack of operating cash flow, forget free cash flow and keep diluting for high growth and market willing to give 50-100x on high accounting PAT growth (no complaints, m also biased on few of them till song is on)

Then, there are some companies who generate so much of free cash flow that they need to have a M&A team to deploy cash else 5 years of free cash flow would be equivalent to 25% of market cap.

Also, they can grow at a healthy 15-20% rate.

However, market is not willing to give them even 20x "free cash flow" ex cash.

However, time fills all the gaps sooner or later.

In between, will come questions like - why this quarter sales growth is 3% down. Why other expenses are 5% up? why qoq growth missing? Why yoy EBITDA numbers slightly lesser?

Such investing would require years of waiting in patience but with continuous tracking of business not quarterly numbers to ensure structurally it is not a broken business, till market understands it and appreciates it.

Disc: Biased from last 2-3 years and added more in last 6 months. Not a buy or sell recommendation

#3BBLACKBIO

2

184

Sigma Advanced continues to win large defense orders. 208 cr export order won from North American customer -

2

171

Correspondens retweeted

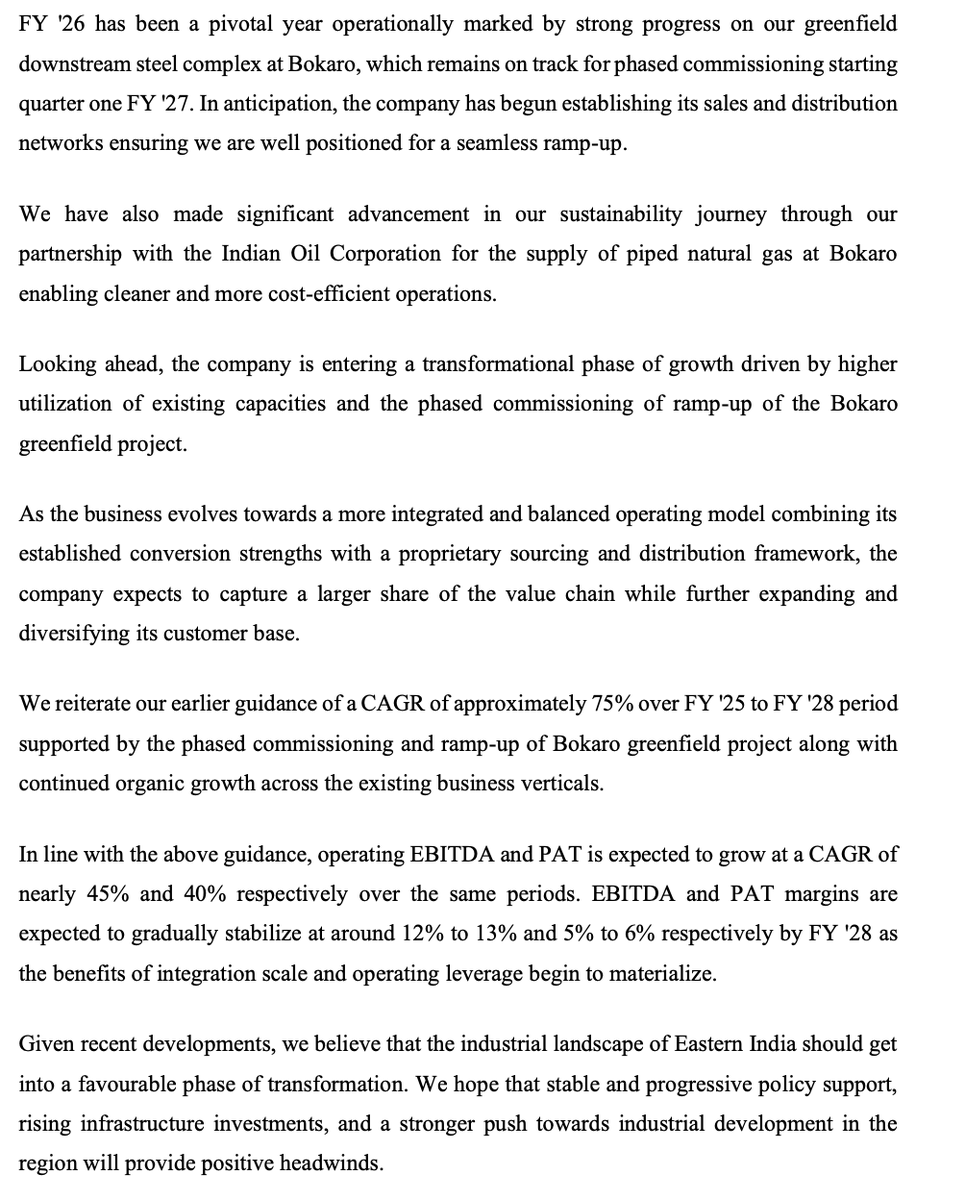

Anyone wondering why BMW Industries is the talk of the town?

👇 Do read this short article that breaks down BMWIL's current business model and why the Bokaro expansion could be a potential inflection point. #BMW #BMWIndustries

3

7

1,720

BMW Industries at 52wk high

May 25

BMW Industries

Kolkata based steel products manufacturer guiding for 75% sales CAGR till FY28 and tailwinds from East India infra push.

Company has been throwing free cash flows for the last 10 years, and is on the cusp of commissioning a ~800 cr expansion project.

449

A real life hero 🙏

VIDEO | Delhi Malviya Nagar fire: A shop owner laid out around 20-22 mattresses from his shop so that people could safely jump on them to escape fire.

Shop owner Armaan says, "I have my shop here, I got information about the fire, there was a massive fire, nobody could get inside or come out. Then 7-8 persons somehow entered. Then I put around 20-22 mattresses from my shop and laid them outside, people jumped on it... Most of them were safe."

#MalviyaNagarFire #DelhiFire

33

Correspondens retweeted

Jun 3

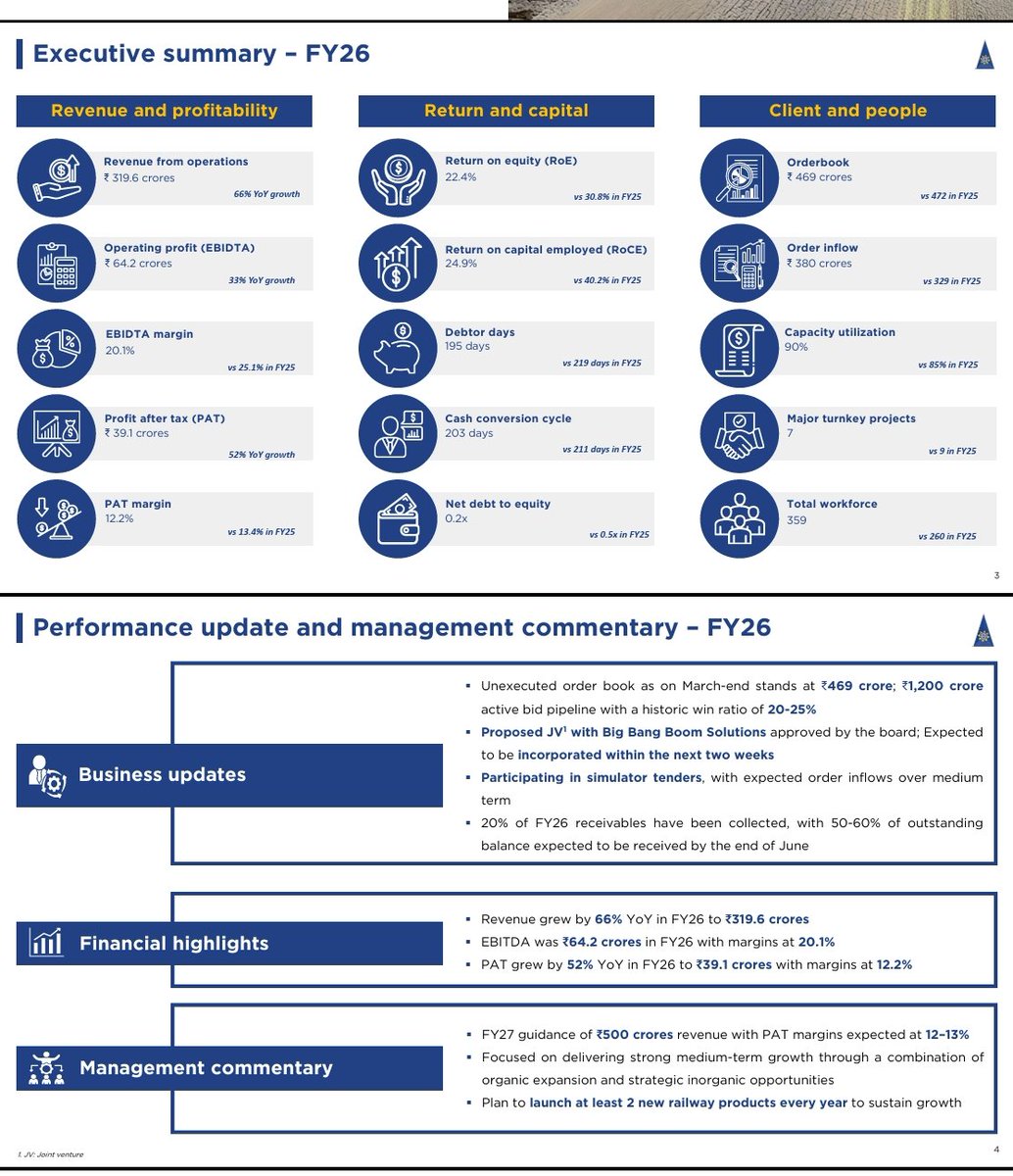

Airfloa Rail Technology

#Airfloa

Unexecuted orderbook at 469cr

1200cr active bid pipeline with win ratio of 20-25%

FY27 guidance:

500cr revenue with 12-13% NPM

1

6

91

13,488

Correspondens retweeted

we must invest in serious dc capacity or we will end up importing most of our tokens from abroad and cause ourselves a big current account deficit. best if we regulate/incentivise so investments come in from hyperscalers (since we will import 70% of bom of dc capex)

Jun 2

Google which is cash surplus, just announced an additional capital raise of $80 bn.

Google annual profit is $160 bn, last quarter $62 bn, and market cap $4.5 trillion. That is close to total profits and market cap of all Indian listed companies put together.

It’s a wake up call to all companies to invest into the future, whatever the present maybe.

Now that IPL is done and dusted, time for India to focus on business of business.

5

5

77

7,950

Epack Prefab 165 cr order received. Stock on fire today

May 17

EPack Prefab 👍🏻

50% PAT growth - stark contrast with Interarch in PEB segment

1

257

Almost 40% of free float exchanged hands today in Jeena Sikho. Crazy volumes

Jun 2

Yesterday: endless tweets on why Jeena Sikho was being avoided by them

When it was at -20% LC.

Today: 20% 😀😀

Funny how narratives change faster than prices.

274

GSM foils revenue of 34.5 cr in May, up 96% YoY. This is with minimal contribution from new Ahmedabad plant.

Guidance is to exit the year at 60-70 cr revenue per month, so it will double again during the year.

Trading at 8x FY27e pe

Jun 2

📌 GSM Foils Limited informed the exchange about sales volumes of ₹345,953,935/- for the month of May, 2026. The company recorded a YoY growth of 96.41% in Net Sales for May, 2026 compared to May, 2025. #SME #GSMFOILS 📈📊

1

233

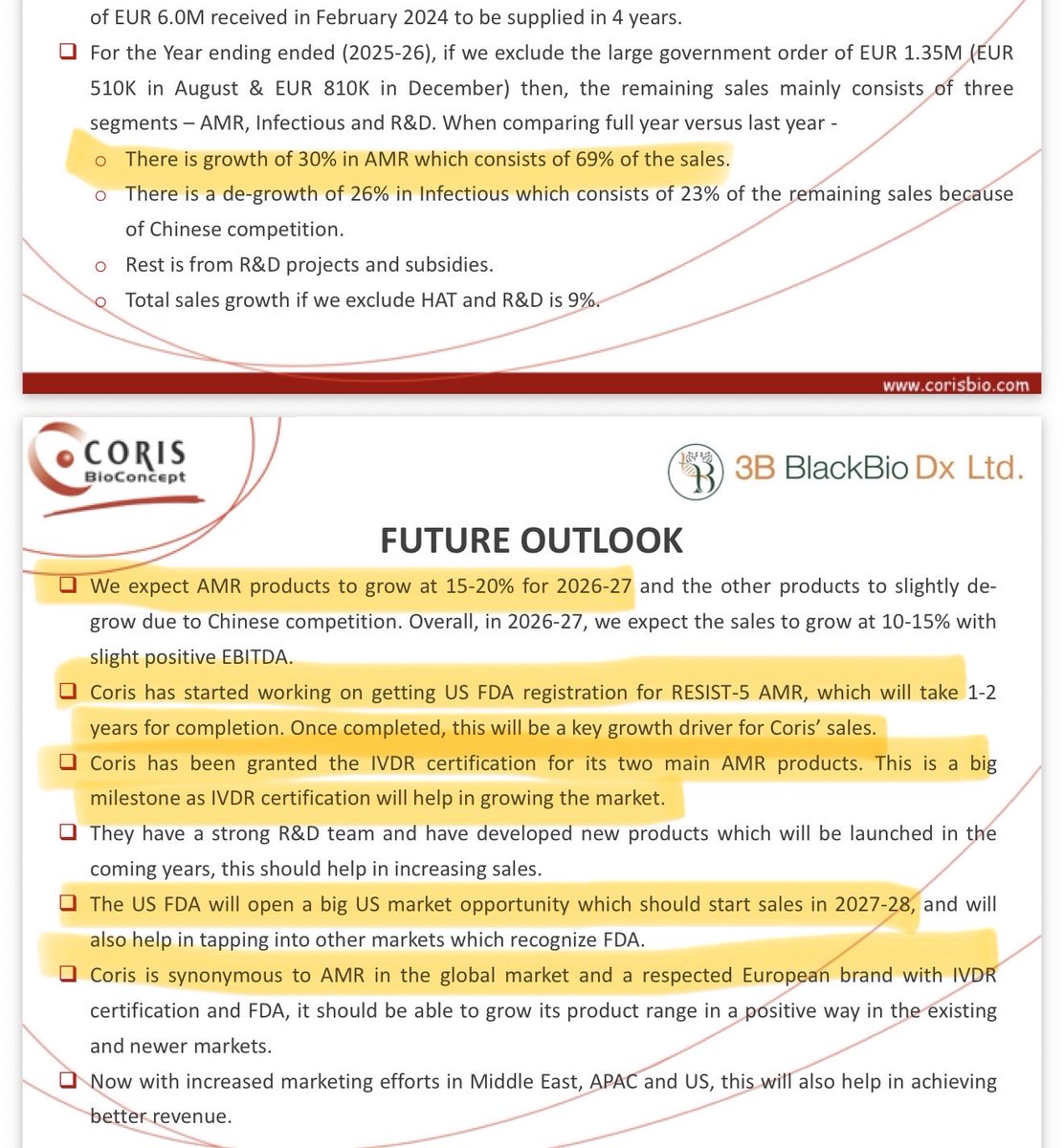

3B BlackBio concall key highlights -

Mgmt is guiding for ~175-180 cr consol revenue vs 142 cr in FY26 ( 23% YoY).

Core 3B TRUPCR Europe should grow 15-20%.

Coris should do ~€5m / ~55 cr revenue in FY27. Mgmt said Coris will be loss-making in Q1/Q2, then HAT orders in Q3/Q4 should help it end the year around EBITDA breakeven / slightly positive.

My read is that full year EBITDA margins should normalize closer to 33%-36%, higher than Q4's 24% and lower than 40% margins pre acqusition. Growth in core business exports other income from the huge treasury will make up for lower Coris margins in FY27.

Few other important takeaways:

1. M&A commentary was very concrete this time

Mgmt said there are advanced discussions, 3-4 consultants are working across France/UK/US, and the company intends to deploy upto 140 cr on out of 250 cr surplus. They are looking at assets upto ~€10m / ~110 cr revenue also and fighting hard to be disciplined on valuation. I think another acquisition in FY27 looks extremely likely now, likely in the diagnostics / molecular / genetics adjacencies

2. Coris roadmap is becoming clearer.

FY27 target is ~€5m revenue, breakeven EBITDA. FY28 target is 5-10% EBITDA margin. US FDA registration is on track for FY28

3. Core business remains strong.

India business has ~15% market share and should grow around 15%, exports faster at 20-25%, and TRUPCR Europe continues to scale even faster

4. Sample-to-answer system will launch by H2

They are taking OEM route, validation is positive, and installations may start by Q3/Q4. This is imp because sample-to-answer and POC are large parts of the global molecular dx market where 3B has had limited participation so far.

Overall, FY27 looks like the first full year of 3B as a proper global diagnostics platform.

Expected revenue: 175-180 cr

Large treasury: ~250 cr liquid assets

Valuation: 16x pe FY27e, 12x pe ex-cash

Q1/Q2 may look optically weak on margins but most of it is priced in already

#3bblackbio #diagnostics #sme

May 29

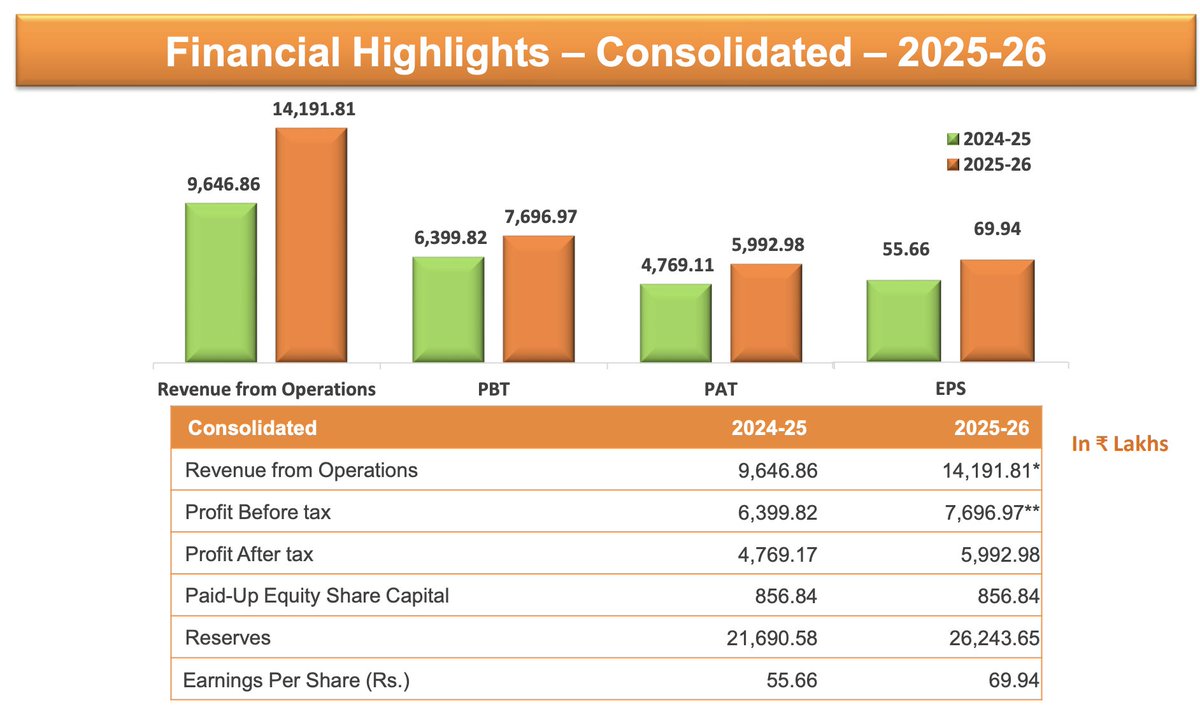

3B BlackBio FY26 result is a strong one.

FY26 Revenue up 47% to 142 cr

FY26 PAT up 26% to 60 cr

Q4 revenue up 58% YoY and PAT up 22% YoY

Coris contributed 36 cr revenue and 8.8 cr profit in part year consolidation. Ex-Coris too, the MDx business grew double digit despite last year’s flu/dengue spike base.

TRUPCR Europe grew 36% YoY and continues to become an important global distribution leg for the company.

Exports were very strong, up 25% YoY to 21.4 cr. Presence now across 70 countries and 200 export customers.

Balance sheet is the best part-

Cash bank: 101 cr

Investments: 158 cr

Debt: just 3 cr

So ~255 cr net liquid assets on the books

Important point:net liquid assets increased by ~30 cr YoY despite acquiring Coris during the year. That tells you how cash generative the underlying business still is.

Cash flows remain best-in-class for a microcap.

CFO was 52.5 cr vs PAT of 59.9 cr, ~88% conversion. Unlike many microcaps that only report accounting profits, they keep throwing out real cash year after year.

Negatives - Q4 had margin compression as Coris got fully integrated (big jump in employee cost and other expenses), and FY26 had some one-offs including the profitable quarter consolidation benefit at Coris. So I would not blindly annualize Q4 or assume FY26 margins are the steady state.

But zooming out, this is a profitable, cash-rich, R&D-led molecular diagnostics company with India UK Europe footprint, growing exports, 120 assays, AMR optionality through Coris, and M&A IVDR USFDA related triggers ahead.

At ~1050 cr market cap, the stock is still only ~17-18x FY26 earnings and ~13-14x ex-cash earnings...

2

250

Roads are still better than India ☠️

Jun 1

New video out of Tehran after internet was restored shows the city during the U.S. and Israeli strikes in March.

@afshin_ismaeli

46

This handle is doing great work by uploading summaries super fast after con calls @2orderequity - recommended follow!

1

1

1

173