Building. Get Off Zero! Opinions, likes, retweets, comments are my own and are all CONTEXT DEPENDENT.

Joined January 2018

- Tweets 1,147

- Following 1,089

- Followers 152

- Likes 4,058

43 Photos and videos

Bit Coyne retweeted

Jun 14

RYE WINS THE CLASS C NYS LACROSSE CHAMPIONSHIP!!!

Rye 15 - 9 Jamesville-DeWitt

Congrats to the Rye Varsity Lacrosse Team on an INCREDIBLE year with a storybook finish!

Congrats on an AMAZING first year of coaching Rye High to Head Coach Gutski and his coaching staff!

3

9

58

21,147

Mar 14

19

Bit Coyne retweeted

Feb 9

Whole stadium trying to figure out wtf they’re watching lmao

503

1,065

10,989

365,999

Bit Coyne retweeted

Feb 6

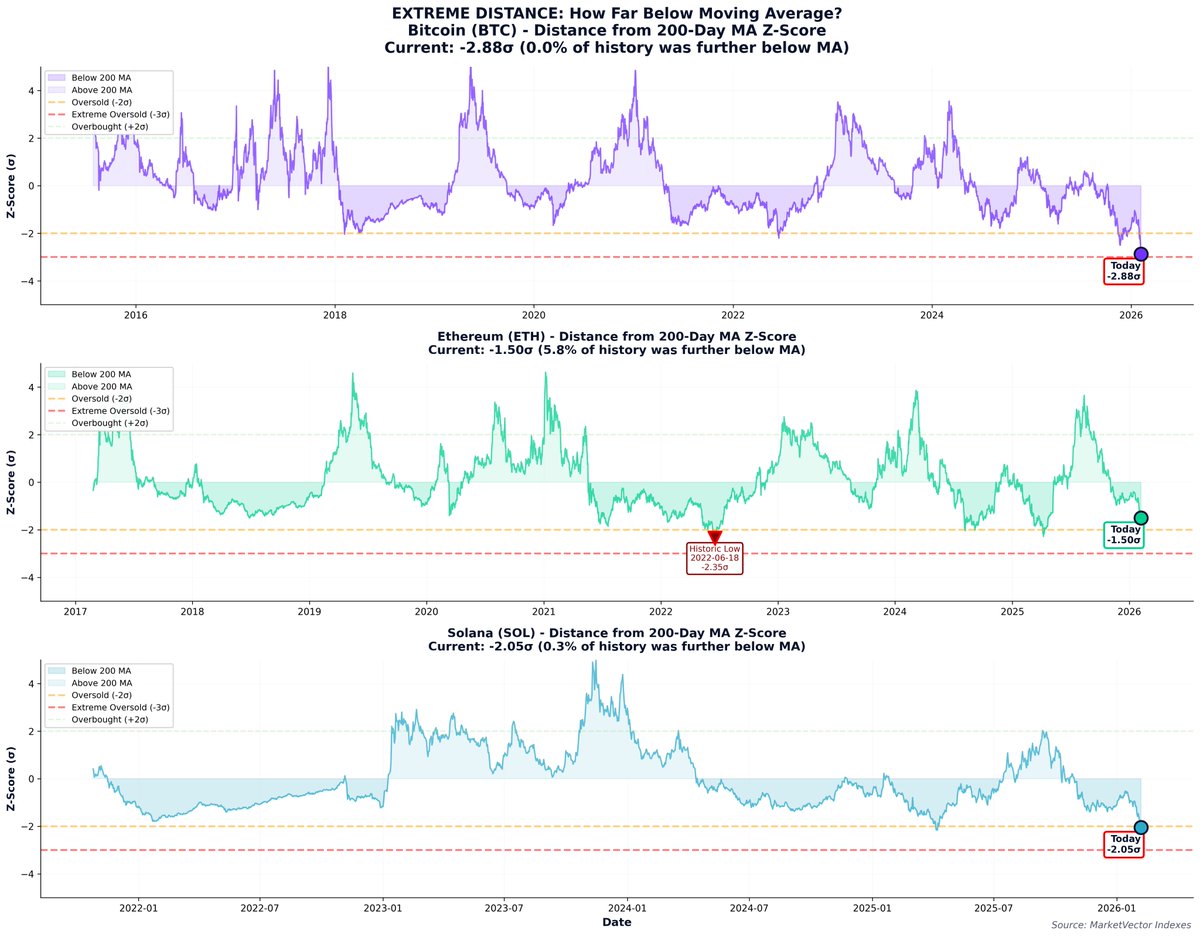

Bitcoin is -2.88σ below its 200-day moving average.

In 10 years of data, this has literally NEVER happened before.

Not during COVID. Not during FTX. Never.

I analyzed what this means. The findings are striking.

🧵 Thread with charts ⬇️

@SASchoenfeld @MarketVector @matthew_sigel

23

63

277

61,444

26 Apr 2025

nypost.com/2025/04/26/opinio…

Blockchain-based stablecoins are now the seventh largest buyer of US government debt, exceeding Germany, Australia and other big countries. And they’re growing quickly — surpassing $200 billion in size this year and nearly $250 billion today.

35

Bit Coyne retweeted

21 Apr 2025

1/ 🚨 Oregon is suing @coinbase — and it’s not just another enforcement action. Here’s why this case matters for the future of crypto regulation in the U.S. 🧵

1

1

5

1,353

Bit Coyne retweeted

3 Apr 2025

“Look, the prices of goods going up and my portfolio going down isn’t necessarily a bad thing, because I love working and that just means I need to grind even harder now”

31

271

7,340

357,318

Bit Coyne retweeted

2 Apr 2025

I've been thinking about this quite a bit since @brian_armstrong wrote it, and didn't want to shoot from the hip (or on April Fools, because this is not my first time on the internet). But I've gathered a few thoughts and want to share them.

1 - I understand why both banks and issuers would like interest to be prohibited for stablecoins. For banks, they see this as eliminating one source of competition. For issuers, well, keep the money! However, there is one group who we didn't mention there, which is consumers.

2 - For the consumer, part of why banks post-2008 have been such a nightmare is that you don't get paid any interest on the checking accounts you have, so if things go well, the bank executives make a ton of money, and if things don't go well, the public bails them out! That's... not a fair arrangement!

3 - For a stablecoin, the assets are much safer but the business model is pretty simple. Again, why isn't the consumer able to get paid yield and we have a competitive market?

4 - All of this is profoundly anti-competitive in the end. It serves as a subsidy for either banks or stablecoin issuers at the expense of competition and the economic returns to the consumer.

5 - This ban on interest will greatly inhibit adoption, which is a point I think is understated (and why the banks likely enjoy the ban). After all, if I have a stablecoin that pays interest less a small fee for management, everyone can take that and hold that and get paid a fair amount. It becomes the "neutral" option for money if only backed with something like t-bills. Interoperable, generally acceptable, cheap to create. Essentially like the Vanguard low fee index fund concept, but for your deposits. You can see why they want to cripple that for companies and not pay interest - otherwise, people might actually use it!

6 - The people most hurt by this will be the non-rich and small businesses. They are the ones currently getting scalped the most by our financial monopoly, and the ban on interest is just a vote to continue expropriating them.

So, after turning this over a few times in my head, I find it hard to construct a non-protectionist argument for why we would want to ban paying interest.

And from a US perspective: another jurisdiction will allow this, so if we don't, we're just going to lose business abroad.

Thus, I think Brian is right. It's a bad idea. It's pro-monopoly and anti-consumer. It's also just silly, in the end.

Let the market sort it out, so long as the rules around reserves and bankruptcy remoteness are correct (that's where the rubber meets the road on safety).

23

42

183

97,628

2 Apr 2025

👀

2 Apr 2025

Hey @ryancohen, curious why @gamestop $GME chose @TDBank_US as sole bookrunner on the Bitcoin convert issuance when TD shut down their crypto unit and bailed on the industry? Why not give it to the old Cowen team who's now at @StoneX_Official and very crypto native?

12

Bit Coyne retweeted

20 Mar 2025

March Madness is here

48

2,221

15,069

1,449,199

Bit Coyne retweeted

12 Mar 2025

BREAKING: Apple just announced the new iPhone, exclusive for ETH holders

297

595

7,226

522,566

Bit Coyne retweeted

10 Mar 2025

The SEC has already dropped 11 lawsuits against crypto-related companies in the last month.

The regulatory shift is clear.

Even if we don't feel its effect on markets right now, the long-term impacts of this cannot be understated.

83

70

397

43,267

Bit Coyne retweeted

24 Dec 2024

Price of a bitcoin on Christmas Eve 🎄

2024: $94,206

2023: $43,389

2022: $16,832

2021: $50,825

2020: $23,475

2019: $7,318

2018: $4,124

2017: $13,611

2016: $899

2015: $453

2014: $330

2013: $651

2012: $13

2011: $4

2010: $0.25

2009: $0

2008: $0

201

1,054

8,260

800,370

Bit Coyne retweeted

24 Dec 2024

The perfect Christmas gift 😉

167

3,501

43,331

1,817,348

24 Dec 2024

In the past week, spot Bitcoin ETFs recorded inflows of 4,349.7 BTC, worth $423.6 million – nearly double the 2,250 BTC mined in the same period. #LETTHATSINKIN

ambcrypto.com/bitcoin-etfs-c…

1

24

Bit Coyne retweeted

21 Dec 2024

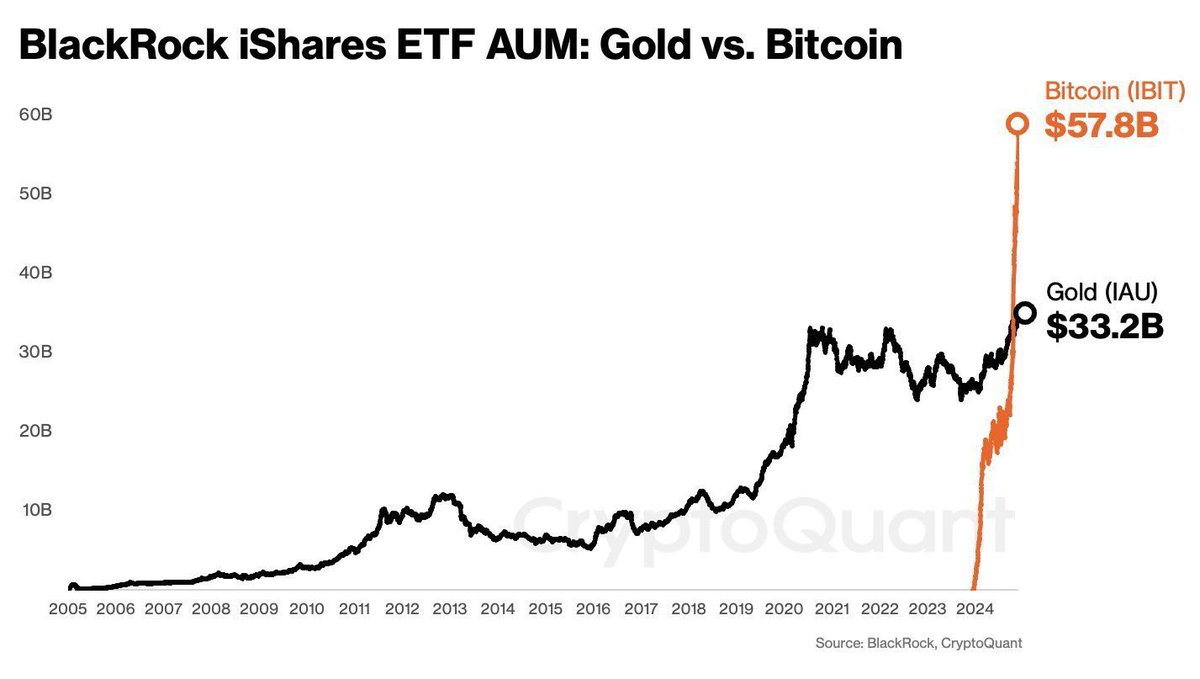

Not sure how this isn’t ETF chart of the year…

Anyone have something better?

40

164

1,202

135,048

Bit Coyne retweeted

20 Nov 2024

The four stages crypto guys go through when trading meme coins

490

799

6,507

630,890