btc stocks and DUBAI LOVER @FrogtownCapital app.hyperliquid.xyz/join/MOC… tg channel t.me/MOCHOsaysYouAPE

Joined April 2017

- Tweets 105,815

- Following 3,642

- Followers 137,068

- Likes 231,832

23,557 Photos and videos

Pinned Tweet

May 29

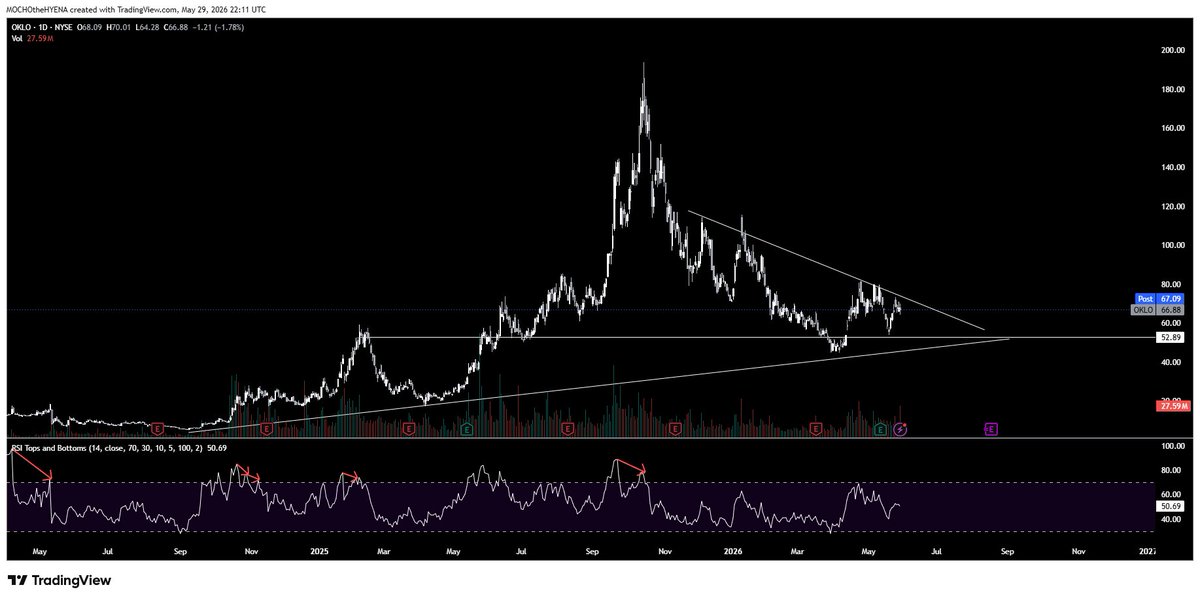

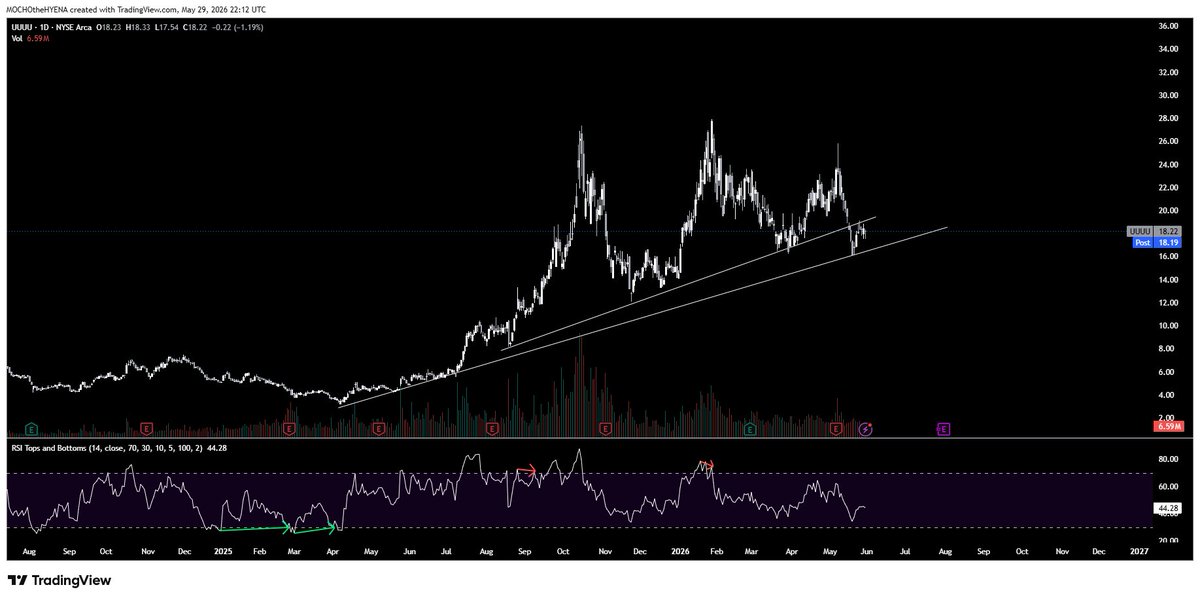

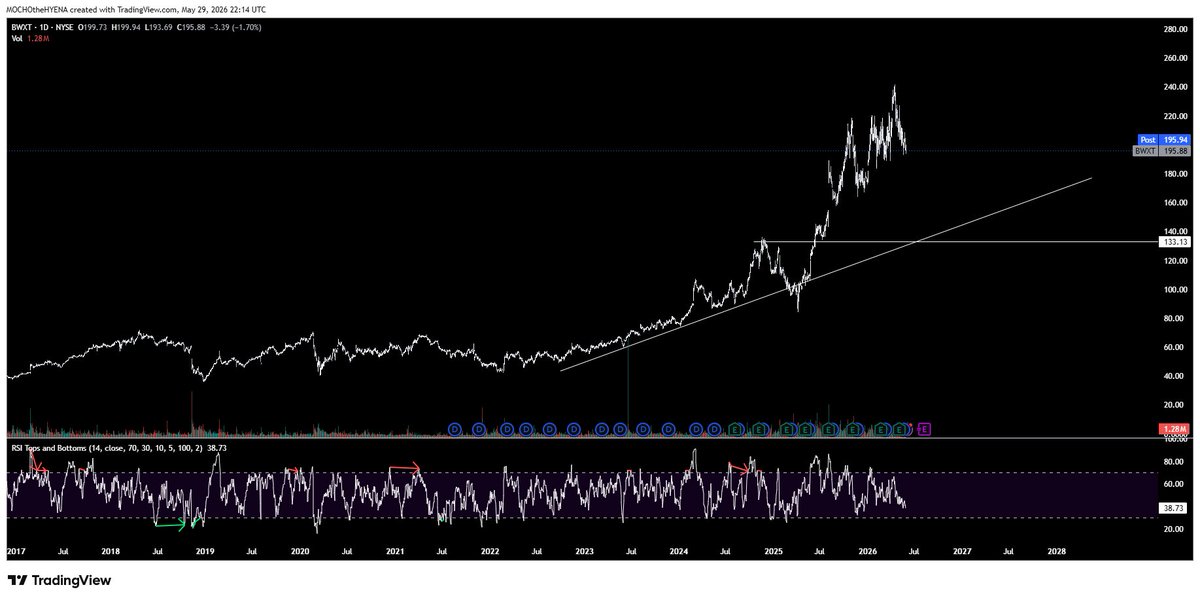

NUCLEAR PORTFOLIO FOR THE NEXT 3 TO 5 YEARS

$LEO CENTRUS ENERGY MONOPOLY IN USA

$OKLO SMALL REACTORS FOR ELECTRICITY CONSUMERS

$UUUU URANIUM MINERS

$BWXT COMPONENTS DEFENCE AND PUBLIC (NOT IN BUY ZONE BUT CAN BE GOOD TO BUY AT GOOD DEEPS )

NOTE speculative this portfolio will be between 150 and 500% in the 5 years term been the next big wave

6

1

15

6,051

#cuba u next in the list

Then I guess back to Venezuela ther are some stufff to clean

ahhhhhhhhh

good stuff

love it

Let's clean all those lefties from those places

2

1

235

mocho17™®© retweeted

SAUDI FOREIGN MINISTRY: WE LOOK FORWARD TO A PERMANENT AGREEMENT THAT TAKES INTO ACCOUNT THE SECURITY INTERESTS OF THE REGION'S COUNTRIES

4

5

26

7,230

mocho17™®© retweeted

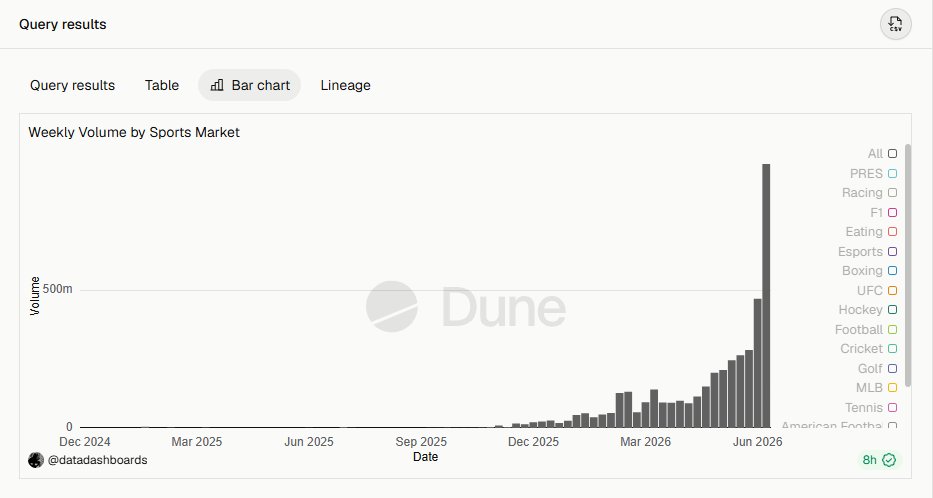

$HOOD Many of us have mentioned that the World Cup would be the biggest event ever in prediction markets, but the numbers we're seeing so far clearly exceed my most bullish expectations.

Robinhood has seen over $167 million in volume through Rothera JUST in World Cup event contracts over the past five days, with the Brazil-Morocco game seeing over $22 million traded on the platform.

Also, Kalshi is seeing its biggest week ever in sports event contracts traded, without including today's figures, which means their weekly number will be well above $3B. Yes, $3B in just A WEEK.

From what I've seen, Robinhood has been offering the World Cup event contracts through Rothera, but I've seen a few games where the fees were higher, which could mean they offered some of these through Kalshi too, which — judging by how big the Kalshi "Other" figure is for the week — would make sense.

Anyway, the World Cup is just getting started, but it looks like Robinhood is well on track to have its biggest month ever in prediction markets. Maybe it's time for those analysts who thought prediction markets were dead after football season to take another look and maybe change their mind.

$HOOD Robinhood's Rothera Predictions markets are growing rapidly. Almost 70m in volume in the past 24 hours!

8

5

95

10,564

mocho17™®© retweeted

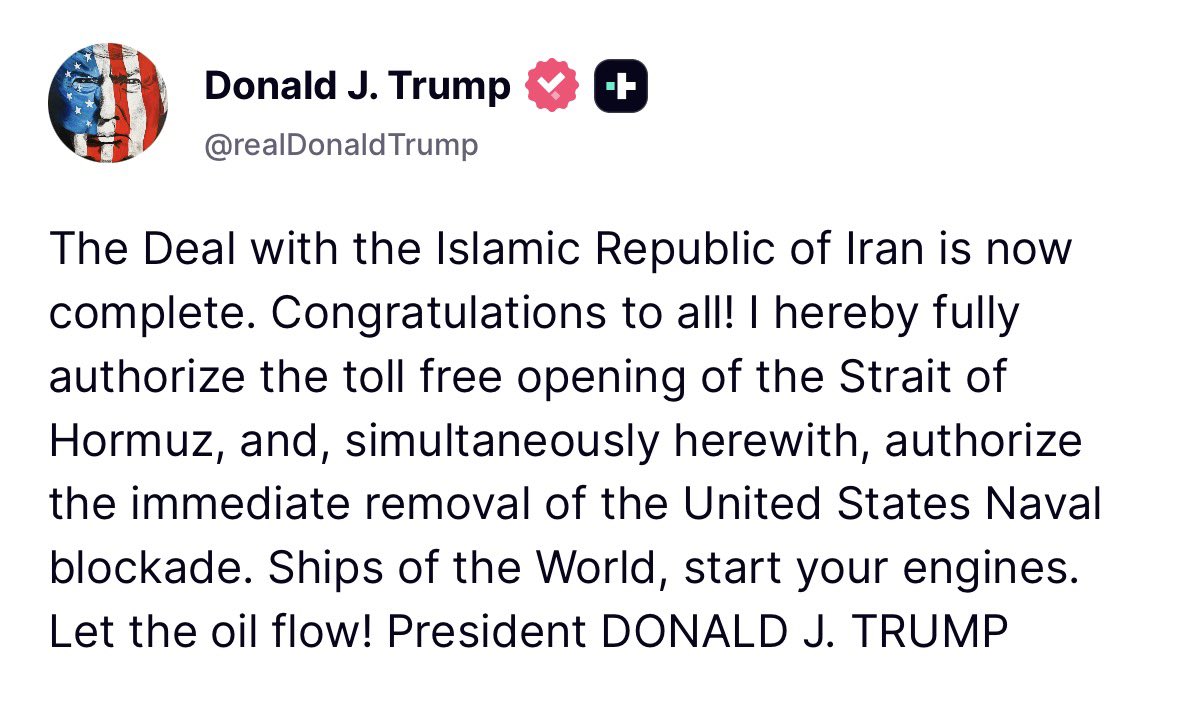

“The Deal with Islamic Republic of Iran is now complete. Congratulations to all!” President Donald J. Trump 🇺🇸

8,279

18,314

84,772

5,949,253

mocho17™®© retweeted

If you want to actually understand $AMPG, stop scrolling hype and read this.

Coffe House Stocks just put out one of the most thorough breakdowns of AMPG I've seen.

Not a pump.

Real research: the business model, the patent moat, the catalysts, and (refreshingly) the risks laid out honestly.

A few things it nails that most threads skip:

The moat is vertical integration.

AMPG designs the MMIC chip in-house, packages it natively, and builds it into its own antennas.

Competitors stitch that together from separate vendors, which adds noise and loss.

That's a real, structural edge, backed by a stack of granted patents (2025 and beyond).

The catalysts are concrete, not vibes.

➟ Open6G OTIC certification (only US-designed 64T64R certified there).

➟ The NVIDIA AI Aerial integration.

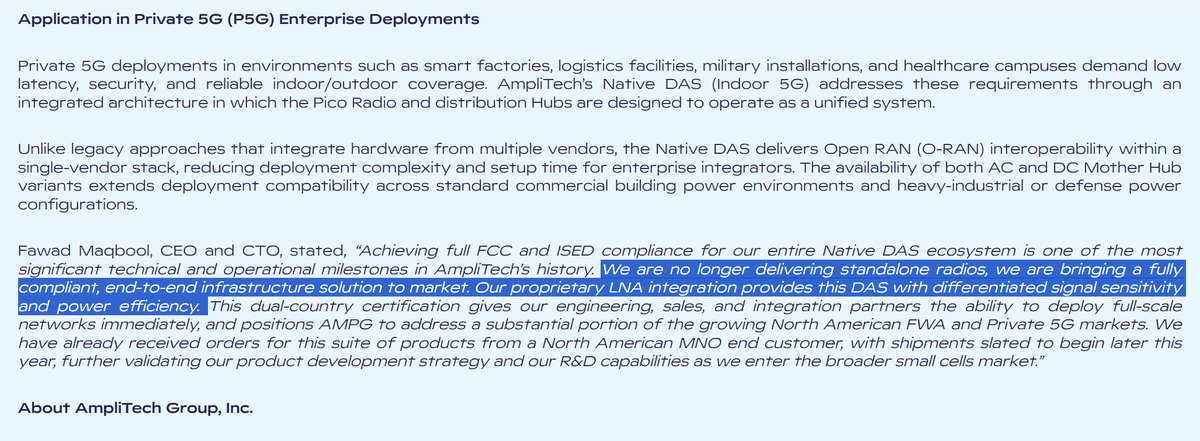

➟ FCC and ISED clearance for the full 5G DAS stack.

➟ Sole 64T64R vendor at the O-RAN Global PlugFest.

➟ And LOIs converting into real funded POs.

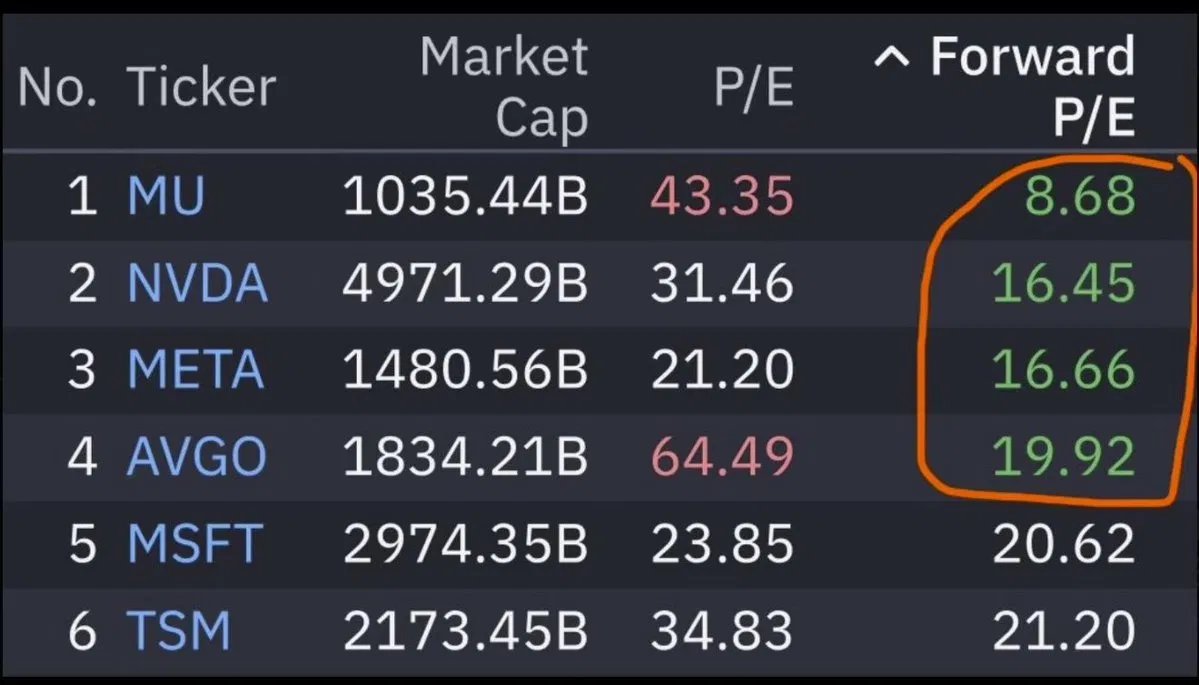

The framing I keep coming back to: a valuation floor (cash, zero debt, real IP, P/S of ~6x) under a genuinely uncapped ceiling across O-RAN, SATCOM and quantum.

And I would add:

➟ Management said they will close deals this quarters, probably straight POs and not LOIs.

➟ Management with bullish vibes, on Linkedin and earnings call.

Asymmetry, with eyes open.

This is the kind of DD this name deserves.

Go read the whole thing and follow @CoffeeHouseStks.

Not financial advice. I'm long $AMPG. DYOR. 📡

7

9

70

6,796

mocho17™®© retweeted

Netherlands just approved a 36% tax on money you haven’t even made yet. Pure paper gains.

Meanwhile in the UAE? Zero tax on crypto, investments, or capital gains.

Capital always moves to where it’s treated with respect. This is why places like Dubai keep winning.

Smart money knows where to go.

13

343

222

11,941

RT @Sajwani: Just in: UAE establishes a federal authority for AI and data. The authority will be led by H.E. @OmarSAlolama and will be unde…

20

mocho17™®© retweeted

No caption needed.. Slaves in Dubai

32

18

235

52,790

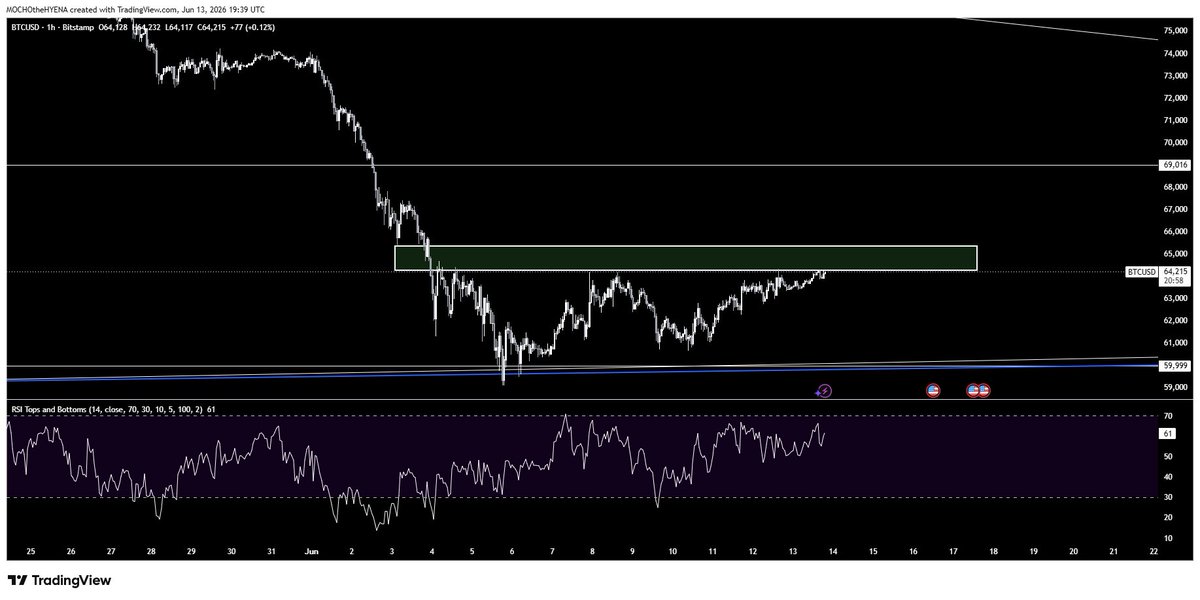

Jun 13

here we go again or these guys sing the MOU, or is because the love ¡bombs lol

Jun 13

IRANIAN FOREIGN MINISTRY SPOKESPERSON SAYS IRAN WILL HAVE TO CHARGE FOR SERVICES PROVIDED IN STRAIT OF HORMUZ -FARS NEWS AGENCY

881

mocho17™®© retweeted

Jun 12

"I missed AI. I can't buy in at these sky high valuations"

112

95

1,969

280,593

mocho17™®© retweeted

Jun 13

Pakistani Prime Minister: We are preparing for the electronic signing ceremony of the peace agreement between the United States and Iran immediately upon its completion.

23

34

238

34,406

mocho17™®© retweeted

Jun 13

JUST IN: Telus spending $66B and $AMPG seems to be involved.

Connect these two dots.

The timing is almost too good. 👀

AmpliTech MASSIVELY DERISKED after this.

➟ May 19: Telus announces a $66 BILLION investment plan for Canada. One of its pillars: converting its old corporate buildings into residential housing under "Telus Living."

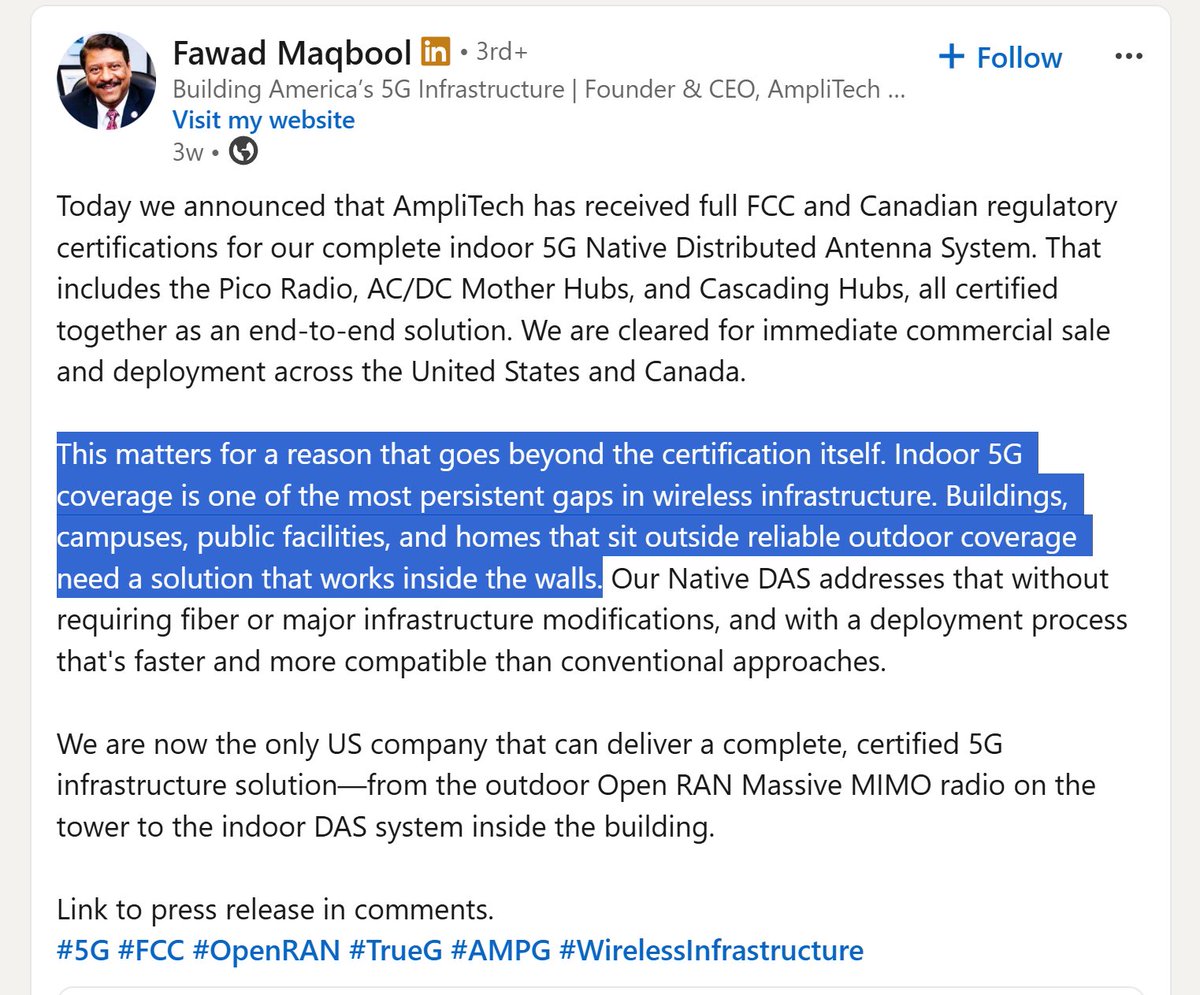

➟ May 20, one day later: AmpliTech announces it received full FCC AND Canadian (ISED) regulatory certifications for its complete indoor 5G Native Distributed Antenna System. Pico Radio, Mother Hubs, Cascading Hubs. The entire end-to-end stack, cleared for immediate commercial sale and deployment across North America.

Now think about what an office-to-residential conversion actually needs.

Thousands of new apartments inside thick old buildings.

Every single one needs indoor 5G coverage.

That's literally what a DAS is for.

And who would Telus call for that?

Maybe the company whose radios are already deployed on its network.

Per Telus's own VP, every Telus Open RAN site already runs AmpliTech antennas, 2 of the 5 radios per sector.

AMPG isn't a stranger knocking on the door.

It's already inside the house.

Now it has the certified indoor product, approved specifically for Canada, the day after Telus announced the buildings.

Honest framing, because I always give it: neither announcement mentions the other. This is me connecting dots, not a disclosed deal.

The certification was surely in the works for months regardless. But an existing Telus supplier getting its indoor 5G system certified for Canada, one day after Telus commits billions to refilling buildings with residents who need coverage... those are the kinds of dots I don't ignore.

Watch this space.

Not financial advice. I'm long $AMPG. DYOR. 📡

12

24

215

33,676

mocho17™®© retweeted

$AMPG

Current price = $8.40

$10 = $260 million market cap

$15 = $390 million market cap

$20 = $520 million market cap

$30 = $780 million market cap

$40 = $1 billion market cap

$50 = $1.3 billion market cap

We are still so early. ⏳

6

16

152

19,845

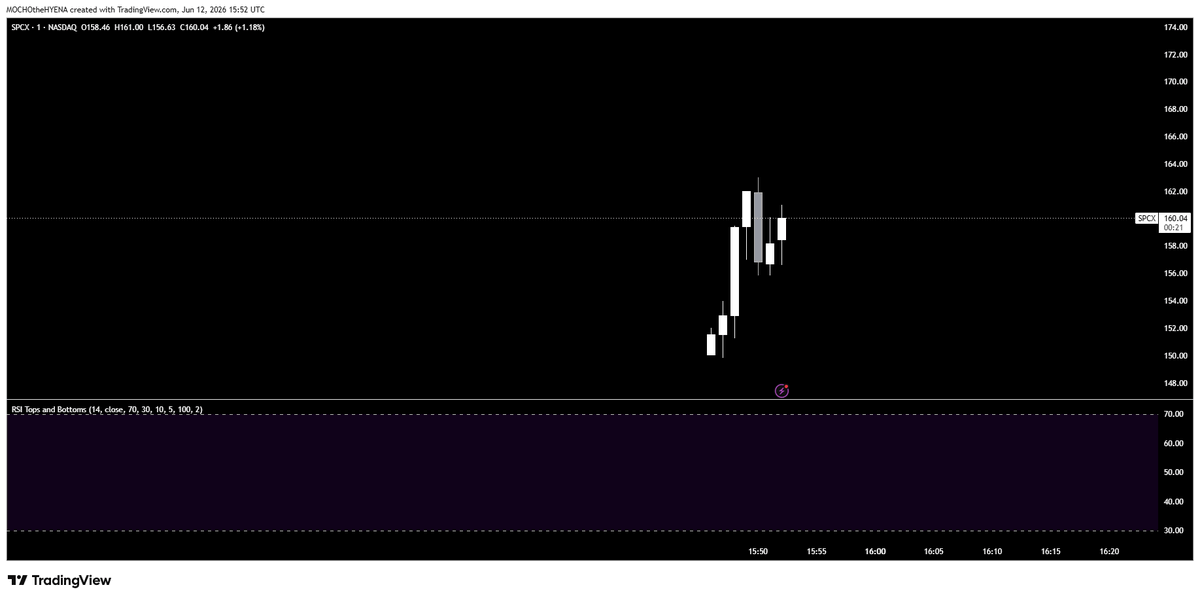

Jun 13

This is really good as the new holder basis is 160 / 164 x share bullish for the next 15 days

Jun 13

517 MILLION SHARES CHANGED HANDS IN ONE DAY — ALMOST MATCHING SPACEX’S ENTIRE IPO SIZE

1

1

883

mocho17™®© retweeted

Jun 12

MSCI: SPACEX ADDED TO STANDARD AND LARGE CAP INDEXES

44

74

1,028

201,222