CUATS

Joined August 2016

- Tweets 159

- Following 110

- Followers 954

- Likes 15

106 Photos and videos

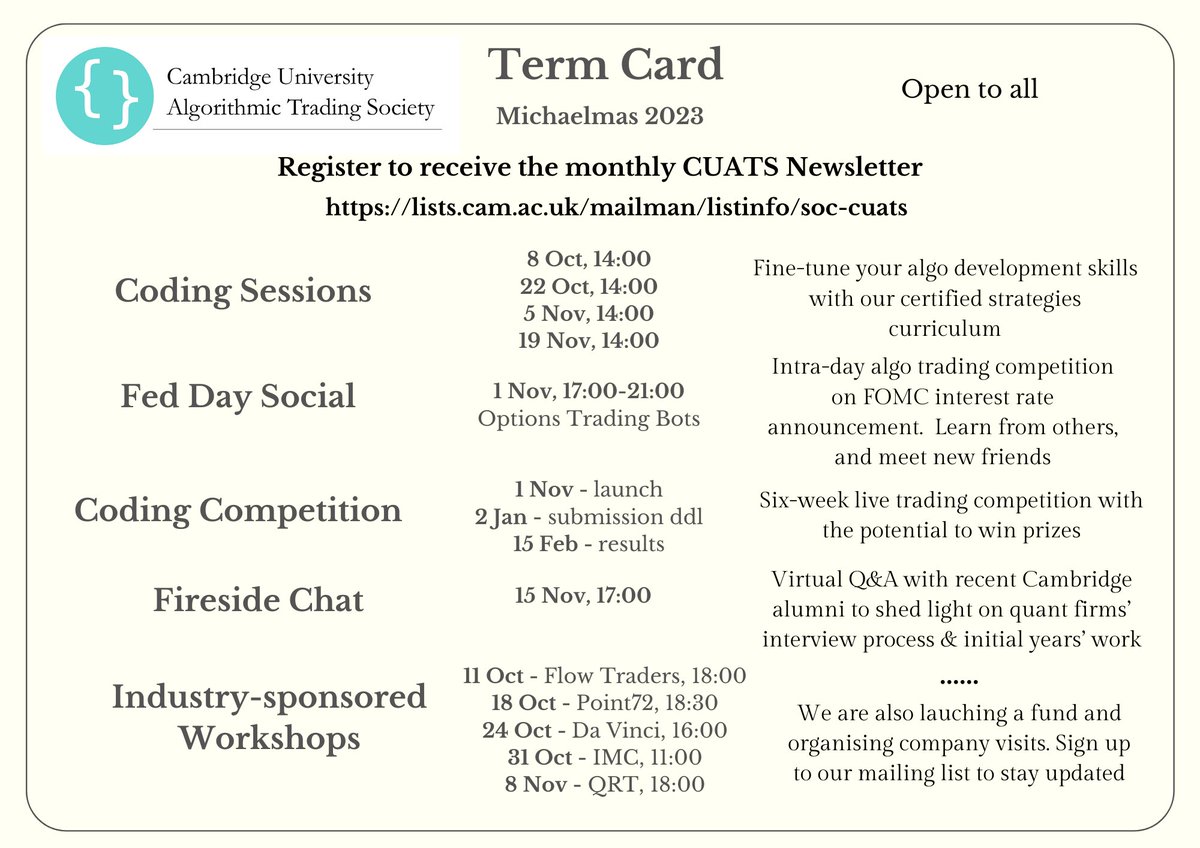

Our first Coding Session of Michaelmas term 2023 on Sun, 8 Oct had a record attendance! Join us at the next one on Sun, 22 Oct., 2:00pm-5:00pm in the University Centre (Hicks Room). Registration is required and a link will be sent by 15 Oct. Book early!

1

7

1,072

Welcome back! We will be at Freshers' Fair (Marquee Three, stall F10) on 3-4 Oct. We have a fantastic line-up of events to kick-off Michaelmas term including Coding Sessions, Industry-sponsored workshops, and competitions. We look forward to your participation!

3

986

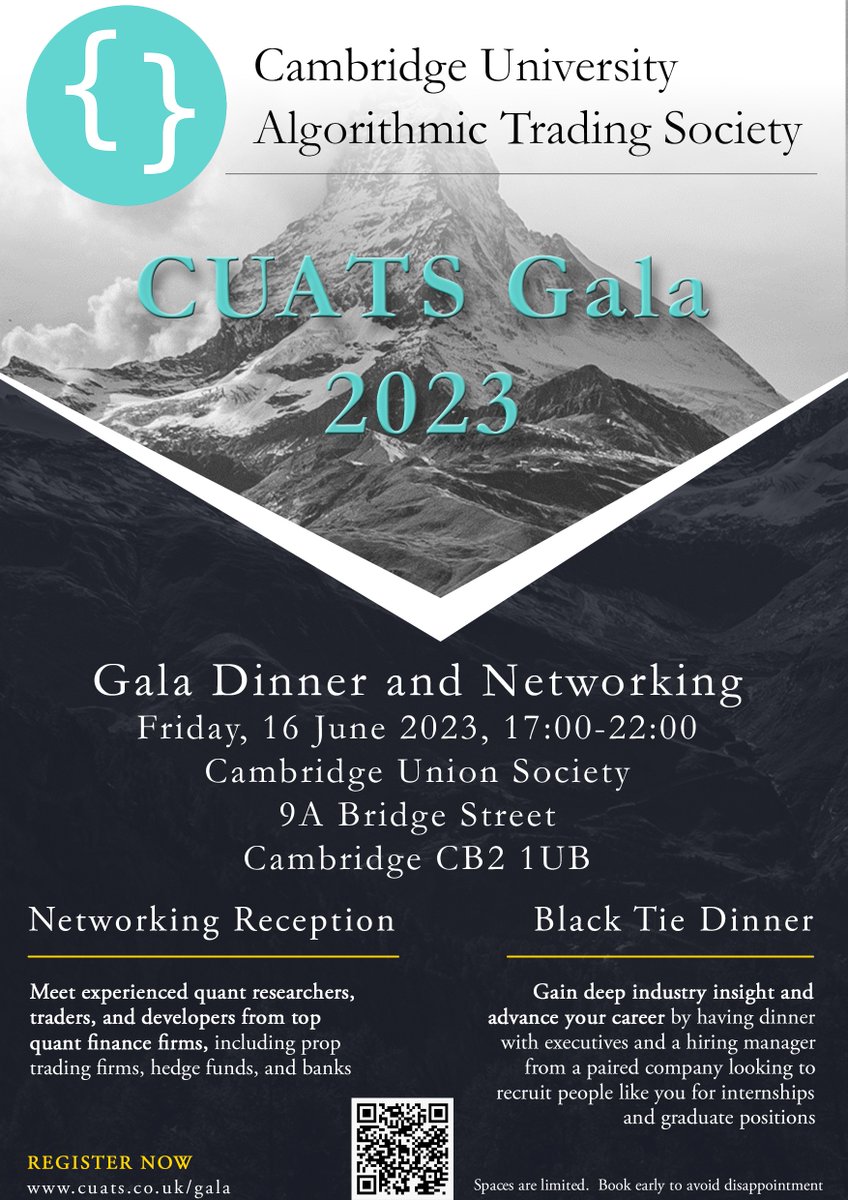

Our flagship event of the year - the CUATS Gala 2023 - will take place on Fri, 16 June, 5:00-10:00pm, in the Cambridge Union Society. This black-tie networking dinner and recruitment event with top hedge funds and prop trading firms is not to be missed! cuats_gala2023.eventbrite.co…

1

741

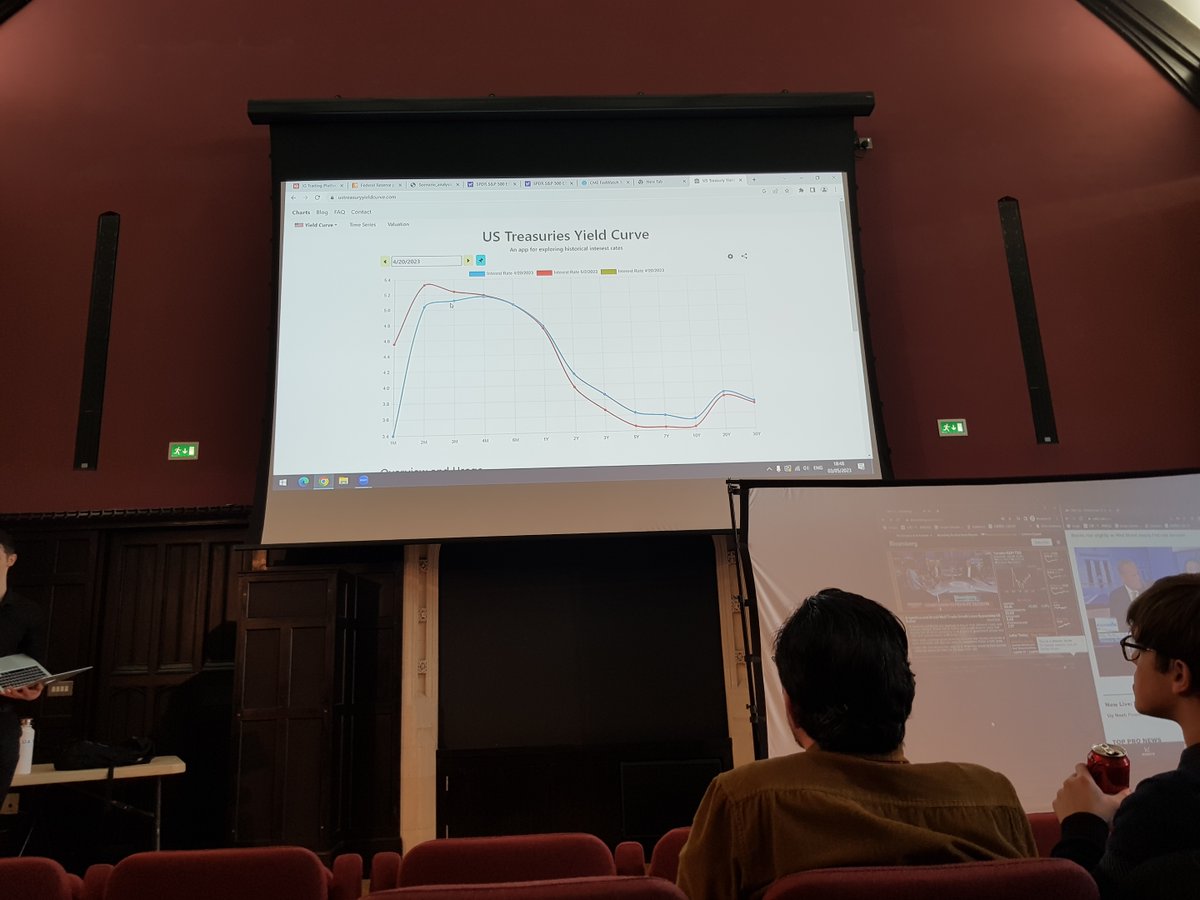

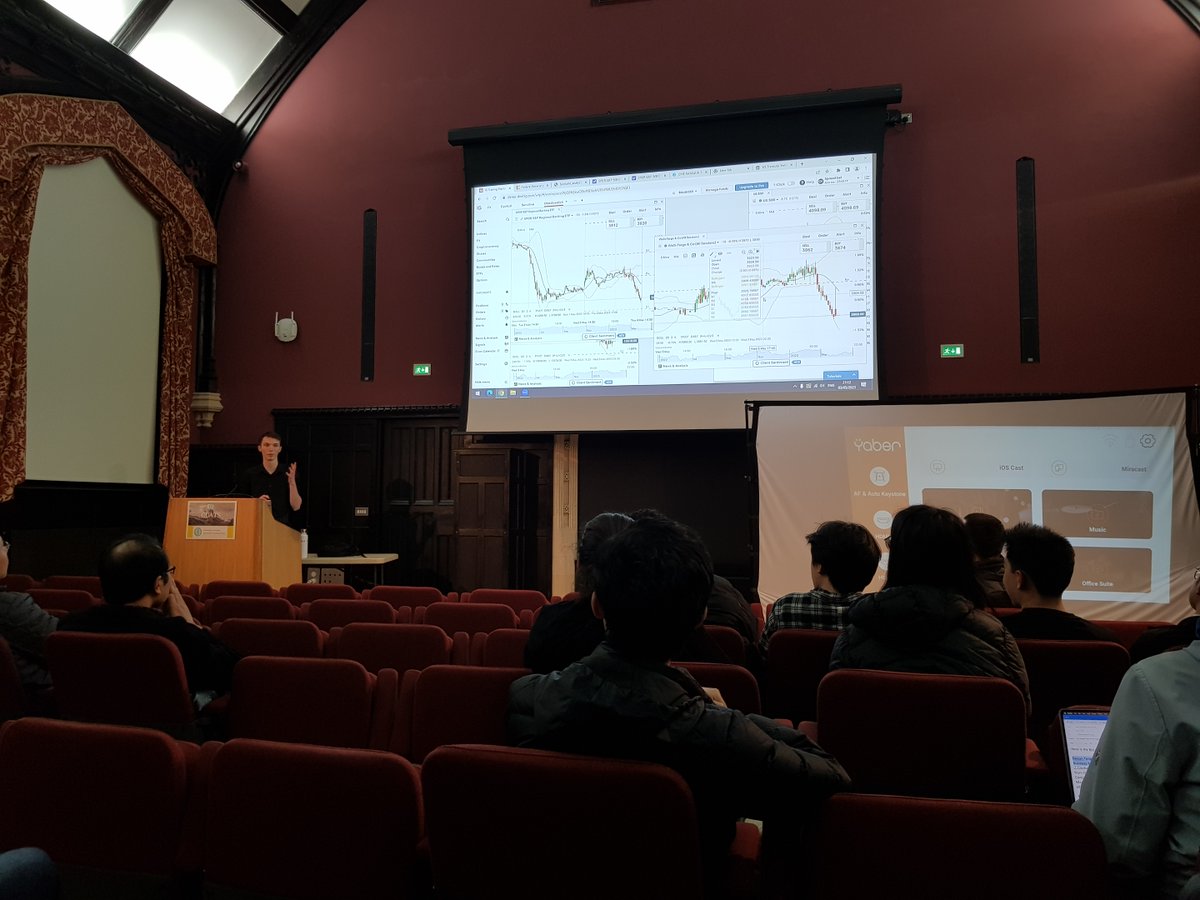

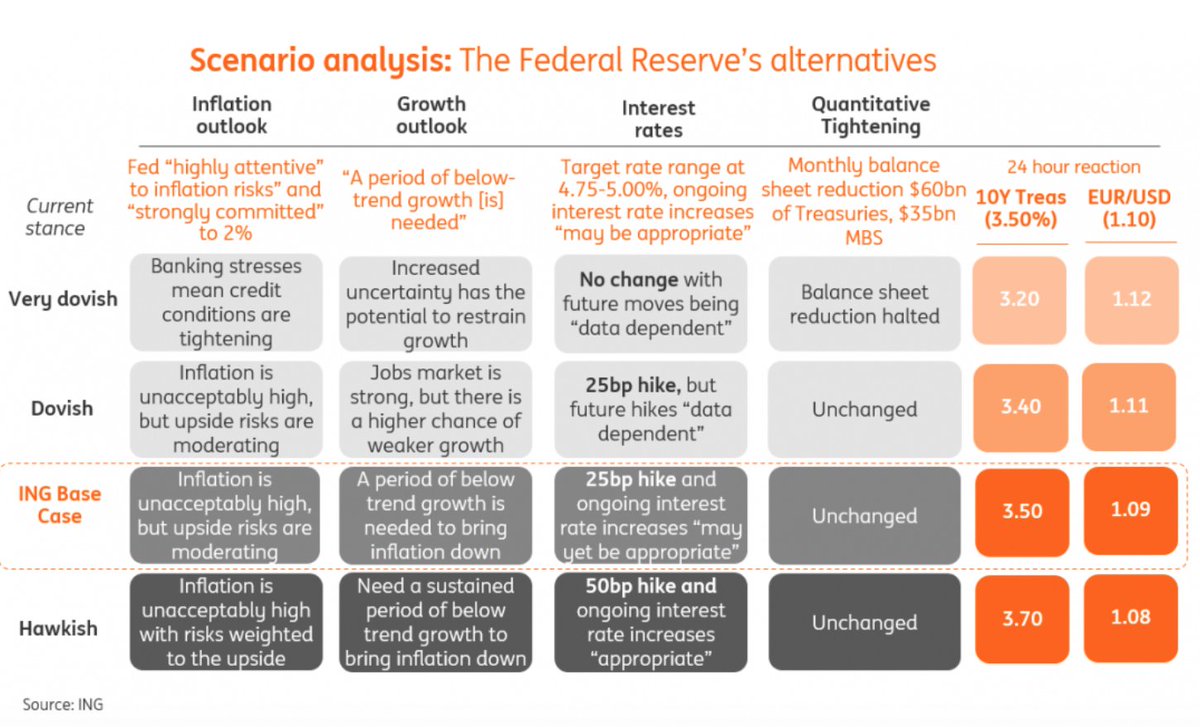

Join us for a Fed Day Social on Wed, 14 Jun, 5:30-10:00pm, in the Auditorium of The Old Divinity School, where we will demonstrate live systematic trading around the Fed announcement and press conference using algorithms developed by teams of CUATS members cuats_fedday4.eventbrite.co.…

502

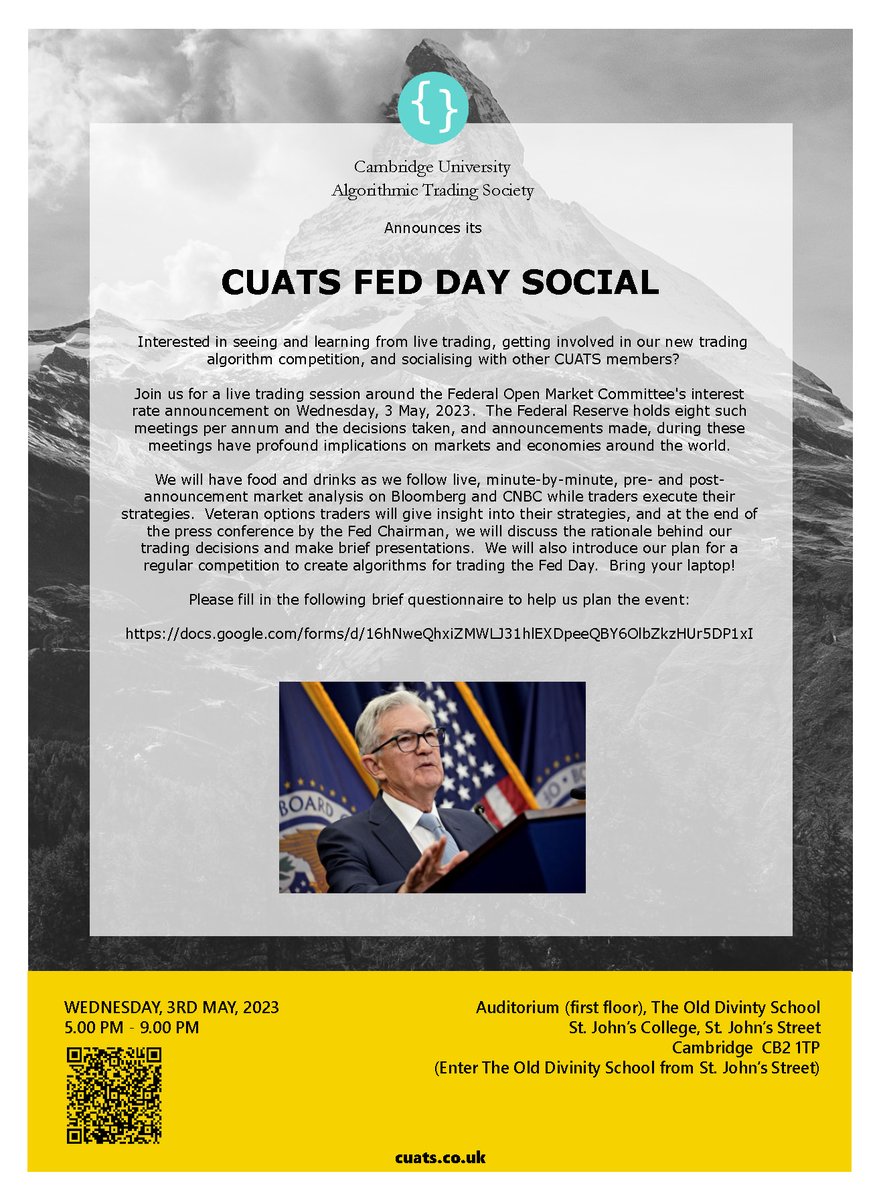

We will be holding our last Coding Session of Easter term on Sun, 11 June, 2:00-5:00pm, in the University Centre, Granta Pl, Mill Lane, where we will cover a trading strategy around the FOMC interest rate announcement. To attend, please register at: cuats_event57.eventbrite.co.…

411

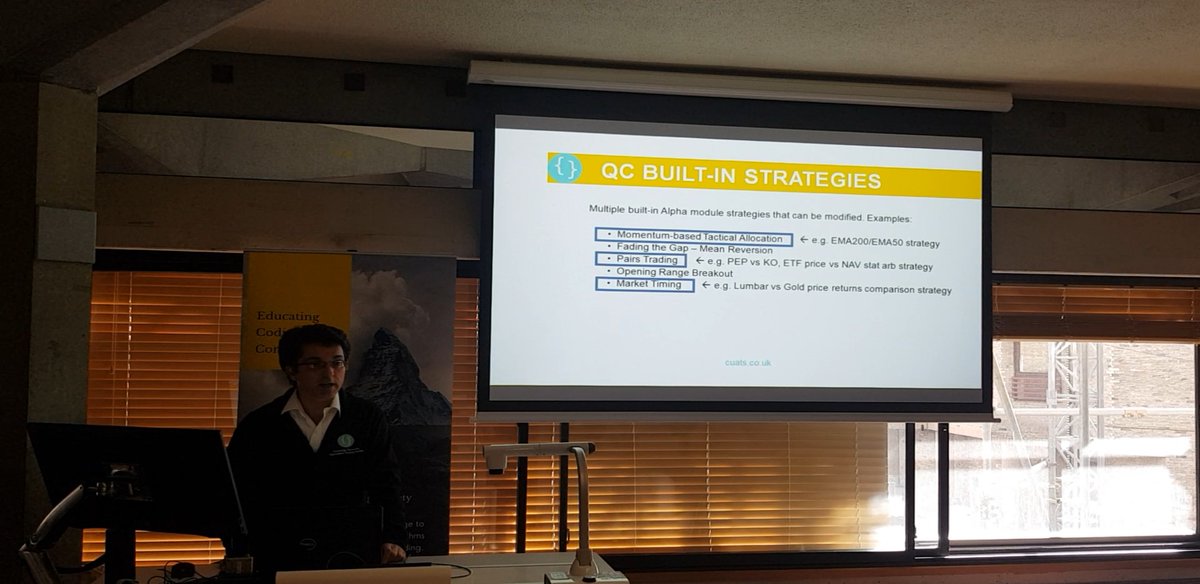

Our first CUATS Coding Session of Easter term 2023 will be on Sun, 14 May, 2-5pm, in the University Centre, Granta Pl, Mill Lane, covering portfolio optimisation and efficient asset allocation. To attend, please register at:

cuats_event56.eventbrite.co.…

1

302

Our next Speaker Series talk will be on Wed, 10 May, 5:30-7:00pm, in the Auditorium, Old Divinity School, with Robert DeWitt, MD & Head of Quant Strat Group Algo, BofA Securities speaking on "Deep Learning for Price Momentum Forecasting." Registration at:

cuats_event55.eventbrite.co.…

281

Our third CUATS Fed Day Social took place on Wed, 3 May, in the Auditorium of the Old Divinity School, across from St. John's College, a welcome break from studying for exams. Next one on Wed, 14 Jun.

cuats_event54.eventbrite.co.…

220

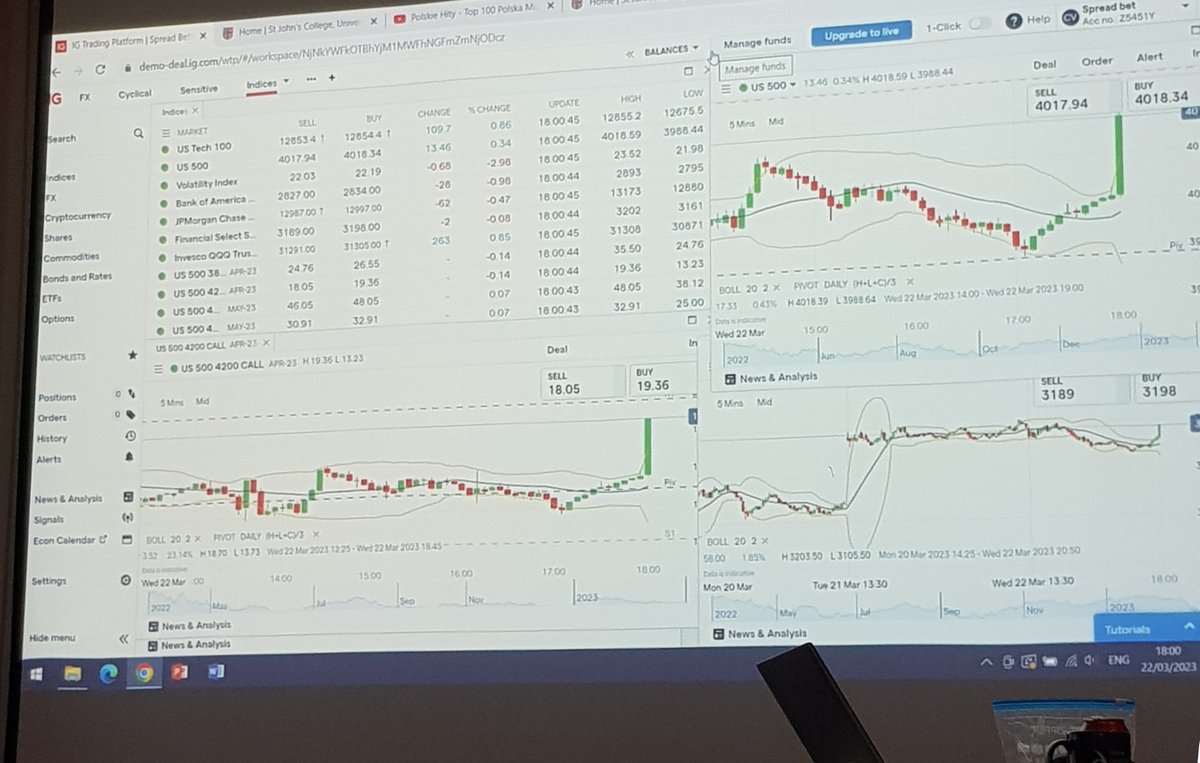

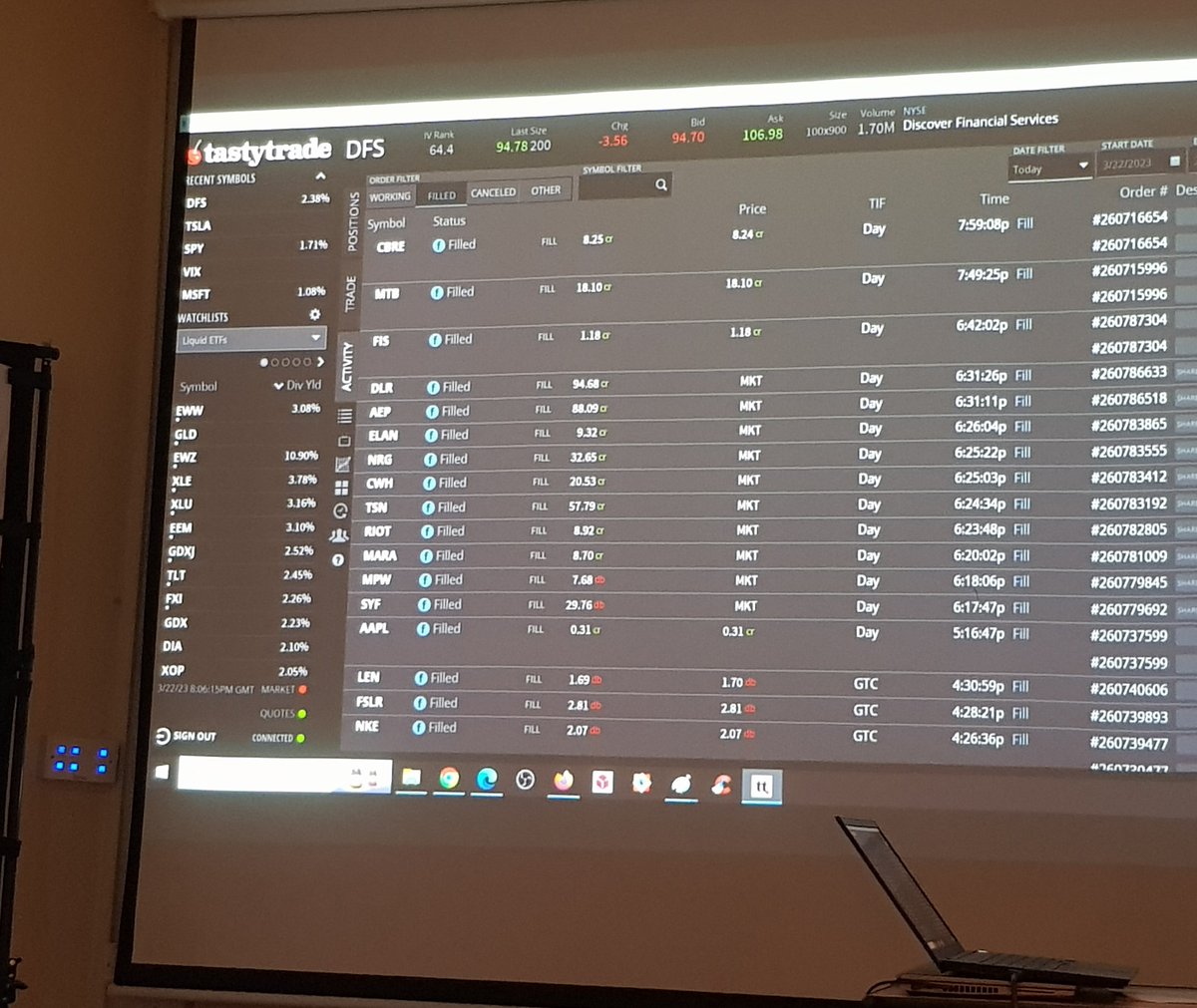

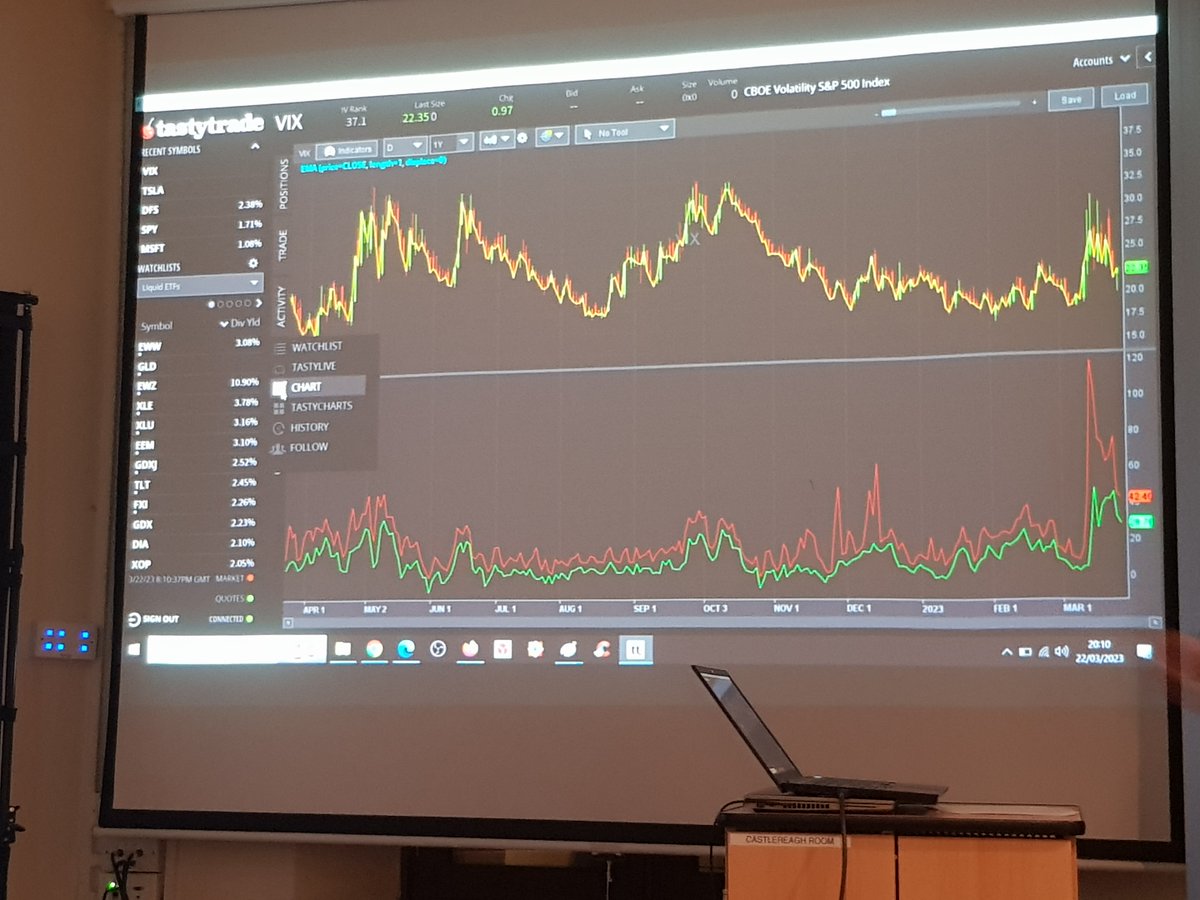

On Wed, 22 Mar, we held our second CUATS Fed Day Social, a live trading event centred around the Fed interest rate announcement. cuats_event52.eventbrite.co.…

188

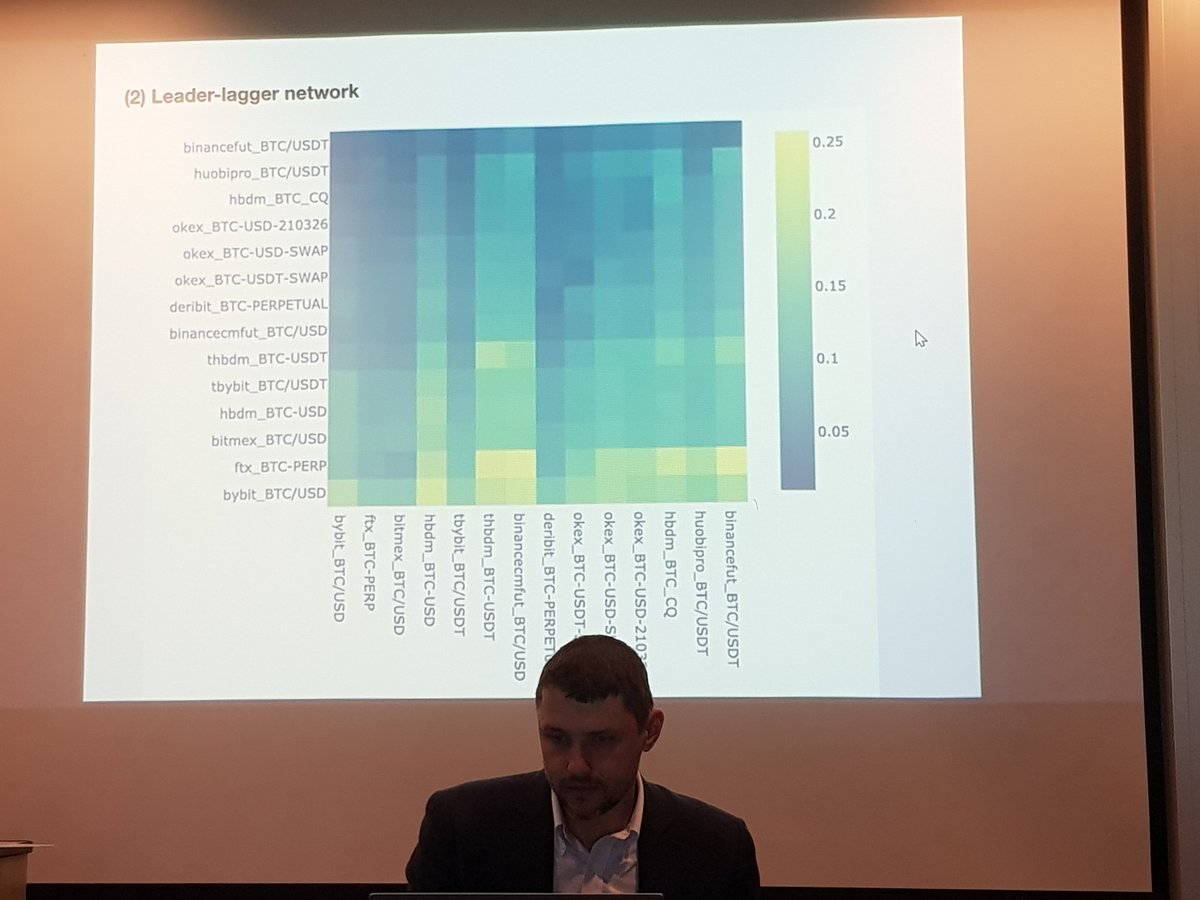

On Tue, 21 Mar, Dr. Alex Shestopaloff, Lecturer at QMUL, presented the CUATS Speaker Series talk for Lent term 2023 titled "Fragmentation, Price Formation, and Cross-Impact in Bitcoin Markets" cuats_event51.eventbrite.co.…

213

On Sun, 5 Mar, 2-5pm, we held our third CUATS Coding Session of Lent term 2023 in the University Centre, 1st floor (Meade Room), examining options skewness

cuats_event50.eventbrite.co.…

155

We held our second CUATS Coding Session of Lent term 2023 on Sun, 19 Feb, 2-5pm, in the University Centre, 1st floor (Meade Room), covering options pricing

cuats_event49.eventbrite.co.…

138

We hope you enjoyed the interaction between academics and practitioners and found the conference both stimulating and beneficial. We look forward to seeing you at next year's CUATS Quant Conference!

228

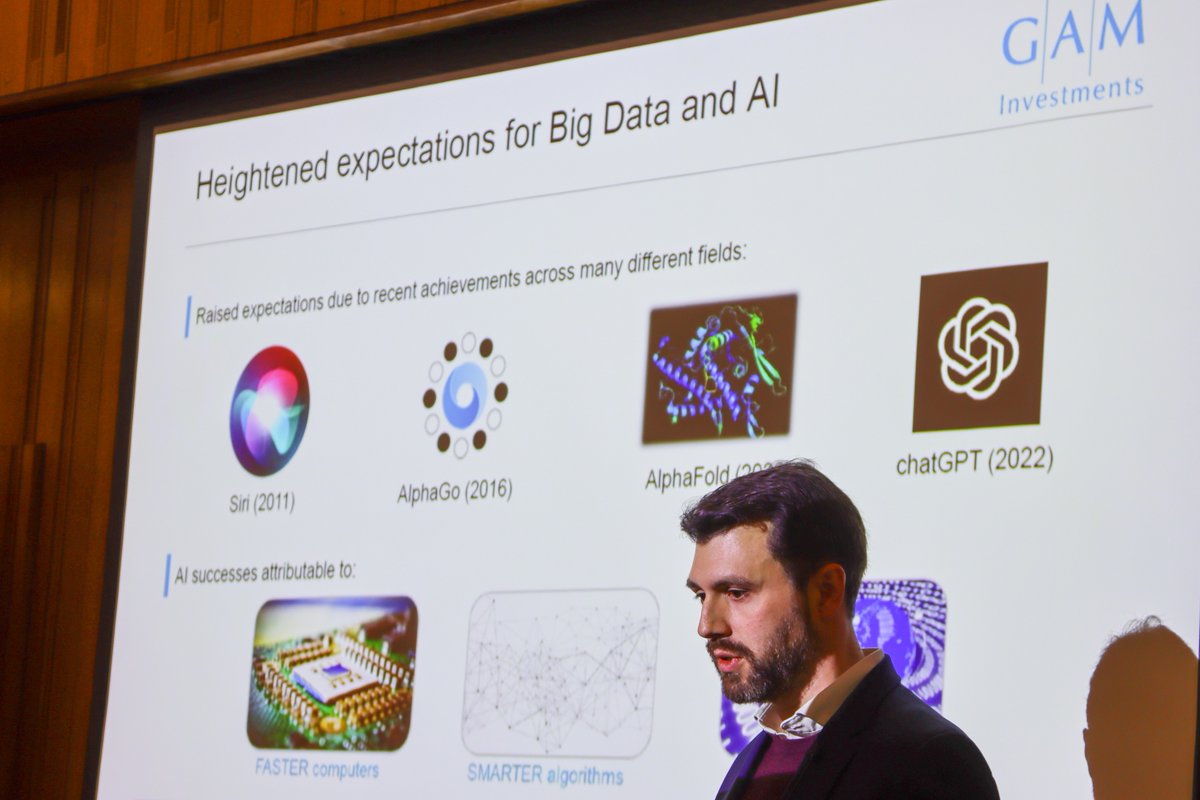

bond portfolio optimization (Marielle de Jong - Grenoble Ecole de Management), deepRL to build alpha portfolios (Will Cong - Cornell), price models from NLP generated sentiment analysis (Matthias Uhl - UBS), and challenges of small data problems (Chris Longworth - GAM Systematic)

1

317

Thank you to all who attended the annual CUATS Quant Conference 2023 on 22 February cuats.co.uk/conference to hear presentations on the effect of order flow on prices (Daniel Giamouridis - BofA Securities), universal impact modeling (Iacopo Mastromatteo - CFM), bond portfolio

216

On 1 Feb we launched the CUATS Fed Day Social - a social event with a trading theme around the FOMC rate decisions where we monitor pre- and post-announcement market moves and make trading decisions & discuss the rationale behind them. Next one on 22 Mar

cuats_event48.eventbrite.co.…

253

Welcome back! Our first Coding Session of Lent term 2023 will be this Sun, 22 Jan, 2:00pm-5:00pm in the University Centre, 1st floor (Meade Room), as usual. In this session, we will explore a sector rotation strategy. Registration at cuats_event47.eventbrite.co.…

196

The first CUATS Insight Day took place on 13 Dec to Bank of America in London where we met with Bobby Previti and Daniel Bowerman and toured the trading floor. We plan to organise more CUATS Insight Day in-person visits to firms in the future!

2

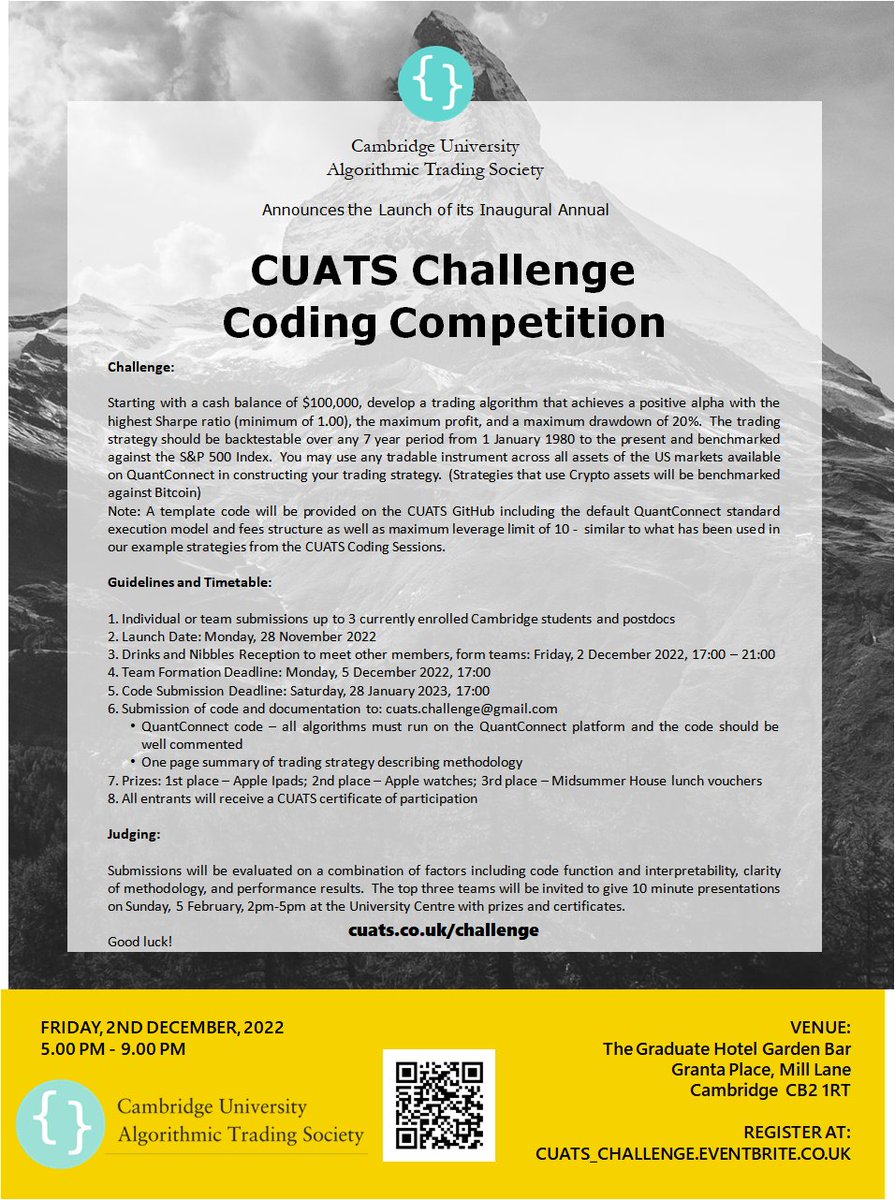

Thank you to all who attended the reception yesterday. If you would like to enter the CUATS Challenge - Coding Competition (either individually or with a team), please send a message to cuats.challenge@gmail.com with your teammates' names and your team's name by Mon, 5 Dec 5pm.

1

We're excited to launch our first CUATS Challenge - Coding Competition! Join us for drinks and nibbles at The Graduate Hotel Garden Room on Fri, 2 Dec, 5-9pm to meet other society members & form teams to develop the best trading algorithms! Register at cuats_challenge.eventbrite.c…

1