Joined January 2024

- Tweets 10,654

- Following 1,191

- Followers 1,168

- Likes 22,200

2,004 Photos and videos

Qubicle | Based Dept. Treasury 🏦 retweeted

THE GOD CANDLE FOR MONDAY IS LOADING

JUST IN: Trump says Iran deal will be signed “within hours” after being delayed by Israel

18

15

438

44,140

Home is at the heart of the American Dream.

Earlier this year, we said every Opendoor buyer would receive a complimentary American flag and flagpole kit to mark the special moment. Today, on Flag Day, we're making good on that promise.

As of today, Flag Day, buyers who purchased an Opendoor home in 2026 can claim theirs after closing.

Read the story: opendoor.com/articles/flag-d…

4

15

89

5,767

Qubicle | Based Dept. Treasury 🏦 retweeted

Earlier this year I said every Opendoor buyer would receive a complimentary American flag and flagpole.

As of today, Opendoor buyers can claim their American made American flag. Home is at the heart of the American Dream. Happy Flag Day, America!

opendoor.com/articles/flag-d…

36

48

518

16,343

Qubicle | Based Dept. Treasury 🏦 retweeted

Jun 12

May 24

What's a video that defines Peak Woke?

20

146

3,273

50,534

RT @MoneyFolder5: You don't understand how much the world has changed in such a short time lmfao

2,005

Qubicle | Based Dept. Treasury 🏦 retweeted

Jun 12

You know what, HELL YEAH.

155

475

5,865

1,313,071

if datadog calls me one more time from a random phone number im going to snap my phone in half

1

1

147

most aggressive sales team I've ever experienced. over 100 calls the last 2 years, different phone numbers, emails, texts. get the hint bro

1

1

99

Qubicle | Based Dept. Treasury 🏦 retweeted

Jun 12

great post by @cubeqube; thanks. just deconstructing the opendoor-zillow warrant structure a bit more here. why tranche 1 is just the start, and it could possibly get better from here.

according to the opendoor’s latest 10-q, @zillow officially vested tranche 1 (300k shares) of those 2022 partnership warrants. some of you might be wondering why it took four whole years just to hit milestone one, and what it means going forward.

here is some food for thoughts:

1️⃣ why did tranche 1 take so long?

the timing was just brutal. right after they signed this in july 2022, the fed started spiking interest rates, which completely froze the housing market. add in the fact that the zillow integration rolled out super cautiously city-by-city rather than nationwide overnight, and possibly the milestone meter was barely moving for two years. it wasn’t until opendoor stabilized its unit economics and scaled "opendoor 2.0" that zillow's funnel finally caught real traction. also, at the same time, opendoor had to play defense, tightening its buy-box and pausing heavy acquisitions. it'd be interesting to know how much of tranche 1 success comes from post-kaz and kaz era, but i think this is not something that @nejatian can publicly disclose.

2️⃣ the clock is ticking (and zillow knows it)

the entire agreement has a hard deadline in july 2027. zillow only has about a year left to unlock the remaining 5.7 million unvested shares. since these tranches vest sequentially based on cumulative referral fees, zillow has a massive incentive to push as many clean, high-quality seller leads to opendoor as possible right now. if they don't optimize the funnel today, they permanently lose out on millions of shares of potential upside.

3️⃣ credit where credit is due. this contract protects us even though old management drafted this, you have to admit it was engineered beautifully to protect retail shareholders from toxic dilution.

first, the exercise price has a hard floor at $15.00; meaning zillow can't dilute the company at pennies on the dollar.

second, the net exercise math means far fewer shares actually hit the float than the headline numbers look like.

third, and more importantly imo, opendoor holds the ultimate veto: they have the right to cash-settle any exercise. if the stock is absolutely ripping, opendoor can refuse to issue new shares and just cut zillow a check for their net profit instead.

and fourth, the $30.00 max cap ensures zillow has serious skin in the game (and you need this in partnership). if they push incredible volume and help send the stock past $30 into the stratosphere, their strike price stays locked at $30, giving them a guaranteed discount and a multi-million dollar payday.

the bottom line:

this setup aligns perfectly with the exact capital allocation rules kaz keeps preaching: zero dilution happens unless shareholders get massive value first. zillow is highly motivated to pump transaction volume before july 2027, and opendoor holds all the structural leverage.

Did you know about Zillow's ($Z) bet on $OPEN 🚪 ?

$30 by Q2 2027 🐂

1

2

13

1,688

Qubicle | Based Dept. Treasury 🏦 retweeted

Jun 11

the war is officially over one day before the biggest ipo in history

153

273

7,443

647,201

Qubicle | Based Dept. Treasury 🏦 retweeted

BREAKING: President Trump says that Iran's Supreme Leader has approved a deal between the US and Iran and a signing is "coming soon."

Details of the deal per President Trump:

1. US Naval blockade is lifted once the deal is signed

2. Memorandum of Understanding has been approved by "everyone in Iran"

3. Kharg Island operation by US Military is now "off the table"

4. Formal Strait of Hormuz reopening deal expected by as early as Saturday or Monday

5. Trump declines to set a deadline for the deal, calling Iran "rational and confident" that a deal will be reached

US oil prices extend losses on the news.

745

618

6,210

839,799

Qubicle | Based Dept. Treasury 🏦 retweeted

Jun 11

We just held our shareholder AGM and the preliminary results suggest shareholders backed every single one of our proposals.

Thank you! We will not let you down.

168

136

1,602

93,633

Qubicle | Based Dept. Treasury 🏦 retweeted

BREAKING: US oil prices collapse below $87/barrel after President Trump cancels scheduled strikes on Iran.

346

852

6,076

1,624,160

Every SaaS needs a Compliance page where you can easily pull compliance information about your instance and controls your instance meets or does not meet that can be used as evidence of compliance. GCP has this with Security Command Center -> Compliance, Azure, AWS, and a few others also have it. Surprising how rare it is though with the direction software compliance is headed

1

1

55

Qubicle | Based Dept. Treasury 🏦 retweeted

Jun 11

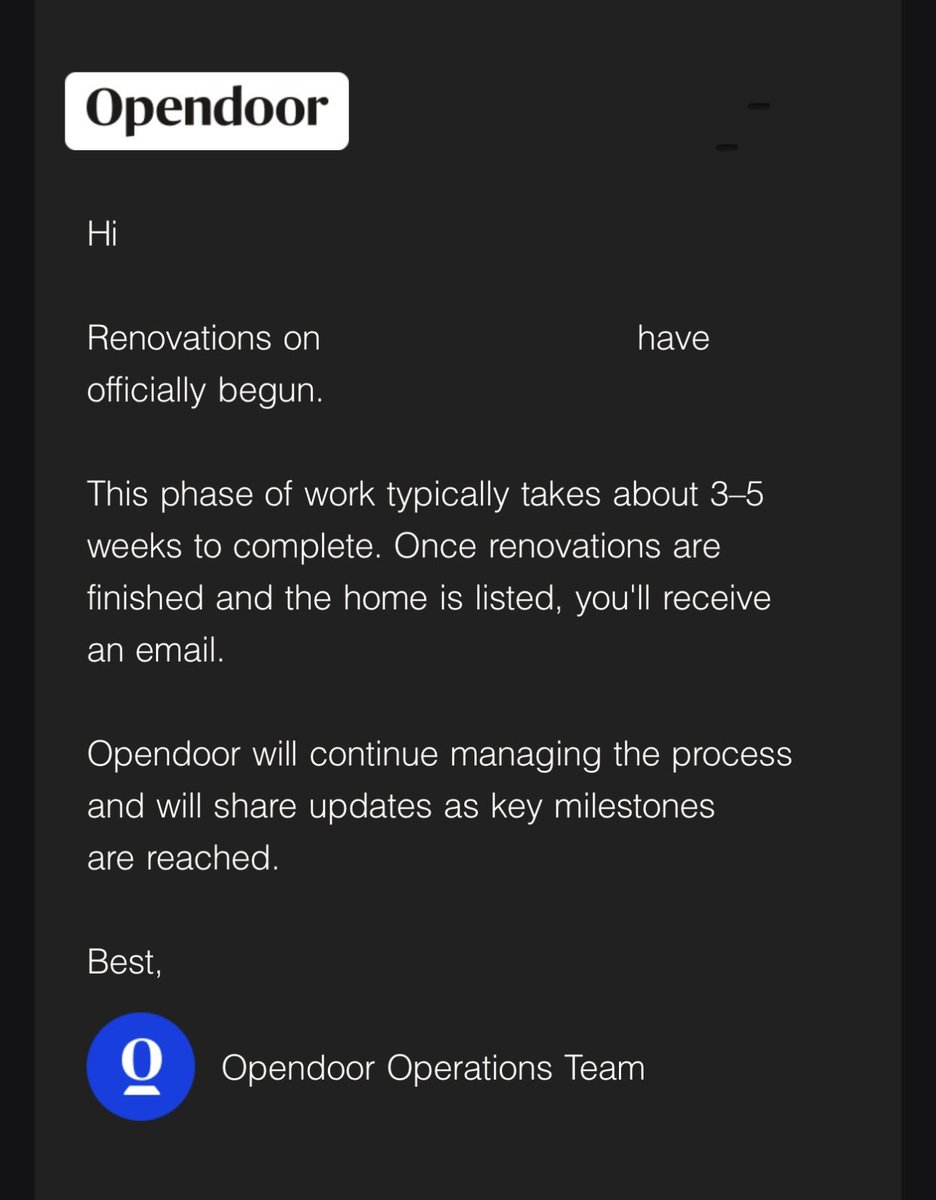

Just got the update that renovations are starting on the property we sold to @Opendoor last week!

Pretty nice knowing renovations are underway and I don’t have to lift a finger yet still get some of the upside when they sell down the road.

Will be fun to see how this plays out, stay tuned! $OPEN

6

17

111

6,448