Enigma Capital. Interests: Physics, Art, Crypto, Systems, History, Farming, Fishing, Service, Poker, Trends, Markets, Inquiry, Advaita, Tao, Zen, Truth.

Joined August 2012

- Tweets 6,282

- Following 7,062

- Followers 1,677

- Likes 87,598

355 Photos and videos

Pinned Tweet

25 Oct 2023

Crypto bull market cheat sheet:

13

1

72

7,979

I'm hiring another Swift /SwiftUI developer for a new consumer social product I build. I want someone with exceptional attention to detail who can think like a user.

4

2

14

560

I write down some reflections on the MSTR, STRC, and BTC situation and wonder if someone else here with a better understanding of the dynamics has a perspective on it:

I think Saylor might wait for a bit to not look desperate, then increase the STRC dividend to 12%. 1% per month is a far more compelling narrative than 0.96% per month even if it doesn't cost him much in extra expense for the preferred. I assume he intentionally starts STRC with a dividend rate at 9% so that he has room to ramp it up to 12% or more. So at 11.5% he has some room. I think he can probably get STRC back above par with a 12% dividend with this and use the proceeds to raise meaningful cash. He now establishes a precedent for selling BTC as a lever, so selling at substantially higher prices, while still uncomfortable for the market, has less of a "shock" factor. He talks about selling meaningfully appreciated Bitcoin as a lever to potentially fund STRC dividends, so with a cost basis around $75k it doesn't make sense for him to sell a bunch down here at $67k to fund STRC, at least not right now.

2

4

202

Apr 10

Hiring: iOS Web Developer

Looking for a SwiftUI and TypeScript developer to get a new consumer iOS app across the finish line. I want someone with high standards, sharp attention to detail, and experience shipping consumer apps for the v1. DM me.

45

46

1,522

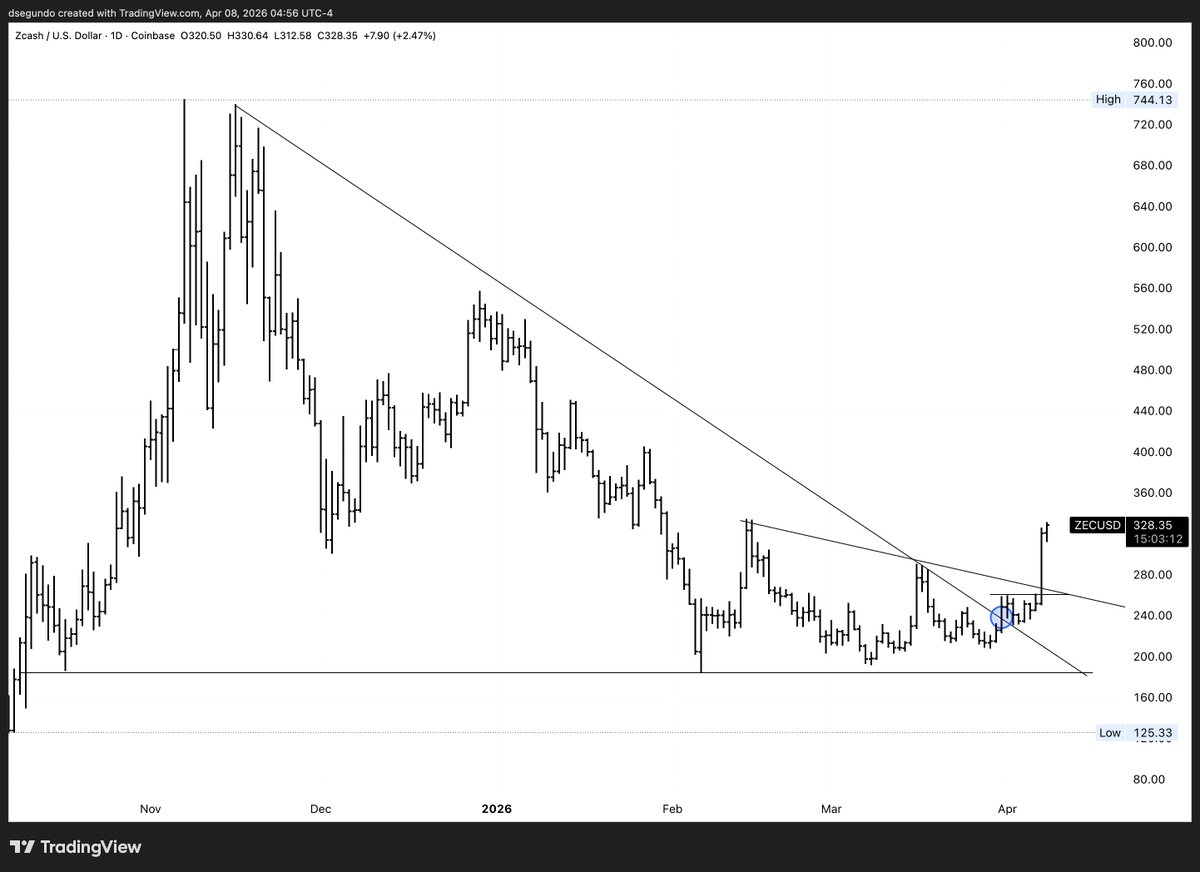

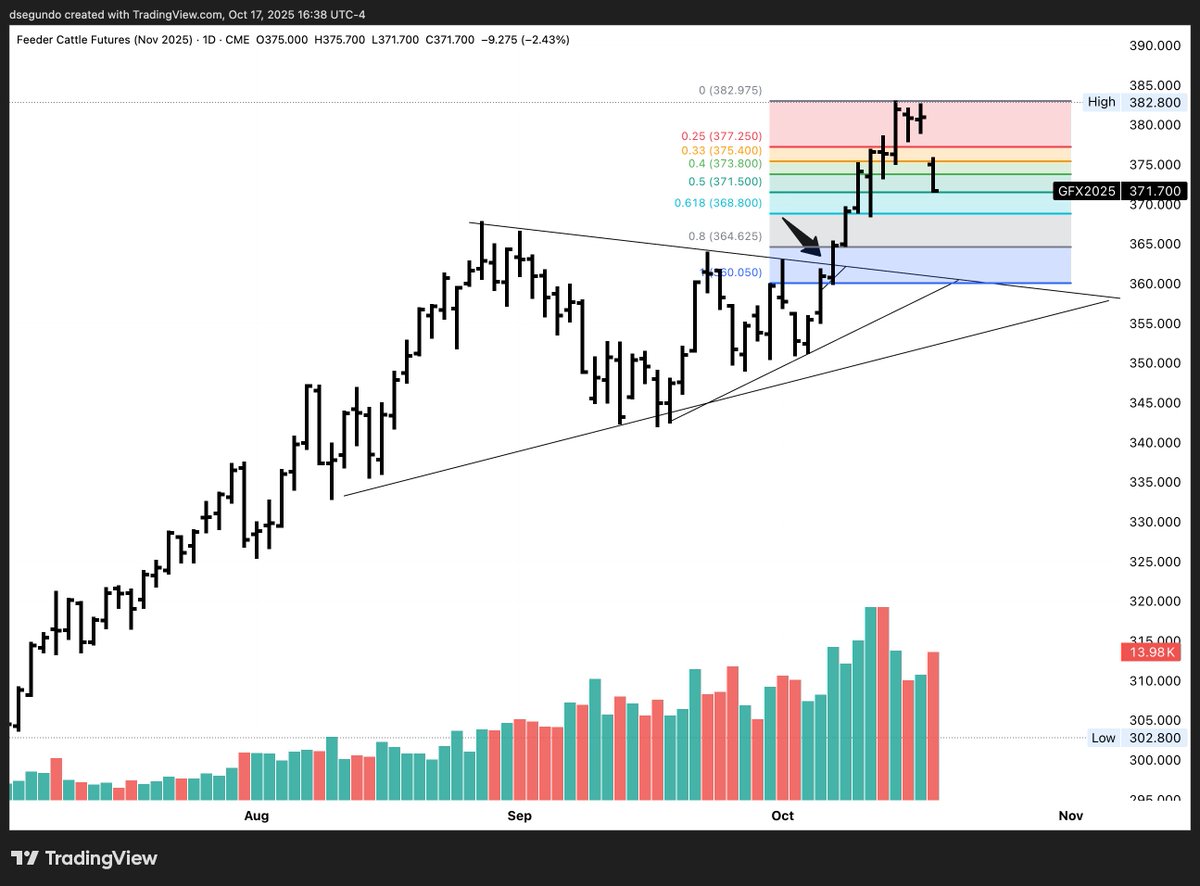

Relative strength between markets really a goated indicator. ZEC shows it lately and that's the canary in the coal mine.

3

112

Mar 23

“If someone asks my abode, I respond: the east edge of the Milky Way.”

— Ryokan

1

3

118

Daniel Segundo retweeted

Mar 18

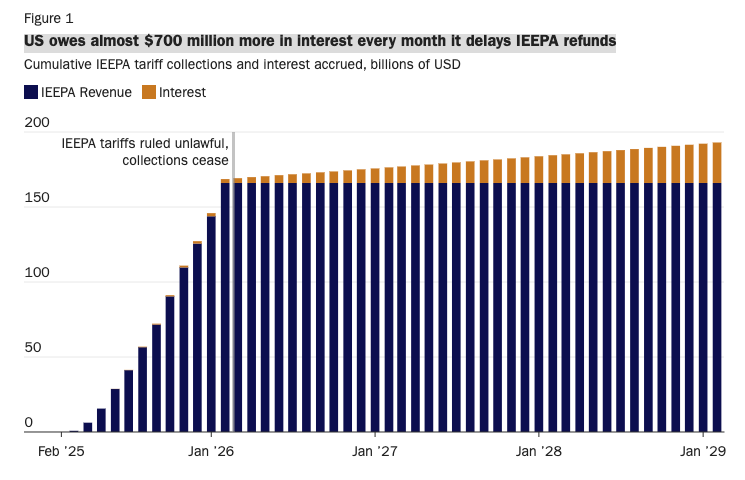

The U.S. owes $700 million more in interest every month it delays IEEPA refunds.

17

90

663

34,041

Daniel Segundo retweeted

Mar 11

Sage advice from Elon:

14

210

2,113

74,733

Mar 10

“Meditate like Christ, he lost himself in love.”

— Neem Karoli Baba

3

5

124

Daniel Segundo retweeted

💯

And what I often see among my most successful clients is a constant comparison to what traders are (supposedly) doing.

That need to be as good or better than someone else is very damaging to a trader's mindset, even successful traders.

Feb 22

Excellently said. I find that a judgment about <not having enough> or some form of lack often accompanies low-discipline forms of trading like daytrading, overtrading, etc.

1

1

13

1,109

Feb 20

"LSD allows you to come into the room and pranam to Christ, but after two hours you must leave. The best medicine is to love Christ."

- Neem Karoli Baba

2

6

149

Daniel Segundo retweeted

Feb 10

“If you want to be successful, I would encourage you to grow a tolerance for failure.”

— Jensen Huang, Nvidia CEO

64

1,134

8,123

164,077

Daniel Segundo retweeted

Feb 5

Stanley Druckenmiller @standuquesne thoughts on hiring a money manager:

"If I were hiring a money manager, the first thing I would look for is if all I heard was they never made a mistake and they’re telling me about all their wins, that is a big red flag. The great money managers I’ve met they generally don’t tell you about their wins, they tell you about a lot of their losses."

6

37

443

36,130