Moving Freight Since 1978🚛💨We’re glad you’re here! Follow along for market updates, info on how to use our products to improve your business, & so much more!

Joined April 2010

- Tweets 9,439

- Following 4,913

- Followers 17,633

- Likes 2,677

3,139 Photos and videos

U.S. manufacturing activity just reached a four-year high🏭🚚

What could that mean for freight demand?

📈 Factory activity continues to gain momentum

📦 Manufacturing remains a key driver of freight demand

🚛 Carriers are watching for signs that stronger industrial activity translates to more freight movement

Could stronger manufacturing activity be an early indicator of what's ahead for freight? 👉 bit.ly/4ejQFyi

2

2

6

224

Deadhead kills margin🚛⛽

Reloads on the Convoy Platform helps cut it by showing what’s waiting at the delivery stop before you book.

See 💰 payout, 📍 deadhead miles, and ⏰ pickup timing right in the load details, then browse next options in-app.

Available now in the Convoy app👀 Want a closer look at how carriers are using reloads? 👉 bit.ly/4uFwUre

1

3

2

235

Yakima is one of the few reefer markets moving in the right direction right now🚛🍒

As summer produce season ramps up:

📈 Yakima rates are gaining momentum

🍒 Cherry season is driving activity

🚚 Capacity is tightening as freight demand increases

While many reefer markets remain under pressure, Yakima is showing signs of seasonal strength.

Is Yakima an early indicator of what's ahead for other produce markets? 👉 bit.ly/4e2ju3k

1

1

203

Fewer storms are expected in 2026, but freight markets should still pay attention🌪️

Even with a quieter hurricane season forecast, freight disruption risks remain.

What signals are you watching as hurricane season gets underway? 👉 bit.ly/4xAvUr0

1

3

179

Hear more from Dean on this week's episode👀 bit.ly/3Sf6Fdo

1

291

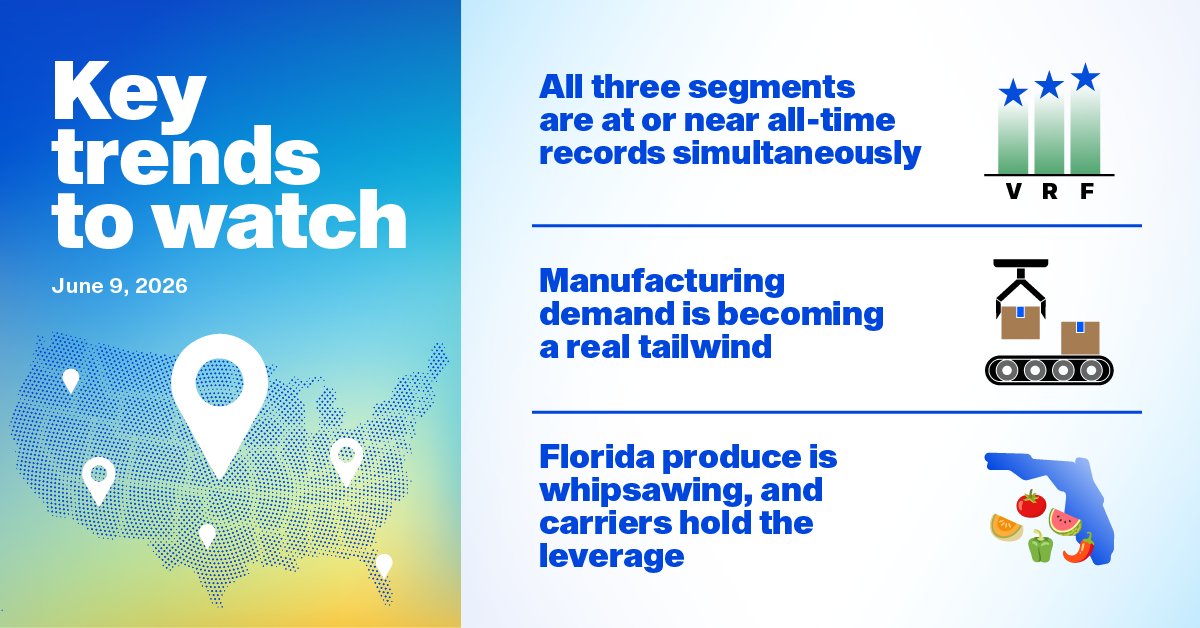

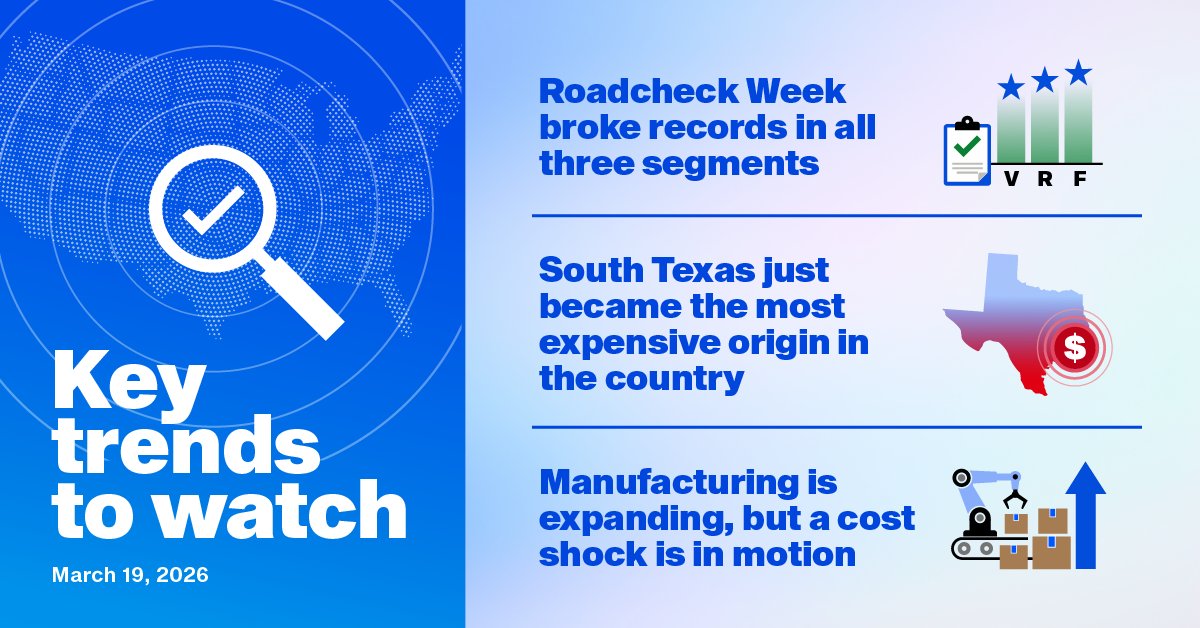

Records are falling. Three more go down.

Flatbed linehaul (rate minus fuel) rates hit $2.93/mile this week, an all-time record, $0.18 above the June 2021 peak after 12 consecutive weeks of gains. Dry van linehaul rates are at $2.39/mile, a new Week 22 record up 43% year-over-year. Reefer is $0.03 from its own all-time mark at $2.69/mile, sitting 37% above last year. Behind the numbers, the demand story is strengthening: the ISM Manufacturing PMI just hit its highest reading in four years, with New Orders at 56.8% and backlogs still building. This isn't just a Roadcheck blip, it’s a sign that the fundamentals are moving.

If you're still pricing freight the way you were last summer, the market has already moved past you.

What's your biggest exposure heading into the back half of Q2?

2

3

4

297

Follow the building permits, and you'll find the freight🏗️🚛

Construction activity across the Southeast is keeping flatbed demand strong.

📦 Lumber, steel, roofing materials & equipment moving

📈 Alabama spot rates up 32% YoY

🚛 Birmingham → Lakeland averaging $4.13/mile ( 28% YoY)

Flatbed carriers, this is the market to watch this week👀

1

2

319

Want to know what’s moving the market this week?👀 bit.ly/4uQxmUe

260

Freight volumes may be holding steady, but transportation costs are telling a different story🚚

According to the latest U.S. Bank Freight Payment Index:

📦 Shipment volumes remained relatively flat

💰 Freight spending increased

🚛 Higher transportation costs continue to put pressure on shippers

It's another sign that market conditions are shifting, even without a significant increase in freight demand 👉 bit.ly/4un5O7L

1

3

3

243

Flatbed freight continues to show signs of resilience🚛

Despite ongoing uncertainty across the freight market, flatbed demand remains relatively steady.

What's supporting activity?

🏗️ Construction spending remains elevated

⚙️ Manufacturing demand is holding up

🚚 Capacity remains relatively balanced in many markets

The latest ATA truck tonnage data points to continued stability for flatbed carriers 👉 bit.ly/43T9eUY

1

2

270

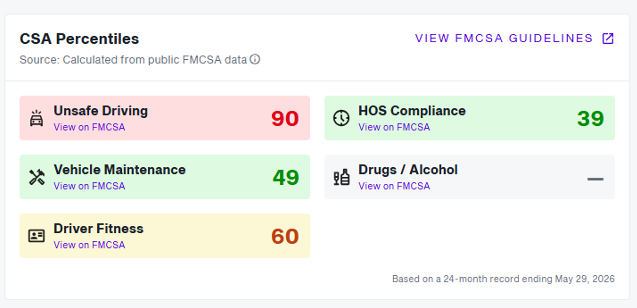

Brokers are under more pressure than ever to document their carrier management decisions.

To help simplify that process, CSA percentile scores are now available on the Company Profile page in DAT One for Carrier Management Suite users.

Having carrier safety data available in the same place brokers are already managing carrier relationships can help:

📋 Streamline documentation

⚡ Reduce the need to switch between systems

📝 Create a clearer record of carrier evaluation

One less gap between due diligence and getting the load covered.

2

1

2

291

Catch the full conversation between Chris Caplice and Ken Adamo👀 bit.ly/42HyzRg

2

6

384

Records are falling, and the market isn't done yet.

Flatbed spot linehaul rates (rates minus fuel) hit $2.89/mile last week, a new all-time high, beating the June 2021 record by $0.14. That's eleven straight weeks of gains, a 21% surge since Roadcheck Week, and a load-to-truck ratio of 76.71. The ATA tonnage index hasn't declined once in 2026. For carriers running steel, lumber, or machinery lanes, the macro setup still favors holding rates through the summer.

Dry van linehaul rates climbed another $0.05 to $2.32/mile, which is 39% above this time last year and just $0.04 shy of the Week 22 record set in 2021. Meanwhile, the Q1 U.S. Bank Freight Payment Index showed freight spending jump 21.8% year-over-year on essentially flat volumes. Shippers are paying more, not because demand broke out, but because supply finally gave way.

On the reefer side, South Texas just gave carriers a reminder: Shortage conditions can reverse in a week. After spiking 25–40% under last week's tight market, rates collapsed by as much as 41% as truck supply normalized. Meanwhile, Yakima Valley availability is tightening without a rate move yet, a classic leading indicator worth watching going into next week.

What does this market look like for your network heading into July 4th?

2

4

474

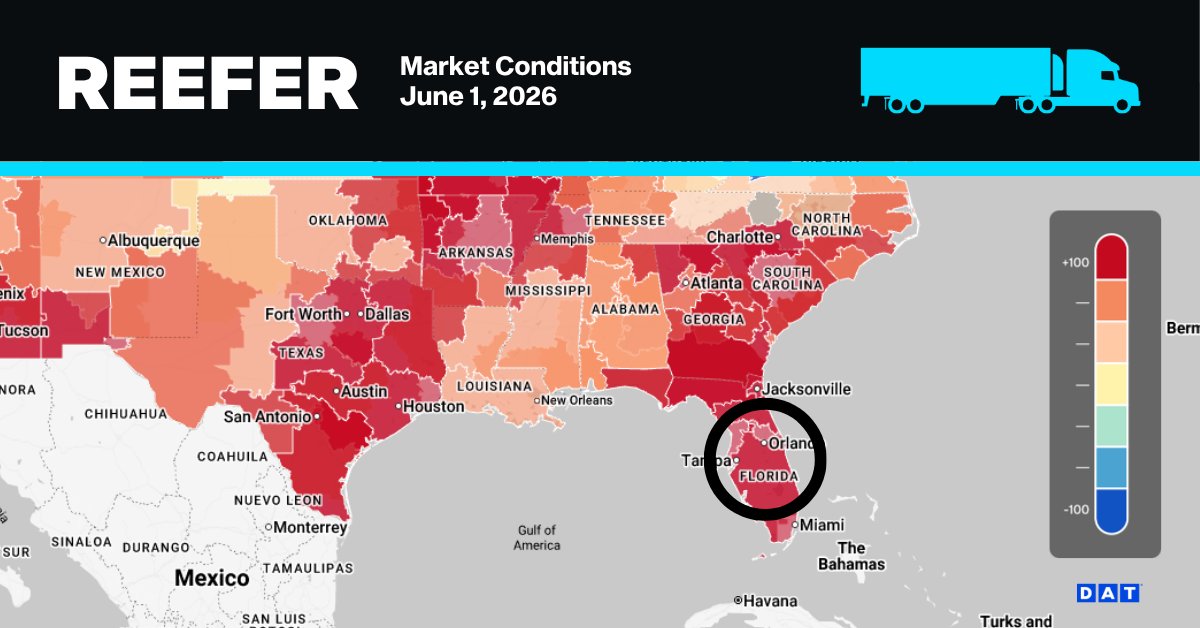

Lakeland is one of the hottest reefer markets to watch this week👀🍉

📦 Florida produce volumes up 32%

🍉 Watermelon shipments up 43%

📈 Lakeland outbound rates continue to climb

1

3

321

What’s shaping the freight market this week? Take a look👀 bit.ly/49x7iVA

1

330

Freight volumes remain soft, but dry van rates aren't waiting🚚

📦 Shipments down 4.4% YoY

📈 Linehaul rates up 5.6% YoY

🚛 Tightening capacity continues to support pricing

The market recovery story isn't just about demand anymore. Are you seeing capacity or demand have a bigger impact on rates right now?👀 bit.ly/4u46e2W

1

3

6

446

When you book a load without picking up the phone

4

239

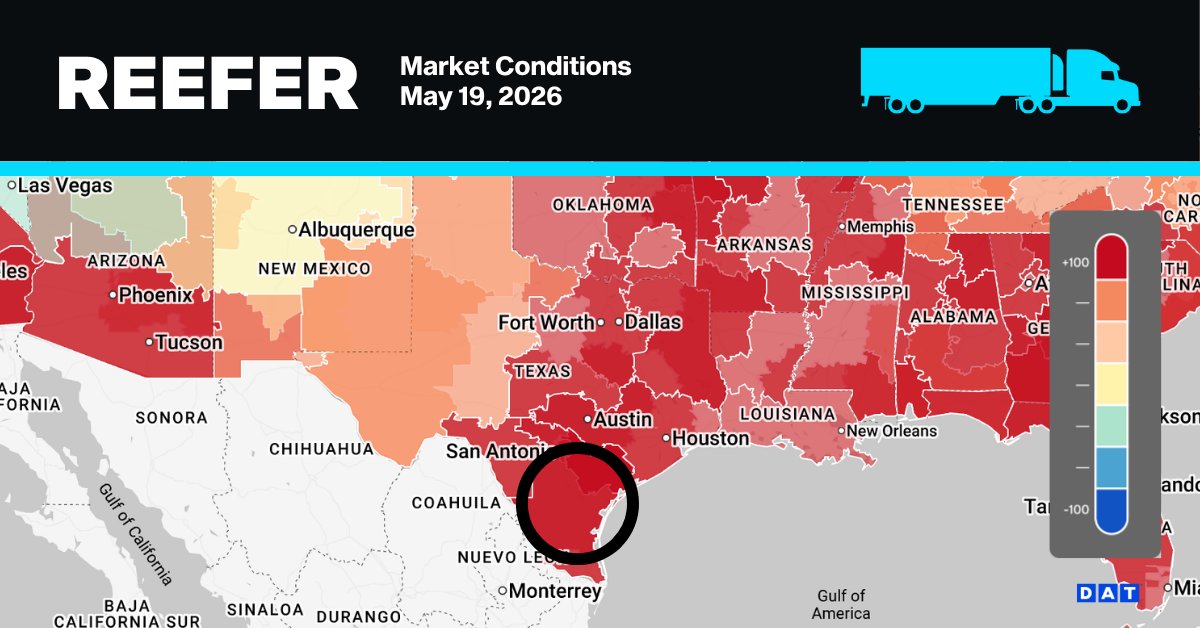

South Texas reefer rates just had one of the sharpest swings of produce season🚛

In just two weeks:

⬆️ Rates jumped 40%

⬇️ Then dropped nearly 40% the next week

What caused the whiplash?

🍉 Produce shifts

🌸 Floral demand fading

🥬 California volumes rising

🚚 Capacity repositioning fast

How are you seeing produce season impact reefer pricing?👀 bit.ly/4vawQQD

1

1

4

315

A unanimous Supreme Court decision could have major implications for freight brokerages🚨

Brokers can now be held liable for negligent carrier hiring, and the ripple effects could impact insurance costs, vetting practices, and smaller brokerages across the industry.

Chris Caplice and Ken Adamo break it all down👀 bit.ly/42ZxUuS

2

1

460

Permian activity is picking back up, and flatbed carriers should be watching 🚛

📦 More energy and oilfield freight returning to the Permian Basin

🏗️ Increased demand for equipment and drilling-related materials

📈 Tightening capacity supporting flatbed demand and spot rates

What could this mean for flatbed rates heading into the next cycle? 👀 bit.ly/3RygPFL

1

3

309