let’s visualize how RWAs could transform money

Joined October 2016

- Tweets 211

- Following 1,052

- Followers 1,233

- Likes 1,820

38 Photos and videos

Pinned Tweet

Apr 21

The core idea behind Reserve is almost 100 years old.

It failed back then for one reason: you needed a physical warehouse.

A digital warehouse is built different.

🗣️ Lawrence H. White at Monetarium 2:

“Going back to the late 19th century, people were worried about instability in the purchasing power of gold under a gold standard.

Even though the long term trend was good, there were short periods of volatility.

An economist named Alfred Marshall said, if the relative price of gold is changing as a result of supply discoveries or demand shocks – and in his day the biggest demand shock was Germany decides to leave the silver standard and join the gold standard – we can diminish the impact of that on the purchasing power of gold by redefining our monetary unit.

The pound would not be defined just in terms of gold, but so much gold plus so much silver. (…)

So you've got two metals defining your unit of account.

That’s a kind of gateway into having a whole bundle of commodities define the unit of account.”

“A commodity reserve currency is an idea that became popular in the Great Depression, but was kind of rediscovered when the problem was not collapsing demand, but rather the need for a way to get the money supply to grow.

That's what the original idea of the commodity reserve currency was.

But the reverse problem of excessive inflation – and so linking the dollar or whatever the unit of account is called to a basket of commodities – would be a way of preventing excessive inflation.

Our friend Hayek from 30 years before denationalization of money saw some merits in this kind of proposal.

It had the benefits of a gold standard in taking the regulation of the quantity of money out of the hands of a committee of central bankers.

It is, in a sense, putting it into the market because anybody could bring commodities to the warehouse and get money. Anybody could bring money to the warehouse and get commodities.

But the proposals in the 30s and 40s were for physical warehouses filled with physical commodities.”

“We don’t need to do that today. We could accomplish pretty much the same thing with a portfolio of tokenized commodities.”

5

14

67

12,887

Jun 11

“It is only because the control of the means of production is divided among many people acting independently that nobody has complete power over us, that we as individuals can decide what to do with ourselves.”

• Friedrich von Hayek

10

205

Jun 9

Reserve does not know which DTF will win.

But haystacks are cool.

🗣️ Nevin Freeman at Monetarium 2:

“Reserve is not actually that opinionated about exactly what any particular diversified portfolio should be.

The Reserve Protocol, as many of you know, but some of you may not, is a platform. It’s a piece of technology that allows anybody to create a decentralized token folio.

And by building a platform, we think that we can bring many, many, many more such products into the world than if we just tried to launch them individually ourselves.”

“An 80-year progression of how the world has held equities. […] clearly [shows] we went from holding assets individually to, over the course of those years, holding more and more assets in bundles.

If you think that the forces that apply to ordinary assets will apply to tokenized assets – and I don’t see why they wouldn’t – then over the long course of time, we think that the same progression is likely to happen. People are going to hold more and more assets in bundles.

How exactly are they going to do it? Which technology are they going to do it with? Well, we’re not sure yet, but that’s what we’re building for.

And so we think that this wave, it’s a slow-moving wave, but it’s very big and powerful.

We think that this is going to repeat itself. We think that that's going to happen in the case of DTFs as well.”

“So, if that's right, then before we get to the point of topping CoinMarketCap, you would see something like getting to a billion-plus in some sort of S&P 500 of crypto-type DTF.

It’s kind of the most boring DTF you could imagine, just a broad crypto market index. And I think that is a reasonable bet for what could get large first, just based on this basic force.”

7

39

1,065

Jun 2

Most currency collapses in history follow a predictable four-step cycle:

Debt • Monetization • Inflation • Loss of faith.

Only the timeline changes.

And for the world’s reserve currency, the runway is always longer…

🗣️ Mark Dinner at Monetarium 2:

“Germany suffered hyperinflation during the Weimar Republic of the 1920s.

France also went through hyperinflation in the 1920s following World War I.

Japan suffered the same fate as they successfully initially operated quantitative easing in the 30s, then as they became more aggressive doing that with their war efforts in the late 30s and abused the printing press, they had a hyperinflation as well.

If managed poorly, the US faces a more accelerated and persistent decline in the dollar that could produce an inflationary spiral in the last decade.

By the way, that occurred with the UK in the 1970s, but not to the degree of the Weimar Republic; it’s a pretty classic way for how currency regime shifts occur.”

“Typically, inflation spirals occur when the government has too much debt in a currency it can’t print, big budget deficits, which it funds by abusing the printing press and monetizing government deficits and debts. Both internal and external geopolitical conflict and wars often undermine the incumbent superpower and its currency as a global reserve.

The US is at risk across these factors, save for the fact that the US government debts - this is important - are in a country that the Fed can print, and the currency is the world’s reserve currency.

This is what makes the current case both fascinating, and it's why the reserve currency shift of the US is intertwined with its position as a global superpower.

Another scenario is basically more of the same and perhaps a more glacial shift.

While the US has debt to GDP of 120 percent and the largest budget deficit outside of a recession since World War II, the dynamics that produce a regime shift are playing out, and it’s a fair point that these dynamics are quite slow.

Sophisticated investors have been discussing a regime shift in the currency for decades. […]”

“The way the current administration is forcing the issues across both internal and external imbalances and conflicts.

For example, through tariffs, which amount to a trade war;

or clauses like 899 in the current bill that threaten taxes on the income on foreign asset holders, which threatens a de facto debt default on US assets;

or a stated preference for a weaker dollar and an easier Fed;

or expanding the budget deficit while looking to cut longer-term spending, and slash regulations to produce a growth miracle.

All of these policies are being shifted so fast it feels like we’re operating at policy warp speed. […]

The tectonic plates underlying the system are now moving faster than we may even fully appreciate.

The path of US debt and faith in the dollar system are set to be tested in a big way in the coming 12, 24, 36 months.” [from June 2025]

2

2

14

420

May 28

“I believe that the reason people typically miss the big moments of evolution coming at them in life is that we each experience only tiny pieces of what’s happening.

We are like ants preoccupied with our jobs of carrying crumbs in our short lifetimes instead of having a broader perspective of the big-picture patterns and cycles, the important interrelated things driving them, and where we are within the cycles and what’s likely to transpire.”

• Ray Dalio

2

17

404

May 26

Trading Apple stock against Bitcoin on the same platform, under the same license.

Chairman Paul Atkins wants to make it possible.

🗣️ Michael Selig, Chief Counsel of the SEC Crypto Task Force, at Monetarium 2:

“Many folks within the markets want to offer something of a super-app, where you can trade Apple stock against Bitcoin, or Tesla against Ether. Trade securities versus non-securities, whether they’re crypto assets or not.

And so we want to be able to provide that type of in-kind platform where people can trade and innovate with financial technologies.

People might also want to offer lending and other types of services all under one roof - under a single broker-dealer license, for example - and [avoid] the red tape of going out and getting different state licenses, a commodity broker license, et cetera.

We’re working expeditiously to try to provide clarity around what can be done through a broker-dealer or a national securities exchange.”

“We want to do things with public notice-and-comment.

We want each commissioner to have their vote on things and be able to be heard, have their concerns weighed by the others. And that dynamic's a good one to get to the right policy.

So rulemaking’s ultimately the goal. (…)

But in the interim, there’s a lot of damage that was done by the prior administration. So staking's a good example. Many staking-as-a-service providers were sued by the prior administration.

There are many that want to come to market with new products quickly.

There are many that aren’t sure if their existing model is now allowed under the securities laws.

And so the staff has taken it upon themselves to issue some of these staff statements that are not notice-and-comment, public process rulemakings.

But the staff has authority to issue its own views on certain matters.

Another area where the staff is open to considering a request is no-action letters. Folks can come in, meet with the staff, submit a request for no-action relief on a matter that maybe the securities laws or regulations today are incompatible with; or [where] it's not clear whether the enforcement division - that sued many crypto participants in the prior administration - would bring a lawsuit again.”

“We should have the minimum amount of disclosure as necessary.

You shouldn’t be imposing additional burdens where it’s not needed.

So we're certainly taking a hard look in line with the president's directive to make sure that all of our regulations are what's necessary, no more than what's necessary.

I think that's really the idea. (…)

The goal is definitely not to add new regulatory requirements.

And that’s why, in particular around crypto, we are very cognizant around making sure that there’s not duplicative regulation.

We want purpose-fit rules that allow people to operate their business, we get the information we need to regulate them, and we can have regulations that are going to protect investors.

That’s our mission, of course. But nothing more than that.”

1

12

489

May 21

“Central banks and governments are not paying enough attention to how tokenization will change the plumbing of financial world, and will change it swiftly.”

• Larry Fink

1

2

24

613

May 19

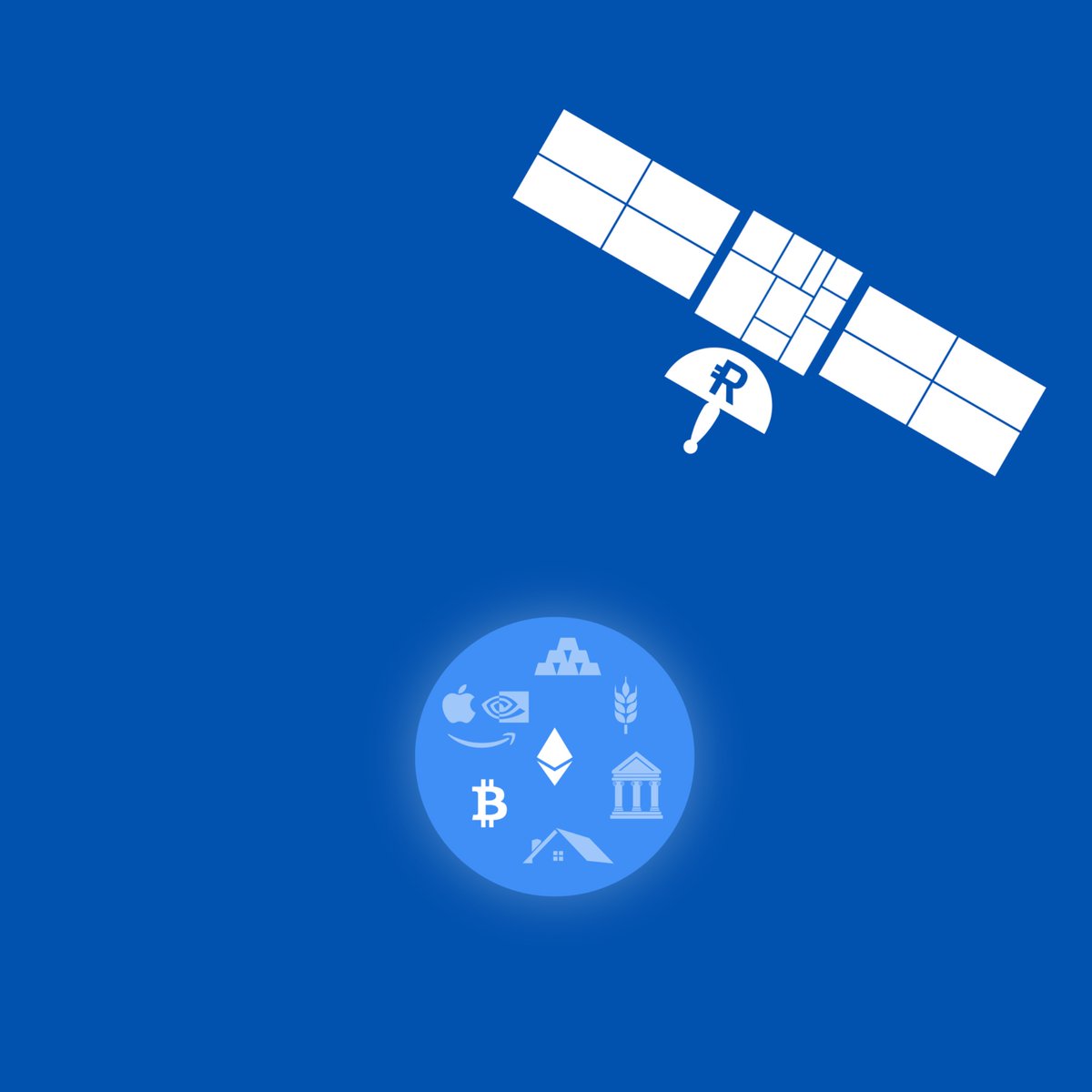

Today Reserve powers baskets of crypto assets.

But as real-world assets get tokenized at scale, what can go into a basket becomes effectively unlimited.

🗣️ Nevin Freeman, co-founder @reserveprotocol, at Monetarium 2:

“Reserve’s technology is used in crypto, in DeFi, to make baskets of different crypto assets. And we do think that is an excellent first use case.

We think that’s what any DTF company should be focused on right now.

But as all of the world’s assets end up tokenized, the universe just gets that much bigger. (…)

This gets even much more exciting than it is today.”

“If you just have these as products that exist on the blockchain with no easy way to use them or spend them as money, then adoption becomes that much harder.

This is part of the original thinking many years ago that led us to decide there should be an arm of the project that builds a convenient user platform to make it possible, to spend this stuff on a card, to make it really easy to handle these assets without having to be a DeFi-native person. (…)

Offering USD stablecoins and diversified stores of value to consumers around the world via our technology platforms (…) is kind of equivalent to delivering satellites into orbit and offering satellite internet around the world.

It's a practical step along the way to our insanely big mission, and it can be profitable and valuable to humanity as we build.”

“With the Digital Securities Initiative, I think you can now see how these pieces come together, where if it is made possible to get all financial assets onchain, to do it in a way that is internationally compatible. (…)

If we can make it as easy to create a fintech app that allows handling of tokenized securities as it is to create a fintech app that allows handling of dollars or ordinary crypto, then that makes it so DTFs that contain securities - and are themselves securities - could be used in many, many different convenient financial applications around the world.”

1

7

37

891

May 14

Imagine clear rules for tokenized assets & the unlocking of institutional participation, among other things… 👀

2

3

22

889

May 12

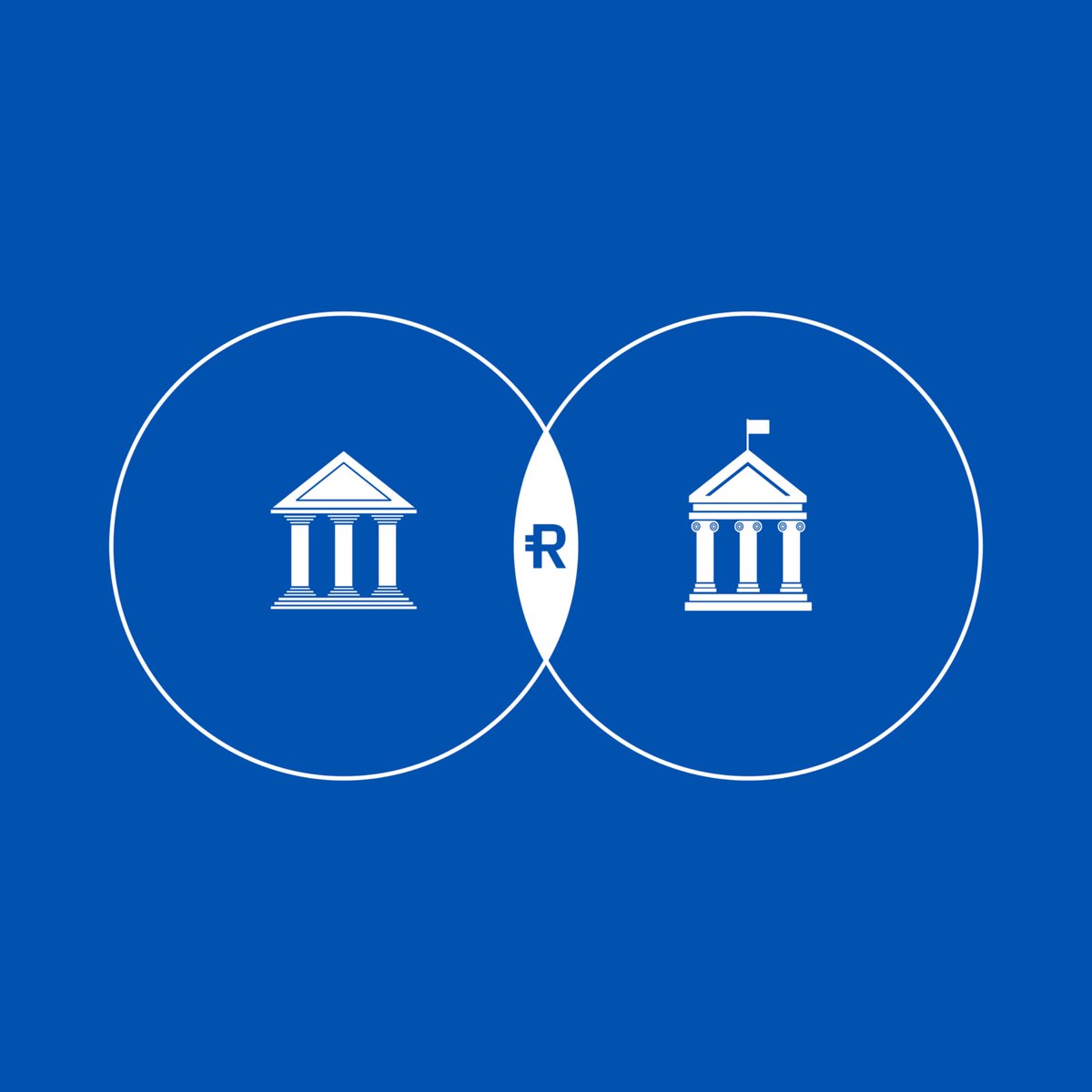

An ex-Fed senior trader described Reserve as something that neither commercial banks nor central banks can do alone:

“What I really like about the Reserve Protocol is that it kind of combines the aspects of both banking and central banking.

You can issue money against assets, like a commercial bank. But unlike a commercial bank, it’s not redeemable for higher forms of money. So there’s no run like you could have in a traditional bank system.”

🗣️ Joseph Wang at Monetarium 1:

“The way that commercial banks handle asset volatility is that they just kind of don’t let you see what happens. Some assets don’t have to be marked to market. And of course, there’s only periodic disclosures. So in a sense, you are asked to close your eyes and just trust the banks. But then I guess if you have a protocol, that could be managed better.”

“One thing that the commercial banks do well that I think would be worth thinking about going forward is the allocation of money.

Reserve has a really good way of issuing asset-backed money. And that’s super important. But at the end of the day, it’s also about how money is allocated.

What if someone doesn’t have assets and they would like to have money? Well, you can go to a commercial bank and they can create that money for you - such that people who don’t have assets can still be able to invest, go to school, get a loan, and so forth.

Basically, the bank makes a judgment as to whether or not the borrower is worthy of having money, whether or not they repay the loan, whether or not the project is worthwhile.

So being able to create money is one thing.

I think that to be able to have a successful monetary system, it's also important to be able to have it allocated in a way. And that could still be done, I suppose, by lending - issuing tokens and then lending them.

But then when you do that, you are also reintroducing many of the conventional risks that we see in the banking system like credit and liquidity.”

“I would emphasize that being able to create money is super important. But having it allocated well is what makes money effective in creating an economy that has good growth but also more equality. It's really hard to know whether or not money will be allocated well.

Are you going to be giving it to someone who is going to spend it wisely? So it's a lot of work for the commercial banks to do a very qualitative judgment to say, is this person credit worthy? Is this project viable?

If you have a monetary system, in addition to having the base layer there, having an idea of how it could be better distributed to be able to benefit everyone, even people who don't have assets to get tokens, I think is really important for its adoption.”

3

8

46

3,035

May 5

Every dollar in your bank account is already backed by assets.

You just don’t get to choose which ones, or see when they lose value.

🗣️ Joseph Wang at Monetarium 1:

“All fiat is basically asset-backed.

When we go and make a loan, for example, that loan backs the deposits that it creates. (…)

If you go and get a mortgage, the deposits created are backed by real estate.

If you go and get a credit card loan, it’s really backed by nothing more than your promise to repay.

But that loan - an unsecured loan - at the end of the day [it] is still an asset. That backs those deposits. The assets backing that vary in value over time.”

“New York Community Bank is a very old, respectable organization who's been around for over 150 years.

Now, they actually invested fairly responsibly, a lot of it in rent-controlled multifamily homes in New York City, and over the past decades has done really well.

So it's not like they were engaged in wild speculation, but they did have a very concentrated portfolio in multifamily loans…

When New York City passed a law that made rent-controlled apartments less valuable by limiting how much you can raise rent, well, that really had a big impact on the value of their assets.

It’s their shareholders that have to pay that price, and it was quite a steep price.”

“Where do bank deposits come from? They are actually created out of thin air by a commercial bank. (…)

If you get a loan from J.P. Morgan, it’s basically like a J.P. Morgan coin.

Contrary to what people think, banks take in someone's deposits and lend them out.”

“A balance sheet [for commercial banks] is basically just a graph of what a bank owns and what it owes.

Its assets are what it owns. Its liabilities are what it owes.

So before a commercial bank creates a loan, you can see [its assets, like reserves and currency, and its liabilities, which are the deposits.]

Then if I were to go to a commercial bank and ask for a loan of $1 million, what the commercial bank does is it really just goes into its database and it types in ‘$1 million due to Joseph’. It's created out of thin air. It's merely a database management question.

We call this expanding their balance sheet. And that is really where bank deposits come from.

Now, this ability to create money is really an awesome power.”

1

2

13

702

Apr 28

In 1980, economist Robert Hall thought he had found the holy grail of inflation hedges: a basket of ammonium nitrate, copper, aluminum, and plywood.

Looking back, it had performed almost perfectly. Then reality came knocking…

🗣️ Lawrence H. White at Monetarium 2:

“It’s important to have a broad basket of commodities and not to pick the basket and the weights on the items in the basket by looking backwards, and doing a grid search for what best matched the CPI.

I say that because an economist named Robert Hall said, look, it would be an almost perfect inflation hedge if you had held over the last 20 years a basket consisting of ammonium nitrate, copper, aluminum, and plywood.”

“How did he pick those four commodities? He had to go back and do a grid search and see what combination of commodities just happened to go up and down with the CPI.

So I had a grad student say, ‘look into how it did after Hall published his article? How did the ANCAP bundle do versus the CPI?’

It was all over the map. It was way up, it was way down. He had picked it.”

“You can always pick a winning stock portfolio in retrospect. This is kind of the same problem.”

“But even if you pick a broad index of commodities – a hypothetical 22 commodity unit of account bundle – even that didn’t maintain its value so well in terms of the Consumer Price Index.

So it’s going to take some research to find a robust set of commodities if you want to match the performance of the CPI.”

1

3

19

2,361

Apr 23

“I skate to where the puck is going to be, not where it has been.”

• Wayne Gretzky

“I do believe we’re just at the beginning of the tokenization of all assets, from real estate to equities, the bonds across the board.”

• Larry Fink

1

1

15

758