Joined July 2014

- Tweets 1,462

- Following 1,180

- Followers 5,414

- Likes 14,935

28 Photos and videos

Pinned Tweet

21 Nov 2025

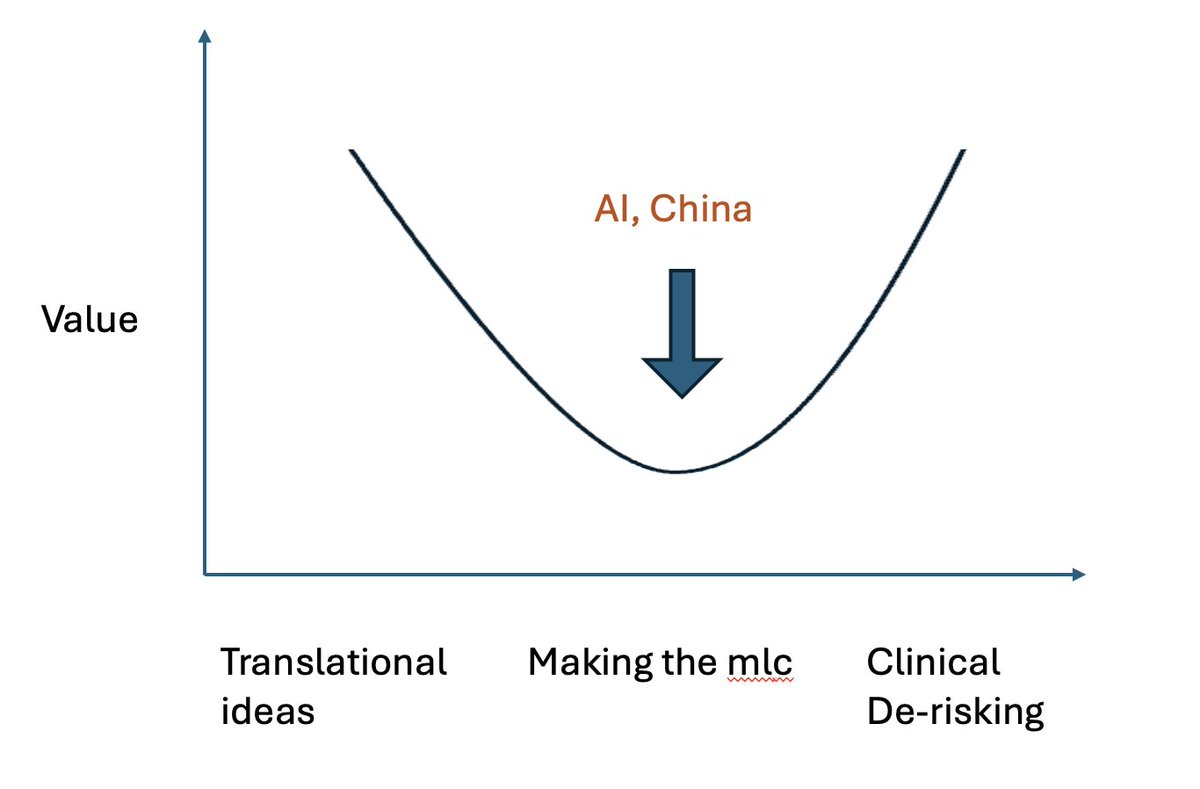

Recent advancements in one-shot AI protein / antibody development by Chai, Nabla, AI Proteins, Generate, and a few others are accelerating the *main* theme in biotech:

Value of building the molecule is going down. The value of novel targets, novel translational ideas, AND also the value of clinical execution is going UP

Here's where the value graph is moving towards:

The twin forces of AI and China are quickly driving down price of mlc dev across many modalities:

For AI - mainly Ab right now, emerging for genetic medicines, small mlc, ADCs, cell therapy;

For China - Abs, cell and gene therapy, small mlc, and soon genetic medicines

Having a "best in class" mlc is no longer enough - many tech platforms will soon offer you a mlc priced on metered compute (getting cheaper) and China CROs / biotechs will continue to eat the world with (over)capacity (continued involution).

To make a valuable drug, you must differentiate on either:

a) Novel translational ideas.

Novel targets, novel mechanisms, but not just that - connecting targets with diseases; novel application of certain targets in new disease settings, new intuition on which patient pops have widest therapeutic index for a drug, etc

OR

b) Clinical execution.

Determining the appropriate endpoints in a trial. Recruiting the right patients. Appropriate relationships with the right PIs / clinical sites. Ability to finance registrational studies in US markets ($10s to 100s of Ms)

Either be a translational target discovery engine / tech platform that unlocks new modalities (which unlocks new translational hypotheses) OR get a team of grizzled clin dev / CMO vets and go raise $X00M to validate a clinical hypothesis

Living in the middle (ie being "full stack") is dangerous work (at least for a startup)

24 Jul 2025

**A grand unified theory on what will happen in biotech in the next 10-20 years**

the two major forces reshaping industrial biotech in the next decade are:

1. China

2. AI

- and they're critically linked

how?

China's low R&D cost basis democratizes execution by providing infrastructure to more drug developers (similar to how AWS helped cloud apps explode in 2010s)

AI makes scientific information much more freely available; agents & lab automation increase R&D productivity as well as throughput, further deflating development costs

What happens when many more translational ideas can be tried much more cheaply?

Value starts accruing in the best ideas to try ie the value shifts earlier in the value chain

if the cost of everything from preclinical R&D to clinical trials are dropping significantly due to combo of AI and China, the disparity between clinical stage vs early pipeline assets shrinks dramatically from the current order of magnitude difference

The premium on true creativity, novel scientific insight, fundamentally new biology will 100x

In a few years the top-of-industry drug hunters / translational biologists will command a hefty premium (maybe not $100m a year like current top AI scientists but ... maybe??)

Even more provocatively, foundational models in translational biology that surface / accelerate novel biological hypotheses will suddenly capture outsized value

When will a translational foundational model be worth more than a top 10 pharma co?

sounds crazy... but like everything else --> slowly, then all at once

10

22

174

39,278

May 31

There is a fundamental flaw with the argument: “U.S. is 70% of global profits in tx and therefore can dictate which therapies are allowed in the U.S., including excluding China assets".

The weight bearing assumption is that China’s biotech industry will not be able to sustain itself without US market.

This does not conform with reality.

Prior to 2022, Chinese biotech industry had minimal capital inflows from outlicensing / newco’s to US / Western pharma AND a very austere tx pricing environment domestically. Yet significant companies grew to dominate the domestic market, and many Chinese biotechs managed to move up the innovation curve.

Do you think that Chinese biotechs sprang up overnight in Dec 2022 when this out licensing wave started? Akeso, Keymed, Hengrui, Hansoh, Innovent, and so many others have been around for years - pretty much all of them starting off by making drugs for the domestic China market. US out licensing deals were few and far in between, and yet many of them became $ B or $10’s Bn companies in the process.

Furthermore, in recent months the Chinese payor market is now getting better at rewarding true innovation. 2025 NRDL reform introduced a higher pricing tier for true innovation (not me-betters). Domestic economics for first-in-class assets are getting meaningfully stronger, regardless of the exit to Western pharma path.

From a unit economics perspective, "removing the exit to the West will kill Chinese biotech progress" argument just isn’t supported by facts on the ground.

Another serious drawback to the banning argument is that presumes Chinese drugs are only me betters or me toos that are knock offs of western efforts (and will continue to be). Otherwise, the interpretation is that US patients would be ok not having access to the latest and greatest drugs.

This, too, does not conform with reality.

Chinese biotechs are now making net new innovative drugs across ADCs, in vivo CARs, genetic medicines and many more modalities, going after novel targets, payloads, and incorporating delivery tech that we have not seen here in the west; and if they work clinically - US patients will want access to as they will improve the clinical treatment paradigm.

I have spoken to the Chinese biotech CEOs and seen these programs. Some will work and some won’t (that’s just drug discovery), but they are coming, and there is no use in arguing about it.

Do you think it will be acceptable that US patients will not have access to best in class / first in class drugs?

so to summarize: in the US, we have an industry that is *losing* pricing power (no matter if R or Ds are in power, tx pricing pressure is on the docket), trying to keep drugs being made from a country with *increasing* pricing power (based on government support) out, at a time when those drugs are increasingly innovative.

Who do you think the actual loser from this is going to be?

US patients.

all this to say: the back and forth arguing is a moot point, the innovation is coming **whether we like it or not**.

I’d suggest we in the US get busy competing, investing in innovative science, deregulating trials, and doing less belly aching.

Patients, American and otherwise, are waiting.

9

3

34

7,045

David Li retweeted

May 22

moolenaar's proposal would likely have the opposite of the intended effect. if u ban US pharma from acquiring chinese IP, what is likely to happen is EU/Japanese pharma will get that IP, and u hand them a structural advantage. if u somehow convince them to also ban china deals, then u force chinese biotech to forward integrate and compete directly sooner. hengrui and at least 10 other biotechs already have the resources to do so. then let's say u ban those companies from the US market, then u just have a replay of the EV story, chinese pharma will just take over the rest of the world.

the proposal also tries to scare people by drawing the analogy to chips and rare earths. there is no such analogy. licensing deals are for IP, and almost always include the right to manufacture wherever you want. so there is no supply chain risk. in fact, in drug world, the vast majority of the value of drug IP accrues to whoever develops and commercializes a drug, not who invented it. so right now western pharma is the winner from this relationship.

so if the Q is well how do we not lose to china longterm? the answer is we must compete. america is great, we should lean into our natural advantages. continue to lead in breakthru science, maintain fda's position as the preeminent regulator, apply our cutting edge technology, and entice the world's best with the most pro-innovation commercial market. these leads are larger than many realize. we should mitigate our weaknesses, most importantly the bureaucracy that comes from being around longer than others that slows us down.

May 22

Could we be nearing the end of the China biotech deal wave? At least one prominent GOP lawmaker is pushing for the government to restrict them.

endpoints.news/gop-lawmaker-…

6

5

45

14,132

May 5

Notes from China visit, Apr - May spring 2026, year of the Fire Horse

Met 20 companies, 5 local VCs & crossover funds, 5 local PIs, and many entrepreneurs in Shanghai and Beijing

===========================

** Local China biotech mood shifts away from newco formation - although IMO that deal structure will still survive; the new slogan: "don’t sell your babies” - ie push assets further independently so that they can capture the larger value inflection post FIH data / early clinical de risking.

The challenge here is that there is still a gap on the type of data, clinical dev strategy that local Chinese biotech / pharma is producing and what is necessary to secure a significant M&A price from global pharma. Arguably a newco in the right hands significantly changes the probability of a success exit for that asset in Western capital / M&A markets. The most discerning Chinese entrepreneurs understand this, and the recent exits by Candid, Oura, Kailera, and others demonstrate the path to $B value creation

** Simultaneously, there is a push for established Chinese pharma to enter into earlier R&D collaboration with western large pharma. Western pharma wants to access R&D efficiencies and provide targets. Chinese pharma executes against these targets to produce assets and secures significant upfront payments while only locking themselves out of areas they do not consider strategically core. Particularly relevant to this theme is the Innovent / Lily deal.

I suspect this trend will move from local Chinese pharma to local biotechs as well, as the quality and speed there can also be high.

** Another prominent slogan amongst China biopharma recently is to “Go global”. This is particularly relevant for China pharma like Hengrui, BeOne, Innovent, etc. See Innovent / Takeda ADC deal where Innovent will co-commercialize US market.

The push for Chinese pharma to start to eye global markets is clear, however IMO these Chinese pharma will fundamentally remain Chinese in decision making and locus of control given their current governance structure. We are still (many?) years from a China pharma turning into a Takeda-like set up where regional pharma has turned into a true global organization

** Turning to the US biotech / pharma side of things - there were obvious signs American Biotech is waking up to the opportunity to work with Chinese R&D ecosystem. Primarily right now through the IIT path (see below) however also starting to explore working with Chinese biotechs beyond just using CROs.

A few US VCs are fully exploring this path e.g. MPM with their K2 Therapeutics platform and RA building a China R&D platform for their internal portfolio, but vast majority of US / western VCs have not figured out a way to unlock the opportunity yet. Doing business in China is not the same as hiring CROs in the style of Western R&D ecosystems

** China’s IIT pathway comes of age. With Decree 818 having come into effect May 1, IIT path becomes more regulated and closer to the requirements of Chinese FDA IND path. This has been a progression away from complete “wild Wild West” of the IIT path in the early days ie prior to 2020, to gradual opening of the path to foreign firms (beginning in 2023/4), to now a significantly more standardized path.

However, there are still significant advantages to the IIT path and spoke with 10 US biotechs looking to leverage this path to get FIH data. Suspect this movement actually grows significantly with Decree 818 in place as it standardizes things / removing grey area risk, and as it is still a fraction of time and cost to do it in US.

Perhaps even more important than speed is the flexibility as you can figure out dosing, patient cohorts, even run different constructs H2H that would not be possible in a US IND trial but is immensely valuable in figuring out clinical dev strategy of a mlc in FIH data

Meanwhile China IND timelines continue to shorten and can be filed at 3 mo max (and 1 mo min); very similar to US IND timelines now, so the two paths (IIT vs China IND) have converged.

** Finally, following the boom of in vivo CAR-T players last year, there are still many players in the space but many fewer that actually have differentiated / proprietary delivery platforms. A significant amount of clinical data will be coming this year, but getting feeling in vivo technologies whether LNP or LVV based will quickly become commoditized (big M&A numbers from large pharma notwithstanding). Simply too many firms that will push clinical data in coming months

===========================

The drum beat of progress and evolution in China biopharma is unrelenting.

For American biotech, I continue to believe that harnessing China ecosystem efficiencies (in both preclinical and clinical) is the path forward to retain global competitiveness.

More to come on this soon.

4

12

91

13,294

Apr 19

traditional biotech VCs are dramatically underweighting the structural threat AI poses to their business model

recently spoke w a US institutional LP - even top tier biotech VC return profiles are not competitive with what AI funds are now producing

when an LP can put capital into an AI fund returning 5-10x net and the biotech fund is grinding out 2-3x on a good vintage, who do you think is going to get the capital?

case in point: the largest bio venture fund raised in last 2 years has been Sofinnova at $1.2b and Frazier at $1.3b; today Sequioa raised a $7bn AI focused opportunities fund; Thrive raised a $10bn fund a few months ago largely focused on AI

most biotech GPs I talk to are treating AI as "yet another wave" in technology and most are pessimistic about near term AI impact in drug discovery;

yes - better binder design is not remotely close to developing clinically impactful drugs; however, I'd encourage these GPs to look more broadly - the competition is no longer SaaS startups getting to $100M in ARR in 8 years; AI native startups are getting there in 8 quarters

"but don't LPs want diversification?" — where was this argument when PE/VC 5x'd their allocation against other asset classes over the last 25 years? same thing is happening now, except with AI. intra asset class diversification is a misnomer. the real diversification is VC vs other asset classes, not biotech VC vs AI VC

a lot of biotech VCs raised funds in 2021 and 2022 when times were good. many of those GPs will need to go back out in 26, 27, 28.

it's going to be a rude awakening when that AI wave they expected to crest has not, and if AI IPOs ie OpenAI, Anthropic, actually IPO - watch out - LPs will be asking why this capital shouldn't just go into the asset class that are printing

7

3

80

12,600

Apr 18

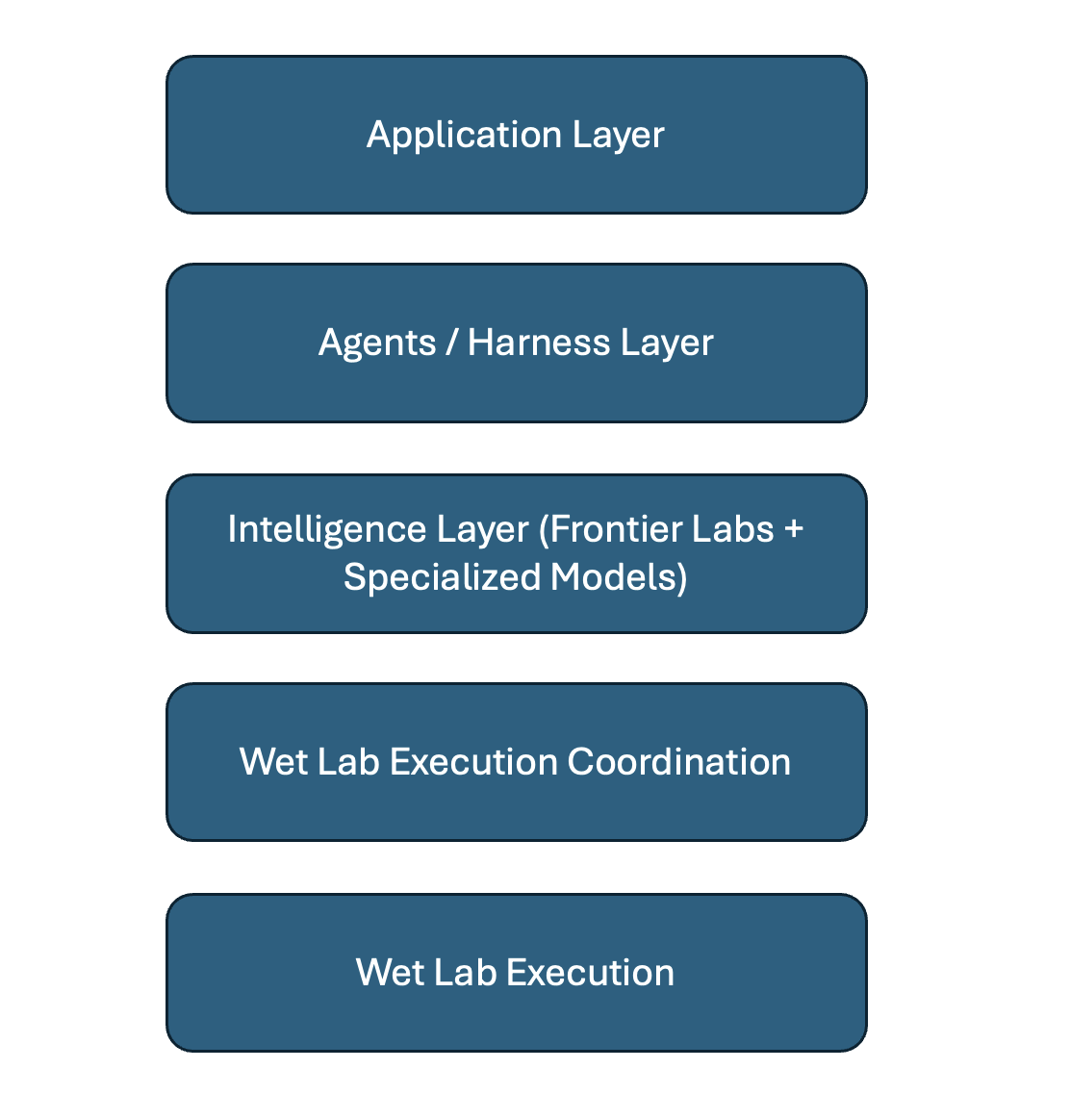

**the emerging AI native life science R&D stack**

the key question from mid 2025 til recently was whether frontier labs were actually serious about building products, capabilities, and orgs in AI x drug discovery or they were using it for marketing purposes in pursuit of ever larger rounds of funding.

fair q when in a few week stretch in 2025, sam altman, demis,and dario all said that one of the biggest benefits of AI for humanity would be huge acceleration of tx development ("dozens of drugs in a decade!") - cue exasperated groans from the trad bio section of the peanut gallery

a few cards have flipped in last few weeks:

OAI: released GPT-rosalind, a life science research model, first vertical specific GPT

Anthropic: acquired Coefficient bio to build biotech infra and a rumored bio model also dropping soon

as the frontier labs' strategy in the space has become clearer, so too has the *AI-native life science R&D stack*

a few comments on each layer of this 5 layer cake, starting with the middle:

Intelligence Layer (Frontier Specialized Models) ~ Ant, OAI, GDP all in running; will proprietary data end up being *the* differentiator? and if so, who actually has access?

Wet Lab Coordination ~ speaking of proprietary data, can't get it at scale without some interface layer to the actual wet lab execution apparatus. in life sciences, that workflow is super outdated, phone calls, Excel, fax , PDFs, all just archaic. nearly no one has an API.

are the frontier labs interested in tackling the long tail of assays and CROs that would need to be wired into a real wet lab coordination layer? nothing to suggest they will right now — but they are hungry for capturing value up and down the chain

AWS Bio is first green shoots that another player will operate in this space but reviews on the ground have not been great - this may be the grittiest but also most unappreciated oppty in the stack

Wet Lab Execution ~ life sciences has a massive long tail of CROs, and given this is where the actual proprietary data gets generated, so this layer can be a genuinely differentiating factor

the interesting topic to watch: are any CROs going to become AI-native and start moving *up* the stack — doing wet lab coordination themselves, or perhaps even becoming preferred data providers to frontier labs?

Early movers like Gingko and Adaptyv are making some noise, but this has to be a topic that the forward-thinking folks running AI strategy at Thermo, Wuxi, and others are thinking about

Agents / Harness Layer ~ sitting on top of intelligence layer, lots of new startups have jumped into this space trying to coordinate models across life sciences specific workflows

big risk looming over all of them is whether frontier labs will simply subsume this into their own product roadmap. Anthropic x Coefficient Bio is an ominous signal (but maybe $ 400M acqui-hire in 12 mo is an outcome that everyone involved is ok with)

Application Layer ~ Benchling is the big gorilla here but if "attention is all you need" is *truly* all you need, the UX / UI with scientist layer becomes critically important, and potentially the most interesting place for a shake-up

frontier labs could still move in. and new form factors could emerge enabling new startups. physical AI could change the whole workflow

additionally is a notebook entry in a digital ELN even the right atomic unit of work in an AI-native workflow?

finally, stepping outside the stack, the looming question that no one has fully answered yet - these are all *infrastructure* plays. what will the truly AI-native therapeutics company actually look like? the actual value creation that comes out of this stack?

how will those AI-native biotechs look different in shape, value creation profile, and capital intensity compared to the biotechs we know today?

stay tuned.

10

17

168

45,398

Apr 1

Translation: Western pharma purchases of Chinese biotech assets will continue

Mar 31

@USTradeRep Greer interview worth a listen in full, esp. on China:

1. Strategic goal is a managed trade relationship where US and China agree on what we buy and sell each other and in which trade is predictable. (FWIW, I agree with Greer that a highly managed trading relationship is the best near/mid-term outcome for U.S.-China trade).

2. Under this approach, the U.S. will buy "low tech consumer goods," potentially some "commodities" that the U.S. doesn't have, etc. China will buy Boeings, medical devices, pharma, ag commodities. (I assume energy as well, though Greer did not mention it specifically).

3. Trade will be managed by a Board of Trade, the launch of which will be a Trump-Xi summit deliverable.

4. Greer cannot "pre-judge" whether the forthcoming Section 301 investigation will fully restore the 20% tariff rate on China that existed prior to the Feb. SCOTUS decision. (Legally, this is true, Greer can't pre-judge a 301 investigation outcome).

5. That said, both the U.S. and China are seeking "stability" and "continuity" and the U.S. wants to reduce the trade deficit and is committed to protecting its domestic economy.

6. Probably no more ministerial-level meetings prior to the Trump-Xi summit, with negotiations being handled by Deputies and staff. Greer said that he has not heard any discussion of pushing the summit back further beyond mid-May.

2

1

15

3,199

Mar 25

as an addendum to this, becoming more obvious that true venture style biotech investing is on the clock ...

in the soon-coming future, vast majority of biotech venture investing will be AI enabled / AI native biotech investing:

the only other flavor will be more PE style / cross over investing where clinical stage deals are being underwritten to 5x returns.

These deals will need more risk reduction profile and that's where China comes in. More biotechs will have validated their platform / biological thesis in China, Australia, Eastern Europe and "biotech venture" will actually be just taking relatively human biology de-risked assets through to clinical value inflection points that are legible to pharma M&A teams

what is left in the preclinical bucket will be AI enabled platforms that get to DC faster for specific modalities / solving specific pharmacological problems by training AI on large data sets

this theme is further reinforced by the fact that we have gone from ~3 to at least 12 modalities in the last~15 years, all of which needs to be "engineered" / optimized in order to become clinically meaningful drugs - a perfect set up for AI applications

Mar 25

given the early stage deal flow i'm seeing, being a tech bio VC that is not willing to go into tx investing is hard place to be

on the tech / infra side you are crowded out by generalist funds by deeper pockets and better brand - why would a founder of "digital life sciences" play getting great traction not take that capital at the early stage?

on the biotech tx side, there is real opportunity right now because traditional biotech VCs have pulled back (esp from early stage / preclinical investing), but most techbio VCs have become gun shy about taking "capital intensity risk" with therapeutic plays

this is actually the exact worst time to do that as AI and AI investing eats everything else that doesn't require deep physical execution moats

will be interesting to see who survives this culling

2

1

47

12,980

Mar 25

given the early stage deal flow i'm seeing, being a tech bio VC that is not willing to go into tx investing is hard place to be

on the tech / infra side you are crowded out by generalist funds by deeper pockets and better brand - why would a founder of "digital life sciences" play getting great traction not take that capital at the early stage?

on the biotech tx side, there is real opportunity right now because traditional biotech VCs have pulled back (esp from early stage / preclinical investing), but most techbio VCs have become gun shy about taking "capital intensity risk" with therapeutic plays

this is actually the exact worst time to do that as AI and AI investing eats everything else that doesn't require deep physical execution moats

will be interesting to see who survives this culling

6

2

63

13,909

Mar 20

earendil labs $787M financing is eye catching for sure

but the AI x China biotech theme is only getting started

have spoken with a number of chinese biotechs (many which the west has not heard of) that are beginning to develop proprietary models. Including RNA therapies, cell therapies, degraders, small mlc's

in a world where time and $ to FIH signal is king, combining AI's ability to cut time to DC and Chinese early clinical execution is going to be hard to beat

4

3

40

5,261

Mar 6

this is coming for drug discovery R&D workflows ... and I can't wait

2

4

47

6,864

Mar 4

the one unequivocal advantage that US biotech has over China biotech is proximity to clinical practice in the largest, deepest payor market in the world

we know exactly what the treatment paradigm is. we know what the patients with most unmet need actually need. we know what the delta is between being successful in a 2nd or 3rd line therapy in every signfiicant market. in short, we know the clinical target product profile and the exact patient population that needs it

the path to domination in the biopharma world still runs through the clinic (as always). we need to double down on this advantage

5

4

48

10,959

Mar 3

until AI x life sciences models can run agent generated hypotheses in the physical world with empirical real world feedback, there will be no meaningful value creation (or value capture)

it will continue to be a nice toy in industrial workflows

12

7

127

9,305

Mar 2

the first in class, first in human data coming out of China in novel modalities (esp in vivo CAR-T, RNA therapies, gene therapies) in the coming 18 months will shock the world.

15

26

175

18,172

Feb 28

the only viable US biotechs going fwd are:

i) novel platform tech (better way to find target, have better selectivity, or super power efficacy in a particular modality)

OR

ii) clinical team that can "king-make" a best in class mlc from China or an AI shop (ie uniquely experienced team for a particular disease indication that has specific expertise for shepherding programs through difficult to execute indications eg rare disease, respiratory, etc)

every co in the middle (potential best in class mlc w/o differentiated clinical team, me-better approaches, and even novel targets without unique clinical strategy) is on the clock

24

20

231

40,865

Feb 23

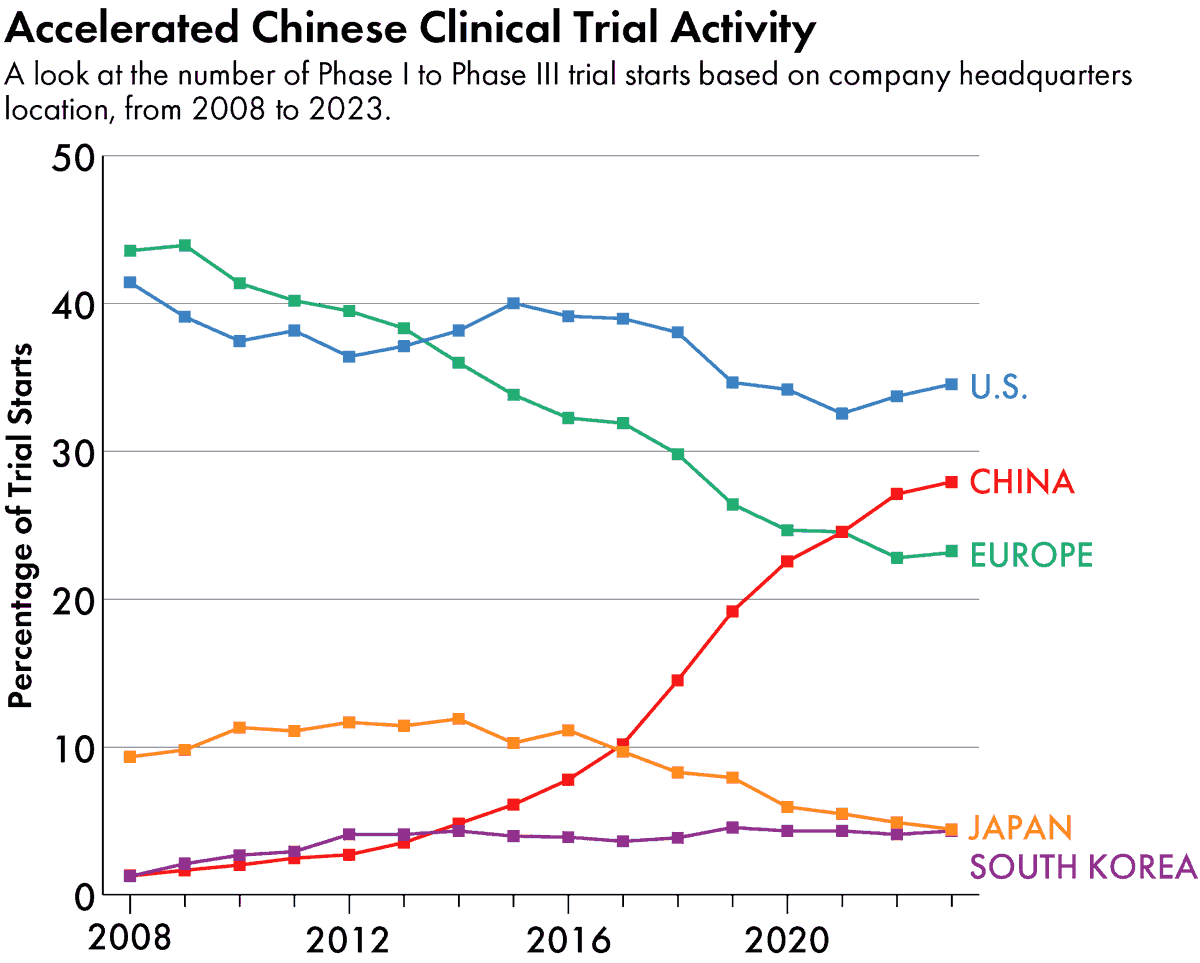

Chinese biotech is steadily climbing the innovation curve

Lots of evidence for this theme in recent weeks. at JPM in Jan, a full blown FIC targets symposium for chinese biotechs. last week, suzhou genhouse outlicenses novel target mat2a synthetic lethal ph1 ready small molecule to Gilead for $80M upfront.

Last year, I wrote about the need for American biotech to lean into novel biology. How to respond if Chinese biotech is also moving into novel targets?

For one, have seen American biotech still has advantage in developing *novel technology platforms* (for the time being). Am actively working with next gen cell therapy armoring technology, target logic gates for CAR signaling, etc that are all cutting edge platform technology companies.

The challenge with these technologies is that they still need to reach value inflection point quickly (generally FIH clinical POC). Given the tx fundraising landscape, human data is still king, and it's far cheaper / faster to get that signal in China market

this circles a ground truth that is market reality - even if not everyone recognizes it: American biotech needs to use every tool at disposal to remain competitive

1

4

50

6,519

Feb 22

sitting downstream of the frontier labs on the value chain is a dangerous place to be imo (even in the life sciences)

specialized verticals would seem to be more insulated, but look at how many connections anthropic is making into downstream specialized knowledge applications in life sciences (quoted list below)

as we've seen in codex, claude code, claude code security, and more - frontier labs are hungry to make your vertical platform a feature on theirs

from a frontier lab perspective, the economics are driving here - as open source LLMs are commoditizing the knowledge api layer, application layer is naturally where you have to go to capture value and justify valuation

this becomes a race of how fast downstream players can build distribution vs how fast life science teams at anthropic, openai, deepmind etc can build features / connections

and since life sciences (and healthcare) is generally a b2b sell (industry R&D researchers don't do IP related work outside of work digital environment), virality is (generally speaking) out of the question

good luck to all in the arena 🙏

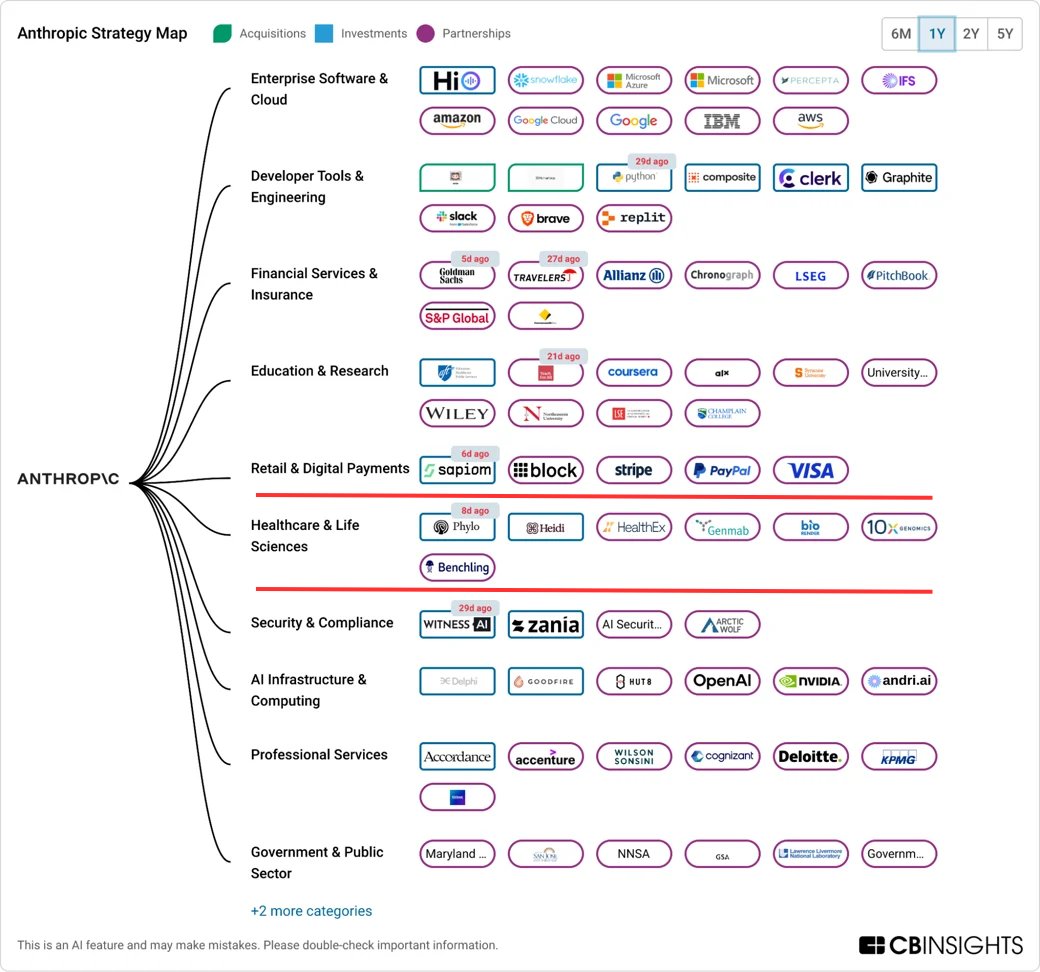

Anthropic’s healthcare & life sciences strategy map

1. Investments

• Phylo – AI-native biotech platform

• Heidi – AI ambient scribe

2. Partnerships

• HealthEx – Health data exchange

• Genmab – Antibody therapeutics & R&D

• BioRender – Scientific visualization

• 10x Genomics – Single-cell biology

• Benchling – Biotech R&D cloud infra

• Allen Institute – Biomedical research

• HHMI – Life science research

8

15

159

33,852

Feb 8

**We are approaching the takeoff runway for R&D lab automation - a (sober) look at where we are and where we’re going**

A few facts to set the scene. December 2025 OpenAI announces results of collaboration with Red Queen Bio, using chatGPT to optimize a genetic engineering process, Gibson Assembly, in a lab in the loop process. Importantly, in this set up, experiments completed by humans were still better than the automated robotics version. But still - showed proof of principle for models designing better scientific processes, result: gibson assembly efficiency was increased by ~79x

February 2026, less than 2 months later, OpenAI announces results of collaboration with Ginkgo, where ChatGPT was hooked up to a (mostly) automated lab, and demonstrated the ability to lower cost of cell free protein production by 40% over 6 closed loop iterations

Pharma sees the wave and is not standing still either. Genentech (launched an internal lab automation effort), Lilly (announced a lab automation initiative with nvidia), and a number of others are allocating 8 figure budgets to automation efforts.

Does this mean automated / lab in loop R&D efforts are imminent and we’re about to get self-improving, recursive agents in science / biopharma broadly?

Not quite.

The design x make x test loop faces real hurdles on both the agent / software and hardware / lab automation sides.

On the agent performance side, based on feedback received from industry practitioners, protocol *selection* is getting close to a solved problem

The challenge lays in physical error troubleshooting & iterative biological reasoning on next step scientific inquiries - which are necessary for extended chain-of-experiment scientific programs that are (much) more extended than multi-parameter optimization problems.

The vast majority of industrial value lay in these types of scientific programs - although there are indeed MPO problems that are quite interesting and valuable (eg ab eng for biologics mfg scale up, directed evolution for enzymes in industrial and pharma applications)

On the lab automation side, only (small) swaths of scientific workflows and assays are currently fully automated. Most of the existing larger players in the space are best thought of as industrialized high throughput biology, and not “text to general protocol” - although shoutout to Medra for the work they’re doing here, think they’re pioneering the right path.

To be clear - big believer in this wave overall, but still tons of opportunity for folks out there to innovate

As others in AI have noted - clarity of vision should not be mistaken for distance

Self driving cars in 2006 could achieve 140 miles in one go. 20 years later and waymo is only now barely rolled out in a handful of markets

it is still early for automated lab-in-the-loop science - but at least we can see the takeoff tarmac

8

16

142

16,396

18 Nov 2025

in biotech down markets, what's impt in raising $ is:

(having) money >> (team) experience >> asset (differentiation) >> platform

reverse in boom times

plan accordingly

8

4

59

6,414

11 Nov 2025

lots of discourse on here recently on how to get FIH clinical data in US cheaper, faster, and more competitively with China

Chinese biotechs, on average across modalities, generate FIH data with ~ $10M USD in funding total (R&D work, clinical ops, mfg, and pt recruitment)

but how do they do this? and what can the US do?

well first for the US side on how to respond, there's been a few more "obvious" answers offered. Accelerate regulatory reviews on IND faster. Open up an IRB path directly with hospitals a la IITs in China.

another vector might be public-private partnerships in form of tax credits, discounted lab space, or targeted translational grants.

On the China side, I've seen folks answer to how they're able do it being some mix of: accelerated regulatory path (ie IRB), government policy, piggy backing on existing IP (ie fast followers only)

One thing I have not seen folks talk about, which to me is the most obvious, is - wait for it - the intense competition that breeds insane levels of hard work in China.

China's local biotech environment is dramatically more competitive than in the US. Here in the US every target has perhaps 2 or 3 competitors. In China every target has dozens.

Case in point: in vivo CAR-T which has recently become a hot area this year, there are maybe 5-10 reasonable competitors in the West.

In China, there are close to 200. ~10 companies will read out FIH data in immunology this year 2025, and a multiple of that number will do so in oncology (the earliest US companies are expected to read out FIH data is 2026).

This is bewildering to observers in the West. Why would any entrepreneur start a company with ostensibly the same technology, targets, mission, etc as so many others that are already out there?

Well Chinese entrepreneurs are not dumb. They do this because the last 40 years of development in China has shown them it is actually a winning strategy. A hard working, enterprising person in the last several decades in China that went into say, textiles at first, then low cost manufacturing, then solar photovoltaics, then EVs (and so on) on balance generally did indeed WIN when they jumped into the fray. The outcomes have worked out enough to incentivize this behavior.

Through a 40 year long battle royale in the business environment, Chinese entrepreneurs know the truth that the best CEOs here in the West know just as well - the only true moat for a company is consistent, relentless execution.

Back to biotech. Biotech is on the list of "strategic sectors" for China and was named again in the 2026-2030 national 5 year plan.

The Chinese biotechs are only going to keep coming - so how does US biotech work to increase the competitiveness of the industry?

Well, leaders in biotech in the West need to hear this: it's not just regulatory policy, government support, or IP leakage that's leading China to win in biotech.

The uncomfortable truth is it's past time for us in the West to get fit and get in shape.

This is going to sound trite, but leaders need to make hard decisions to prioritize appropriately, to focus ruthlessly on the key value drivers, to make shrewd decisions that extend runway. Leaders need to push *hard*.

Teams need to put in the hours to help make that push. Labs and offices in South SF and Boston should not be empty at 4pm on a Thursday. Or a Friday for that matter. In my last trip to Shanghai, I visited a large R&D lab of a biotech on a Friday afternoon, 5:30pm. Every seat was filled by a scientist *actually executing an experiment*.

Ultimately the path to global primacy in biotech is paved with hard work, smart science, shrewd decisions, and the indomitable will of founders & leaders.

True here in the US, true in China, true wherever new medicines will be created.

10

18

134

38,753