The Banking Infrastructure for Tokenized Deposits and Stablecoin Payments. Chat with our AI: ai.dcm.systems

Joined June 2023

- Tweets 130

- Following 52

- Followers 174

- Likes 32

72 Photos and videos

Pinned Tweet

Mar 20

What took decades to build shouldn't have to change in weeks.

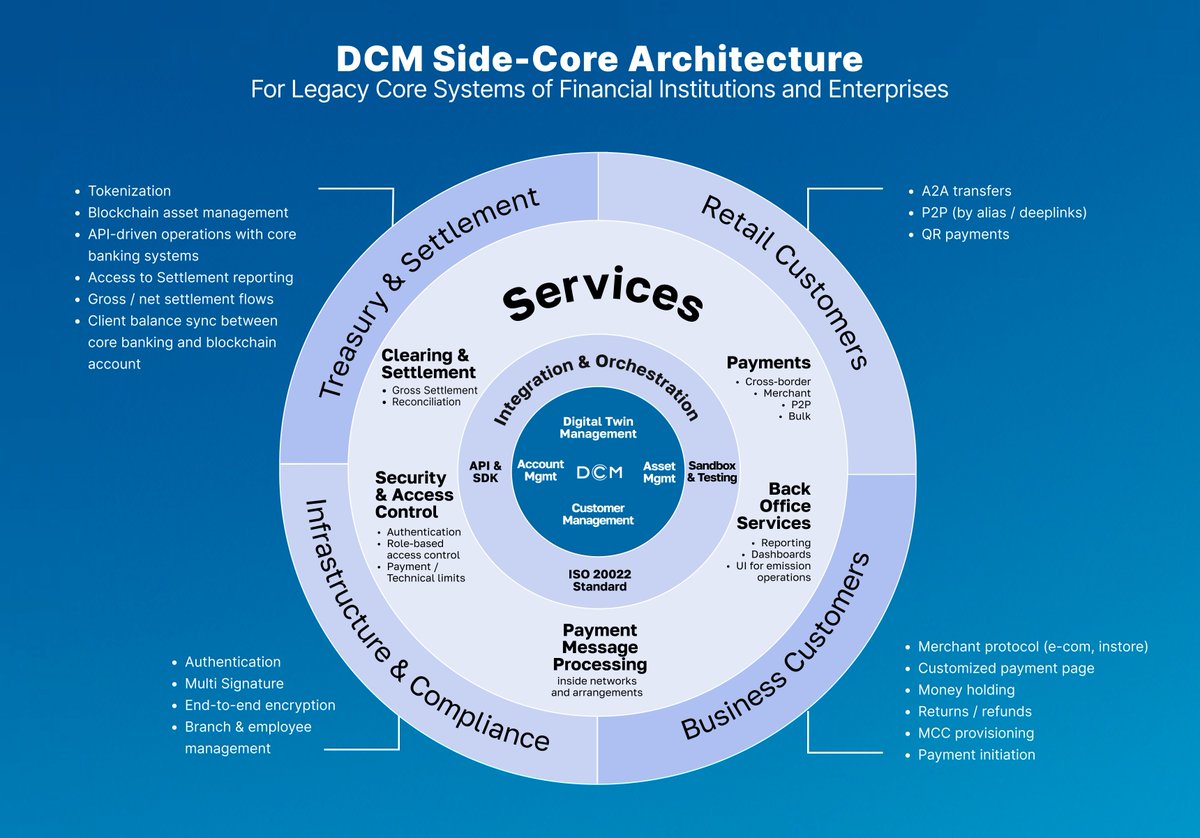

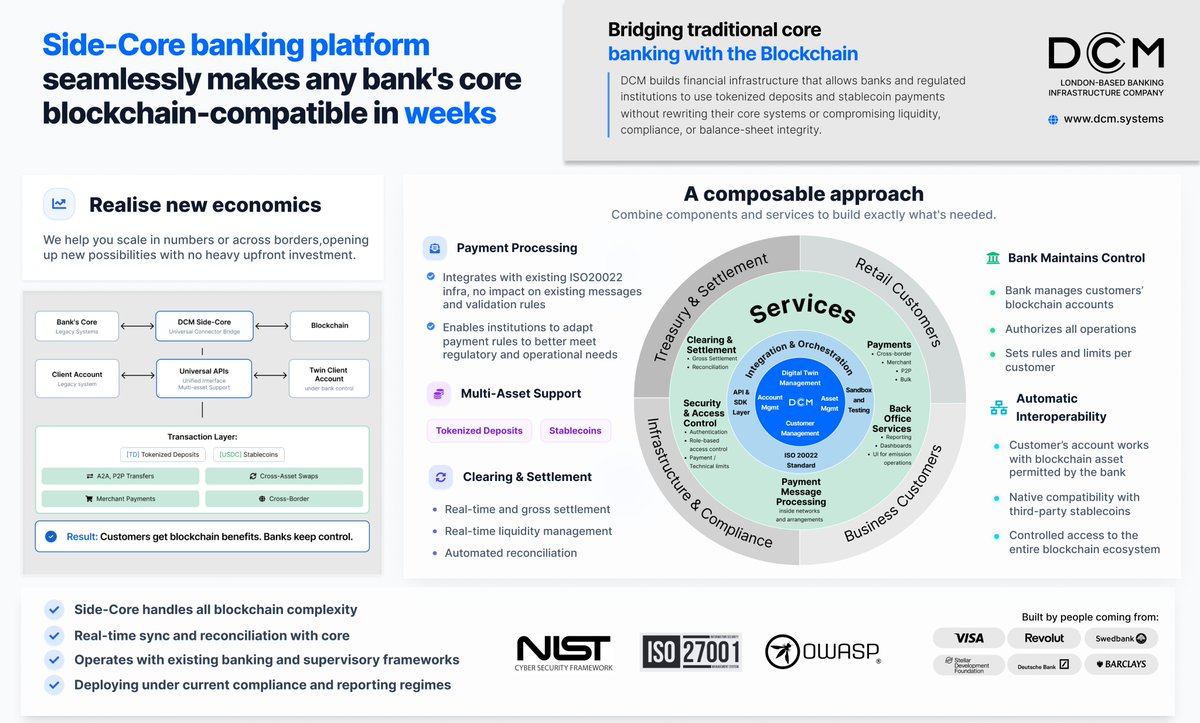

Core banking systems hold more than account balances. They hold the rules, controls, and processes that keep banks running reliably — day after day, under any pressure.

@dcm_systems developed a side-core platform that strengthens that foundation.

It sits alongside the existing bank core, keeps all records in place, and layers new capabilities on top: real-time settlement, easy connections between institutions, and blockchain execution where it actually makes sense — all within the operating standards banks already follow.

Integration takes weeks, not years. The core stays untouched. The bank just gets a new gear.

Learn more on our website - dcm.systems/

Or ask our AI any question you have - ai.dcm.systems/

2

99

1h

When wholesale banks invest in the network they plan to operate on, that may signal something worth paying attention to.

Digital Asset recently raised $355m for the Canton Network — with major wholesale banks among the investors. The headline is the capital. But the more interesting detail might be who is writing the checks and why.

Institutions that operate at this scale tend to invest in infrastructure they intend to use, not infrastructure they intend to watch. That pattern points to something shifting at the rails level — not at the application layer, not at the product layer, but in the underlying execution fabric these banks expect to settle on.

This raises a question that doesn't get asked often enough: if the rebuild is happening at the network layer, what role does the existing core banking system play going forward?

The answer, for most regulated institutions, is probably not replacement. Core migrations at wholesale scale carry execution risk that most institutions aren't positioned to absorb — and the value of those systems as records of balances, limits, and governance isn't diminished by the emergence of new settlement rails. The tension isn't between old and new. It's about how they connect.

What the Canton raise may suggest is that the institutions asking this question are moving past the theoretical phase. They're not funding a proof of concept — they're funding the network they expect to coordinate on. The architecture question that follows is how existing infrastructure participates in that network without requiring a full rebuild to do so.

That's the space DCM is designed for. Not replacing the core. Not patching around it. Building a coordination layer that sits alongside it — connecting existing systems to blockchain-native settlement, tokenized deposit flows, and real-time liquidity operations through an API-based integration that leaves the core as the system of record.

The Canton raise doesn't prove a direction. But it does point to where institutional attention is concentrating — and that concentration seems to be at the infrastructure layer, not the interface layer.

6

15h

mBridge is moving toward commercial launch. That may be worth pausing on.

For years, wholesale CBDC has existed mostly as research, pilots, and geopolitical signaling. mBridge — the multi-central-bank blockchain platform built across China, Hong Kong, Thailand, the UAE, and others — has now crossed into a different phase. A commercial launch suggests the question is shifting from "will sovereign digital money move on blockchain rails" to "how quickly does that reshape the infrastructure banks rely on."

What makes this particularly relevant is what mBridge is actually competing with. It is not positioned against crypto markets or retail payment apps. It points directly at correspondent banking rails — the SWIFT-era infrastructure that has governed cross-border interbank settlement for decades. That is a different kind of pressure.

Correspondent banking works through a chain of bilateral relationships, nostro/vostro accounts, and sequential settlement. It is functional, but it carries friction — delays, liquidity tied up in pre-funded accounts, limited transparency mid-flight. A blockchain-native sovereign settlement layer could, in principle, compress some of that. Whether mBridge delivers on that at scale remains to be seen, but the architecture is designed with that gap in mind.

The infrastructure question this raises for banks is a practical one. Participating in — or even maintaining optionality around — wCBDC rails requires a layer of blockchain interoperability that most core banking systems were not built to provide. Core replacement is not a realistic response to that. But a coordination layer that can connect existing systems to tokenized settlement flows, handle governed execution, and maintain the bank's own system of record intact — that may be what the readiness question actually looks like.

DCM's side-core architecture was designed with this kind of interoperability in mind. The platform connects to existing bank cores via API, supports tokenized deposit and stablecoin settlement flows, and is built on public blockchain infrastructure with ISO 20022 compatibility. The goal is not to replace what banks have built — it is to extend its reach into rails that are now going live.

mBridge's commercial launch does not mean correspondent banking disappears. But it may signal that the window for building blockchain-ready infrastructure — before sovereign networks start setting the terms — is narrower than it looked a year ago.

2

65

18h

Dharmesh Mistry recently put a number on something worth sitting with: AI agents could push daily banking transactions from 11 million toward 1 billion.

That shift is worth examining — not as a prediction, but as a question about infrastructure readiness.

The framing that tends to dominate AI-in-banking discussions is experience: smarter interfaces, better recommendations, more responsive service. That framing may be underselling the deeper implication. AI agents that initiate transactions aren't a UX layer — they're an execution layer. And execution at machine speed operates on different assumptions than anything legacy settlement rails were designed to support.

Batch processing, manual reconciliation, and asynchronous settlement were built around human-paced workflows. They may hold up reasonably well at current volumes. The question is whether they hold up when the initiating party is an agent operating at millisecond cadence, across multiple counterparties, with no tolerance for ambiguity in settlement state.

At that point, the bottleneck isn't intelligence — it's infrastructure. Specifically: whether the rails underneath can confirm settlement in real time, expose machine-readable state, and reconcile without manual intervention.

This is where the architecture question becomes practical rather than theoretical. Real-time settlement, programmable execution, and structured auditability aren't features that can be added incrementally to fragmented rails. They may need to be present by design — as a prerequisite for agentic flows to operate reliably, not as an upgrade after the fact.

Tokenized deposits and ISO 20022-native coordination point toward this kind of readiness: settlement that is deterministic, auditable, and legible to automated systems at the moment of execution.

None of this suggests existing infrastructure needs to be replaced. The more likely pattern is augmentation — connecting programmable execution layers to systems of record that remain exactly where they are, while extending their reach into environments that require real-time, machine-native settlement.

The 1 billion transactions figure may or may not materialize on any particular timeline. But the structural question it raises seems worth taking seriously now: if the execution layer is the constraint, what does the settlement layer need to look like before agents can operate at scale?

2

28

Jun 13

Visa is building the technology layer to convert traditional bank deposits into programmable digital money.

This is worth sitting with for a moment — not as a headline, but as a signal about where the infrastructure conversation is heading.

When a network-layer player of Visa's scale begins architecting around tokenized deposits, it may suggest that programmable bank money is crossing a threshold. Less an emerging experiment, more an expected capability that payment infrastructure is beginning to assume is present.

The architecture question this raises for banks is a specific one: if network-layer players are building deposit rails, which institution owns the layer closest to the deposit itself?

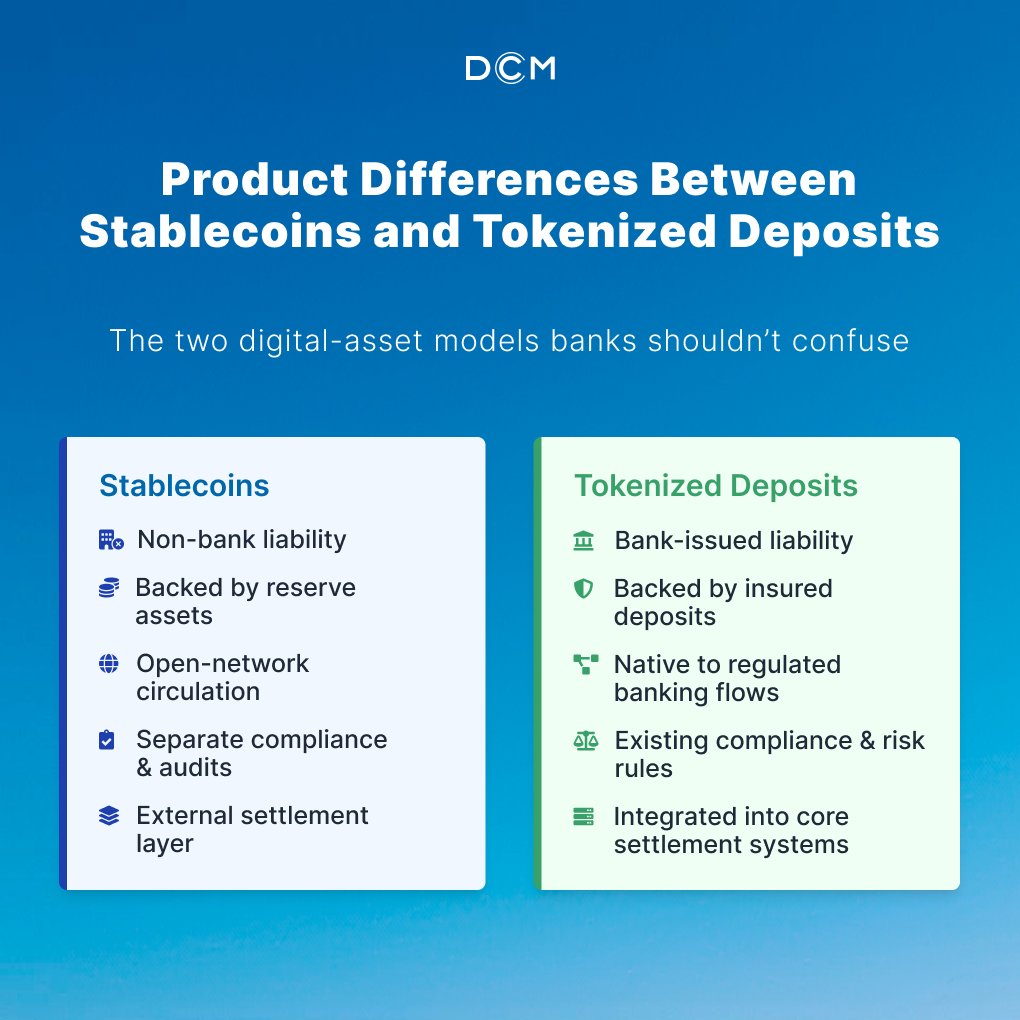

Tokenized deposits, by design, preserve the banking liability model. Balances stay on the bank's balance sheet. Governance and compliance remain under institutional authority. The bank core stays the system of record. What changes is the execution layer — how those deposits move, settle, and interact with programmable flows.

That execution layer is where the architectural decision becomes consequential. A bank that builds its own tokenized deposit infrastructure retains direct control over how its deposits behave in programmable environments. A bank that depends on third-party overlays may find that control is held elsewhere.

This is not a criticism of any particular approach — there are valid reasons institutions move at different speeds and through different partnerships. But the entry of players like Visa into this layer could point to a narrowing window for banks to define their own position before the layer above them is already built.

The infrastructure choices being made now — about where the execution layer sits, who governs it, and how it connects to existing core systems — may turn out to be more durable than they appear in the moment.

Programmable bank money seems to be moving from a differentiation story toward a baseline architecture question. The more interesting question may be who owns the rails when it gets there.

1

4

218

Jun 13

Mastercard is now settling card transactions on the Stellar network, 24/7, using regulated stablecoins. Monthly stablecoin volumes on Stellar are up 73% year-to-date and have reached all-time highs for three consecutive months.

That's worth sitting with for a moment.

This isn't a pilot or a proof-of-concept. One of the world's largest payment networks appears to be moving production settlement volume onto public blockchain rails — continuously, without batch windows, without correspondent intermediaries in the flow.

For infrastructure builders, the more interesting question this raises isn't about Mastercard specifically. It's about what happens to clearing architectures that were designed around T 1 cycles, batch netting, and correspondent relationships when settlement is increasingly happening in real time, around the clock, on shared public infrastructure.

The two models don't necessarily conflict — but they may not be fully compatible either. The gap between always-on settlement and batch-dependent reconciliation could become a meaningful operational friction point for institutions trying to participate in both worlds simultaneously.

This is roughly the fault line that DCM's side-core infrastructure sits on. Not by replacing what banks already run — the core banking system remains the system of record — but by connecting existing infrastructure to real-time settlement, tokenized deposit flows, and blockchain-based clearing without requiring a core migration.

The Mastercard signal may suggest that always-on settlement is moving from an emerging capability to an expected one. If that's the direction, the more pressing question for regulated institutions is probably less about whether to engage with these rails, and more about how existing infrastructure connects to them without creating new reconciliation gaps in the process.

Worth watching how this develops across other networks and settlement layers over the next 12-18 months.

1

1

3

77

Jun 12

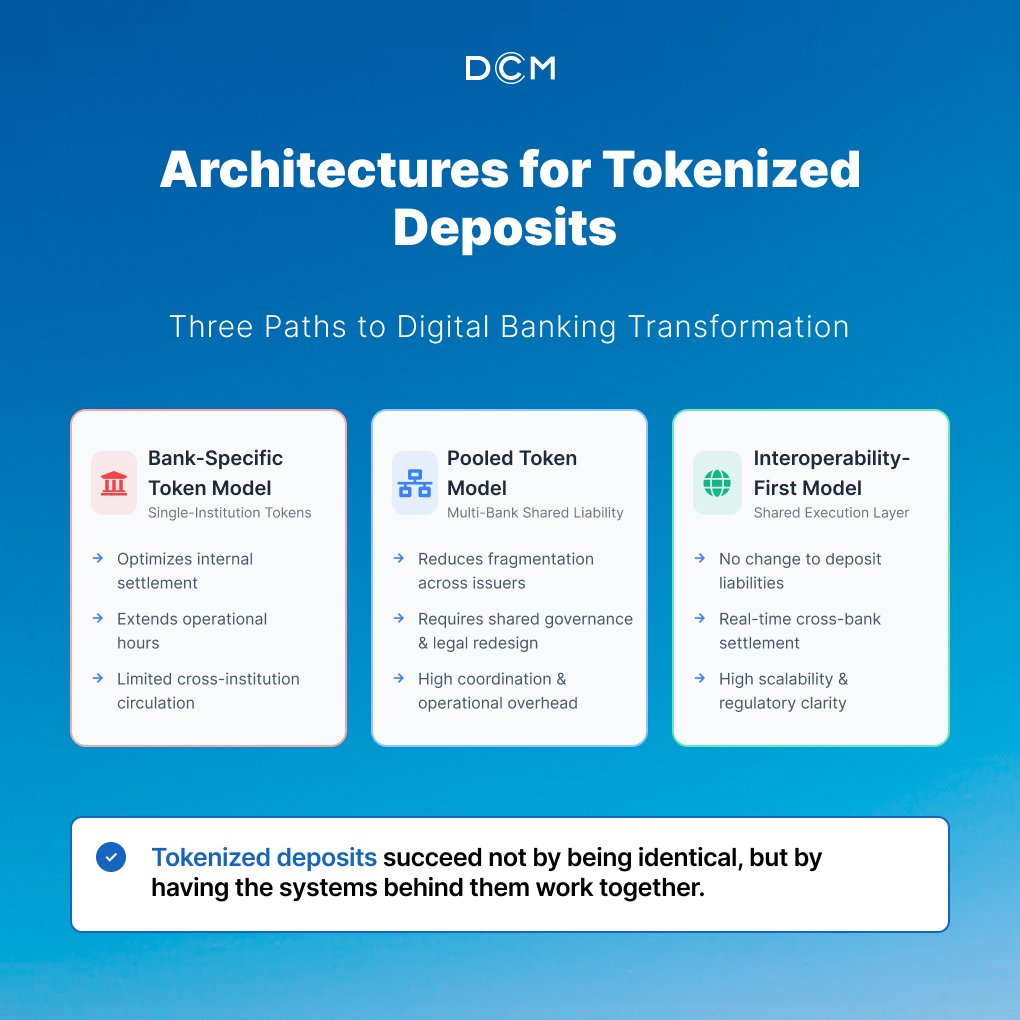

Major US banks are reportedly moving to co-build a shared tokenized deposit network through The Clearing House, with a mid-2027 target. That timeline and that structure are worth examining carefully.

When institutions of that scale choose to build shared rails rather than compete on rails, it tends to signal that the infrastructure layer is where the real coordination is happening — not at the product layer.

But shared rails raise a practical question that often gets less attention: what connects a bank's existing core to those rails? Legacy core banking systems were not designed for tokenized deposit flows, real-time settlement logic, or blockchain-based execution. The gap between where most banks operate today and where those rails will run is not trivial.

This is where the infrastructure conversation gets more nuanced. A bank joining a shared network still needs to handle tokenized deposit issuance, intraday liquidity coordination, reconciliation, and governed execution — all of which have to connect back to the core as the system of record. That connective layer doesn't come with the network membership.

The DCM side-core is designed precisely for this kind of environment. It sits between an institution's existing core and external execution infrastructure — whether that's a shared network, a blockchain layer, or a counterparty system — without replacing or migrating anything the bank already runs.

What the TCH announcement may suggest is that the tokenized deposit infrastructure conversation is maturing from 'whether' to 'how.' And the 'how' points toward a significant amount of integration work that institutions will need to solve at the middleware level.

The largest banks co-building the rails could become a validation point for the broader category — but it also raises the question of what has to exist underneath for any bank, not just the largest ones, to participate meaningfully.

That question is, arguably, where the more durable infrastructure opportunity sits.

2

21

Jun 12

TIPS just went live with real-time cross-currency settlement between euro, Danish krone, and Swedish krona.

What's worth noting: this wasn't unlocked by a new policy framework. It was delivered through infrastructure engineering — payment service providers can now settle across currencies in real time because the underlying plumbing was built to support it.

The same logic may apply to the ISO 20022 ↔ blockchain translation challenge. Interoperability between structured financial messaging and programmable settlement rails looks like a coordination problem on the surface — but at its core, it's an engineering one.

That's the layer DCM is built to operate in.

49

Jun 10

The ICBA's call for a policy pause on digital asset integration points to something worth examining carefully.

The core of their argument isn't really about blockchain — it's about what's missing: deposit insurance equivalence, clear identity accountability, and meaningful loss-absorption mechanisms. Those gaps are real, and consumer distrust around exchange hacks and uninsured losses reflects them.

What's interesting is that this framing inadvertently reads like an infrastructure specification. The trust that makes bank deposits reliable isn't regulatory sentiment — it's a set of concrete design layers: governed identity, institutional accountability, and defined recourse structures.

Any blockchain-ready banking architecture that doesn't address those primitives from the start may face the same credibility questions. The technology isn't the variable — the governance design is.

For regulated institutions exploring this space, that distinction could matter quite a bit.

17

Jun 10

The conversation around agentic payments is moving fast — and most of it is focused on the orchestration layer: AI agents routing transactions, optimizing rails, automating decisions.

That framing may be missing something important.

When agentic systems execute value in real time across digital currencies and instant rails, the question shifts from 'who is routing?' to 'what does the layer beneath actually guarantee?' Orchestration can be intelligent. But settlement is either final or it isn't.

This points to a distinction worth examining more carefully. Orchestration optimizes the path. Settlement resolves the obligation. The two are not the same problem — and building adaptive payment fabric on top of a clearing layer that wasn't designed for real-time, multi-currency, machine-initiated flows may introduce more fragility than the orchestration layer can absorb.

What the finality layer likely needs to provide — regardless of how sophisticated the agents above it become — is something closer to: atomic settlement across counterparties, deterministic reconciliation that doesn't require manual intervention, and an audit trail that is immutable and available in real time, not reconstructed after the fact.

The infrastructure challenge here isn't just latency. It's the coordination problem. When multiple agents are executing across multiple rails simultaneously, the clearing layer needs to resolve obligations without creating cascading dependencies or silent failures that only surface during end-of-day reconciliation.

ISO 20022 compatibility, on-chain settlement finality, and governed execution start to look less like feature considerations and more like foundational requirements when the payment fabric is expected to operate autonomously.

The 'intelligent payments fabric' framing from conversations like EBAday 2026 raises a useful question for infrastructure teams: is the intelligence being added to a settlement layer that can support it — or is it being layered over architecture that was designed for a different operating model?

That may be the more durable question as agentic payment narratives continue to develop.

2

24

Jun 9

With instant payments now mandatory across the euro area, something quieter is starting to shift in how European B2B treasuries think about settlement.

Rather than treating the invoice as the trigger for payment, more treasury teams appear to be moving toward the underlying contract as the reference point — linking payment execution directly to milestone conditions, delivery confirmation, or agreed terms. On the surface, this looks like a workflow change. But the infrastructure implications may run considerably deeper.

Contract-linked payment triggers are, in effect, programmable money logic. They assume that somewhere in the stack, a system can receive a condition signal, validate it against a shared reference, and initiate settlement — without a human manually matching an invoice to a payment run. That is not how most clearing and liquidity layers were designed to work.

The question this raises for banks is fairly specific: can their settlement infrastructure expose programmable triggers at the contract level? And if not, what fills that gap? Fintechs operating on the edge of the payment stack have shown a consistent pattern of routing around layers that cannot expose the right interfaces quickly enough.

This points to a broader architectural tension. Instant payment rails have compressed settlement time. But the reconciliation and liquidity management layers underneath often still operate on batch logic, disconnected from the conditions that actually govern when an obligation is due. Closing that gap may require more than faster messaging — it could demand a coordination layer that connects contract state to settlement execution in real time, with auditability on both sides.

For regulated institutions, the governance dimension compounds the challenge. Contract-linked triggers need to be permissioned, auditable, and aligned with the bank's existing compliance controls — not bypassing them. Infrastructure that sits between the contract and the payment rail, without displacing the core system of record, seems better positioned to absorb that complexity than solutions that require core migration or new intermediary relationships.

What the shift toward contract-linked payments may ultimately signal is that the unit of settlement is evolving — from the invoice, to the obligation, to the condition. Banks that can expose that logic through their clearing infrastructure may find themselves better positioned as B2B treasury expectations continue to move.

3

22

Jun 9

JPMorgan, Citi, Bank of America, and Wells Fargo are reportedly building a shared blockchain for tokenized deposits through The Clearing House, with a target launch around 2027.

The stated motivation is worth noting: defensive positioning against stablecoins, not client demand. That framing may reveal something important about how large institutions are currently approaching digital settlement infrastructure.

Building a shared closed-loop rail among the largest banks solves one problem — internal interoperability among participants — while potentially creating another. A proprietary consortium network is, by design, bounded. It raises a question about what happens at the edges: where that rail meets other banks, other jurisdictions, other token standards, or counterparties operating on open networks.

The boundary between a bank deposit rail and a token rail is where the real infrastructure complexity tends to concentrate. Reconciliation logic, intraday liquidity positions, compliance controls, auditability — these don't resolve themselves by choosing one network over another. They require an execution layer that can operate across both environments without abandoning the governance model banks are built on.

This is arguably the more durable infrastructure question: not which network wins, but what sits at the junction between existing core banking systems and emerging token-based settlement flows — and whether that layer is bank-grade.

Tokenized deposits preserve the banking liability model. Balances remain on bank balance sheets. The bank core remains the system of record. Those principles don't change with the network. What changes is whether the coordination layer connecting them can handle the compliance, permissioning, and liquidity logic that regulated institutions require.

The direction these institutions are moving points to growing institutional seriousness about deposit tokenization as infrastructure — not a product category. How that infrastructure gets built, and who controls the boundary layer, may matter more in the long run than which consortium gets to launch first.

49

Jun 9

When Visa, Mastercard, Stripe, and Coinbase converge on shared stablecoin rails, it may be worth asking: what does that mean for institutions that aren't part of that architecture?

Reports of a joint stablecoin platform involving these four networks point to something beyond a product announcement. It looks more like the early formation of a clearing layer — one built around stablecoin settlement rather than traditional interbank messaging.

For banks, the question this raises isn't really about stablecoins as an asset class. It's about settlement connectivity. If the dominant payment networks begin routing through a shared stablecoin rail, institutions without a way to interact with that infrastructure may find themselves outside the execution flow — not by strategic choice, but by architectural default.

This signals a shift worth examining carefully. The gap may no longer be between banks that have a "crypto strategy" and those that don't. It could become a gap between institutions that can connect to emerging settlement layers and those that can only operate within legacy ones.

What makes this particularly relevant for regulated institutions is that stablecoin interoperability doesn't require abandoning existing core banking systems. The more useful frame may be: can your current infrastructure coordinate with tokenized flows, govern them, and settle them — while keeping your balance sheet as the source of truth?

For most institutions, the honest answer today is probably no — not because the will isn't there, but because the connective layer doesn't yet exist inside their stack.

That connective layer is precisely what a side-core architecture is designed to provide. Not a replacement for the bank core, but an execution and coordination layer that can handle stablecoin settlement, tokenized deposit issuance, and third-party stablecoin interoperability — all under institutional governance and compliance controls.

The Visa–Mastercard–Stripe–Coinbase signal may suggest that the window for building that connectivity is narrowing. The more measured reading is that this is still early — but the structural direction seems increasingly clear.

1

42

Jun 4

Mastercard is now piloting instant cross-currency payments on the ECB's TIPS platform, working alongside the central banks of Denmark and Sweden. It's worth paying attention to what's actually being tested here.

TIPS was built for euro-denominated instant settlement. Extending it to cross-currency flows — in real time — is a meaningful architectural stress test. The decisions made in these pilots about message formats, settlement finality, and interoperability protocols tend not to stay experimental for long.

What gets hardened in central bank infrastructure pilots often becomes the baseline that everything else has to connect to. That's not a criticism of the process — it's how standards form. But it does raise a practical question for banks: what does your side of that interface look like?

Connecting to TIPS-class rails, whether today's version or a future wCBDC-enabled variant, requires more than API access. It points to a need for settlement logic that can handle tokenized cash flows, ISO 20022-aligned messaging, and governed execution — without those capabilities requiring a core banking replacement to achieve.

ISO 20022 compatibility matters here in a specific way. It's not just a formatting question. It's the connective tissue between legacy interbank messaging and whatever settlement architecture emerges from pilots like this one. Infrastructure that can translate between those layers — without sitting in the middle as a financial intermediary — may become increasingly relevant as these standards solidify.

The governance dimension is also worth noting. wCBDC and TIPS-class rails come with auditability and permissioning expectations that mirror what regulated institutions already manage internally. The infrastructure on the bank's side likely needs to reflect those same properties.

None of this suggests that existing core banking systems are inadequate. It suggests that the execution and coordination layer sitting between a bank's core and external settlement rails may need to evolve in a fairly specific direction — standards-aligned, auditable, and capable of handling tokenized settlement flows alongside conventional ones.

These pilots are still early. But the architectural choices being made in them are worth watching closely.

finextra.com/newsarticle/478…

1

2

50

Jun 4

KBank and Ant International are now running live USD settlement on JPMorgan's Kinexys blockchain infrastructure. That's worth pausing on.

This isn't a sandbox experiment or a proof-of-concept announcement. Two significant Asia-Pacific financial players have moved real cross-border USD flows onto blockchain rails — bypassing the correspondent banking chain that has defined international settlement for decades.

What that may suggest isn't that correspondent banking is finished, but that the threshold question has shifted. It's no longer 'can blockchain infrastructure handle production settlement?' — that case appears increasingly settled. The more active question now seems to be: how does an institution get there without dismantling what already works?

This is where the infrastructure tension becomes interesting. Most banks running cross-border USD flows have existing core systems, reconciliation processes, and compliance frameworks that aren't going anywhere. The challenge isn't access to modern rails — it's connecting those rails to legacy architecture in a way that preserves institutional control, auditability, and governance.

A deployment like Kinexys points to what's becoming the real differentiator: not just having blockchain settlement capability, but having the connective layer that lets a regulated institution activate it cleanly. The rails matter, but so does what sits between the rails and the bank's system of record.

For institutions watching this, the question worth asking may be less 'which blockchain network?' and more 'what does our integration architecture need to look like to participate in these flows without rebuilding from scratch?'

That connective tissue — between existing core infrastructure and real-time settlement rails — is where the operational complexity actually lives. And it's where the next set of infrastructure decisions will likely be made.

finextra.com/newsarticle/478…

43

Jun 1

ClearBank's Digital Asset Rails launch is worth pausing on — not just for the 24/7 EUR payout capability, but for what the architecture behind it implies.

The headline feature is SEPA Instant settlement bridging digital assets and traditional rails. That matters. But the deeper signal may be what it reveals about how settlement infrastructure is being rethought at the layer below the product.

Most bank cores were designed around a sequential logic: initiate, clear, reconcile, fund. Those steps happen in discrete systems, often with meaningful latency between them. That architecture worked when settlement windows were fixed and liquidity could be planned accordingly.

What programmable liquidity introduces is a different coupling — one where settlement finality and liquidity coordination need to resolve together, in real time, across counterparties that may be operating on different underlying systems. That's not a feature addition. It points to a structural redesign of how the settlement layer functions.

The question this raises for most institutions is less about whether to support digital asset flows, and more about whether their existing infrastructure can support the coordination logic that real-time programmable settlement requires. Those are not the same problem.

What ClearBank appears to be building — and what moves like this may signal more broadly — is that the settlement layer is becoming a programmable execution environment, not just a ledger update at the end of a transaction chain.

For banks evaluating where to invest in infrastructure, this distinction could matter quite a bit. The 24/7 availability is visible. The coordination architecture that makes it function reliably is less visible, but arguably more consequential.

That's the layer worth building around.

finextra.com/pressarticle/10…

18

Jun 1

The BIS just published findings from a multi-central-bank prototype demonstrating that tokenisation can meaningfully address inefficiencies in wholesale cross-border payment flows.

This is worth pausing on — not because tokenised settlement is a new idea, but because the conversation has shifted. Central banks are no longer publishing whitepapers about what tokenised rails could do. They are building, testing, and measuring.

The gap that emerges from this kind of work is instructive. Legacy correspondent banking was designed around a different set of constraints — batch processing, bilateral relationships, deferred reconciliation. Tokenised settlement operates on a different logic: atomic, programmable, with settlement finality that doesn't depend on the same chain of intermediaries. Bridging these two architectures isn't purely a policy question anymore. It points toward an infrastructure question.

For banks, this may suggest that the relevant preparation isn't a core replacement or a migration project — it's building a translation layer capable of working with both. Something that can speak ISO 20022 to existing systems and tokenised deposit or wCBDC rails simultaneously, without forcing an either/or decision.

What the BIS prototype signals, at least in part, is that the institutions closest to readiness will likely be those that have already begun testing that interoperability — not waiting for wCBDC to be fully defined before engaging with the architectural questions it raises.

The infrastructure gap between where correspondent banking sits today and where these prototypes are operating is now something that can be measured in working code. That feels like a meaningful shift in how banks might want to think about their own preparation timelines.

finextra.com/newsarticle/478…

1

153

May 27

Georgia's government has commissioned Tether to build GEL₮ — a Lari-pegged stablecoin for national use. It's an interesting architectural moment worth examining carefully.

When a sovereign government outsources its monetary rail to a private issuer, the settlement layer for that currency becomes someone else's infrastructure. Every bank operating in that jurisdiction now has a dependency they didn't design, didn't negotiate, and don't control at the protocol level.

That may not be a problem in the short term. But it does raise a question that banks operating in similar jurisdictions will increasingly face: how do you integrate with a nationally significant stablecoin rail while maintaining your own compliance controls, liquidity governance, and balance-sheet integrity?

The tension isn't about whether private issuers can build capable infrastructure — clearly they can. It points more to a structural gap: banks weren't typically part of the architecture decision, yet they're expected to operate within whatever rails emerge.

This signals a broader pattern. As stablecoin rails — whether sovereign-commissioned or market-driven — become part of the settlement fabric, banks may need a coordination layer that sits between their core systems and external monetary infrastructure. Something that handles interoperability, compliance mapping, and liquidity movement without requiring the bank to rebuild its internal architecture around each new rail.

Tokenized deposits could play a role here too. If a bank can issue its own deposit-backed instrument that settles natively alongside GEL₮ or similar assets, it maintains a presence in the settlement layer rather than pure dependency on it.

The Georgia case may be early and specific — but the architectural question it surfaces could become relevant far more broadly as governments and institutions continue experimenting with commissioned stablecoin infrastructure.

finextra.com/newsarticle/478…

1

41

May 27

There's a growing assumption that moving onto blockchain rails simplifies reconciliation. The data may suggest otherwise.

When tokenized deposits or stablecoin flows are introduced, auditability doesn't consolidate — it splits. On-chain state and off-chain state now need to match, continuously, in a way that holds up under regulatory review.

For regulated institutions, that points to a structural question: is reconciliation infrastructure being treated as a compliance requirement, or still as an operational afterthought?

The inability to prove data consistency across systems could become a compliance exposure in its own right — not just an operational inefficiency. That framing seems worth taking seriously before the audit, not after.

finextra.com/blogposting/318…

2

23

Apr 29

@dcm_systems has completed ISO/IEC 27001:2022 certification

The certification validates our approach to information security across internal processes, infrastructure, and data management

It is assessed through regular external audits and ongoing controls

A consistent way to ensure security standards are applied and maintained

2

74

Apr 9

Every time we read a document like this, we come back to the same feeling: we're moving in the right direction. It just takes time.

This month, the @IMFNews published a note on tokenized finance by @TobiasAdrian1, the Fund's Financial Counselor. His conclusion: tokenization is not a marginal efficiency gain. It's a structural reallocation of trust within the financial system.

The IMF outlines what this future system requires:

→ Settlement anchored in safe assets (tokenized deposits or wCBDC)

→ Shared ledgers with clear institutional governance

→ Legal certainty and finality

→ Interoperability across institutions and borders

→ Crisis management tools that work at machine speed

When we read this, we weren't surprised. This is what we've been building — and what we launched in production in late 2024.

The prozora.network is a live interbank network built leveraging blockchain, with an institutional governance layer anchored by the Central Bank’s payment system. Payments settle atomically. Compliance is embedded. Participants are identified and regulated.

Not a pilot. Not an MVP. Production.

Documents like this matter to us — not as validation, but as a compass. When leading policymakers describe what the future of finance should look like, it helps us make sure we're still on the right track.

The window for shaping tokenized financial architecture is open. As the IMF notes — it won't remain so indefinitely. This note is worth reading.

Read the note here - elibrary.imf.org/view/journa…

1

4

53