@AnchorlessBD Founder & Managing Partner. Global capital for Bangladesh. Diaspora narrative at @bdeshiglobal. Film, Ramen Gaming. 🇧🇩☀️

Joined February 2009

- Tweets 6,467

- Following 978

- Followers 4,651

- Likes 3,954

933 Photos and videos

Pinned Tweet

Jun 8

Centralized my writing on capital, culture and the Bangladeshi diaspora in one place:

rahatahmed.com

1

5

232

Jun 6

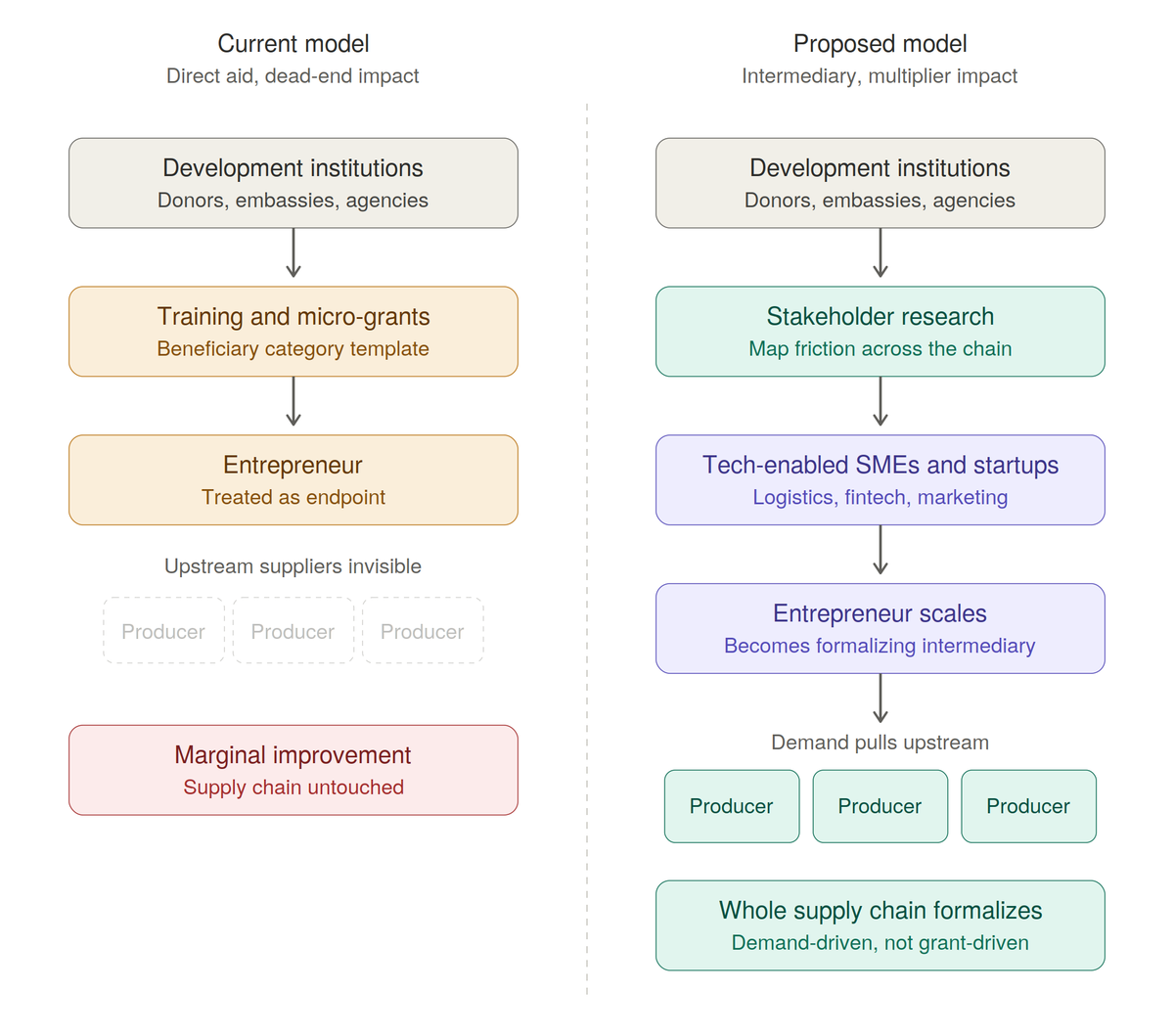

Why are Bangladesh's non-tech entrepreneurs not getting the support they need to be successful?

My latest piece talks about the structural flaw in the country's current approach—and how to work towards fixing it.

1

5

340

May 19

I started following Arsenal seriously in 2006. This has been 20 years in the making. Countless hours at Nevada Smith's on 3rd Avenue, at the Blind Pig and O'Hanlons on 14th Street. Countless mornings in New York, countless nights in Dhaka. Through thick and thin, here we are. COME ON, YOU GUNNERS! CHAMPIONS WE ARE!

4

451

May 19

Last week, I had the privilege of introducing the framework for @bsicfund's US$35M inaugural VC fund.

Backed by 39 Bangladeshi banks, BSIC activates local capital, offers co-investment for foreign VCs, and shapes policy for Bangladesh's startups at unprecedented scale.

1

1

8

601

May 8

Bangladeshi filmmaker Rezwan Shahriar Sumit's latest film Master (2026) is playing at the @sydfilmfest on June 4th and 6th! 🇧🇩🥳

sff.org.au/program/event/mas…

Sumit is also the only person I know who went to @NYUTischSchool as well as IBA, Bangladesh's top business school!

1

253

May 6

Second place or not, we're finally gonna have a Bangladeshi-American comedian going big! @UsamaStandsUp's phone is gonna be ringing! 🇧🇩🥳

The moment Ron Taylor won #FunnyAFwithKevinHart LIVE on Netflix!!!

Winning the live vote, Ron will go on to star in his very own Netflix comedy special.

1

10

729

Apr 29

Bangladeshi-American standup comedian Usama Siddiquee @UsamaStandsUp is a finalist on Netflix's Funny AF with Kevin Hart! On May 4 and 5, viewers will be able to vote via their app on who the winner is—so let's go and show our man some love! 🇧🇩☀️

#FunnyAFwithKevinHart

8

114

4,610

Apr 24

Shompa Kabir representing Bangladeshi food and getting an apron from @GordonRamsay on @MASTERCHEFonFOX!

Gotta love the "New York runs on Bangladeshis, man!"

4

79

477

14,624

Apr 12

In memory of Asha Bhosle’s passing, here’s the seminal “Brimful of Asha” by @CornershopHQ—made as a tribute to her—that put South Asian vibes across global households back in 1997.

4 Mar 2024

Cornershop

“Brimful of Asha”

When I Was Born for the 7th Time

Wiiija (1997)

Director: Phil Harder

3

461

Apr 9

39 banks in Bangladesh just launched a US$35 million venture capital fund together. It will operate in an institutional structure, built to global standards and terminology.

A total gamechanger for founders and co-investors, globally and locally.

exitstack.co/posts/39-bangla…

2

3

7

320

Apr 2

Herzog talking about Edward Yang’s Yi Yi feels so exceptionally comforting.

“Films let us live three times.”

3

305

Mar 25

Watching this free kick by @RonanSullivan12 excites me about the future of sports in Bangladesh. What a goal!

Mar 24

Watch this stunning free-kick from 18-year-old Ronan Sullivan, brother of USMNT and Manchester City prospect, Cavan, for the Bangladesh U20 national team 🇧🇩

7

426

Mar 16

"Why Bangladesh Should Use FDI as a Foreign Policy Strategy" — my latest in the Daily Star on why investment remains one of the most underutilized and misunderstood tools in Bangladesh's diplomatic approach:

thedailystar.net/slow-reads/…

1

4

291

Mar 8

One of the biggest fintech opportunities in the world right now may be in Bangladesh.

Bank deposits have hit a five year high in Bangladesh—which ironically means banks are less incentivized to lend to SMEs and the middle class. And considering there's not much credit scoring infrastructure, there's no way to do it easily anyway.

The result? SME contribution to GDP sits at 25-30%—compared to 45-60% in Indonesia, Vietnam, and Pakistan. This means millions of people and businesses can't borrow, can't scale, and can't build wealth.

This is exactly where well-funded fintech startups can fill the gap: Alternative credit scoring—mobile money flows, utility payments, transaction history—can do what traditional banks haven't been able to.

And the market makes it even more compelling: 180 million people, a nearly $500 billion economy, and a middle class with rising incomes and almost no access to formal credit.

For those in the diaspora and beyond, this is a rare moment where market timing, market size, and genuine human impact align. This wouldn't just be about making money but fundamentally changing the lives of millions.

2

10

503