9 Photos and videos

If you are a B2B SaaS founder in 2026 still dealing with 3-day banking delays, heavy manual accounting tracking, and high cross-border settlement fees just because you think stablecoins "aren't ready for enterprise use," you are actively bleeding margin.The infrastructure is live. The volume is scaling.

We bootstrapped @xentfi to mainnet and hit $25k MRR by solving exactly this for 50 merchants who realized waiting for legacy banking rails is a slow death sentence for cash flow velocity.

Ship on the reality of the market, not old tech debt.

#buildinpublic #web3 #fintech #startup

2

13

Unpopular opinion: The market has completely stopped rewarding vague "decentralization" stories.

In 2026, nobody cares if your architecture is 100% ideologically pure if it takes 3 clicks too many and breaks at month-end reconciliation. The capital is aggressively moving toward projects that solve boring, expensive, legally messy business workflows. High-throughput rails are an easy win. The real engineering moat is handling the quiet structural chaos of automated ledger reconciliation when thousands of multi-chain corporate transactions hit at once.

Stop shipping tech looking for a problem. Fix the friction. That’s the entire blueprint behind @xentfi.

1

11

The 2026 tech playbook has officially inverted.Five years ago, founders used complex crypto jargon to try and look futuristic to traditional businesses. Today, the biggest institutions on earth are quietly moving billions onto stablecoin rails while early-stage founders are trying to build consumer frontends with no backend substance.The "Mullet Strategy" won: Traditional, boring business in the front. Immutable, high-velocity Web3 rails in the back.

If your B2B platform isn't actively automating stablecoin operations and cross-border settlement yet, you aren't "waiting for maturity." You’re just letting your competitors out-scale your capital efficiency.We didn't wait for permission. We built @xentfi because the infrastructure layer is where the real value settles.

1

1

1

9

Jun 12

Visa moving billions in stablecoins across VisaNet and expanding 7-day on-chain settlement is the ultimate corporate validation.

For years, critics said stablecoins were just for DeFi degens. In 2026, the biggest payment aggregators on earth are treating them as room-temperature superconductors for enterprise liquidity.

If you are a B2B founder still relying on 3-day SWIFT banking delays because you think crypto "isn't ready for corporate use," your competitors are already out-executing you.

Stop waiting for permission. We built @xentfi to give businesses instant, friction-free stablecoin ledger reconciliation right now. Build on the trend, or get left behind.

Jun 12

Two days ago, Visa’s Chief Product Officer dropped a quote that every B2B founder needs to pin to their wall:

“AI is transforming the front end of commerce. Stablecoins are reshaping the back end.”

When the world’s biggest payments network openly admits that stablecoins are the definitive backend for global money movement, the debate is over.

But here’s the reality: while Visa scales the high-level rails, mid-market B2B enterprises are still drowning in manual ledger reconciliation and multi-chain settlement fragmentation.

This is exactly why we built @xentfi. We didn't wait for the giants to clear the path. We built the automated execution infrastructure that allows businesses to run on these rails today with $10k MRR and 50 merchants already live.

The future isn't coming; it's being coded. Let’s scale.

1

7

Jun 12

Two days ago, Visa’s Chief Product Officer dropped a quote that every B2B founder needs to pin to their wall:

“AI is transforming the front end of commerce. Stablecoins are reshaping the back end.”

When the world’s biggest payments network openly admits that stablecoins are the definitive backend for global money movement, the debate is over.

But here’s the reality: while Visa scales the high-level rails, mid-market B2B enterprises are still drowning in manual ledger reconciliation and multi-chain settlement fragmentation.

This is exactly why we built @xentfi. We didn't wait for the giants to clear the path. We built the automated execution infrastructure that allows businesses to run on these rails today with $10k MRR and 50 merchants already live.

The future isn't coming; it's being coded. Let’s scale.

15

Jun 12

Mastercard just announced they are officially expanding their global network to support regulated stablecoins (USDC, PYUSD) for weekend and holiday cross-border settlement.

Traditional finance isn't fighting crypto anymore—they are treating it as the definitive corporate liquidity rail.

But while Mastercard is opening the floodgates for card networks, global businesses still face a massive bottleneck: local B2B ledger reconciliation, accounting, and multi-chain execution are still incredibly fragmented.

This is exactly why we are building @xentfi.

As the giants build the high-level infrastructure, Xentfi provides the seamless B2B execution layer that lets companies automate corporate ledger reconciliation and scale stablecoin operations with zero friction. TradFi is validating the rail; we are scaling the utility.

#buildinpublic #web3 #fintech #startup

1

1

37

Jun 12

Unpopular opinion: "Stealth mode" is the biggest trap for early-stage founders.

Unless you are building literal rocket propulsion systems or deep proprietary defense tech, nobody is going to copy your raw idea. And if your startup can be completely killed just because a competitor saw a screenshot of your product, you didn't have a moat anyway.

Build out loud, ship fast, and let the copycats try to keep up with your execution velocity.

12

Jun 12

The hardest pill to swallow as a founder:

No one cares about your 40-page whitepaper.

No one cares about your perfect pitch deck.

No one cares about your "stealth mode" landing page.

Until you have a live product that a user can actually interact with, you don't have a startup. You have a hobby.

Stop optimizing for aesthetics and start optimizing for velocity. Ship the code out loud.

8

Jun 11

We built a B2B stablecoin infrastructure layer, launched on mainnet, onboarded 50 merchants, cleared $100k in volume in our first week and scaled to $10k MRR in less time than it takes an institutional VC to schedule a second partner meeting.

Traditional tech startup playbook: Spend 6 months polishing a pitch deck, raising a massive pre-seed round, and hunting for validation from committees.

Our playbook: Ship the code, solve the actual settlement friction for real users, and let the traction fund the growth.

The best validation isn't a term sheet signed by a suit—it's a recurring invoice paid by a business owner who uses your infrastructure every day.

If you are a founder waiting for "market conditions" or a check to start building, you’re already losing to the teams who are just out-shipping you.

#buildinpublic #web3 #fintech #founder

8

Jun 11

No VC check can buy the raw feedback you get from building in public.

When we started building @xentfi, we decided to bypass the slow, institutional fundraising cycle and just ship directly to mainnet.

The result? By building out loud, we didn’t just get vanity metrics—we got 50 real B2B merchants who told us exactly where legacy payment rails were failing them, allowing us to clear $100k in volume in our first 2 weeks.

The biggest lesson I’ve learned: Investors back momentum, but users back products that solve real pain. When you build in public, you don't have to guess if you have product-market fit. Your timeline tells you every single day.

Stop waiting for permission or a term sheet to validate your vision. Drop your build, listen to the feedback, and let the traction do the talking.

#buildinpublic #web3 #fintech #startup

1

12

Jun 11

Bootstrapped to cross-chain mainnet, onboarded 50 B2B merchants, and cleared over $100k in transaction volume in our first 2 weeks.

We didn't wait for rigid institutional check-boxes. We just built the stablecoin payment infrastructure designed to scale global businesses safely without the friction.

With this kind of immediate traction out of the gate, how much do you think we should raise for our pre-seed? Drop your thoughts below 👇

10

Jun 11

The global B2B cross-border payments market is a $150T opportunity, with annual stablecoin settlement volume already surpassing $10T.

The dominant macro trend is enterprise adoption shifting away from legacy SWIFT friction toward on-chain liquidity. @xentfi captures this growth by providing the compliant infrastructure layer required to scale stablecoin payments safely for global businesses.

9

Jun 11

Global businesses face massive operational friction and manual reconciliation delays when trying to scale with stablecoin payments.

,@Xentfi builds unified, compliance-ready payment infrastructure that automates stablecoin settlements seamlessly.

8

Mar 26

We’re coming hard 🚀 Time to disrupt the silence.

Meet my co-founder @FaithfulGodwinC

Nigeria ➡️ Africa ➡️ The Globe. 🌍

We are shipping @xentfi —embedded stablecoin infrastructure for B2B payments using cNGN & USDC for instant settlement.

#BuildInPublic #Web3

1

3

56

The countdown has officially begun. In exactly 4 days, the "invisible engine" for stablecoin infrastructure goes live.

What’s landing in 4 days:

🔹Waas 🔹 The Automation Engine🔹The Smart Router

The OS for 2026 is landing.

join👉 xentfi.com

1

1

47

Jan 28

3s stablecoin finality is an illusion.

Behind it, a hidden fiat engine determines if you settle or stall. Xentfi builds the bare-metal infra for this:

🔹 WaaS: Auto-Sweep & Settlement

🔹 Rails: Smart Routing & Minting

In my next post, I'll reveal how.

2

37

Jan 11

We built a cross chain swap API which allows businesses to accept any stable in (across chains) and the business receives their desired one (or we issue a custom stable for them).

Cross chain deposits are tough, but super needed.

Just build on @xentfi, problem solved.

39

Angus || XentFi retweeted

8 Dec 2025

JUST IN: JPMorgan CEO Jamie Dimon says stablecoins should work better for international payments.

536

522

5,309

331,480

9 Dec 2025

Banks: deposits are better than stablecoins because they pay 0.1% interest

Stablecoins: we can pay more than that

Banks: no you can't

Stablecoins: why not

8 Dec 2025

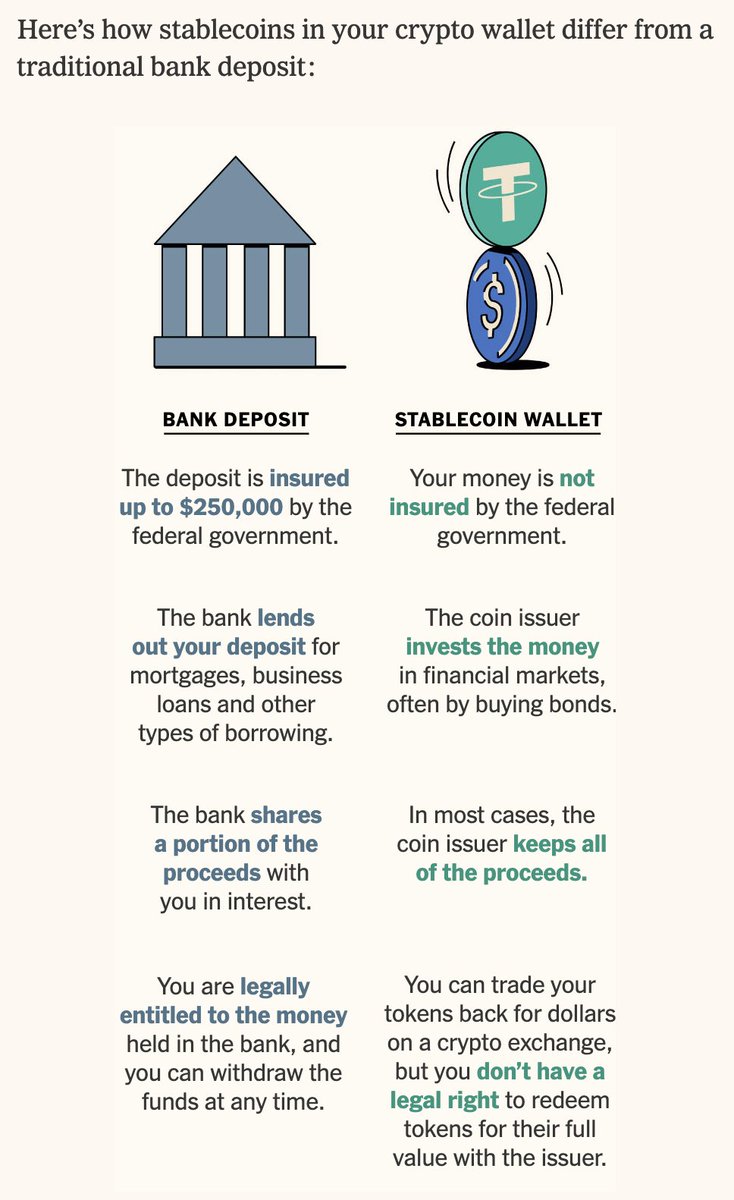

Putting aside the gross misrepresentation here of the regulatory requirement to hold cash and cashlike assets (short-term US govt debt, among the safest and most liquid assets out there) as "invest[ing] the money in financial markets, often by buying bonds" --

I find it the height of irony that the NYT says that bank deposits are better than stablecoins because they share *some* (~.01%) interest with depositors, and yet any argument that, perhaps, stablecoin issuers should be permitted to pass on interest to tokenholders is taboo. Can't have it both ways here guys.

25